Abstract

Motivated by the growing importance of swing contracts in natural gas markets, this article extends the literature on commodity price modelling as well as valuation methods and sensitivity analysis for swing options. While most previous studies focused on simple price models, we face the challenge of deriving option properties under more realistic commodity price dynamics. We begin by formulating a multi-factor price forward curve model with parametric volatility functions, which can capture uncertainty in both yearly seasonality and time-to-maturity effects, and propose a two-step calibration procedure to fit such models to empirical data. We then show how results from the literature can be combined to obtain swing option values and sensitivities in such a general framework. In this context, we also provide new theoretical results and a first numerical approach to efficiently estimate swing options’ gammas. For options’ deltas, we expand upon existing studies by including a larger variety of contract specifications and by focusing on a multidimensional variant of the Longstaff–Schwartz algorithm as an alternative option valuation method. With these contributions, we supply important tools for swing option sellers and buyers relying on accurate option value and risk estimates to maintain their business models, hedge option-related risks and adequately represent swing options in financial reporting.

Similar content being viewed by others

Notes

Joskow (1985, 1987) identifies common properties in coal contracts such as take-or-pay provisions and delivery schedules with minimum and maximum production and purchase obligations. Barbieri and Garman (1996) and Garman and Barbieri (1997) provide a systematization of different swing option variants.

For a brief discussion of such modifications, see Sect. 2.2.3.3.

More details on the VNG Group are available in its annual report of 2016 (see http://vng-gruppe.de/sites/default/files/vng_annual_report_2016_en_web.pdf).

Note that our focus is not a full empirical analysis of the European natural gas market. This sample serves the sole purpose of illustrating our methodologies. Thus, its small size is sufficient for our application.

\(\Gamma \) is equal to the square-root of the corresponding correlation matrix \(\Gamma ^2 = \Gamma \Gamma '\) (see Benmenzer et al. 2007).

We assume the existence of a unique equivalent martingale measure. The existence and uniqueness of such measures in different markets is a formidable topic in itself, so a detailed discussion is outside the scope of our study.

An alternative estimation approach is to use option-implied volatilities of forwards. Kiesel et al. (2009) consider a two-factor variant of the price model below for modelling electricity futures. They calibrate the model to options on electricity futures and discuss its performance in practical applications.

We do not intend to estimate the market price of risk. We refer to it simply to justify our approach.

On average, our sample data covers about 241 trading days per year. Thus, in what follows, we always use the factor \(\sqrt{241}\) to annualize volatilities.

More precisely, \(K = 48\) independent factors capture the entire return covariance structure.

Detailed results for the monthly and seasonal PCA are available upon request.

Each column \(x_k(t_n)\) of \(X_n\) contains a discretized normalized volatility function. In the case of (2.6), we have \(x_1(t_n) = (1,...,1)'\), \(x_2(t_n) = (\exp (-\textstyle {\frac{\vartheta }{12}}(\tau _j)))_{j=1,...,m}\) and \(x_3(t_n) = (\cos (\textstyle {\frac{2\pi }{12}} (\tau _j + (t_n\bmod 12))))_{j=1,...,m}\). In this example, it is clear that \(X_n\) has linearly independent columns.

We leave the detailed statistical properties of this estimator for future research.

We plot the resulting average \(R^2\) dependent on the choice of \(\vartheta \) in Fig. 12 of the appendix.

For fixed optimal \(\vartheta \), we use the standard \(95\%\) OLS confidence intervals.

If \(\sigma _3(t,T)\) captures fewer season spreads at the front end of the forward curve (e.g. if we choose \((c_{\min }^{(3)}, c_{\max }^{(3)}) = (0,6)\)), the TSLS procedure yields high negative correlations (\(\rho _{12}\) and \(\rho _{23}\)) of short-term variation with both long-term and seasonal variation. This finding is not in line with our previous results which suggest positively correlated long- and short-term variation as well as very low correlation between seasonal variation and other factors. Thus, we have to be careful when choosing piecewise volatility functions.

The normalized seasonal volatility functions (in the case of \(\tau _1\) being a January) are plotted in Fig. 14 of the appendix.

Additional sample regression plots are illustrated in Fig. 15 of the appendix.

We emphasize that we do not find monotonically increasing spread volatilities to be a general feature of the natural gas market. By applying another PFC methodology, which also fulfills the properties described in Sect. 2.1, on more recent market data, we also obtain low seasonal volatilities at the very front end of the curve, but find that spread variation peaks near 36 front months and subsequently decreases. To be precise, we estimate \(\hat{\sigma }_{\text {sw}} = (1.88\%, 2.36\%, 2.67\%, 3.32\%, 2.85\%, 2.45\%)^{\prime }\) based on PFC data for the year 2015.

Similar models have been used by Maciejowska and Weron (2013) for electricity price forecasting. They propose a factor model to reduce the dimension of the original multivariate time-series and suggest to model the factors based on a vector autoregressive process.

We restrict our attention to this model because our alternative model with piecewise seasonal volatility functions (2.18) allows similar conclusions.

We drop the contract \(j = 48\) because our P-TSLS procedure requires a total number of months which can be divided by six.

This is why we keep the spot price extension simple but point out that, of course, it could be improved.

We truncate outliers by considering data points inside the three sigma band only. As the outliers cluster together, a regime-switching model extension might be considered. However, this is beyond the scope of this article because we focus on deriving option pricing and sensitivity results based on simpler processes.

We can easily translate the results of the following sections to the price model introduced in Sect. 2.

We address the use of information in decision making more explicitly in Sect. 3.4.

Broadie and Glasserman (1996) have developed a pathwise derivative method to determine sensitivities of option prices. This pathwise approach is justified if we can interchange differentiation and taking expectations. While this is not allowed in our context, we are still able to express first-order sensitivities as the expectation of a pathwise calculable term.

We used the fact that, as shown in (3.15), the partial derivative of \(S_T\) with respect to F(0, T) is a pathwise constant term such that the second-order partial derivative of \(S_T\) vanishes.

A sequence \((x_n)\) of vectors in a Hilbert space H is said to be total, if the linear subspace spanned by \((x_n)\) is dense in H.

The choice of \(R_{cond}\) is crucial for the performance of the valuation algorithm. We find unstable regression matrices X, which are very sensitive to input parameters, for barriers with low denominators around \(\epsilon \cdot 10^3\). In contrast, a too high denominator around \(\epsilon \cdot 10^9\) results in too small regression matrices, which contain only a few basis functions on average. Therefore, we suggest using a denominator around \(\epsilon \cdot 10^6\) to ensure stability.

