Journal of Ambient Intelligence and Humanized Computing ( IF 3.662 ) Pub Date : 2024-03-12 , DOI: 10.1007/s12652-024-04766-2 Luckshay Batra , H. C. Taneja

|

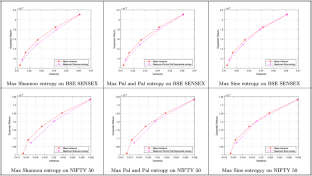

This paper presents a rich class of information theoretical measures designed to enhance the accuracy of portfolio risk assessments. The Mean-Variance model, pioneered by Harry Markowitz, revolutionized the financial sector as the first formal mathematical method to risk-averse investing in portfolio optimization theory. We analyze the effectiveness of this with the models that replace expected portfolio variance with measures of information (uncertainty of the portfolio allocations to the different assets) and five major practical issues. The empirical analysis is carried out on the historical data of Indian financial stock indices by application of portfolio optimization problem with information measures as the objective function and constraints derived from the return and the risk. Our findings indicate that the information measures with parameters can be used as an adequate supplement to traditional portfolio optimization models such as the mean-variance model.

中文翻译:

投资组合优化问题中信息测度的比较研究

本文提出了丰富的信息理论措施,旨在提高投资组合风险评估的准确性。由 Harry Markowitz 首创的均值-方差模型彻底改变了金融领域,成为投资组合优化理论中风险规避投资的第一个正式数学方法。我们通过用信息度量(不同资产的投资组合分配的不确定性)代替预期投资组合方差的模型和五个主要实际问题来分析其有效性。应用以信息测度为目标函数、以收益和风险为约束条件的投资组合优化问题,对印度金融股指的历史数据进行实证分析。我们的研究结果表明,带有参数的信息度量可以用作传统投资组合优化模型(例如均值方差模型)的充分补充。

京公网安备 11010802027423号

京公网安备 11010802027423号