Journal of Commodity Markets ( IF 3.317 ) Pub Date : 2023-03-04 , DOI: 10.1016/j.jcomm.2023.100323 Jinxin Cui , Aktham Maghyereh

|

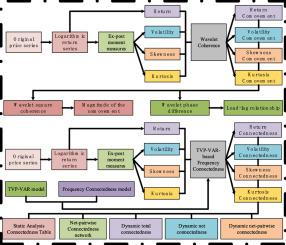

Investigating the dependence and connectedness among global oil markets is of great significance for cross-market investors and regulators. However, most of the existing studies are confined to lower-order moments and the time domain. This paper is the first to examine the time-frequency dependence and connectedness among global oil markets from the higher-order moment perspective by applying the wavelet coherence method and the newly proposed time-varying parameter vector autoregression-based frequency connectedness approach. The empirical results demonstrate that higher-order moment dependence among oil markets is weaker than return and volatility dependence. In general, Dubai, Minas, and Tapis oil exhibit relatively higher wavelet coherence with Daqing oil at all moments. The lead-lag relationships are heterogeneous during most sample intervals. The total return and volatility connectedness indices are higher than the skewness and kurtosis. The return connectedness mainly occurs in the short term (1–5 days) whereas the volatility, skewness, and kurtosis connectedness occur in the long run (22-Inf days). West Texas Intermediate oil dominates the return, volatility, and skewness connectedness network while Dubai oil dominates the kurtosis connectedness network. Furthermore, the dynamic total, net, and net-pairwise connectedness indices are all time-varying and event-dependent with the higher-order moment connectedness illustrating more volatile features. Several practical implications are provided for various market agents.

中文翻译:

全球石油市场之间的时频依赖性和连通性:来自高阶矩视角的新证据

研究全球石油市场之间的依赖性和关联性对于跨市场投资者和监管机构具有重要意义。然而,大多数现有研究仅限于低阶矩和时域。本文首次通过应用小波相干方法和新提出的基于时变参数向量自回归的频率连通性方法,从高阶矩的角度考察了全球石油市场之间的时频依赖性和连通性。实证结果表明,石油市场之间的高阶矩依赖性弱于回报和波动性依赖性。总的来说,迪拜、米纳斯和塔皮斯油与大庆油在任何时刻都表现出较高的小波相干性。在大多数样本间隔期间,超前-滞后关系是异质的。总回报率和波动率连通性指数高于偏度和峰度。回报连通性主要发生在短期(1-5 天),而波动性、偏度和峰态连通性发生在长期(22-Inf 天)。西德克萨斯中质油主导收益、波动性和偏度连通性网络,而迪拜石油主导峰度连通性网络。此外,动态总连通性、净连通性和净成对连通性指数都是随时间变化和事件相关的,高阶矩连通性说明了更易变的特征。为各种市场代理人提供了一些实际意义。回报连通性主要发生在短期(1-5 天),而波动性、偏度和峰态连通性发生在长期(22-Inf 天)。西德克萨斯中质油主导收益、波动性和偏度连通性网络,而迪拜石油主导峰度连通性网络。此外,动态总连通性、净连通性和净成对连通性指数都是随时间变化和事件相关的,高阶矩连通性说明了更易变的特征。为各种市场代理人提供了一些实际意义。回报连通性主要发生在短期(1-5 天),而波动性、偏度和峰态连通性发生在长期(22-Inf 天)。西德克萨斯中质油主导收益、波动性和偏度连通性网络,而迪拜石油主导峰度连通性网络。此外,动态总连通性、净连通性和净成对连通性指数都是随时间变化和事件相关的,高阶矩连通性说明了更易变的特征。为各种市场代理人提供了一些实际意义。动态总连通性、净连通性和净成对连通性指数都是随时间变化和事件相关的,高阶矩连通性说明了更易变的特征。为各种市场代理人提供了一些实际意义。动态总连通性、净连通性和净成对连通性指数都是随时间变化和事件相关的,高阶矩连通性说明了更易变的特征。为各种市场代理人提供了一些实际意义。

京公网安备 11010802027423号

京公网安备 11010802027423号