Besides the power class, other polynomial families like Chebyshev, Hermite, Legendre or Laguerre could be used in modelling. However, because most of them underperform and/or require more computation time, Boogert and De Jong (2011) conclude that powers are the preferred choice of basis functions.

The existence of the functional relationship \(\mathcal {C}_t^r(F_t)\) is guaranteed by the Markov property and the factorization lemma of measure theory (see Klenke 2007, Corollary 1.97).

Details of this problem are illustrated in the simulation study of Sect. 4.4.

Because seasonal variation is not correlated with the other factors at economically significant levels, we set the corresponding correlation estimates equal to zero.

For simplicity and because it does not qualitatively change our results, we disregard discounting by setting the interest rate equal to zero.

Figure 16 of the appendix illustrates some sample PFCs resulting in our simulations.

Our performance measure is not designed to compare estimated values and true values because the latter are unknown. We ensure accuracy by basing our estimation approach on solid theory and previous results.

In Sect. 4.3.2, we find support for the hypothesis that this phenomenon might be related to the suboptimality of the forwards strategy.

This can be shown using random state variables as basis functions which are not correlated with the expected future payoff. The detailed results of such a simulation are available upon request.

Some instructions on this topic are given in Asmussen and Glynn (2007, sec. 2a).

For the commonly traded energy band products (“swing” contracts with \(Q_{\min } = Q_{\max } = 365\)), we do not need the swing option valuation methodology.

The detailed results of the analysis with sample size \(N = 5000\) are reported in Table 11 of the appendix.

Recall that T has to fit calendar month numbering, i.e., \(T \bmod 12 = c\) with \(c \in \{0,...,11\} \, \hat{=} \{\text {Jan},..., \text {Dec}\}\).

We report the results for the corresponding PFD and TFD approaches in Table 12 of the appendix.

This proposition is similar to Bardou et al. (2010, Theorem 2). However, we avoid the triangular set notation introduced by the authors and provide a shorter proof by inducting backwards with Bellman’s equation.

Operations preserving convexity are discussed in, for example, Boyd and Vandenberghe (2009).

We obtain similar results for our forwards approach.

A theoretical discussion of an existing bias-variance tradeoff can be found in the last section of this appendix, where we focus on bandwidth choice for the gamma estimator.

The results for the other contracts and for the forwards approach are similar.

This would be the case if the integrand itself was differentiable almost everywhere (as stated by L’Ecuyer 2007). In fact, our analysis confirms exploding variance for small \(\varepsilon _N\).

References

Alexandrov, A. (1939). Almost everywhere existence of the second differential of a convex function and some properties of convex surfaces connected with it. Leningrad State University Annals, Mathematics Series, 37, 3–35.

Anupindi, R., & Bassok, Y. (1999). Supply contracts with quantity commitments and stochastic demands. In S. Tayur, G. Ram, & M. Magazine (Eds.), Quantitative models for supply change management (pp. 197–232). Boston: Kluwer Academic Publishers.

Asmussen, S., & Glynn, P. (2007). Stochastic simulation: Algorithms and analysis (57th ed.). New York: Springer.

Balvers, R., Wu, Y., & Gilliland, E. (2000). Mean reversion across national stock markets and parametric contrarian investment strategies. Journal of Finance, 55(2), 745–772.

Barbieri, A., & Garman, M. (1996). Putting a price on swings. Energy Power Risk Management, 1(6), 17–19.

Bardou, O., Bouthemy, S., & Pagés, G. (2010). When are swing options bang-bang and how to use it. International Journal of Theoretical and Applied Finance, 13(6), 867–899.

Barrera-Esteve, C., Bergeret, F., Dossal, C., Gobet, E., Meziou, A., Munos, R., et al. (2006). Numerical methods for the pricing of swing options: A stochastic control approach. Methodology and Computing in Applied Probability, 8(4), 517–540.

Bellman, R. (1952). On the theory of dynamic programming. Proceedings of the National Academy of Sciences, 38(8), 716–719.

Bellman, R. (1957). Dynamic programming. Princeton, NJ: Princeton University Press.

Benmenzer, G., Gobet, E., & Jérusalem, T. (2007). Arbitrage free cointegrated models in gas and oil future markets. Working Paper, Cornell University.

Black, F. (1976). The pricing of commodity contracts. Journal of Financial Economics, 3(1–2), 167–179.

Black, F., & Scholes, M. (1973). The pricing of options and corporate liabilities. Journal of Political Economy, 81(3), 637–654.

Bonnans, J., Cen, Z., & Christel, T. (2012). Sensitivity analysis of energy contracts by stochastic programming techniques. In R. Carmona, P. Del Moral, P. Hu, & N. Oudjane (Eds.), Numerical methods in finance (pp. 447–471). Berlin, Heidelberg: Springer.

Bonnans, J., & Shapiro, A. (2000). Perturbation analysis of optimization problems. New York: Springer.

Boogert, A., & De Jong, C. (2011). Gas storage valuation using a multi-factor price process. Journal of Energy Markets, 4(4), 29–52.

Boyd, S., & Vandenberghe, L. (2009). Convex optimization (7th ed.). Cambridge, MA: Cambridge University Press.

Boyle, R., Broadie, M., & Glasserman, P. (1997). Monte Carlo methods for security pricing. Journal of Economic Dynamics and Control, 21(8–9), 1267–1321.

Breslin, J., Clewlow, L., Kwok, C., & Strickland, C. (2008). Gaining from complexity: MFMC models. Energy Risk, April, 60–64.

Brezis, H. (2010). Functional analysis, Sobolev spaces and partial differential equations. New York: Springer.

Broadie, M., & Glasserman, P. (1996). Estimating security price derivatives using simulation. Management Science, 42(2), 269–285.

Broadie, M., & Glasserman, P. (1997). Pricing American-style securities using simulation. Journal of Economic Dynamics and Control, 21(8–9), 1323–1352.

Brown, S., & Yücel, M. (2008). What drives natural gas prices? Energy Journal, 29(2), 45–60.

Carmona, R., & Touzi, N. (2008). Optimal multiple stopping and valuation of swing options. Mathematical Finance, 18(2), 239–268.

Chen, N., & Liu, Y. (2014). American option sensitivities estimation via a generalized infinitesimal perturbation analysis approach. Operations Research, 62(3), 616–632.

Chiarella, C., Clewlow, L., & Kang, B. (2009). Modelling and estimating the forward price curve in the energy market. Working Paper 260, Quantitative Finance Research Centre, University of Technology Sydney.

