Abstract

This study reports on the impact of exposure to tax dilemmas on tax morale. We focus on young adults in their “impressionable years” and with little or no previous tax exposure in order to estimate the impact of actual (albeit experimental) exposure to tax dilemmas on their self-declared tax morale. First, we ascertain the participants’ (N = 385), representation and attitudes towards tax, and second, we observe the impact of facing tax decisions on their present and future level of tax compliance. This allows us to investigate, in the realm of taxation, the generic question of knowing how one’s history (and one’s decisions) influences one’s ethical representations and attitude. Although of less external validity than studies using naturally occurring events or historical periods, the use of an experimental simulation enables us to investigate the three different dimensions that could shape people’s personal history: acting, experiencing and observing. Thanks to an interactive and systemic approach, participants are invited to make decisions in a tax context, to experience tax “events” and are given the opportunity to observe both their own behavior, that of others as well as the consequences of those actions, and repeat and test those three different steps several times. We find that the simulation tends to reduce honesty and ethical concerns with respect to taxation, a decrease in tax morale. This reduction seems to be driven by those subjects who were actually facing a tax dilemma and have to make a compliance decision. Other subjects, only observing or experiencing the effects of low tax compliance, are only marginally affected. One possible interpretation is that individuals have an initial overconfidence in their propensity to tax compliance and tax morale, which is challenged by their own decisions in typical dilemmas.

Similar content being viewed by others

Notes

We use the first three rounds, and not just the first one, to make sure that participants become familiar with the environment, their roles, and the consequences of their actions within the game.

Rather than seeing this as a weakness, we think it is reassuring not to obtain a statistically large effect, which would indicate an experimental demand effect: it seems unreasonable to have individuals’ tax morale be strongly affected by a one-hour experimental simulation.

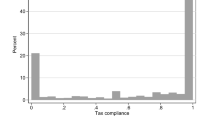

Appendix d also provides the same figures but for the TAX questions. The analysis and interpretation are similar.

In particular, except for minimal secondary aspects, it is notoriously difficult in France to cheat on income tax if you are an employee,as employers declare wages and salaries directly to the tax authorities.

References

Abdixhiku L, Krasniqi B, Pugh G, Hashi I (2017) Firm-level determinants of tax evasion in transition economies. Econ Syst 41(3):354–366

Ahmed E, Braithwaite V (2005) A need for emotionally intelligent policy: linking tax evasion with higher education funding. Legal Crim Psych 10(2):291–308

Alesina A, Fuchs-Schündeln N (2007) Good-bye lenin (or not?): the effect of communism on people’s preferences. The Am Econ Rev 97(4):1507–1528

Allingham M, Sandmo A (1972) Income tax evasion: a theoretical analysis. J Pub Econ 1(2–3):323–338

Alm J, Kirchler E, Muehlbacher S (2012) Combining psychology and economics in the analysis of compliance: from enforcement to cooperation. Econ Policy 42(2):133–151

Alm J, Gomez JL (2008) Social capital and tax morale in Spain. Adv Econ Analysis Policy 38(1):73–87

Alm J, Malézieux A (2021) 40 years of tax evasion games: a meta-analysis. Exp Econ 24(3):699–750

Alm J, McClellan C (2012) Tax morale and tax compliance from the firm’s perspective. Kyklos 65(1):1–17

Alm J, Torgler B (2006) Culture differences and tax morale in the United States and in Europe. J Econ Psych 27(2):224–246

Alm J, Sanchez I, de Juan A (1995) Economic and noneconomic factors in tax compliance. Kyklos 48(1):3–18

Alstadsæter A, Johannesen N, Zucman G (2019) Tax evasion and inequality. Am Econ Review 109(6):2073–2103

Andreoni J (1988) Why free ride? Strategies and learning in public goods experiments. J Pub Econ 37(3):291–304

Andreoni J, Erard B, Feinstein J (1998) Tax compliance. J Econ Lit 36:818–860

Ajzen I (1985) From intentions to actions: a theory of planned behavior. In: Kuhn J, Beckman J (eds) Action-control: from cognition to behavior. Springer, Heidelberg, pp 11–39

