Networks and Spatial Economics ( IF 2.4 ) Pub Date : 2024-01-27 , DOI: 10.1007/s11067-024-09614-6 Yunquan Song , Minmin Zhan , Yue Zhang , Yongxin Liu

|

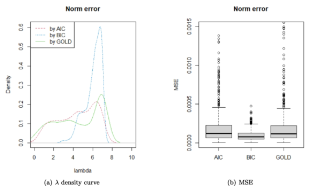

In recent times, the significance of variable selection has amplified because of the advent of high-dimensional data. The regularization method is a popular technique for variable selection and parameter estimation. However, spatial data is more intricate than ordinary data because of spatial correlation and non-stationarity. This article proposes a robust regularization regression estimator based on Huber loss and a generalized Lasso penalty to surmount these obstacles. Moreover, linear equality and inequality constraints are contemplated to boost the efficiency and accuracy of model estimation. To evaluate the suggested model’s performance, we formulate its Karush-Kuhn-Tucker (KKT) conditions, which are indicators used to assess the model’s characteristics and constraints, and establish a set of indicators, comprising the formula for the degrees of freedom. We employ these indicators to construct the AIC and BIC information criteria, which assist in choosing the optimal tuning parameters in numerical simulations. Using the classic Boston Housing dataset, we compare the suggested model’s performance with that of the model under squared loss in scenarios with and without anomalies. The outcomes demonstrate that the suggested model accomplishes robust variable selection. This investigation provides a novel approach for spatial data analysis with extensive applications in various fields, including economics, ecology, and medicine, and can facilitate the enhancement of the efficiency and accuracy of model estimation.

中文翻译:

Huber 损失满足空间自回归模型:一种具有先验信息的鲁棒变量选择方法

近年来,由于高维数据的出现,变量选择的重要性被放大。正则化方法是变量选择和参数估计的流行技术。然而,由于空间相关性和非平稳性,空间数据比普通数据更加复杂。本文提出了一种基于 Huber 损失和广义 Lasso 惩罚的鲁棒正则化回归估计器来克服这些障碍。此外,考虑线性等式和不等式约束来提高模型估计的效率和准确性。为了评估建议模型的性能,我们制定了其Karush-Kuhn-Tucker(KKT)条件,这些条件是用于评估模型特征和约束的指标,并建立了一组指标,其中包括自由度公式。我们利用这些指标来构建 AIC 和 BIC 信息标准,这有助于在数值模拟中选择最佳调整参数。使用经典的波士顿住房数据集,我们将建议模型的性能与平方损失下的模型在有异常和无异常的情况下的性能进行比较。结果表明,建议的模型实现了稳健的变量选择。这项研究为空间数据分析提供了一种新的方法,在经济学、生态学和医学等各个领域都有广泛的应用,有助于提高模型估计的效率和准确性。

京公网安备 11010802027423号

京公网安备 11010802027423号