Clément, E., Lamberton, D., & Protter, P. (2002). An analysis of a least squares regression method for American option pricing. Finance and Stochastics, 6(4), 449–471.

Clewlow, L., & Strickland, C. (1999a). A multi-factor model for energy derivatives. QFRC Research Paper Series 28, University of Technology Sydney.

Clewlow, L., & Strickland, C., (1999b). Valuing energy options in a one factor model fitted to forward prices. QFRC Research Paper Series 10, University of Technology Sydney.

Clewlow, L., & Strickland, C. (2000). Energy derivatives: Pricing and risk management. London: Lacima Publications.

Cortazar, G., & Schwartz, E. (1994). The valuation of commodity contingent claims. Journal of Derivatives, 1(4), 27–39.

Dahlgren, M. (2005). A continuous time model to price commodity-based swing options. Review of Derivatives Research, 8(1), 27–47.

De Jong, C., (2006). The nature of power spikes: A regime-switch approach. Studies in Nonlinear Dynamics and Econometrics, 10(3), Article 3.

De Maeseneire, J. (2010). Estimating forward price curve in energy markets with MCMC method. Research Paper, University of Waterloo.

Deaton, A., & Laroque, G. (1992). On the behaviour of commodity prices. Review of Economic Studies, 59(1), 1–23.

Efron, B., & Tibshirani, R. (1993). An introduction to the bootstrap. Boca Raton: Chapman & Hall.

Eydeland, A., & Wolyniec, K. (2003). Energy and power risk management: New developments in modeling, pricing and hedging (Vol. 206). Hoboken, NJ: Wiley.

Garman, M., & Barbieri, A. (1997). Ups and downs of swing. Energy Power Risk Management, 2(1).

Geman, H. (2005). Commodities and commodity derivatives: Modelling and pricing for agricultures, metals and energy. Chichester: Wiley.

Gibson, R., & Schwartz, E. (1990). Stochastic convenience yield and the pricing of oil contingent claims. Journal of Finance, 45(3), 959–976.

Glasserman, P. (2003). Monte Carlo methods in financial engineering. New York: Springer.

Glasserman, P., & Yu, B. (2004). Number of paths versus number of basis functions in American option pricing. Annals of Applied Probability, 14(4), 2090–2119.

Hambly, B., Howison, S., & Kluge, T. (2009). Modelling spikes and pricing swing options in electricity markets. Quantitative Finance, 9(8), 937–949.

Haugh, M., & Kogan, L. (2004). Pricing American options: A duality approach. Operations Research, 52(2), 258–270.

Hayashi, T., & Mykland, P. (2005). Evaluating hedging error: An asymptotic approach. Mathematical Finance, 15(1), 309–343.

Hedestig, J. (2014). Pricing and hedging of swing options in the European electricity and gas markets. Student Paper, Lund University.

Hubbard, R., & Weiner, R. (1986). Regulation and long-term contracting US natural gas markets. Journal of Industrial Economics, 35(1), 71–79.

Hull, J., & White, A. (1994). Numerical procedures for implementing term structure models i: Single factor models. Journal of Derivatives, 2(1), 7–16.

Ibáñez, A., & Zapatero, F. (2004). Monte Carlo valuation of American options through computation of the optimal exercise frontier. Journal of Financial and Quantitative Analysis, 39(2), 253–275.

Jaillet, J., Ronn, E., & Tompaidis, S. (2004). Valuation of commodity-based swing options. Management Science, 50(7), 909–921.

Jamishidian, F. (1991). Commodity option valuation in the Gaussian futures term structure model. Review of Futures Markets, 10(2), 324–346.

Jin, Y., & Jorion, P. (2006). Firm value and hedging: Evidence from US oil and gas producers. Journal of Finance, 61(2), 893–919.

Johnson, R., & Wichern, D. (2007). Applied multivariate statistical analysis (6th ed.). Upper Saddle River, NJ: Prentice Hall.

Joskow, P. (1985). Vertical integration and long-term contracts: The case of coal-burning electric generating plants. Journal of Law, Economics, & Organization, 1(1), 33–80.

Joskow, P. (1987). Contract duration and relationship-specific investments: Empirical evidence from coal markets. American Economic Review, 77(1), 168–185.

Kiesel, R., Gernhard, J., & Stoll, S. (2010). Valuation of commodity-based swing options. Journal of Energy Markets, 3(3), 91–112.

Kiesel, R., Schindlmayr, G., & Börger, R. (2009). A two-factor model for the electricity forward market. Quantitative Finance, 9(3), 279–287.

Klenke, A. (2007). Probability theory: A comprehensive course. London: Springer.

Kohler, M. (2011). A review of regression-based Monte Carlo methods for pricing American options. In L. Devroye, B. Karasözen, M. Kohler, & R. Korn (Eds.), Recent developments in applied probability and statistics (pp. 37–58). Heidelberg: Physica.

Kolb, R., & Overdahl, J. (Eds.). (2010). Financial derivatives: Pricing and risk management. Hoboken, NJ: Wiley.

Kovacevic, R., Pflug, G., & Vespucci, M. (2013). Handbook of risk management in energy production and trading. New York: Springer.

L’Ecuyer, P., (2007). Variance reduction’s greatest hits. In Proceedings of the 2007 European simulation and modeling conference (pp. 5–12). European Multidisciplinary Society for Modelling and Simulation Technology, Ostend.

L’Ecuyer, P., & Perron, G. (1994). On the convergence rates of IPA and FDC derivative estimators. Operations Research, 42(4), 643–656.

Lioui, A., & Poncet, P. (2005). Dynamic asset allocation with forwards and futures. New York: Springer.

Løland, A., & Lindqvist, O., (2008). Valuation of commodity-based swing options: A survey. Note SAMBA/38/80, Norwegian Computing Center.

Longstaff, F., & Schwartz, E. (2001). Valuing American options by simulation: A simple least-squares approach. Review of Financial Studies, 14(1), 113–147.

MacAvoy, P. (2000). The natural gas market: Sixty years of regulation and deregulation. New Haven, London: Yale University Press.

Maciejowska, K., & Weron, R., (2013). Forecasting of daily electricity spot prices by incorporating intra-day relationships: Evidence from the UK power market. In IEEE conference proceedings, 10th international conference in the European energy market (EEM).

Manoliu, M., & Tompaidis, S. (2002). Energy futures prices: Term structure models with Kalman filter estimation. Applied Mathematical Finance, 9(1), 21–43.