Barkworth JM, Murphy K (2015) Procedural justice policing and citizen compliance behaviour: the importance of emotion. Psych, Crime Law 21(3):254–273

Bazerman MH, Tenbrunsel AE (2012) Blind spots: Why we fail to do what’s right and what to do about it. Princeton University Press, USA

Becker GS (1968) Crime and punishment: an economic approach. J Pol Econ 76(2):169–217

Beer S, Kasper M, Kirchler E, Erard B (2020) Do audits deter or provoke future tax noncompliance? Evidence on self-employed taxpayers. Cesifo Econ Stud 2019:1–17

Besley T, Jensen A, Persson T. (2019) Norms, enforcement, and tax evasion (No w25575). National Bureau of Economic Research.

Biasucci C, Prentice R (2020) Behavioral ethics in practice: why we sometimes make the wrong decisions. Routledge.

Bicchieri C (2005) The grammar of society: the nature and dynamics of social norms. Cambridge University Press, UK

Bicchieri C, Xiao E (2009) Do the right thing: but only if others do so. J Behav Dec Mak 22(2):191–208

Blanken I, van de Ven N, Zeelenberg M (2015) A meta-analytic review of moral licensing. Pers Soc Psychol Bull 41(4):540–558

Blaufus K, Bob J, Otto PE, Wolf N (2017) The effect of tax privacy on tax compliance–An experimental investigation. Eur Acc Rev 26(3):561–580

Botella M, Fürst G, Myszkowski N, Storme M, Pereira Da Costa M, Luminet O (2015) French validation of the overexcitability questionnaire 2: psychometric properties and factorial structure. J Perso Ass 97(2):209–220

Braithwaite V (2003) Dancing with tax authorities: motivational postures and non-compliant actions. Tax Dem 3:15–39

Braithwaite V (2002) Taxing democracy. Ashgate Publishing Ltd, England

Chan CW, Troutman CS, O’Bryan D (2000) An expanded model of taxpayer compliance: empirical evidence from the United States and Hong Kong. J Int Acc, Audit Tax 9(2):83–103

Cogley T, Sargent T (2008) The market price of risk and the equity premium: a legacy of the great depression. J Monet Econ 55:454–476

Coricelli G, Rusconi E, Villeval MC (2014) Tax evasion and emotions: an empirical test of re-integrative shaming theory. J Econ Psy 40:49–61

Cummings RG, Martinez-Vazquez J, McKee M, Torgler B (2009) Tax morale affects tax compliance: evidence from surveys and an artefactual field experiment. J Econ Behav Organ 70(3):447–457

D'Attoma J, Volintiru C, Malezieux A (2018) Gender, social value orientation, and tax compliance, CESifo Econ St.

DeBacker J, Heim BT, Tran A (2015) Importing corruption culture from overseas: evidence from corporate tax evasion in the United States. J Fin Econ 117(1):122–138

Dell’Anno R (2009) Tax evasion, tax morale and policy maker’s effectiveness. The J Socio-Econ 38(6):988–997

Danzer A, Danzer N, Fehr E (2016) The Behavioral and Psychological Consequences of a Nuclear Catastrophe. The Case of Chernobyl, mimeo.

Doerrenberg P, Peichl A (2013) Progressive taxation and tax morale. Public Choice 155(3–4):293–316

Dunn P, Farrar J, Hausserman C (2016) The influence of guilt cognitions on taxpayers voluntary disclosures. J Bus Ethics 148(3):689–701

Elffers H, Weigel RH, Hessing DJ (1987) The consequences of different strategies for measuring tax evasion behavior. J Econ Psy 8(3):311–337

Eriksen K, Fallan L (1996) Tax knowledge and attitudes towards taxation: a report on a quasi-experiment. J Econ Psy 17:387–402

Falk A, Ichino A (2006) Clean evidence on peer effects. J Lab Econ 24:39–57

Fallan L (1999) Gender, exposure to tax knowledge and attitudes towards taxation: an experimental approach. J Bus Ethics 18:173–184

Fehr E, Gächter S (2002) Altruistic punishment in humans. Nature 415(6868):137

Fischer CM, Wartick M, Mark M (1992) Detection probability and taxpayer compliance: a review of the literature. J Acc Lit 11:1–46

Friedland N, Maital S, Rutenberg A (1978) A simulation study of income tax evasion. J Public Econ 10:107–116

Giuliano P, Spilimbergo A (2009) Growing up in a recession: Beliefs and the macroeconomy. NBER Working Paper 15321.

