Statistical Methods & Applications ( IF 1 ) Pub Date : 2023-09-28 , DOI: 10.1007/s10260-023-00724-y Paolo Pagnottoni , Alessandro Spelta

|

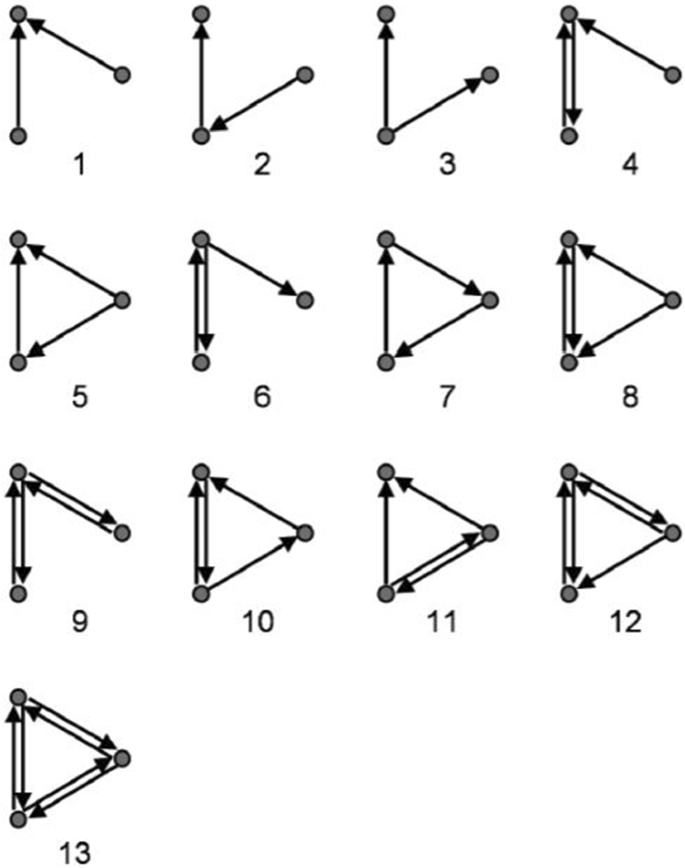

We propose a method for characterizing the local structure of weighted multivariate time series networks. We draw intensity and coherence of network motifs, i.e. statistically recurrent subgraphs, to characterize the system behavior via higher-order structures derived upon effective transfer entropy networks. The latter consists of a model-free methodology enabling to correct for small sample biases affecting Shannon transfer entropy, other than conducting inference on the estimated directional time series information flows. We demonstrate the usefulness of our proposed method with an application to a set of global commodity prices. Our main result shows that, despite simple triadic structures are the most intense, coherent and statistically recurrent over time, their intensity suddenly decreases after the Global Financial Crisis, in favor of most complex triadic structures, while all types of subgraphs tend to become more coherent thereafter.

中文翻译:

经过统计验证的信息流时间网络的一致性和强度

我们提出了一种表征加权多元时间序列网络局部结构的方法。我们绘制网络主题的强度和连贯性,即统计上的循环子图,以通过有效转移熵网络派生的高阶结构来表征系统行为。后者包含一种无模型方法,能够纠正影响香农传递熵的小样本偏差,而不是对估计的方向时间序列信息流进行推断。我们通过应用于一组全球商品价格来证明我们提出的方法的实用性。我们的主要结果表明,尽管简单的三元结构随着时间的推移是最强烈、最连贯和统计上最重复的,但它们的强度在全球金融危机后突然下降,

京公网安备 11010802027423号

京公网安备 11010802027423号