McLeish, D. (2011). Monte Carlo simulation and finance. Hoboken, NJ: Wiley.

Merton, R. (1973). Theory of rational option pricing. Bell Journal of Economics and Management Science, 4(1), 141–183.

Musiela, M., & Rutkowski, M. (2004). Martingale methods in financial modelling (2nd ed.). Berlin: Springer.

Pascucci, A. (2011). PDE and martingale methods in option pricing. Milano: Springer, Bocconi University Press.

Pflug, G., & Broussev, N. (2009). Electricity swing options: Behavioral models and pricing. European Journal of Operational Research, 197(3), 1041–1050.

Pilipovic, D. (2007). Energy risk: Valuing and managing energy derivatives (2nd ed.). New York: McGraw-Hill.

Pilipovic, D., & Wengler, J. (1998). Getting into the swing. Energy Power Risk Management, 2(10).

Pinar, M. (2007). Robust scenario optimization based on downside-risk measure for mulit-period portfolio selection. OR Spectrum, 29(2), 295–309.

Poterba, J. (1988). Mean reversion in stock prices: Evidence and implications. Journal of Financial Economics, 22(1), 27–59.

Rockafellar, R., & Wets, R. (2009). Variational analysis (Vol. 317). Berlin: Springer.

Rodríguez, R. (2008). Real option valuation of free destination in long-term liquefied natural gas supplies. Energy Economics, 30(4), 1909–1932.

Rudin, W. (1964). Principles of mathematical analysis (3rd ed.). New York: McGraw-Hill.

Schwartz, E. (1997). The stochastic behaviour of commodity prices: Implications for valuation and hedging. Journal of Finance, 52(3), 923–973.

Schwartz, E., & Smith, J. (2000). Short-term variations and long-term dynamics in commodity prices. Management Science, 46(7), 893–911.

Smith, C., & Zimmerman, J. (1976). Valuing employee stock option plans using option pricing models. Journal of Accounting Research, 14(2), 357–364.

Thompson, A. (1995). Valuation of path-dependent contingent claims with multiple exercise decisions over time: The case of take-or-pay. Journal of Financial and Quantitative Analysis, 30(2), 271–293.

van der Hoek, J., & Elliott, R. (2006). Binomial models in finance. New York: Springer.

Vinga, S., (2004). Convolution integrals of normal distribution functions. Supplementary material to Vinga and Almeida (2004) “Rényi continuous entropy of DNA sequences”.

Wahab, M., & Lee, C. (2011). Pricing swing options with regime switching. Annals of Operations Research, 185(1), 139–160.

Wahab, M., Yin, Z., & Edirisinghe, N. (2010). Pricing swing options in the electricity markets under regime-switching uncertainty. Quantitative Finance, 10(9), 975–994.

Warin, X. (2012). Hedging swing contract on gas markets. Working Paper, Cornell University.

Acknowledgements

We thank the Verbundnetz Gas AG for supporting our research by supplying forward price data and by contributing important ideas for the design of the estimation methods developed in our article. We are also indebted to Max von Renesse, Ralf Wunderlich, Xaver Muschik, the editor, and an anonymous reviewer for valuable comments and suggestions. Generous financial support was provided by the Wissenschaftsförderung der Sparkassen-Finanzgruppe e.V.

Author information

Authors and Affiliations

Corresponding author

Appendices

Appendix

Proofs

Proof of Lemma 2.4

Let \(f_{\mu ,\Sigma }\) denote the probability density function of a multivariate normal distribution with mean \(\mu \) and covariance \(\Sigma \). The unconditional probability density function \(\varphi _Y\) of Y is

where \(*\) denotes the convolution operator (see Klenke 2007, p. 277). For a detailed verification of the last equation, see Vinga (2004). \(\square \)

Proof of Proposition 2.5

With \(\varepsilon _n \sim \mathcal {N}(0, \sigma _\varepsilon ^2 I)\), we have \(\hat{a}_n | a_n \sim \mathcal {N}(a_n, \sigma _\varepsilon ^2 (X' X)^{-1})\) (see Johnson and Wichern 2007, p. 370). Under \(\mathbb {P}_\Sigma \), we have \(a_n \sim \mathcal {N}(\eta ,\Sigma )\) by definition. Thus, Lemma 2.4 implies

Considering the independence assumptions, the proposition follows by the definition of the Wishart distribution (see Johnson and Wichern 2007, p. 174). \(\square \)

Proof of Proposition 3.1

\(\mathcal {Q}\), taking values in \([0,1]^T \) and being constrained by (3.3), is a bounded and closed subset of \(\mathcal {L}^2 \cap \mathcal {L}^\infty \). Using the Banach-Alaoglu theorem (see, Brezis 2010, Theorem 3.16), we can deduce that it is a weak compact subset of \(\mathcal {L}^2\) (see Bonnans et al. 2012). The objective function \(\mathcal {J}: \mathcal {Q}\rightarrow \mathbb {R}\), defined by

is weakly continuous, such that the image of the compact space \(\mathcal {Q}\) under the continuous mapping \(\mathcal {J}\) is also compact. Because \(\mathcal {J}(\mathcal {Q})\) is a closed and bounded subset of \(\mathbb {R}\), the function \(\mathcal {J}\) reaches its supremum. \(\square \)

Proof of Lemma 3.3

(based on, Bardou et al. 2010, Property P3) We only prove the concavity property because piecewise affinity can be verified by backward induction similar to the proof of Proposition 3.4, which handles the case \(Q_{\min }, Q_{\max }\in \mathbb {N}_0\).

For fixed \(t \in \{0,...,T -1\}\), let \(Q_t, Q'_t \in {[}\underline{Q}_t, \overline{Q}_t]\), \(\lambda \in [0,1]\) and \(F_t\) be given. Additionally, let \((q_t) \in \mathcal {Q}\) be a feasible policy reached with \(\sum _{s=0}^{t-1} q_t = Q_t\) (almost surely) and

and let \(q' \in \mathcal {Q}\) be a feasible policy with \(\sum _{s=0}^{t-1} q'_t = Q'_t\) and

Note that, since q and \(q'\) are both [0, 1]-valued, \(\lambda q + (1-\lambda ) q' := (\lambda q_t + (1-\lambda ) q'_t)_{0\le t \le T -1}\) is also [0, 1]-valued. Furthermore, \(\lambda q + (1-\lambda ) q'\) reaches \(\lambda Q_t + (1-\lambda ) Q'_t\) on day t and fulfills the global constraints, such that it is a feasible policy. We have

i.e., \(\mathfrak {V}_{t}(Q_{t}, F_{t})\) is concave in \(Q_t\). \(\square \)

Proof of Proposition 3.4

Footnote 57 For \(Q_t \in [\underline{Q}_t, \overline{Q}_t] \cap \mathbb {N}_0\), we have \(\underline{q}_t, \overline{q}_t \in \mathbb {N}_0\). We show that, in this case, the mapping

is affine on \([\underline{q}_t, \overline{q}_t]\) for all \(t\in \{0,...,T -1\}\) and \(F_t\in \mathbb {R}^{T -t}_+\). Without loss of generality, we assume \(Q_{t} \ge Q_{\min } - (T-t-1)\) and \(Q_{t} \le Q_{\max }-1\), such that \([\underline{q}_t, \overline{q}_t]=[0,1]\). We proceed by backward induction on t.

