Abstract

The central role of Value-at-Risk (VaR) within bank market risk regulation received significant criticism from financial media and government investigations into the events of the 2007–2009 financial crisis. Impending reform of bank market risk regulation under the Fundamental Review of the Trading Book (FRTB) demotes VaR, replacing it with a layered framework centred on expected shortfall (ES). However, many of these criticisms assume full integration of internal and regulatory market risk models and further, a linear relationship between risk models and regulatory capital. We examine bank practitioners’ perspectives and experienced realities to better understand the operational relationship between internal and regulatory market risk models, and between risk models and capital. This has important policy implications for the efficacy of the reforms to banking regulation, financial stability and navigating the dichotomy of private and public interests.

Similar content being viewed by others

Introduction

The complex nature of managing bank market risk under competing commercial and societal needs necessitates careful consideration of the operational mechanisms used. Bank regulation is expected to oversee bank risk-taking with a public interest mandate [1]. However, domestic and global banking regulation received significant criticism in the aftermath of the financial crisis [2]. The resultant nationalisation of some private banks and socialisation of bank losses significantly damaged the credibility of the banking regulatory framework [3,4,5,6,7,8,9,10]. Moreover, Langley [11] outlines how mispricing or under-pricing of risk became a common characterisation of the criticisms of the regulatory framework and the underpinning capital. Value-at-risk (VaR) models are the central market risk measures of Basel II, used as the basis for determining market risk regulatory capital for banks with approval for their internal model approach (IMA). This is the key lever used to manage the prudential risk-taking of banks. These criticisms of VaR hinge on its perceived inability to curtail the risk-taking behaviour of banks, and further, that it could not ensure adequate capital buffers to prevent the socialisation of risk. The criticism often assumes the same risk model is used for regulatory and internal risk management purposes. However, Mehta et al. [12] find that 50% of banks reviewed use different market risk models for internal and regulatory purposes. We argue that this decoupling of banks’ internal risk management practice from the regulatory requirements has deepened further with the impending implementation of FRTB. The phenomenon of decoupling in this context is not addressed in the current literature or policy documentation.

The context of why the decoupling of internal practice and regulatory market risk management is an important issue centres on the opprobrium of VaR. VaR became a cynosure of public anger at the risk-taking behaviour of banks. VaR received particular criticism for its role with headlines like: ‘The number that killed us’ [13] (p. 1); ‘… widespread institutional reliance on VaR was a terrible mistake’ [14] (p. 2); ‘The monster of VaR has not gone away’ [15] (p. 1). The assumption that the internal practice role of VaR is fully integrated with the regulatory role is implicit in the criticism of VaR’s significance in the financial crisis. The criticisms assume that VaR directs behaviour, controls risk-taking and determines sufficient capital to cover market losses. This is a significant overestimation of the power of VaR and implies that practitioners slavishly follow the models [16]. Indeed, banks may also have used the models as a protective foil of ‘mechanical’ objectivity [17, 18]. Furthermore, criticisms characterising market risk bank regulation as neoliberal self-regulation and/or regulatory capture infer that internal VaR is a conduit of regulation, which therefore assumes integration of internal practice and regulatory VaR [19,20,21,22,23]. This paper examines (1) whether the internal practice VaR is decoupled from regulatory VaR and its successor expected shortfall (ES) and importantly, decoupled from regulatory capital, and (2) whether the impending implementation of FRTB has compounded this and deepened this decoupling effect. If decoupling of market risk regulation and internal risk management practices exists (and is deepening), it has serious implications for the efficacy of impending regulatory reform and its mandate to ensure a stable global banking system.

