Humanities & Social Sciences Communications ( IF 2.731 ) Pub Date : 2024-03-04 , DOI: 10.1057/s41599-024-02788-x Congxiao Chen , Wenya Chen , Li Shang , Haiqiao Wang , Decai Tang , David D. Lansana

|

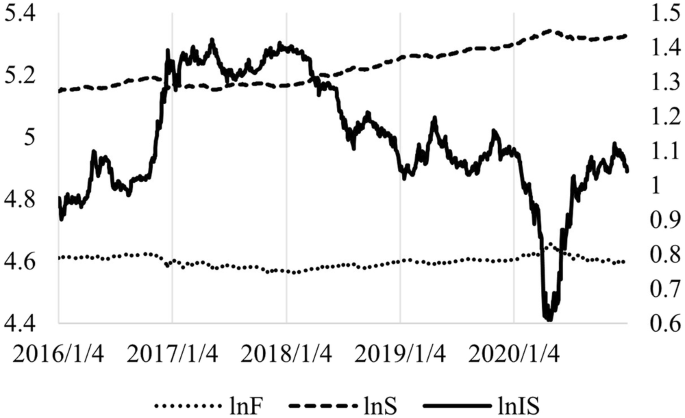

The interest rate derivatives market is an important force in promoting the development of the bond market and is an effective tool to manage interest rate risk. The research on price discovery and volatility spillover of the market can help provide valuable reference information for investors. Based on treasury bond futures and interest rate swaps, the paper aims to discuss the price discovery function and spillover structure of the interest rate derivatives market. The paper establishes the information share model and spillover index model for empirical analysis. The results show that: First, the calculation results of the information share model show that the price discovery of treasury bond futures and interest rate swap markets is stronger than that of the spot market. Second, based on structural break analysis, treasury bond futures and interest rate swaps do not have breakpoints, while the treasury bond spot has three breakpoints. The paper divides the entire sample into four stages based on structural breakpoints and finds that the price discovery ability of the interest rate derivative market dynamically changed. Third, as a net spillover in the market, treasury bond futures have developed relatively stable. Both treasury bond futures and interest rate swaps have spillover effects on the spot market, indicating that China’s interest rate derivatives market can impact the treasury bond spot market.

中文翻译:

利率衍生品市场的价格发现和波动溢出

利率衍生品市场是推动债券市场发展的重要力量,是管理利率风险的有效工具。对市场价格发现和波动溢出的研究可以为投资者提供有价值的参考信息。本文以国债期货和利率掉期为基础,探讨利率衍生品市场的价格发现功能和溢出结构。文章建立信息共享模型和溢出指数模型进行实证分析。研究结果表明:首先,信息共享模型的计算结果表明,国债期货和利率互换市场的价格发现能力强于现货市场。其次,从结构性断点分析,国债期货和利率掉期没有断点,而国债现货有3个断点。论文基于结构断点将整个样本分为四个阶段,发现利率衍生品市场的价格发现能力动态变化。第三,国债期货作为市场的净溢出,发展相对稳定。国债期货和利率互换均对现货市场产生溢出效应,表明我国利率衍生品市场能够对国债现货市场产生冲击。

京公网安备 11010802027423号

京公网安备 11010802027423号