Basis For \(t = T - 1\), we have to consider \(Q_{T -1} \in [\underline{Q}_{T -1}, \overline{Q}_{T -1}]\) and \(q_{T -1} \in [\underline{q}_{T -1}, \overline{q}_{T -1}]\). Under these constraints, we have \(Q_{\min } \le Q_T \le Q_{\max }\) such that mapping (A.1) becomes

which is linear.

Induction hypothesis Assume that, for some \(t \in \{1,...,T -1\}\), we have: For all \(Q_t \in [\underline{Q}_t, \overline{Q}_t]\) with \(Q_t\in \mathbb {N}_0\) and all \(F_t\in \mathbb {R}^{T -t}_+\), the mapping

is affine on \([\underline{q}_t, \overline{q}_t]\).

Inductive step Now we move from t to \(t-1\). Let \(Q_{t-1} \in [0 \vee (Q_{\min } - (T-t)), (Q_{\max }-1) \wedge (t-1)] \cap \mathbb {N}_0\). Thus, we have to show the affinity of

on [0, 1]. For \(q_{t-1}\) and \(F_t\) both fixed, we look closer at

on \([\underline{q}_{t},\overline{q}_{t}]\). Note that \(1-q_{t-1} \in [\underline{q}_{t},\overline{q}_{t}]\) because \(Q_{\min } - (T-t) \le Q_{t-1} \le Q_{\max }-1\). We use the induction hypothesis to conclude that (A.2) is piecewise affine; more precisely, affine on \([\underline{q}_{t}, 1-q_{t-1}]\) and \([1-q_{t-1}, \overline{q}_{t}]\).

If \(q_t \in [\underline{q}_{t}, 1-q_{t-1}]\), we have \(q_{t-1}+q_t \le 1\). We define \(\tilde{Q}_t := Q_{t-1}\). Since \(\tilde{Q}_t \in [\underline{Q}_t, \overline{Q}_t] \cap \mathbb {N}_0\), the mapping

is affine on \([0 \vee (Q_{\min }-Q_{t-1}-(T-t-1)), 1]\) by induction hypothesis. Setting \(\tilde{q}_t = q_{t-1}+q_t\) then implies that mapping (A.2) is affine on \([\underline{q}_{t}, 1-q_{t-1}]\).

At the same time, we have \(q_{t-1}+q_t \ge 1\) if \(q_t \in [1-q_{t-1}, \overline{q}_{t}]\). We now set \(\tilde{Q}_t := Q_{t-1} + 1 \in [\underline{Q}_t, \overline{Q}_t] \cap \mathbb {N}_0\). Again, the induction hypothesis states that (A.3) is affine on \([0, 1 \wedge (Q_{\max }-Q_{t-1}-1)]\), which implies that mapping (A.2) is affine on \([1-q_{t-1}, \overline{q}_{t}]\) by setting \(\tilde{q}_t = q_{t-1}+q_t-1\).

It follows that (A.2) is piecewise affine with monotonicity breakpoint at \(1-q_{t-1}\) such that the mapping reaches its maximum at the interval endpoints \(\underline{q}_{t}, \overline{q}_{t}\) or at its monotonicity breakpoint. We have

For fixed \(F_{t}\), we consider the mappings

on [0, 1] for \(q_t \in \{\underline{q}_{t}, 1-q_{t-1}, \overline{q}_{t}\}\).

For \(q_t = 1-q_{t-1}\), (A.4) becomes

which is affine.

For \(q_t = \underline{q}_{t} = 0 \vee (Q_{\min }-Q_{t-1}-q_{t-1}-(T-t-1))\), note that \(Q_{\min }-Q_{t-1}-(T-t-1) \in \mathbb {Z}\), such that we have either \(\underline{q}_{t} = 0\) or \(\underline{q}_{t} = Q_{\min }-Q_{t-1}-q_{t-1}-(T-t-1) \ge 0\) on the entire interval \(q_{t-1}\in [0,1]\). If \(\underline{q}_{t} = 0\), (A.4) becomes

which is affine by induction hypothesis (setting \(\tilde{Q}_t := Q_{t-1} \in \mathbb {N}_0\)). Otherwise, we have

which is also affine. For \(q_t = \underline{q}_{t} = 1 \wedge (Q_{\max } - Q_{t-1} - q_{t-1})\), we can similarly verify the affinity of (A.4).

It follows that \(q_{t-1} \mapsto \mathfrak {V}_{t}(Q_{t-1} + q_{t-1}, F_{t})\) is convex as a pointwise maximum of affine mappings on [0, 1]. It is affine because we know from Lemma 3.3 that it is also concave. Taking conditional expectations with respect to \(\mathcal {F}_{t-1}\) and adding \(f_{t-1}(S_{t-1}) \cdot q_{t-1}\) completes the inductive step.

Starting at \(t=0\) with \(Q_0 = 0 \in \mathbb {N}_0\), we conclude by forward induction that taking \(q_t\) from \(\{\underline{q}_t, \overline{q}_t\} \subseteq \{0,1\}\) is always one optimal choice because (A.1) is affine in the case of \(Q_t \in \mathbb {N}_0\). Hence, we can optimally exercise in digital fashion. \(\square \)

Proof of Corollary 3.6

(based on, Bonnans et al. 2012, Corollary 4.4) Because \(\phi (x)\) is locally Lipschitz continuous by Danskin’s theorem, Rademacher’s theorem (see, Rockafellar and Wets 2009, Theorem 9.60) states that it is totally differentiable almost everywhere.