Hutter [16] commends the need for research that examines the action of regulation and risk-based initiatives. She identifies the concern that the risk tools could be followed slavishly, that their limitations need to be acknowledged, but also that they can be used as a means of shifting blame:

‘Moreover, they might have the added benefit of distancing any blame-shifting should a crisis emerge, that is they might allow regulators to appeal to seemingly objective models against which they made their allocative decisions’ [16] (p. 12)

Her paper predates the financial crisis and addresses the wide application of risk-based regulation across many sectors but is hugely prescient of what transpired with the financial crisis. There is a dominant narrative that banks were undercapitalised because of inadequacies in their proprietary risk models. The assumption of linearity between the internal and regulatory VaR/ES risk model and capital (and thereby risk behaviour) enforces this narrative and shields questions about the foundational soundness of risk-based regulation. Our study examines the veracity of this linear assumption, whether in practice there is significant decoupling of internal and regulatory VaR/ES risk models and between the risk models and regulatory capital, and whether this has been accelerated with FRTB.

This study contributes to the literature examining the impact and efficacy of banking regulation by examining and holding up to view how regulation is experienced by practitioners. This research has implications for the full realisation of regulatory reform. If the regulatory framework seeks to effectively influence risk-taking behaviour, ensure the stability of the banking system, and act in the interest of society, multiple perspectives on its current and future implementation are required. This research yields insights from banking and regulatory practitioners into the decoupling of internal and regulatory market risk models and, importantly, decoupling with regulatory capital.

The paper begins by setting the context in terms of VaR’s role within Basel II capital-based banking regulation and the impending changes under FRTB, including the demotion of VaR. We then explore the theoretical basis of the study, examining risk-based and capital-based bank regulations. Then follows an outline of our methodology, which deploys interviews with participants from banking including risk managers, traders, and regulators. We then present our findings and analysis of the interviews before concluding.

Background: regulation of market risk

Before we can examine the decoupling of internal and regulatory VaR/ES risk models, and regulatory capital and risk models, we need to revisit to principles of capital regulation. The legitimacy of regulation hinges on the assessment that bank activity impacts the domestic economy and yet banks’ private interests’ decision-making may not be aligned to this public interest. This forms the basis for the existence of bank regulation to reconcile public and private interests. Bank regulation evolved from ‘lender of last resort’ to deposit insurance and structural supervision [24], before developing into a capital-based system.

Market risk banking regulation

Before the introduction of Basel I (the Accord) in 1988, bank regulation focused on market structure, asset and liability management, foreign exchange and interest rates [1]. The increased globalisation of financial activity demanded a form of regulation that extended beyond national boundaries [25]. The formation of the Basel Committee on Banking Supervision (BCBS) in 1975 was propelled by growing global commodity and foreign exchange volatility. Further impetus was given by the failure of Bankhaus Herstatt in 1974, highlighting issues around settlement risk in the foreign exchange market. The BCBS focus was primarily on monitoring the systemic stability of the global banking system and providing advice to G10 bank governors. Subsequently, the Latin American debt crisis in 1982 prompted the Federal Reserve Board to introduce bank capital adequacy requirements and further, seek an international equivalent. This became the remit of the BCBS [26]. Basel I introduced a minimum capital requirement for credit risks of up to 8% of the loan. In 1993, it extended its remit to market risks, again taking this rigid capital ratio approach. Subsequently, banks were permitted to use their own VaR models (subject to approval) to determine their market risk regulatory capital requirements.

Following extensive consultation, a revised capital framework was issued in June 2004, which became known as Basel II. This framework introduced the three-pillar approach. The three pillars are minimum capital requirements, supervision and market disclosure. The initial focus of the Basel II framework was the risks posed by assets in the Banking Book. The Banking Book refers to assets which are assumed held until maturity, whereas the Trading Book refers to assets that are traded frequently. The different Book designations are subject to different accounting and capital requirement treatment. Goodhart [26] describes the activities in the trading book as ‘… akin to, and competitive with, those in investment houses’. The BCBS collaborated with the International Organisation of Securities Commissions (IOSCO) to develop a framework for the treatment of banks’ Trading Books. This approach was integrated into the Basel II document and in June 2006, a comprehensive framework was published. With the growth of derivatives markets, most of a bank’s market risk is in the trading book, hence, this is the focus of much of the literature on market risk modelling and the determination of market risk capital using the internal model approach (IMA), which was most commonly a VaR model. The role of VaR within the regulatory framework is heavily criticised as discussed in Sect. 2.2.

