Journal of Banking Regulation Pub Date : 2024-03-21 , DOI: 10.1057/s41261-024-00240-3 Ulrich Krüger , Christoph Roling , Leonid Silbermann , Lui-Hsian Wong

|

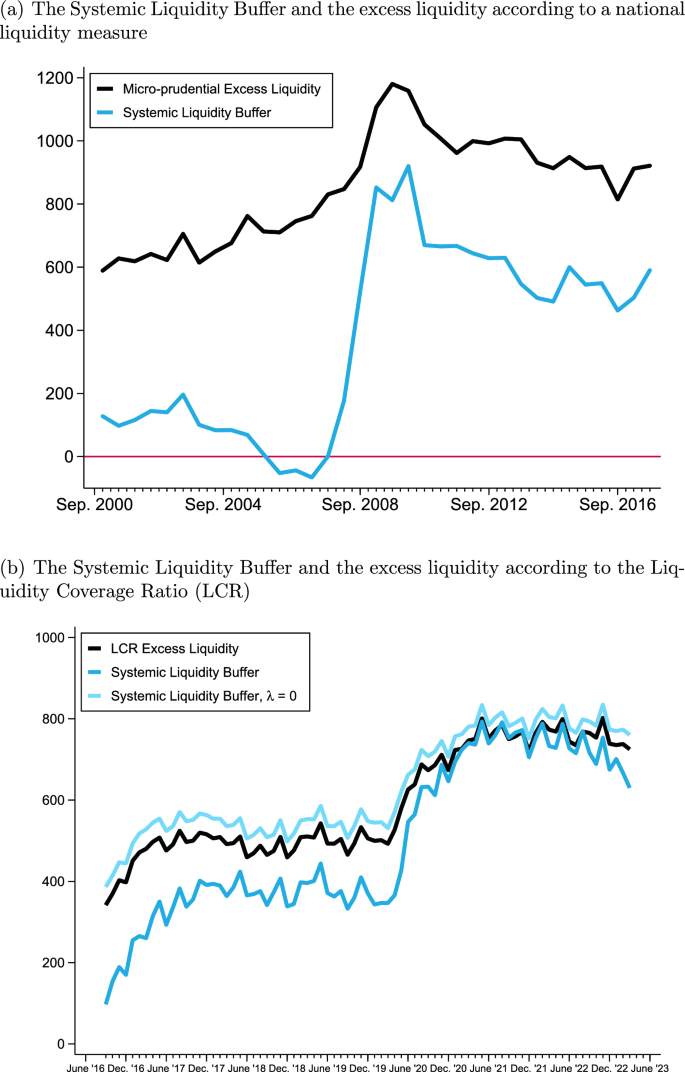

When a widespread funding shock hits the banking system, banks may engage in strategic behaviour to deal with funding shortages by a pre-emptive disposal of assets. Alternatively, they may adopt a more cautious strategy to mitigate price reactions, thereby distributing the assets sales into smaller portions over time. We model banks’ optimal behaviour using standard optimisation techniques and show that an equilibrium always exits in a stylised setting. A numerical analysis to approximate the equilibrium supplements the theoretical part. The implementation delivers two liquidity measures for the German banking system: the Systemic Liquidity Buffer and the Systemic Liquidity Shortfall. These measures are more informative about systemic liquidity risk than regulatory liquidity measures, such as the LCR, because they model adverse, nonlinear price dynamics in a more realistic way. Our approach is applied to different stress scenarios.

中文翻译:

银行的战略互动、不利的价格动态和系统性流动性风险

当广泛的资金冲击冲击银行体系时,银行可能会采取战略行为,通过先发制人的资产处置来应对资金短缺。或者,他们可能会采取更谨慎的策略来减轻价格反应,从而随着时间的推移将资产销售分成更小的部分。我们使用标准优化技术对银行的最优行为进行建模,并表明均衡总是存在于程式化的环境中。近似平衡的数值分析补充了理论部分。该实施为德国银行体系提供了两项流动性措施:系统流动性缓冲和系统流动性短缺。这些指标比 LCR 等监管流动性指标更能提供有关系统性流动性风险的信息,因为它们以更现实的方式模拟不利的非线性价格动态。我们的方法适用于不同的压力场景。

京公网安备 11010802027423号

京公网安备 11010802027423号