Now, let \(x \in \mathbb {R}^n\) and \(\phi (x)\) be totally differentiable at x. Assume Eq. (3.11) does not hold, i.e., there exist \(v_1^*, v_2^* \in V^*(x)\) such that \({{\mathrm{d}}}_x \psi (x, v_1^*)\not ={{\mathrm{d}}}_x \psi (x, v_2^*)\). That is, the corresponding gradients differ in at least one entry with index i. Consider the direction \(h = (0,...,0,1,0,...0)\) where 1 is placed at position i. With Eq. (3.9), we then have

Thus, \(\phi (x)\) is not totally differentiable at x and we have a contradiction. \(\square \)

Proof of Lemma 3.7

(based on, Bonnans et al. 2012, Lemma 4.1 and Proposition 4.2) In the first step, we show that, for every t, the partial derivative of \(\mathcal {J}\) with respect to F(0, t) exists. We define \(g(F(0,t), \omega ) := f_t(S_t(F(0,t), \omega ))\cdot q_t\). Let \(x\in \mathbb {R}_+\) and \((x_n)\) be a sequence in \(\mathbb {R}_+\) with \(x_n \not = x\) for every \(n\in \mathbb {N}\) and \(\lim _{n\rightarrow \infty } x_n = x\). We now show that the corresponding sequence of difference quotients converges. To this end, set

for every \(\omega \in \Omega \). In view of the Lipschitz continuity of \(f_t\), Rademacher’s theorem (see, Rockafellar and Wets 2009, Theorem 9.60) states that it is differentiable almost everywhere and that its derivative is bounded. Combined with the partial differentiability of \(S_t\) in F(0, t), we know that \(g(\cdot ,\omega )\) is differentiable for almost every \(\omega \) such that

almost surely. According to the mean value theorem (see, Rudin 1964, Theorem 5.10), for every \(n \in \mathbb {N}\) and almost every \(\omega \in \Omega \), there exists \(y_n(\omega )\in \mathbb {R}_+\) such that \(\Delta g_n(\omega )= g'(y_n(\omega ),\omega )\). In particular, \(g_n\) is bounded almost everywhere for every n. Since \(g(x,\cdot )\) is integrable for every x, we can apply the dominated convergence theorem (see, Klenke 2007, Corollary 6.26) to see that \(g'(x, \cdot )\) is integrable and

Rewritten in our original terms, we have

In the second step, we verify the continuity of the partial derivatives. Again, let \(x^*\in \mathbb {R}_+\) and \((x_n)\) be a sequence in \(\mathbb {R}_+\) with \(x_n \not = x^*\) for every \(n\in \mathbb {N}\) and \(\lim _{n\rightarrow \infty } x_n = x^*\). Furthermore, denote \(\tilde{g}(F(0,t)) := S_t(F(0,t))\) and \(S_t^n := \tilde{g}(x_n)\), \(S_t^* := \tilde{g}(x^*)\). We have to show that

in \(\mathcal {L}^1\). By the chain rule of differentiation, at the points where \(f_t\) is differentiable, we have

Denote \(f_{\partial x} := \frac{\partial f}{\partial x}\). By assumption, the partial derivatives of \(S_t^*\) and \(S_t^n\) both have bounded density functions \(\varphi _t^*\) and \(\varphi _t^n\) with respect to the Lebesgue measure. Since \(f_t\) is Lipschitz continuous, \(\partial _{S_t} f_t \in \mathcal {L}^\infty (\Omega ,\mathcal {F},\mathbb {P}) \subseteq \mathcal {L}^q(\Omega ,\mathcal {F},\mathbb {P})\), \(1\le q < \infty \). Because the space of continuous functions with compact support \(C_c(\Omega )\) is dense in \(\mathcal {L}^q(\Omega ,\mathcal {F},\mathbb {P})\), we have

It follows that

and analogously

Moreover, \(\lim _{n\rightarrow \infty } S_t^n = S_t^*\) almost surely and \(\lim _{n\rightarrow \infty } \partial _{F(0,t)} S_t^n = \partial _{F(0,t)} S_t^*\) in \(\mathcal {L}^p\), \(1\le p<\infty \). By continuity of h and the dominated convergence theorem (see, Klenke 2007, Corollary 6.26), there exists a \(N_h\) such that

for all \(n\ge N_h\). Thus, we have

for all \(n\ge N_h\). Let \(\varepsilon \rightarrow 0\). Then, we obtain \(\lim _{n\rightarrow \infty } \partial _{S_t} f_t(S_t^n) = \partial _{S_t} f_t(S_t^*)\) in \(\mathcal {L}^q\). Finally, taking \(p^{-1}+q^{-1}=1\), \(\lim _{n\rightarrow \infty } \partial _{F(0,t)} f_t(S_t^n) = \partial _{F(0,t)} f_t(S_t^*)\) in \(\mathcal {L}^1\) follows by combining the convergence of \(\partial _{S_t} f_t(S_t)\) in \(\mathcal {L}^p\) and the convergence of \(\partial _{F(0,t)} S_t\) in \(\mathcal {L}^q\).

J having continuous partial derivatives is totally differentiable and its derivative is given by (3.12). In this perspective, \(J'\) is weakly continuous with respect to q. \(\square \)

Proof of Proposition 3.8

To apply Danskin’s theorem (Theorem 3.5), we have to verify its assumptions. In view of Lemma 3.7, we only have to recall that the feasible solution space \(\mathcal {Q}\) is weakly compact as argued in the proof of Proposition 3.1. Hence, Theorem 3.5 or rather Corollary 3.6 provides the result. \(\square \)

Proof of Proposition 3.9

We show by backward induction that \(F_t \mapsto \mathfrak {V}_t(Q_t, F_t)\) is convex on \(\mathbb {R}^{T -t}_+\) for every \(t \in \{0,...,T -1\}\) and every valid quantity \(Q_t\). Note that, for every t, we have \(F(t,t) = S_t\) such that \(F_t \mapsto f_t(S_t(F_t))\) is convex by assumption. For \(t=T -1\) and \(Q_{T -1} \in [\underline{Q}_{T -1}, \overline{Q}_{T -1}]\), we have

which, as a pointwise maximum over a set of convex functions, is convex in \(F_{T -1}\).Footnote 58

We now move from t to \(t-1\). Let \(Q_{t-1} \in [\underline{Q}_{t-1}, \overline{Q}_{t-1}]\). By induction assumption, \(F_{t} \mapsto \mathfrak {V}_{t}(Q_{t-1} + q_{t-1}, F_{t})\) is convex for every \(q_{t-1} \in [\underline{q}_{t-1}, \overline{q}_{t-1}]\). For fixed \(\Delta W(t-1)\), the function \(g_{t-1}(F_{t-1}, \Delta W(t-1))\) is affine in \(F_{t-1}\) by assumption, such that the mapping \(F_{t-1} \mapsto \mathfrak {V}_{t}(Q_{t-1} + q_{t-1}, g_{t-1}(F_{t-1}, \Delta W(t-1)))\) is convex. Denote by \(\varphi _{t-1}\) the density function of \(\Delta W_{t-1}\). Then, it follows that

is convex. Since \(F_{t-1} \mapsto f_{t-1}(S_{t-1})\) is convex by assumption and taking the pointwise maximum or adding functions of this kind are operations preserving convexity,

is convex, which concludes the induction step.