Basel II.5 is the industry label given to the collection of changes to (market) risk regulatory capital calculation following the large losses in the banking sector during the 2007–2009 financial crisis. The official BCBS document specifying the changes to market risk capital calculation (BCBS 193) was published in December 2010, with an implementation date of 31st December 2011. The key measures introduced were: Stressed VaR measure (SVaR), an Incremental Risk Charge (IRC) and a Comprehensive Risk Measure (CRM) [27]. The Stressed VaR calculated the 99% VaR calibrated on a 12 month period within the span of the financial crisis 2007–2009. A weighted average of the normal VaR and the Stressed VaR was used to determine market risk regulatory capital. The incremental risk charge was introduced to counteract issues such as the transference of assets to the trading book incentivised by lower capital charges, the market risk impact of a deterioration in creditworthiness and the inadequacy of the standard 10-day liquidity horizon. For securitised products, capital charges pertaining to the banking book were applied unless banks were permitted by their supervisor to recognise correlation-trading activities, which were then subject to the Comprehensive Risk Measure (CRM). The CRM was required to take account of cumulative risk arising from multiple defaults, credit spread risk, volatility of implied correlations, basis risk, recovery rate volatility, risk of hedge slippage and the cost of hedge rebalancing.

The regulatory changes introduced under Basel III address many key areas of concern prominent during the financial crisis of 2007–2009. These areas of concern include excessive leverage, procyclical regulatory capital requirements, market and funding liquidity, and inadequate quality and quantity of capital. The measures introduced include countercyclical buffers, capital conservation buffers, leverage and liquidity ratios. Furthermore, Basel III introduces the Output Floor which limits the benefits achieved under the internal model approach relative to the standardised approach. BCBS argue that the output floor will strengthen the principle of the level playing field between SA and IMA banks, and that it will improve the comparability of disclosures and enhance the credibility of capital calculations [28]. Capital requirements will be calculated as the higher of: (a) capital calculated using the internal model approach (where the bank has approval for their use) and (b) 72.5% of the capital requirements calculated under the standardised (or simplified standardised where appropriate) approach.

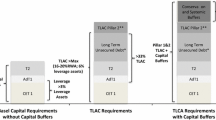

The Fundamental Review of the Trading Book (FRTB) is the market risk component of Basel III, replacing the intermediate measures brought in under Basel II.5 (Stressed VaR and IRC). The reforms under FRTB are considered so comprehensive as to be dubbed Basel IV [29,30,31]. The headline event of FRTB is the change from VaR at 99% confidence level to ES at 97.5% confidence level and follows significant literature promoting ES as a superior metric (see Danielsson et al. [32] for an early progenitor of this school of thought and Artzner et al. [33] for criteria of coherent risk measures). ES measures the average of the losses in the tail at the 2.5% significance level (1–97.5% confidence level). The promoted advantages of ES are that it satisfies the subadditivity criteria and that it is less easily gamed than VaR as the full distribution is considered in its calculation. It is recognised that implementation of FRTB will lead to an increase in capital requirements [34, 35], but that this is due to the complex layers of the FRTB framework rather than due to the change to ES at 97.5% confidence level. FRTB introduces significant changes to the approval of internal risk models through backtesting and profit and loss attribution (PLA) tests required at the trading desk level. Failure to jointly meet these desk-level backtest requirements along with the PLA tests will mean that the desk will not be authorised to use the internal model approach (IMA) (regulatory VaR/ES). For banks to be eligible to use the internal model approach, a minimum of 10% of aggregated market risk capital requirements must be derived from desks with IMA approval.

