当前位置:

X-MOL 学术

›

Rev. Deriv. Res.

›

论文详情

Our official English website, www.x-mol.net, welcomes your feedback! (Note: you will need to create a separate account there.)

CMS spread options in quadratic Gaussian model

Review of Derivatives Research ( IF 0.786 ) Pub Date : 2022-09-10 , DOI: 10.1007/s11147-022-09188-w Parviz Rakhmonov , Firuz Rakhmonov

中文翻译:

二次高斯模型中的 CMS 传播选项

更新日期:2022-09-11

Review of Derivatives Research ( IF 0.786 ) Pub Date : 2022-09-10 , DOI: 10.1007/s11147-022-09188-w Parviz Rakhmonov , Firuz Rakhmonov

|

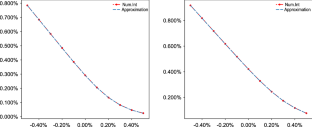

In this paper we present a closed-form approximation for analytic pricing of CMS spread options in multifactor Quadratic Gaussian model. We benchmark prices calculated using closed-form approximation to the one calculated via numerical integration and demonstrate that approximation errors are very small. We also demonstrate that resulting pricing formulae are easy to implement, therefore should be particularly useful in calibration of multifactor Quadratic Gaussian model to CMS spread option prices.

中文翻译:

二次高斯模型中的 CMS 传播选项

在本文中,我们提出了多因素二次高斯模型中 CMS 价差期权分析定价的封闭式近似。我们将使用封闭式近似计算的价格与通过数值积分计算的价格进行基准比较,并证明近似误差非常小。我们还证明了由此产生的定价公式很容易实现,因此在校准多因素二次高斯模型到 CMS 价差期权价格时应该特别有用。

京公网安备 11010802027423号

京公网安备 11010802027423号