International Advances in Economic Research Pub Date : 2023-03-20 , DOI: 10.1007/s11294-023-09867-w Evaggelia Siopi , Thomas Poufinas , James Ming Chen , Charalampos Agiropoulos

|

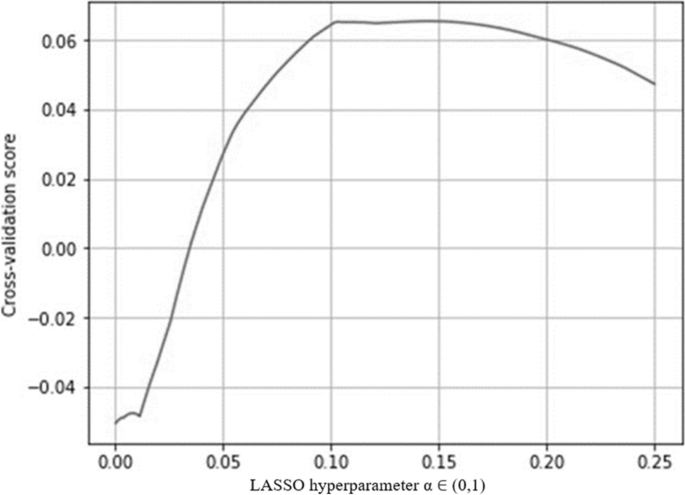

Successive crises in the early twenty-first century prompted regulators around the world to ask financial institutions to implement a series of regulations. These measures aimed to increase transparency, improve consumer and investor protection, restructure financial capital, stabilize insurance and pension markets, and improve solvency. The Solvency II framework introduced in the European Union applied these principles to insurance companies. This study attempts to predict the solvency of an insurer within a set of European insurers. The dataset consists of 29 insurance groups that operate across the European Union with a country of origin within the European Union for the period 2016 to 2020. The variables were constructed from annual financial statements retrieved from (Thomson Reuters) DataStream. The solvency capital requirement ratios were obtained manually from the solvency financial condition reports of each group. Regularized linear regression applying a ℓ1/ least-absolute-shrinkage-and-selection-operator penalty showed that the reinvestment rate, cash and equivalents, long term investment, and losses-benefits-and-adjustments expenses have the greatest predictive impact on the solvency of insurers. The contribution of this paper lies in the identification of determinants that allow insurance companies to maintain strong solvency capital requirement ratios so that they can maintain internal operations with minimal interruption.

中文翻译:

监管会影响保险公司的偿付能力吗?来自欧洲保险公司的新证据

二十世纪初接连不断的危机促使世界各地的监管机构要求金融机构实施一系列监管。这些措施旨在提高透明度,改善消费者和投资者保护,重组金融资本,稳定保险和养老金市场,并提高偿付能力。欧盟引入的 Solvency II 框架将这些原则应用于保险公司。本研究试图预测一组欧洲保险公司中一家保险公司的偿付能力。该数据集由 29 个保险集团组成,这些集团在 2016 年至 2020 年期间在欧盟范围内运营,原产国位于欧盟境内。变量是根据从 (Thomson Reuters) DataStream 检索的年度财务报表构建的。偿付能力资本要求比率是从每个组的偿付能力财务状况报告中手动获得的。应用 ℓ 的正则化线性回归1 / least-absolute-shrinkage-and-selection-operator penalty 表明,再投资率、现金和等价物、长期投资、损失收益和调整费用对保险公司的偿付能力具有最大的预测影响。本文的贡献在于确定了使保险公司能够保持强大的偿付能力资本要求比率的决定因素,以便他们能够以最少的干扰维持内部运营。

京公网安备 11010802027423号

京公网安备 11010802027423号