An important change under FRTB is the granulation of liquidity horizons. Under Basel II, assets held on the trading book were assumed to be of sufficient (and equal) market liquidity that the position could be unwound or hedged within ten days [36]. The FRTB documentation recognises this as a significant flaw and has aligned the liquidity horizon of various asset classes to the average time required to unwind or hedge a position in a stressed market without having a material impact on market prices [37]. FRTB introduces five levels of risk horizon from ten days to one year and assets are categorised within these levels. They argue that varying liquidity horizons is a key means of factoring market liquidity risk into their risk measure and regulatory capital. They also argue that this will reduce the incentive for arbitrage between the trading book and the banking book.

A base liquidity horizon of ten days is specified, which permits scaling from a 10-day valuation but not from 1- to 10-day. There was significant criticism of the permitted use of √h scaling rule under Basel II [32, 38]. Several empirical studies have reviewed the issue of scaling from 1- to 10-day [39,40,41,42], finding that the √h scaling rule is only appropriate for distributions that are alpha-stable normal and independent and identically distributed (i.i.d.). Otherwise, its application underestimates the h-day VaR. While there is no BCBS explanation for the ten-day base liquidity horizon, Balter and McNeil [43] justify the ten-day base horizon on the premise that ten-day market risk factor changes can be assumed to follow a Gaussian white noise process, that is, independent and identically distributed. While they acknowledge this assumption may be unlikely to be true in practice, they justify its use on the basis that it is a less problematic assumption for ten-day risk factor changes than for 1-day risk factor changes.

A further important change under FRTB, contributing to its complexity and inhibiting linear dependence on the chosen risk model, is the limitation on diversification benefits. ES is calculated at the entity level based on a shock to all approved risk factors (at appropriate liquidity horizons) and then also calculated based on a shock to a subset of risk factors while the remaining risk factors are held constant. An average of these calculations is then performed to determine the regulatory capital requirements.

Criticisms of the market risk regulatory framework

Power [23] contests the rationale of utilising VaR in market risk management as a means of countering the crude, conservative ratios with a risk-sensitive measure:

While some of the motivation for VaR as a standard for risk management was to counter regulatory conservatism, it had more to do with improving divisional control in financial organisations and charging activities and transactions with a required return hurdle for risk. [23] (p. 72)

He further argues that VaR is beyond a technical measure and represents ‘the financialisation of governance’ [23]. He presents the adoption of VaR for regulatory purposes as an appropriation of a technique that was being used to contest imposed regulatory requirements.Footnote 1 Alternatively, Lall [44] characterises this appropriation instead as a co-opting of banks’ internal models into the Basel II framework through the influence of lobby groups representing large banks. However, Young [45] argues that ‘access translating to influence’ by private interest lobby groups on the formation of the Basel II policy process was more restricted than that implied by regulatory capture. He refers to the ‘common ideational perspective of bankers and members of the BCBS’ (p. 668) as a social relationship influenced by shared contemporary wisdom, which is the context in which the Basel II policies are formulated. Carpenter and Moss [46] describe regulatory capture as the reverse of regulation for public interest: ‘regulation applied for the benefit of regulated entities’ [46]. Nonetheless, Gunningham and Rees [47] find that self-regulation in certain contexts can be an efficacious form of control. However, they find that self-regulation works most effectively when there is strong homology between the public and private interests. Albu et al. [48] find the absence of homology between practitioner knowledge and the changes being implemented can result in lower levels of compliance with the new policies or procedures. This suggests that differences between the internal and regulatory forms of market risk modelling may result in a further decoupling of internal and regulatory VaR/ES risk models.

