Statistical Papers ( IF 1.3 ) Pub Date : 2023-11-16 , DOI: 10.1007/s00362-023-01495-0 Stergios B. Fotopoulos , Abhishek Kaul , Vasileios Pavlopoulos , Venkata K. Jandhyala

|

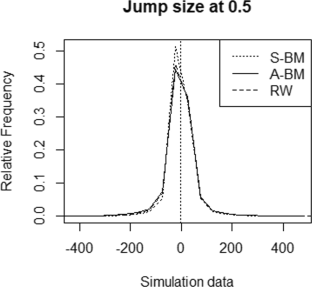

The article offers a method for estimating the volatility covariance matrix of vectors of financial time series data using a change point approach. The proposed method supersedes general varying-coefficient parametric models, such as GARCH, whose coefficients may vary with time, by a change point model. In this study, an adaptive pointwise selection of homogeneous segments with a given right-end point by a local change point analysis is introduced. Sufficient conditions are obtained under which the maximum likelihood process is adaptive against the covariance estimate to yield an optimal rate of convergence with respect to the change size. This rate is preserved while allowing the jump size to diminish. Under these circumstances, argmax results of a two-sided negative Brownian motion or a two-sided negative drift random walk under vanishing and non-vanishing jump size regimes, respectively, provide inference for the change point parameter. Theoretical results are supported by the Monte–Carlo simulation study. A bivariate data on daily log returns of two US stock market indices as well as tri-variate data on daily log returns of three banks are analyzed by constructing confidence interval estimates for multiple change points that have been identified previously for each of the two data sets.

中文翻译:

协方差结构变化下的自适应参数变点推断

本文提供了一种使用变点方法来估计金融时间序列数据向量的波动率协方差矩阵的方法。所提出的方法通过变点模型取代了一般的变系数参数模型,例如 GARCH,其系数可能随时间变化。在本研究中,引入了通过局部变化点分析对具有给定右端点的同质段进行自适应逐点选择。获得了最大似然过程自适应于协方差估计的充分条件,以产生相对于变化大小的最佳收敛率。该速率得以保留,同时允许跳跃大小减小。在这些情况下,两侧负布朗运动或两侧负漂移随机游走在消失和非消失跳跃大小状态下的 argmax 结果分别为变化点参数提供了推断。理论结果得到蒙特卡罗模拟研究的支持。通过为两个数据集中的每一个先前确定的多个变化点构建置信区间估计,分析两个美国股票市场指数的日对数回报的双变量数据以及三个银行的日对数回报的三变量数据。

京公网安备 11010802027423号

京公网安备 11010802027423号