Because \(v: \mathbb {R}^T \rightarrow \mathbb {R}\) is convex, the theorem of Alexandrov (1939) ensures the twice totally differentiability almost everywhere. \(\square \)

Additional results

The following tables and figures present results extending our main analysis. They are ordered according to their line of occurrence/reference in the main text (Tables 9, 10, 11, 12 and Figs. 12, 13, 14, 15, 16).

Additional derivations and discussions

Derivation of drift term (2.26) Based on the solution (2.21) of the spot price process in the multi-factor framework, we obtain

which implies

It follows that

With \(\int _0^t \exp (-2\vartheta (t-s)) ds = \frac{1}{2\vartheta }(1-\exp (-2\vartheta t))\), we get

where

Thus we have obtained the drift term (2.26). \(\square \)

Error propagation Uncertainty in continuation values (emerging from, for example, approximation error in the LSM) directly influences the exercise strategy and thus fair value and sensitivity estimates. To analyse the impact of such uncertainty in general, we perform a simple simulation study. That is, in our benchmark setting with three state variables and \(N = 1000\), we set \(^\epsilon \mathcal {C}_t^{r} = \mathcal {C}_t^{r} + \epsilon _t^r\), where \(\epsilon _t^r\) are i.i.d. standard normal random variables.Footnote 59 Table 13 reports the consequences of this procedure for our estimates, e.g., the change in the option value \(\Delta v := \,^\varepsilon v-v\). Besides changes in fair values, pathwise deltas and TFD long-term gammas, we present the changes in the expected consumption quantity \(\mathbb {E}[q^*] := \mathbb {E}[\sum _{t=0}^{T -1}q^*_t]\). As expected, the value estimate is reduced in all cases. In most cases, expected consumption and deltas, which are closely related, also decrease. Gamma changes occur in both directions.

Average \(R^2\) in least-squares procedure dependent on \(\vartheta \). a B-TSLS. b P-TSLS. For the basic (B-TSLS) and the piecewise (P-TSLS) two-stage least-squares procedures introduced in Sect. 2.2.3, this figure plots the resulting average regression \(R^2\) dependent on the short-term volatility decay parameter \(\vartheta \). We consider data for 48 front months in both cases. The maximization leads to optimal \(\vartheta \) choices of 0.990 and 1.861 in the B-TSLS and P-TSLS approach, respectively

Sample returns with fitted volatility functions (B-TSLS). a\(R^2 = 0.7533\). b\(R^2 = 0.9517\). c\(R^2 = 0.8957 \). d\(R^2 =0.5843\). e\(R^2 = 0.5092\). f\(R^2 = 0.1186\). g\(R^2 = 0.7288\). h\(R^2 = 0.1270\). This figure plots sample log returns for 24 (a–f) and 48 (g, h) front months with volatility functions fitted according to our B-TSLS procedure and corresponding 95% confidence intervals

Normalized piecewise seasonal volatility functions. a\(f_3(t,T)\). b\(f_4(t,T)\). c\(f_5(t,T)\). d\(f_6(t,T)\). e\(f_7(t,T)\). f\(f_8(t,T)\). In our P-TSLS regression approach, we capture the seasonal volatility for each season spread individually. Formally, we use six normalized volatility functions \(f_k\) given by Eq. (2.18). We set \((c_{\min }, c_{\max }) = (0,18)\) for \(k=3\), \((c_{\min }, c_{\max }) = (18,24)\) for \(k=4\), \((c_{\min }, c_{\max }) = (30,36)\) for \(k=5\), etc. The functions \(f_k\), \(k=3,...,8\), without correction term \(\mu _k(t,T)\), are plotted above

Sample returns with fitted volatility functions (P-TSLS). a\(R^2 = 0.9479\). b\(R^2 = 0.9855\). c\(R^2 = 0.8802\). d\(R^2 = 0.4870\). This figure plots sample log returns for 48 front months with volatility functions fitted according to our P-TSLS procedure and corresponding 95% confidence intervals

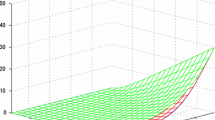

Simulated forward curves. a Path \(n = 1\). b Path \(n = 2\). c Path \(n = 3\). This figure exemplarily plots forward prices derived from our simulation procedure which is based on the discretized version of the multi-factor PFC model (2.1) with volatility functions (2.6) and estimates taken from Table 3. For each day in the period from October 1, 2014 to September 30, 2016, we display the current forward prices (in €/MWh) of the respective next 36 months

Different random seeds In our analysis, we fix the random seed for two reasons. First, we ensure that the value, delta and gamma estimates correspond to each other because they are calculated based on the same price paths. Second, we opt for common random numbers because they are a variance reduction technique typically used when estimates are drawn from more than one simulated scenario. While finite differences derivative estimates are naturally biased (see, Glasserman 2003, chpt. 7.1), this dependent sampling method does not introduce additional bias.Footnote 60

To illustrate the variance reduction, we consider the forward difference of \(\delta \), i.e.,

where \(\Delta F_0 = \varepsilon \cdot dF_0\). Case (i) reflects the independent (with different random seeds) simulation of \(v(F_0)\) and \(v(F_0 + \Delta F_0)\). We then have

under the assumption that \(\text {Var}(v(F_0))\) is continuous in \(\varepsilon \). Consequently, the variance of the estimator \((v(F_0 + \Delta F_0) - v(F_0))/\varepsilon \) explodes (converges to infinity at rate \(1/\varepsilon ^2\)) for \(\varepsilon \rightarrow 0\) and there is no hope of obtaining reasonable sensitivity estimates. Case (ii) occurs (under some mild conditions) when common random numbers are used for the simulations at \(F_0\) and \(F_0 + \Delta F_0\) (see L’Ecuyer and Perron 1994). Here, the overall variance of the derivative estimator stays bounded for \(\varepsilon \rightarrow 0\). These considerations similarly hold for the regression delta estimates and for our second-order sensitivity estimates.

