European Actuarial Journal Pub Date : 2022-11-10 , DOI: 10.1007/s13385-022-00325-1 Lucas Reck , Johannes Schupp , Andreas Reuß

|

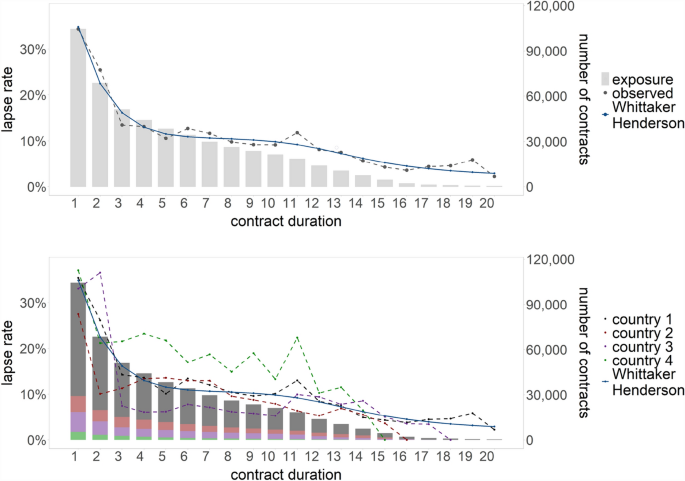

Lapse risk is a key risk driver for life and pensions business with a material impact on the cash flow profile and the profitability. The application of data science methods can replace the largely manual and time-consuming process of estimating a lapse model that reflects various contract characteristics and provides best estimate lapse rates, as needed for Solvency II valuations. In this paper, we use the Lasso method which is based on a multivariate model and can identify patterns in the data set automatically. To identify hidden structures within covariates, we adapt and combine recently developed extended versions of the Lasso that apply different sub-penalties for individual covariates. In contrast to random forests or neural networks, the predictions of our lapse model remain fully explainable, and the coefficients can be used to interpret the lapse rate on an individual contract level. The advantages of the method are illustrated based on data from a European life insurer operating in four countries. We show how structures can be identified efficiently and fed into a highly competitive, automatically calibrated lapse model.

中文翻译:

确定人寿保险失效率的决定因素:一种自动化的 Lasso 方法

失效风险是人寿和养老金业务的主要风险驱动因素,对现金流状况和盈利能力产生重大影响。根据 Solvency II 估值的需要,数据科学方法的应用可以取代大部分人工和耗时的估计失效模型的过程,该模型反映了各种合同特征并提供最佳估计失效率。在本文中,我们使用基于多元模型的 Lasso 方法,可以自动识别数据集中的模式。为了识别协变量中的隐藏结构,我们调整并结合了最近开发的 Lasso 扩展版本,该版本对各个协变量应用不同的子惩罚。与随机森林或神经网络相比,我们的失效模型的预测仍然完全可以解释,并且这些系数可用于解释单个合同级别的失效率。该方法的优势基于在四个国家运营的欧洲人寿保险公司的数据进行了说明。我们展示了如何有效地识别结构并将其输入到极具竞争力的自动校准失效模型中。

京公网安备 11010802027423号

京公网安备 11010802027423号