Baud and Chiapello [22] argue that Basel II is a neoliberalisation of bank regulation, whereby ostensibly banks retain a form of self-regulation through the authorised use of their proprietary risk models. Incentivised by potential reductions in capital requirements, this self-determination is conditional on adherence to specified criteria, described in the study as a ‘disciplinarisation’ process. Similarly, Black [49] describes the enrolment of the regulated system as central to the cooperative relationship between the regulator and the regulated in risk-based regulation. Mikes [50] describes this mode of regulation as ‘coercive isomorphism’, whereby entities have autonomy but are induced to conform to a standard. Similarly, Power [23] describes this as the attainment of regulation through asserting control of self-regulation. However, Ford [51] argues that the concept of enforced self-regulation or that of ‘responsive regulation’ [19] does not account for the gaps in ‘regulatory spheres of responsibility’ [51] realised in the financial crisis. Alternatively, Beltratti and Paladino [52] explain the original rationale for the Basel Committee on Banking Supervision (BCBS) authorised use of proprietary risk models as a means of aligning the forecasts with their true risks. BCBS advocate the internal information theory, as necessary to achieve a level playing field [53]. The theme of a level playing field is central to the BCBS multi-jurisdictional approach to banking regulation, reducing cherry-picking of regulatory regimes when capital is mobile, thus incentivising efficient banking models. Van der Heijden [54] highlights the need for transnational regulatory collaboration following the increased internationalisation of capital markets. However, the impact of banking regulation is not uniform, for example, Leonida and Muzzupappa [55] find that while Basel II has improved alignment between banks and regulators in the German market, it has caused the disparity between large and small UK banks.

Remarkably, Lall [44] finds that the Institute of International Finance (IIF) lobbied the BCBS to allow banks to calibrate their regulatory requirements based on internal VaR models to ensure greater risk sensitivity. Similarly, Goldbach [56] finds significant influence on Basel standard-setting by transnational and national coalitions. Lall [44] argues that the influence of this informal social network led to favourable structuring of Basel II market risk capital requirements for large international and complex banks. A key criticism of internal model-based calculations of market risk regulatory capital is that the internal model can be designed in such a way to minimise the resultant capital, thus introducing moral hazard [57]. This is potentially easier to achieve for international portfolios with access to advanced, technical modelling, thus favouring internationally large, complex banks. Bank’s regulatory capital was insufficient to cover the unexpected losses of the 2007–2009 financial crisis [6]. Furthermore, Conlon et al. [58] highlight the importance of examining regulatory capital composition.

Alternatively, Cannata and Quagliariello [59] contend that the appropriation of proprietary models was a pragmatic approach by regulators to gain buy-in by banking institutions for the Basel II market risk regulatory regime. They find that industry apprehensions were assuaged by the reduced regulatory capital and systems impact of adopting proprietary models. However, Moosa [60] is critical of the retention of proprietary risk models in the FRTB framework. Conversely, Walker [61] describes the confluence of political and media pressure together with volatile financial markets, as an existential challenge for banking regulators. This literature predominately relates to regulation under Basel II. Importantly, the continued use of proprietary risk models under FRTB is rationalised as the key means of achieving: (1) risk-sensitive allocation of capital; (2) level playing field competition; and (3) the restoration of trust and credibility of proprietary risk models [62].

Alignment specifications between risk models used for regulatory and internal purposes were limited under Basel II. However, alignment between the regulatory and internal risk models is strongly mandated under FRTB. Validation of this alignment is central to the approval for IMA, through the assessment of a ‘use test’ [62]. However, findings by Mehta et al. [12] and McCullagh et al. [63] suggest that banks will retain their use of proprietary VaR risk models in practice, even when they diverge from the regulatory risk VaR/ES models.

Interestingly, the criticism of VaR as a means of modelling market risk predates its adoption to its regulatory role. Notably, Danielsson et al. [32] issued a warning to regulators about their choice of metric, describing it as a ‘poor quality measure(s) of risk’. Of further concern is the lack of consistency between the outcomes of various VaR models, noting that VaR is a family of models. Basel II does not specify what form the VaR model must take, instead relying on a system of exceedances to encourage conformity of use. In 1995, Beder applied eight common VaR methodologies to three hypothetical portfolios and found results varying by a magnitude of fourteen [64]. Similarly, Berkowitz and O'Brien [65] and Pritsker [66] found significant variation across banks’ resolution models. There is a rich literature that examines the performance of candidate resolution models [67,68,69,70,71] in terms of their forecasting performance, the propensity to experience loss exceedances and stability inference of VaR and ES at different confidence levels. However, a McKinsey report on the choice of resolution models finds a preference for simpler models [12]. Additionally, Hermsen [72] examines empirically the conflict between improved model performance and minimising capital requirements. He finds that banks are not incentivised to deploy better models under the Basel II framework. There is an internal conflict between deploying the best candidate model and the resource implications. Ultimately, there is a preference shown for models that imply the lowest capital requirements, while simultaneously minimising system requirements.

