Finance and Stochastics ( IF 1.7 ) Pub Date : 2023-03-29 , DOI: 10.1007/s00780-023-00502-4 Sarah Bensalem , Nicolás Hernández-Santibáñez , Nabil Kazi-Tani

|

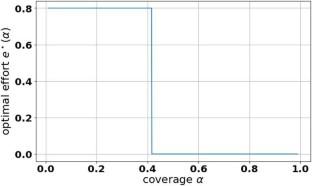

This paper deals with an optimal linear insurance demand model, where the protection buyer can also exert a time-dynamic costly prevention effort to reduce her risk exposure. This is expressed as a stochastic control problem that consists in maximising an exponential utility of a terminal wealth. We assume that the effort reduces the intensity of the jump arrival process and interpret this as dynamic self-protection. We solve the problem by using a dynamic programming approach, and we provide a representation of the certainty equivalent of the buyer as the solution to a backward stochastic differential equation (BSDE). Using this representation, we prove that an exponential utility maximiser has an incentive to modify her effort dynamically only in the presence of a terminal reimbursement in the contract. Otherwise, the dynamic effort is actually constant, for a class of compound Poisson loss processes. If there is no terminal reimbursement, we solve the problem explicitly and identify the dynamic certainty equivalent of the protection buyer. This shows in particular that the Lévy property of the loss process is preserved under exponential utility maximisation. We also characterise the constant effort as the unique minimiser of an explicit Hamiltonian, from which we can determine the optimal effort in particular cases. Finally, after studying the dependence of the BSDE associated to the insurance buyer on the linear insurance contract parameter, we prove the existence of an optimal linear cover that is not necessarily zero or full insurance.

中文翻译:

自我保护的连续时间模型

本文讨论了一个最优线性保险需求模型,其中保护购买者还可以施加时间动态的代价高昂的预防努力来减少她的风险敞口。这表示为一个随机控制问题,该问题在于最大化最终财富的指数效用。我们假设这种努力降低了跳跃到达过程的强度,并将其解释为动态自我保护。我们通过使用动态规划方法解决了这个问题,并且我们提供了买方的确定性等价表示作为向后随机微分方程 (BSDE) 的解。使用这种表示,我们证明了指数效用最大化者只有在合同中存在终端补偿的情况下才有动力动态修改她的努力。否则,对于一类复合泊松损失过程,动态努力实际上是恒定的。如果没有终端报销,我们明确解决问题并确定保护买方的动态确定性等价物。这特别表明损失过程的 Lévy 属性在指数效用最大化下得以保留。我们还将不断的努力描述为显式哈密顿量的唯一最小化器,我们可以从中确定特定情况下的最佳努力。最后,在研究了与保险购买者相关的 BSDE 对线性保险合同参数的依赖性之后,我们证明了不一定是零保险或全保险的最优线性保险的存在性。我们明确地解决了这个问题,并确定了保护买方的动态确定性等价物。这特别表明损失过程的 Lévy 属性在指数效用最大化下得以保留。我们还将不断的努力描述为显式哈密顿量的唯一最小化器,我们可以从中确定特定情况下的最佳努力。最后,在研究了与保险购买者相关的 BSDE 对线性保险合同参数的依赖性之后,我们证明了不一定是零保险或全保险的最优线性保险的存在性。我们明确地解决了这个问题,并确定了保护买方的动态确定性等价物。这特别表明损失过程的 Lévy 属性在指数效用最大化下得以保留。我们还将不断的努力描述为显式哈密顿量的唯一最小化器,我们可以从中确定特定情况下的最佳努力。最后,在研究了与保险购买者相关的 BSDE 对线性保险合同参数的依赖性之后,我们证明了不一定是零保险或全保险的最优线性保险的存在性。我们还将不断的努力描述为显式哈密顿量的唯一最小化器,我们可以从中确定特定情况下的最佳努力。最后,在研究了与保险购买者相关的 BSDE 对线性保险合同参数的依赖性之后,我们证明了不一定是零保险或全保险的最优线性保险的存在性。我们还将不断的努力描述为显式哈密顿量的唯一最小化器,我们可以从中确定特定情况下的最佳努力。最后,在研究了与保险购买者相关的 BSDE 对线性保险合同参数的依赖性之后,我们证明了不一定是零保险或全保险的最优线性保险的存在性。

京公网安备 11010802027423号

京公网安备 11010802027423号