Applied Mathematics and Optimization ( IF 1.8 ) Pub Date : 2023-12-05 , DOI: 10.1007/s00245-023-10079-1 Wenyuan Wang , Xiang Yu , Xiaowen Zhou

|

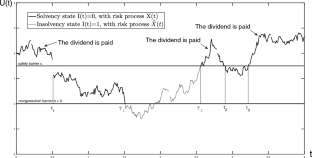

Motivated by recent developments in risk management based on the U.S. bankruptcy code, we revisit the De Finetti’s optimal dividend problem by incorporating the reorganization process and regulator’s intervention documented in Chapter 11 bankruptcy. The resulting surplus process, bearing financial stress towards the more subtle concept of bankruptcy, corresponds to a non-standard spectrally negative Lévy process with endogenous regime switching. Some explicit expressions of the expected present values under a barrier strategy, new to the literature, are established in terms of scale functions. With the help of these expressions, when the tail of the Lévy measure is log-convex, the optimal dividend control is shown to be of the barrier type and the associated optimal barrier can be identified using scale functions of spectrally negative Lévy processes. Some financial implications are also discussed in an illustrative example.

中文翻译:

内生制度转换下障碍股利控制的最优性及其在第十一章破产法中的应用

受基于美国破产法的风险管理最新发展的推动,我们通过结合第 11 章破产法中记录的重组过程和监管机构干预,重新审视 De Finetti 的最优股息问题。由此产生的盈余过程,对更微妙的破产概念带来财务压力,对应于具有内生政权转换的非标准光谱负利维过程。障碍策略下预期现值的一些明确表达是根据尺度函数建立的,这对于文献来说是新的。借助这些表达式,当 Lévy 测度的尾部为对数凸时,最优股息控制被证明是障碍类型,并且可以使用谱负 Lévy 过程的尺度函数来识别相关的最优障碍。一些财务影响也在说明性示例中进行了讨论。

京公网安备 11010802027423号

京公网安备 11010802027423号