Górecki MA, Letki N (2020) Social norms moderate the effect of tax system on tax evasion: evidence from a large-scale survey experiment. J Bus Ethics 172:727

Gosling SD, Rentfrow PJ, Swann WB Jr (2003) A very brief measure of the big five personality domains. J R Personal 37:504–528

Grasmick HG, Bursik RJ Jr, Kinsey KA (1991) Shame and embarrassment as deterrents to noncompliance with the law: the case of an anti-littering campaign. Env and Behav 23(2):233–251

Grasso LP, Kaplan SE (1998) An examination of ethical standards for tax issues. J Acc Ed 16(1):85–100

Groenland EA, Van Veldhoven GM (1983) Tax evasion behavior: a psychological framework. J Econ Psy 3(2):129–144

Guerra A, Harrington B (2018) Attitude–behavior consistency in tax compliance: a cross-national comparison. J Econ Behav Organ 156:184–205

Halla M (2012) Tax morale and compliance behavior: first evidence on a causal link. The BE J Econ Anal Policy 12(1):1–21

Hashimzade N, Epifantseva Y (Eds) (2017) The Routledge Companion to Tax Avoidance Research. Routledge.

Hessing DJ, Elffers H, Weigel RH (1988) Exploring the limits of self-reports and reasoned action: an investigation of the psychology of tax evasion behavior. J Pers and Soc Psy 54(3):405

Hofmann E, Hoelzl E, Kirchler E (2008) Preconditions of voluntary tax compliance: knowledge and evaluation of taxation, norms, fairness, and motivation to cooperate. Zeitschrift Für Psychologie/j Psy 216(4):209–217

Jacquemet N, Luchini S, Malézieux A, Shogren J (2019) A psychometric investigation of the personality traits underlying individual tax morale. The BE J Econ Anal Policy 19(3):1935

Kemme DM, Parikh B, Steigner T (2020) Tax morale and international tax evasion. J World Bus 55(3):101052

Kirchler E (2007) The economic psychology of tax behavior. Cambridge University Press, UK

Kirchler E, Maciejovsky B, Schneider F (2003) Everyday representations of tax avoidance, tax evasion, and tax flight: do legal differences matter? J Econ Psy 24(4):535–553

Krosnick JA, Alwin DF (1989) Aging and susceptibility to attitude change. J Pers and Soc Psy 57:416–425

Lago-Peñas I, Lago-Peñas S (2010) The determinants of tax morale in comparative perspective: Eevidence from European countries. Eur J Pol Econ 26(4):441–453

Lenz H (2020) Aggressive tax avoidance by managers of multinational companies as a violation of their moral duty to obey the law: a Kantian rationale. J Bus Ethics 165(4):681–697

Love E, Salinas TC, Rotman JD (2020) The ethical standards of judgment questionnaire: development and validation of independent measures of formalism and consequentialism. J Bus Ethics 161(1):115–132

Luttmer EF, Singhal M (2014) Tax morale. J Econ Persp 28(4):149–168

Malézieux A (2018) A practical guide to setting up your tax evasion game. J Tax Admin 4(1):107–127

Malmendier U, Nagel S (2011) Depression babies: do macroeconomic experiences affect risk taking? Quart J Econ 126(1):373–416

Malmendier U, Nagel S (2013) Learning from inflation experiences, mimeo. University of California, Berkeley

Malmendier U, Nagel S (2015) Learning from inflation experiences. The Quart J Econ 131(1):53–87

Malmendier U, Wellsjo A (2020) Rent or Buy? The Role of Lifetime Experiences on Homeownership within and Across Countries. CEPR Discussion Paper No. DP14935.

