Review of Derivatives Research ( IF 0.786 ) Pub Date : 2022-09-18 , DOI: 10.1007/s11147-022-09190-2 Philip Stahl

|

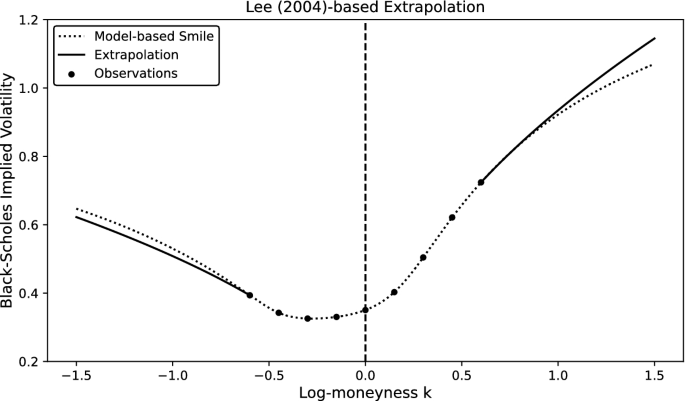

We show that the VIX Index structurally underestimates model-free implied volatility because its implementation omits extrapolation of the volatility smile in the tails. We use the asymptotic behavior of the volatility surface to construct a correction term that is model-independent and only requires option prices at the two outermost strikes. We show how to apply this correction to the VIX Index ex-post as well as how to modify its implementation accordingly. Furthermore, we show that the degree of underestimation varies over time. For the S&P 500 Index and the DJIA Index the error is larger in periods of sustained low volatility. This cannot be observed for the Volatility-of-VIX Index.

中文翻译:

无模型隐含方差的渐近外推:探索 VIX 指数中的结构性低估

我们表明,VIX 指数在结构上低估了无模型隐含波动率,因为它的实施忽略了尾部波动率微笑的外推。我们使用波动率表面的渐近行为来构建一个与模型无关的修正项,并且只需要两个最外层行使价的期权价格。我们展示了如何事后将此修正应用于 VIX 指数,以及如何相应地修改其实施。此外,我们表明低估程度随时间而变化。对于标准普尔 500 指数和 DJIA 指数,在持续低波动期间误差更大。VIX 波动率指数无法观察到这一点。

京公网安备 11010802027423号

京公网安备 11010802027423号