Applied Mathematics and Optimization ( IF 1.8 ) Pub Date : 2023-08-11 , DOI: 10.1007/s00245-023-10037-x Christian Dehm , Thai Nguyen , Mitja Stadje

|

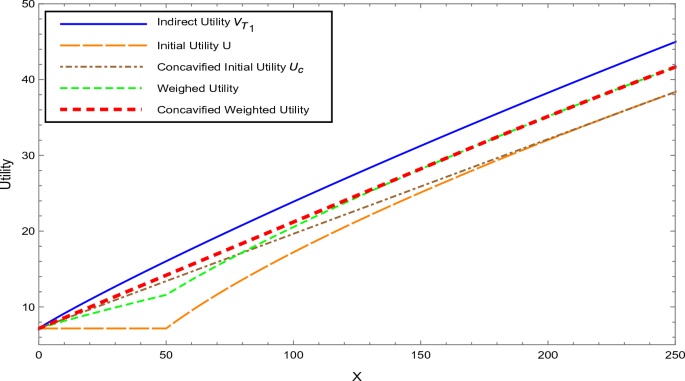

We consider an expected utility maximization problem where the utility function is not necessarily concave and the time horizon is uncertain. We establish a necessary and sufficient condition for the optimality for general non-concave utility function in a complete financial market. We show that the general concavification approach of the utility function to deal with non-concavity, while being still applicable when the time horizon is a stopping time with respect to the financial market filtration, leads to sub-optimality when the time horizon is independent of the financial risk, and hence can not be directly applied. For the latter case, we suggest a recursive procedure which is based on the dynamic programming principle. We illustrate our findings by carrying out a multi-period numerical analysis for optimal investment problem under a convex option compensation scheme with random time horizon. We observe that the distribution of the non-concave portfolio in both certain and uncertain random time horizon is right-skewed with a long right tail, indicating that the investor expects frequent small losses and a few large gains from the investment. While the (certain) average time horizon portfolio at a premature stopping date is unimodal, the random time horizon portfolio is multimodal distributed which provides the investor a certain flexibility of switching between the local maximizers, depending on the market performance. The multimodal structure with multiple peaks of different heights can be explained by the concavification procedure, whereas the distribution of the time horizon has significant impact on the amplitude between the modes.

中文翻译:

时间范围不确定的非凹预期效用优化

我们考虑一个预期效用最大化问题,其中效用函数不一定是凹的并且时间范围是不确定的。我们建立了完整金融市场中一般非凹效用函数最优的充要条件。我们表明,处理非凹性的效用函数的一般凹化方法虽然在时间范围是金融市场过滤的停止时间时仍然适用,但当时间范围独立于财务风险较大,不能直接应用。对于后一种情况,我们建议采用基于动态规划原理的递归过程。我们通过对随机时间范围的凸期权补偿方案下的最优投资问题进行多周期数值分析来说明我们的发现。我们观察到,非凹投资组合在确定和不确定的随机时间范围内的分布都是右偏的,具有长的右尾,表明投资者期望从投资中频繁获得小额损失和少量大额收益。虽然提前停止日期的(某些)平均时间范围投资组合是单峰的,但随机时间范围投资组合是多峰分布的,这为投资者提供了根据市场表现在局部最大化之间切换的一定灵活性。具有不同高度的多个峰的多峰结构可以通过凹化过程来解释,

京公网安备 11010802027423号

京公网安备 11010802027423号