Journal of Banking Regulation Pub Date : 2024-03-07 , DOI: 10.1057/s41261-024-00234-1 Paul Tanyi , Jack Cathey

|

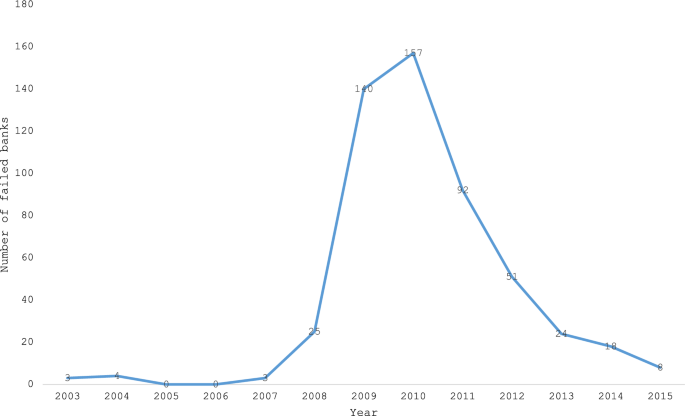

The most recent financial crisis exposed to the auditors the risk associated with the audit engagement of their banking clients. Because many banking clients failed and investors suffered trillions of dollars in losses, auditors are now defendants in numerous shareholder and regulatory lawsuits. There is consensus that the financial crisis was created by an abundance of credit, excessive risk taking through complex financial instruments, weak corporate structures, and ineffective regulatory mechanisms. In this study, we examine how the financial crisis has affected the audit engagements of banking clients. We examine audit fees, audit report lag, and auditor changes before and after the financial crisis with respect to specific bank risks like credit risk, interest rate risk, and liquidity. Overall, we find that auditors are more responsive to bank risks in the post-financial crisis period compared to the pre-financial crisis period.

中文翻译:

美国银行审计:金融危机以来有变化吗?

最近的金融危机向审计师暴露了与银行客户审计业务相关的风险。由于许多银行客户倒闭,投资者蒙受数万亿美元的损失,审计师现在成为众多股东和监管诉讼的被告。人们一致认为,金融危机是由信贷过剩、复杂金融工具过度冒险、薄弱的公司结构和无效的监管机制造成的。在这项研究中,我们研究了金融危机如何影响银行客户的审计业务。我们针对信用风险、利率风险和流动性等特定银行风险,检查金融危机前后的审计费用、审计报告滞后和审计师变更。总体而言,我们发现与金融危机前时期相比,审计师在金融危机后时期对银行风险的反应更加灵敏。

京公网安备 11010802027423号

京公网安备 11010802027423号