Review of Derivatives Research ( IF 0.786 ) Pub Date : 2022-09-18 , DOI: 10.1007/s11147-022-09189-9 Matthias Muck

|

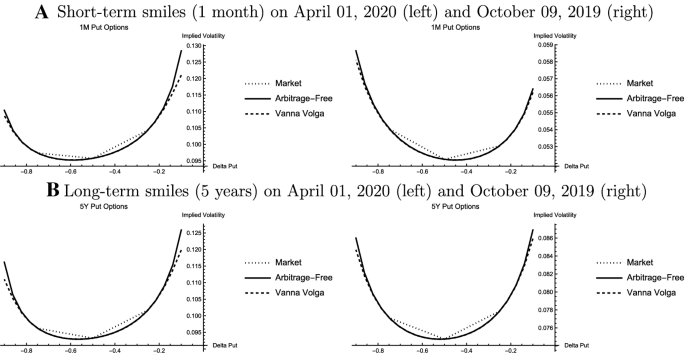

This paper addresses arbitrage-free FX smile construction from near-term implied volatility dynamics proposed by Carr (J Financ Econ, 120(1), 1–20, 2016). The approach is directly applicable to FX option market conventions. Prices of market benchmark contracts (risk reversals and butterflies) are identified as the roots of a cubic polynomial and ATM-volatility can be matched by construction. Implied volatilities are computed with respect to (non-premium adjusted) option deltas. The approach is compared to the Vanna Volga Approach, which does not guarantee arbitrage-free prices. An empirical application to a normal and a stress scenario demonstrates that arbitrage-free implied volatilities coincide with those from the Vanna Volga Approach when prices are interpolated between the \(\Delta\)25-call and \(\Delta\)25-put options. Differences are observed when implied volatilities are extrapolated to the wings. Empirically, these differences are particularly relevant in a stress scenario during the Coronavirus crises (2020).

中文翻译:

使用 Garman-Kohlhagen delta 和隐含波动率在外汇期权市场上构建无套利微笑微笑

本文从 Carr (J Financ Econ, 120(1), 1-20, 2016) 提出的近期隐含波动率动态中探讨了无套利外汇微笑构造。该方法直接适用于外汇期权市场惯例。市场基准合约(风险逆转和蝴蝶)的价格被确定为三次多项式的根,并且 ATM 波动率可以通过构造来匹配。隐含波动率是根据(非溢价调整的)期权增量计算的。该方法与不保证无套利价格的万纳伏尔加方法相比较。对正常和压力情景的实证应用表明,当价格在\(\Delta\) 25 看涨期权和\(\Delta\) 25-看跌期权。当隐含波动率外推到机翼时,可以观察到差异。根据经验,这些差异在冠状病毒危机(2020 年)期间的压力情景中尤为重要。

京公网安备 11010802027423号

京公网安备 11010802027423号