Malmendier U, Nagel S, Yan Z (2021) The making of hawks and doves. J Monet Econ 117:19–42

Mascagni G (2018) From the lab to the field: a review of tax experiments. J Econ Surv 32(2):273–301

OECD (2013) Tax and development: What drives tax morale? Organization for Economic Cooperation and Development, http://www.oecd.org/ctp/tax-global/what-drives-tax-morale.pdf Retrieved January 4, 2021

Oreopoulos P, Von Wachter T, Heisz A (2012) The short- and long-term career effects of graduating in a recession: hysteresis and heterogeneity in the market for college graduates. Am Econ J: App Econ 4(1):1–29

Oz Yalama G, Gumus E (2013) Determinants of tax evasion behavior: empirical evidence from survey data. Int Bus and Manage 6(2):15–23

Plott CR (1996) Rational individual behaviour in markets and social choice processes: The discovered preference hypothesis. In KJ Arrow et al. (Eds) The rational foundations of economic behaviour: Proceedings of the IEA Conference held in Turin, Italy, IEA Conference 114: 225–250, New York, St. Martin’s Press, Macmillan Press in association with the International Economic Association, London.

Riahi-Belkaoui A (2004) Relationship between tax compliance internationally and selected determinants of tax morale. J Inter Acc, Audit and Taxation 13(2):135–143

Sandmo A (2005) The theory of tax evasion: a retrospective view. Nat Tax J 58:643–663

Slemrod J (2007) Cheating ourselves: the economics of tax evasion. J Econ Persp 21(1):25–48

Schmölders G (1959) Fiscal psychology: a new branch of public finance. Nat Tax J 12(4):340–345

Slovic P (1995) The construction of preference. Am Psy 50(5):364

Song YD, Yarbrough TE (1978) Tax ethics and taxpayer attitudes: a survey. Pub Admin Rev 38(5):442–452

Spicer MW, Lundstedt SB (1976) Understanding tax evasion. Pub Fin 21(2):295–305

Spire A (2018) Résistances à l’impôt, attachement à l’Etat-Enquête sur les contribuables français. Le Seuil, Paris

Storme M, Tavani JL, Myszkowski N (2016) Psychometric properties of the French ten-item personality inventory (TIPI). J Ind Diff 37(2):81–87

Srinivasan T (1973) Tax evasion: a model. J Pub Econ 2(3):339–346

Torgler B (2005) Tax morale in Latin America. Pub Choice 122(1–2):133–157

Torgler B (2006) The importance of faith: tax morale and religiosity. J Econ Beh Org 61(1):81–109

Torgler B (2007) Tax compliance and tax morale: a theoretical and empirical analysis. Edward Elgar Publishing, Cheltenham UK

Torgler B (2003) Tax morale in transition countries. Post-Communist Econ 15(3):357–381

Torgler B, Werner J (2005) Tax morale and fiscal autonomy: evidence from Germany. Pub Fin Manage 5(4):460–485

Zizzo DJ (2010) Experimenter demand effects in economic experiments. Exp Econ 13(1):75–98

Acknowledgements

The authors would like to thank Prof E Kirchler, Prof J. Alm and Prof L Mittone for the insightful and valuable comments and questions made at the 6th Shadow Economy Conference–Tax Evasion and Economic Inequality held at the Department of Economics and Management at the University of Trento (Italy), July 11–13, 2019.

Funding

Funding and technical assistance for this research was received from the ANR PIA 16-DUNE-0004 project Ephemer (Ethique et Pédagogie Holoptique pour un EnseigneMEnt en Réseau).

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendices

Appendix

Appendix A. Pre- and Post-Questionnaires

2.1 Pre-Questionnaire (translated from french)

Please insert your student number here:

2.2 PART 1: Ten-Item Personality Inventory (TIPI)

2.2.1 Please answer the questions below:

Totally disagree | Disagree | Disagree somewhat | Indifferent | Agree somewhat | Agree | Totally agree | |

|---|---|---|---|---|---|---|---|

I see myself as: extraverted; enthusiastic | |||||||

I see myself as: critical, quarrelsome | |||||||

I see myself as: Dependable, self-disciplined | |||||||

I see myself as: Anxious, easily upset | |||||||

I see myself as open to new experiences, complex | |||||||

I see myself as: Reserved, quiet | |||||||

I see myself as: sympathetic, warm | |||||||

I see myself as: disorganised, careless | |||||||

I see myself as: Calm, emotionally stable | |||||||

I see myself as: Conventional, uncreative |

2.3 PART 2a: Questions on civic duties (WVS)

For the following conducts, please indicate whether it appears to you always justified, never justified, or something in between, on a scale from 1 to 10, 1 meaning never justified while 10 means always justified.