Despite this advantage, using (fixed or variable) random numbers always introduces a Monte Carlo error. To quantify this error, we analyse the distributions of our estimators for different random seeds. Specifically, we obtain the sampling distributions of the fair value, pathwise delta and TFD long-term gamma estimators (of our benchmark approach) using \(S = 1000\) distinct seeds. All other settings remain unchanged. That is, the Monte Carlo error corresponds to \(N = 1000\) simulated price paths. Figure 17 presents our results for the contracts with \(Q_{\min } = 60\cdot i\) and \(Q_{\max } = 180\), \(i = 0,1,2,3\).Footnote 61

Estimator distributions under variable random seeds. For contracts with \(Q_{\min } = 60\cdot i\) and \(Q_{\max } = 180\), \(i = 0,1,2,3\), and based on \(S = 1000\) different random seeds, this figure shows the histograms of the fair value, pathwise delta and TFD long-term gamma estimators (of our benchmark approach) reflecting the Monte Carlo error related to \(N = 1000\) simulated price paths

Because of our low number of \(N = 1000\) simulated price paths, we can observe non-negligible Monte Carlo error. The standard deviation of our estimators is naturally related to the magnitude of the estimated sensitivity. For example, the pathwise delta estimator of the inflexible contract with \(Q_{\min } = 180\) has a very low standard error because the option’s gamma is nearly zero. To obtain more precise estimates and more narrow distributions, we could increase N, which significantly increases computation time. However, as pointed out in Sect. 4.2, we can illustrate all features and the proper functioning of our approach based on this sample size.

Optimal bandwidth choice We assume that v is three times continuous (directional) differentiable in a neighborhood of \(F_0\). We elaborate the estimation procedure for the overall gamma in the forwards approach, i.e., for the second-order derivative of v in the direction \(d F_0 = (1,...,1)'\). We denote by \(v', v''\) etc. the derivatives in this direction.

By Taylor expansion, we have \(\delta (F_0 + \Delta F_0) = \delta (F_0) + \varepsilon _N \delta '(F_0) + \frac{1}{2} \varepsilon _N^2 \delta ''(F_0 + \xi dF_0)\), where \(\xi \in [0, \varepsilon _N]\). Thus, for the estimator’s bias, we get

as \(N\rightarrow \infty \). We write \(y_n = o(x_n)\), if \(\lim _{n\rightarrow \infty } |\frac{y_n}{x_n}|=0\), and \(y_n = \mathcal {O}(x_n)\), if \(\limsup _{n\rightarrow \infty } |\frac{y_n}{x_n}|<\infty \). For the variance of the estimator, we have

Furthermore, we define

Because we use common random numbers, we have \(\lim _{N\rightarrow \infty } q^*_t(F_0 + \Delta F_0) = q^*_t(F_0)\) almost surely for every t, which implies \(\lim _{N\rightarrow \infty } \mathcal {V}_\gamma (\varepsilon _N) = 0\). Thus, what is left is to determine the speed of the convergence. Note that simulating \(F_t(F_0)\) and \(F_t(F_0 + \Delta F_0)\) with independent samples would cause \(\mathcal {V}_\gamma (\varepsilon _N) = \mathcal {O}(1)\) because

Because the payoff is pathwise discontinuous, we do not expect \(\mathcal {V}_\gamma (\varepsilon _N) = \mathcal {O}(\varepsilon _N^2)\) such that the overall variance of the estimator stays bounded as \(\varepsilon _N \rightarrow 0\).Footnote 62

We now present some heuristics to argue why we have at least \(\mathcal {V}_\gamma (\varepsilon _N) = \mathcal {O}(\varepsilon _N)\). Because of

we have \(S_t(F_0 + \Delta F_0) - S_t(F_0) = \mathcal {O}(\varepsilon _N)\). For fixed \(r_t\), it follows that \(\mathcal {C}_t^{r_t}(F_t + \Delta F_t) - \mathcal {C}_t^{r_t}(F_t) = \mathcal {O}(\varepsilon _N)\) because \(\mathcal {C}_t^{r_t}\) is differentiable in \(F_t\) which can be seen by applying our previous results to the subproblem (3.5). Thus, toggling between \(F_0\) and \(F_0 + \Delta F_0\) shifts the exercise condition \(S_t-\mathscr {K}+ \mathcal {C}_t^{r_t+1} - \mathcal {C}_t^{r_t}\) in \(\mathcal {O}(\varepsilon _N)\). Since

the probability that the exercise condition crosses zero on day t for fixed \(r_t\) is \(\mathcal {O}(\varepsilon _N)\). Because we consider a discrete finite time horizon and a digital optimal control, there is only a finite number of exercise conditions which could lead to a discontinuous payoff. It follows that

i.e., the probability that the overall payoff is discontinuous in \([F_0, F_0 + \Delta F_0]\) converges to zero as \(\mathcal {O}(\varepsilon _N)\). Bridging discontinuities costs \(\mathcal {O}(1)\), whereas we have \(\mathcal {O}(\varepsilon _N)\) for a continuous payoff. Let \(A := \{\omega \in \Omega : X(w)\text { is continuous in }[F_0, F_0 + \Delta F_0]\}\). It follows

and

Hence, we have

We now turn to Monte Carlo methods. For \(\varepsilon _N \in \{-2, -1.5, -1, -0.5, 0, 0.5, 1, 1.5, 2\}\), we use the corresponding pathwise delta estimates in the OLS regression

In addition, we set \(^n\delta (\varepsilon _N) := \sum _{t=0}^{T -1} \frac{\partial \,\, ^nS_t}{\partial F(0, t)} \cdot \,^n q^*_t(F_0 + \Delta F_0)\), calculate

for each \(\varepsilon _N\) and then perform the regression

We report the estimates of \({\delta }''(F_0)\) and \({\mathcal {V}}'_\gamma \) in Table 14. These values, related to the bias and variance of our gamma estimator, are then used to derive the optimal bandwidth parameter minimizing (4.10), which is also presented in Table 14. \(\square \)

Pseudo code

Rights and permissions

About this article

Cite this article

Kohrs, H., Mühlichen, H., Auer, B.R. et al. Pricing and risk of swing contracts in natural gas markets. Rev Deriv Res 22, 77–167 (2019). https://doi.org/10.1007/s11147-018-9146-x

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11147-018-9146-x