Advances in Difference Equations ( IF 4.1 ) Pub Date : 2023-05-18 , DOI: 10.1186/s13662-023-03772-6 Gaofeng Zong

|

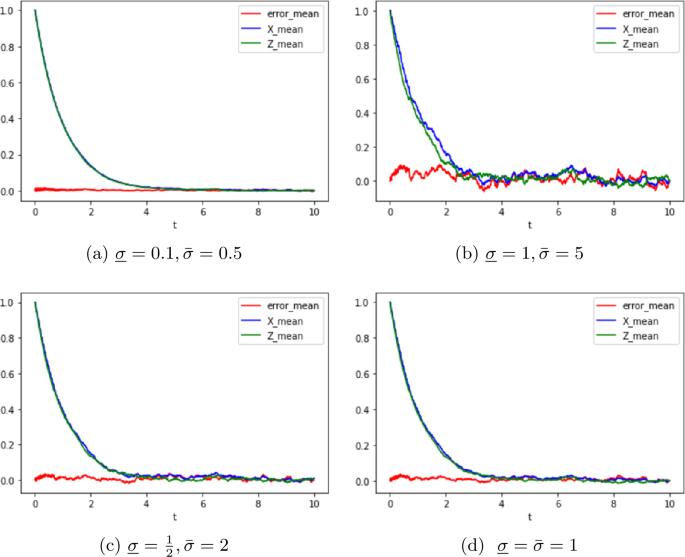

In this paper, we tame the uncertainty about the volatility in time-averaging principle for stochastic differential equations driven by G-Brownian motion (G-SDEs) based on the Lyapunov condition. That means we treat the time-averaging principle for stochastic differential equations based on the Lyapunov condition in the presence of a family of probability measures, each corresponding to a different scenario for the volatility. The main tool for the mathematical analysis is the G-stochastic calculus, which is introduced in the book by Peng (Nonlinear Expectations and Stochastic Calculus Under Uncertainty. Springer, Berlin, 2019). We show that the solution of a standard equation converges to the solution of the corresponding averaging equation in the sense of sublinear expectation with the help of some properties of G-stochastic calculus. Numerical results obtained using PYTHON illustrate the efficiency of the averaging method.

中文翻译:

基于李雅普诺夫条件的 G-SDE 时间平均原理

在本文中,我们驯服了基于李雅普诺夫条件的 G-布朗运动 (G-SDE) 驱动的随机微分方程的时间平均原理中波动性的不确定性。这意味着我们在存在一系列概率测度的情况下,基于 Lyapunov 条件处理随机微分方程的时间平均原理,每个测度对应于波动率的不同场景。数学分析的主要工具是 G-stochastic calculus,它在 Peng 的书中介绍(Nonlinear Expectations and Stochastic Calculus Under Uncertainty. Springer, Berlin, 2019)。借助 G-随机微积分的某些性质,我们证明了标准方程的解在次线性期望意义上收敛于相应平均方程的解。

京公网安备 11010802027423号

京公网安备 11010802027423号