Knowledge and Information Systems ( IF 2.7 ) Pub Date : 2024-04-22 , DOI: 10.1007/s10115-024-02095-6 Douglas Castilho , Thársis T. P. Souza , Soong Moon Kang , João Gama , André C. P. L. F. de Carvalho

|

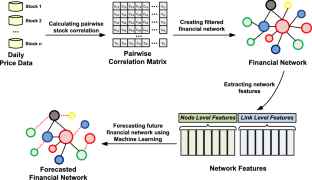

We propose a model that forecasts market correlation structure from link- and node-based financial network features using machine learning. For such, market structure is modeled as a dynamic asset network by quantifying time-dependent co-movement of asset price returns across company constituents of major global market indices. We provide empirical evidence using three different network filtering methods to estimate market structure, namely Dynamic Asset Graph, Dynamic Minimal Spanning Tree and Dynamic Threshold Networks. Experimental results show that the proposed model can forecast market structure with high predictive performance with up to \(40\%\) improvement over a time-invariant correlation-based benchmark. Non-pair-wise correlation features showed to be important compared to traditionally used pair-wise correlation measures for all markets studied, particularly in the long-term forecasting of stock market structure. Evidence is provided for stock constituents of the DAX30, EUROSTOXX50, FTSE100, HANGSENG50, NASDAQ100 and NIFTY50 market indices. Findings can be useful to improve portfolio selection and risk management methods, which commonly rely on a backward-looking covariance matrix to estimate portfolio risk.

中文翻译:

使用机器学习根据网络特征预测金融市场结构

我们提出了一种模型,使用机器学习根据基于链路和节点的金融网络特征来预测市场相关结构。为此,通过量化主要全球市场指数的公司成分之间资产价格回报的时间相关联动,将市场结构建模为动态资产网络。我们使用三种不同的网络过滤方法来估计市场结构,即动态资产图、动态最小生成树和动态阈值网络,提供经验证据。实验结果表明,所提出的模型可以以较高的预测性能预测市场结构,与基于时不变相关性的基准相比,提高了高达\(40\%\) 。对于所研究的所有市场,与传统使用的成对相关性度量相比,非成对相关性特征非常重要,特别是在股票市场结构的长期预测中。提供 DAX30、EUROSTOXX50、FTSE100、HANGSENG50、NASDAQ100 和 NIFTY50 市场指数的股票成分证据。研究结果有助于改进投资组合选择和风险管理方法,这些方法通常依赖于向后看的协方差矩阵来估计投资组合风险。

京公网安备 11010802027423号

京公网安备 11010802027423号