Annals of Finance Pub Date : 2023-02-05 , DOI: 10.1007/s10436-023-00424-3 Dilip B. Madan , King Wang

|

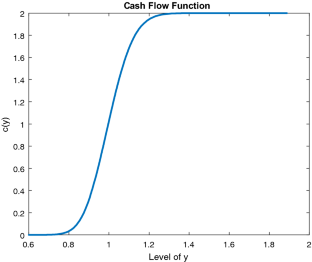

Corporations are modeled as owning a perpetual derivative security that has a claim on future cash flows. The cash flows are defined by deterministic functions of state variables. In a time homogeneous and Markovian context the value of a corporation is then given by a deterministic function of the state variables termed the corporate valuation function. This valuation function solves an integro differential equation with a boundary condition of zero at infinity. Solutions are illustrated in dimensions one, two and ten. It is observed that for positive and bounded cash flow functions the valuation functions cannot be linear. The attitude of a corporation to risk then depends on the nonlinearity. In higher dimensions the corporation will be a risk taker in some directions and simultaneously a risk avoider in others. The valuation theory also leads to new asset pricing equations inferring asset variations from risk neutral covariations. The shift from mean returns and covariances is necessitated by the focus on instantaneous risk exposures represented by measures replacing probabilities.

中文翻译:

公司估值:衍生品定价视角

公司被建模为拥有对未来现金流有索取权的永久衍生证券。现金流由状态变量的确定性函数定义。在时间同质和马尔可夫语境中,公司的价值由状态变量的确定性函数给出,称为公司估值函数。该估值函数求解边界条件为零的积分微分方程。解决方案在维度一、二和十中进行了说明。据观察,对于正的和有界的现金流量函数,估值函数不能是线性的。公司对风险的态度取决于非线性。在更高的维度上,公司将在某些方面成为风险承担者,同时在其他方面成为风险规避者。估值理论还导致新的资产定价方程从风险中性协变推断资产变化。对以替代概率的度量为代表的瞬时风险敞口的关注需要从平均回报和协方差的转变。

京公网安备 11010802027423号

京公网安备 11010802027423号