International Journal of Disclosure and Governance Pub Date : 2023-12-22 , DOI: 10.1057/s41310-023-00221-4 Zunaiba Abdulrahman , Tahera Ebrahimi , Basil Al-Najjar

|

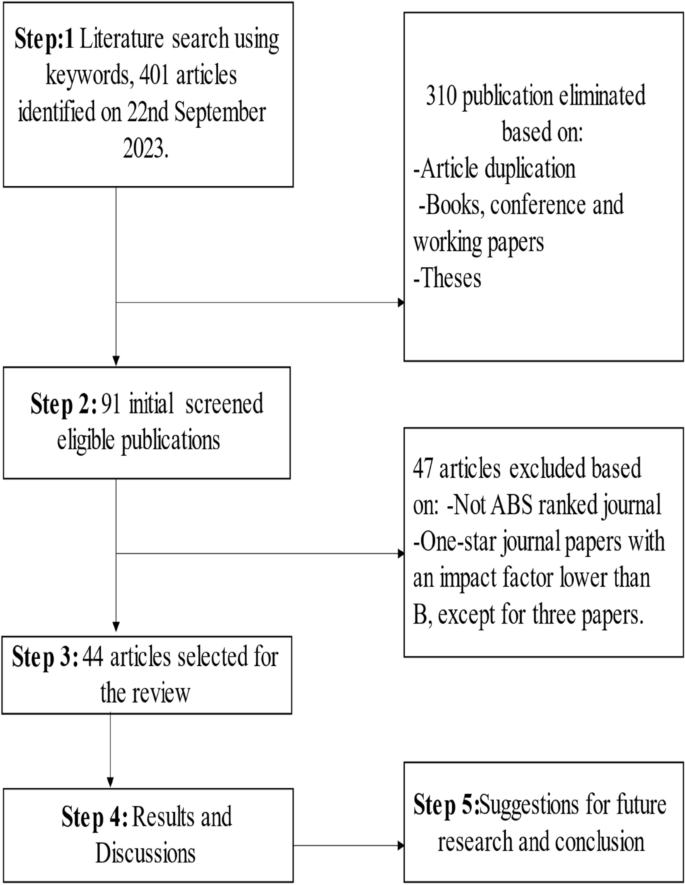

A substantial scholarly discourse surrounds Shariah legislation, yet previous studies have offered limited evidence regarding the necessity of Shariah-related disclosure (SRD), its extent, determining factors, and its impact on performance. This paper seeks to provide a comprehensive review of existing SRD literature within Islamic institutions. To achieve this, we conducted a systematic literature review encompassing 44 studies published in journals from 2003 to 2023. The research articles were systematically categorized based on types of SRD, levels, methodologies employed, determining factors, and their consequent effects on performance. The findings underscore a significant knowledge gap and inconclusive results in the current literature, thereby identifying avenues for future research. Notably, our results indicate that the majority of prior studies are quantitative in nature and have employed secondary data from Islamic banks in Muslim countries. Likewise, research pertaining to other Islamic institutions and their voluntary adherence to Accounting and Auditing Organization for Islamic Financial Institutions guidelines is underreported. Furthermore, our findings suggest that previous studies have often placed undue emphasis on other forms of disclosure or have only considered SRD as a subset of broader categories. Contrarily, the number of studies on this subject has increased in recent years, with more than half of the surveys conducted in the last 8 years of the sample period. In forthcoming research, it is advisable to independently explore SRD and employ Islamic proxies to assess its impact on performance. Moreover, researchers are encouraged to investigate cross-industry differences in this context. The results of this survey will be of significant interest to both academics and non-academics seeking information on Shariah compliance disclosures.

中文翻译:

伊斯兰教法相关披露:文献综述和未来研究方向

学术界对伊斯兰教法立法进行了大量讨论,但之前的研究对于伊斯兰教法相关披露(SRD)的必要性、其范围、决定因素及其对绩效的影响提供的证据有限。本文旨在对伊斯兰机构内现有的 SRD 文献进行全面回顾。为了实现这一目标,我们对 2003 年至 2023 年在期刊上发表的 44 项研究进行了系统的文献综述。研究文章根据 SRD 的类型、水平、采用的方法、决定因素及其对绩效的影响进行系统分类。研究结果强调了当前文献中存在的重大知识差距和不确定的结果,从而确定了未来研究的途径。值得注意的是,我们的结果表明,大多数先前的研究本质上都是定量的,并且采用了来自穆斯林国家伊斯兰银行的二手数据。同样,有关其他伊斯兰机构及其自愿遵守伊斯兰金融机构会计和审计组织指南的研究也未得到充分报道。此外,我们的研究结果表明,以前的研究往往过分强调其他形式的披露,或者仅将 SRD 视为更广泛类别的子集。相反,近年来有关这一主题的研究数量有所增加,超过一半的调查是在样本期的最后 8 年进行的。在即将进行的研究中,建议独立探索 SRD 并使用伊斯兰代理来评估其对性能的影响。此外,鼓励研究人员调查这种背景下的跨行业差异。这项调查的结果将引起寻求伊斯兰教法合规性披露信息的学者和非学者的极大兴趣。

京公网安备 11010802027423号

京公网安备 11010802027423号