2.4 Question 1

Claiming government benefits to which you are not entitled.1 2 3 4 5 7 8 9 10.

2.5 Question 2

Avoiding a fare on public transport.1 2 3 4 5 7 8 9 10.

2.6 Question 3

Stealing property.1 2 3 4 5 7 8 9 10.

2.7 Question 4

Cheating on taxes if you have a chance.1 2 3 4 5 7 8 9 10.

2.8 Question 5

Someone accepting a bribe in the course of their duties.1 2 3 4 5 7 8 9 10.

2.9 PART 2b: Questions on Taxation

In a scale from 1 (strongly disagree) to 5 (totally agree) please answer the following questions:

2.10 Question 1

Most people do not cheat on their taxes 1 2 3 4 5.

2.11 Question 2

I prefer to work for a company that pays its taxes in France rather than in a tax haven1 2 3 4 5.

2.12 Question 3

In the future, I will declare my income tax honestly. 1 2 3 4 5

2.13 Question 4

It is justified to cheat on taxes if the opportunity arises. 1 2 3 4 5

2.14 Question 5

Tax flight is unfair towards other taxpayers 1 2 3 4 5.

2.15 Post-Questionnaire

2.15.1 PART 2a: Questions on civic duties (WVS)

For the following conducts, please indicate whether it appears to you always justified, never justified, or something in between, on a scale from 1 to 10, 1 meaning never justified while 10 means always justified.

2.16 Question 1

To receive social benefits you are not allowed to.1 2 3 4 5 7 8 9 10.

2.17 Question 2

To free-ride public transportation.1 2 3 4 5 7 8 9 10.

2.18 Question 3

Theft.1 2 3 4 5 7 8 9 10.

2.19 Question 4

To cheat tax if the opportunity arises.1 2 3 4 5 7 8 9 10.

2.20 Question 5

To accept bribes on the job.1 2 3 4 5 7 8 9 10.

2.21 PART 2b: Questions on Taxation

In a scale from 1 (strongly disagree) to 5 (totally agree) please answer the following questions:

2.22 Question 1

Most people do not cheat on their taxes 1 2 3 4 5.

2.23 Question 2

I prefer to work for a company that pays its taxes in France rather than in a tax haven1 2 3 4 5.

2.24 Question 3

In the future, I will declare my income tax honestly. 1 2 3 4 5

2.25 Question 4

It is justified to cheat taxes if the opportunity arises 1 2 3 4 5.

2.26 Question 5

Tax flight is unfair towards other taxpayers 1 2 3 4 5.

Appendix B: Principal Component Analysis

To get an overall vision of the changes induced by the tax simulation, we ran a Principal Component Analysis on the five questions. Usual diagnostics suggest keeping two components for analysis (when applying a threshold for the eigenvalue of 1 or more). Two components account for around 65% of the variance, and three 80%.

The typical variable factor maps help interpreting the PC: the y-axis corresponds to the empirical norm, meaning the proportion of individuals being honest with respect to taxes (Question 1 of the questionnaire almost exclusively), while the x-axis seems to correspond to the individual attitude of the respondent.

See Figs.

Amount of explained variance by factors

2 and

Representation of variables with respect to factors (“Dim”)

3.1 C – Validity of the 5-item questionnaire

A standard reliability analysis shows (see Table below), we obtain a satisfactory level of validity when dropping the first question. This is in line with our intuition that Question 1 measured something different. It is also fully consistent with the results obtained in the Principle Component Analysis (PCA).

See Table

3.2 D—Additional statistical analyses

See Table

Rights and permissions

About this article

Cite this article

Deglaire, E., Daly, P. & Le Lec, F. Exposure to tax dilemmas deteriorate individuals' self-declared tax morale. Econ Gov 22, 363–397 (2021). https://doi.org/10.1007/s10101-021-00262-x

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10101-021-00262-x