Review of Derivatives Research ( IF 0.786 ) Pub Date : 2022-06-21 , DOI: 10.1007/s11147-022-09187-x Pakorn Aschakulporn , Jin E. Zhang

|

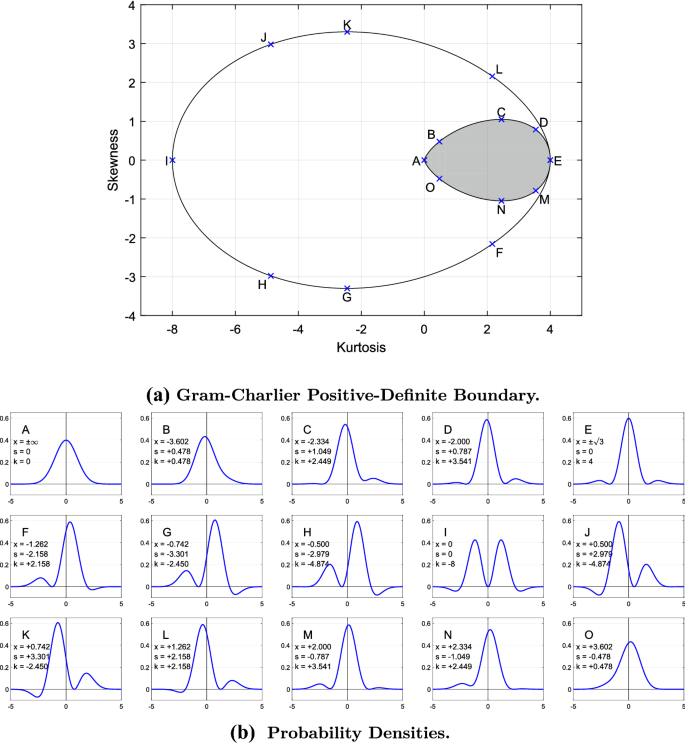

This paper is a sequel to Aschakulporn and Zhang (J Futures Mark 42(3):365–388, 2022). The errors of the Bakshi et al. (Rev Financ Stud 16(1):101–143, 2003) risk-neutral moment estimators is studied using the Gram–Charlier density—with the skewness and excess kurtosis specified. To obtain skewness with (absolute) errors less than \(10^{-3}\), the range of strikes (\(K_{\min }, K_{\max }\)) must contain at least 3/4 to 4/3 of the forward price and have a step size (\(\Delta K\)) of no more than 0.1% of the forward price. The range of strikes and step size corresponds to truncation and discretization errors, respectively. This is consistent to Aschakulporn and Zhang (2022) for non-volatile market periods.

中文翻译:

Bakshi、Kapadia 和 Madan (2003) 风险中性矩估计量:Gram-Charlier 密度方法

本文是 Aschakulporn 和 Zhang (J Futures Mark 42(3):365–388, 2022) 的续集。Bakshi 等人的错误。(Rev Financ Stud 16(1):101–143, 2003) 使用 Gram-Charlier 密度研究风险中性矩估计量,并指定偏度和过度峰态。要获得(绝对)误差小于\(10^{-3}\)的偏度,罢工范围(\(K_{\min }, K_{\max }\))必须至少包含 3/4 到远期价格的 4/3,步长 ( \(\Delta K\) ) 不超过远期价格的 0.1%。罢工的范围和步长分别对应于截断和离散化误差。这与 Aschakulporn 和 Zhang (2022) 的非波动市场时期一致。

京公网安备 11010802027423号

京公网安备 11010802027423号