Review of Derivatives Research ( IF 0.786 ) Pub Date : 2024-01-19 , DOI: 10.1007/s11147-023-09200-x Philip Stahl , Jérôme Blauth

|

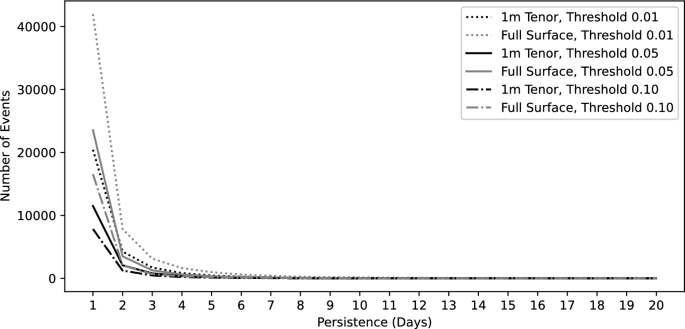

The martingale theory of bubbles enables testing for asset price bubbles by analyzing option prices. As recently shown by Piiroinen et al. (Asset price bubbles: an option-based indicator, 2018), the SABR model is a strict local martingale when its parameterization implies a positive correlation between stock and option prices. We operationalize this theoretical result and analyze stock price bubbles in 2576 stocks over 26 years. Martingale defect conditions are absorbed quickly by options markets, but identify high proportions in significant and permanent changes in distribution of price returns, option trading activity, short interest in the underlying, and institutional ownership. These results confirm many common assumptions about stock price bubbles. These bubbles are temporally clustered, and tend to occur in periods of positive market development. Martingale defects are rare in market corrections, which indicates that they are a result of overoptimistic speculation.

中文翻译:

波动率表面的鞅缺陷和底层的气泡条件

泡沫鞅理论可以通过分析期权价格来测试资产价格泡沫。正如 Piiroinen 等人最近所表明的。(资产价格泡沫:基于期权的指标,2018),当 SABR 模型的参数化意味着股票和期权价格之间存在正相关时,它是严格的局部鞅。我们将这一理论结果付诸实践,并分析了 26 年来 2576 只股票的股价泡沫。马丁格尔缺陷条件很快被期权市场吸收,但在价格回报分布、期权交易活动、标的物空头利息和机构所有权方面,识别出显着且永久性变化的比例很高。这些结果证实了许多关于股价泡沫的常见假设。这些泡沫在时间上是聚集的,并且往往发生在市场积极发展的时期。马丁格尔缺陷在市场调整中很少见,这表明它们是过度乐观投机的结果。

京公网安备 11010802027423号

京公网安备 11010802027423号