Deinstitutionalisation of VaR

The intense public cynosure of VaR, resulted in its position as the central regulatory market risk measure, becoming untenable. Clemente and Roulet [73] develop a theoretical model to explain how public opinion can influence the deinstitutionalisation of a practice. Deinstitutionalisation is where practices are dropped because of their reduced social approval. VaR’s displacement as the central risk model in the determination of market risk regulatory capital can be interpreted as a deinstitutionalisation of VaR whereby public opinion perceives it as having violated what Robson et al. [74] describe as the ‘social contract’ inferred under self-regulation serving the public interest. Similarly, O’Regan and Killian [75] discuss how a stress event can heighten tensions between the self-regulated and society through erosion of trust. The financial crisis was one such stress event that caused the public to question the efficacy of banking regulation, with particular censure for perceived self-regulatory mechanisms. For example, Nesvetailova and Palan [76] argue that Basel II not only failed to ensure stability, but its system of ‘privatised financial regulation’ also exacerbated the crisis. However, Callan et al. [77] report the IIF’s belief that the banking sector itself should devise the necessary regulatory reforms. This illustrates the coexistence in the immediate aftermath of the financial crisis, of opposing industry and societal logics [78].

Examining this conflict further, Roulet [79] examines the internal mediation of external opposition and finds that, because of the opacity of the financial sector, it can withstand pressure to acquiesce to societal logics. Yet, the BCBS through FRTB, have replaced the infamous VaR with a highly prescriptive framework [80], within which approval for internal risk models is heavily vetted [81]. Oliver [82] finds that the endurance of organisational practices is dependent on their perceived legitimacy. Using the characteristics of accounting measures defined by Miller and Power [83] to examine the latent power and endurance of the VaR measure, McCullagh et al. [63] find that VaR’s legitimacy is predominantly derived from its internal control role, rather than its regulatory imprimatur.

Methodology

The issues explored in this paper centre on the practitioners’ perception of the role of VaR/ES risk models within the market risk regulatory capital framework. In particular, we are interested in the strength of association between internal and regulatory risk models, risk models and regulatory capital, and regulatory capital and risk behaviour. The context of the impending regulatory reform under FRTB heightens the prescience of this research. The FRTB framework is designed to ensure the stability of banking systems through a risk-based capital calculation mechanism that is more prescriptive than the VaR-based mechanism under Basel II. However, this may be undermined by (1) further decoupling of internal and regulatory VaR/ES, and (2) decoupling of capital and VaR/ES risk models.

Hutter [16] discusses the emergence of risk-based regulation, arguing that inefficiencies in the public sector prompted the adoption and ‘almost unthinking acceptance’ of the suitability of private-sector practices (p. 2). The objectivity and transparency inferred by risk-based approaches were viewed as a means of reconciling different interest groups and informing the allocation of resources. Furthermore, Hutter [16] finds that risk models were used to legitimise regulation, enabling the further retraction of government. Power [23] describes regulatory systems linked to licencing privileges (such as bank licenses) as following an ‘enforced self-regulation model’ that enrols ‘self-regulating resources’. The inherent conflict of regulators is that they are ‘… in part about political perceptions of effectiveness and the possibility of blame’, yet they are empowering self-regulation of entities where the bank’s self-interest transcends public interest.

The regulation of banks’ exposure to market losses manifests the conflict between the shareholder value theory deployment of VaR, characterised by Power [23] as the internal capital allocation and control mechanism, and the fail-safe public expectations of bank regulations over which VaR currently presides [84]. They argue that regulators have a blameless protective foil via the regulatory conditionality of self-governance by regulated entities but are exposed to the interface of the risk-based philosophy (which includes failure within its accepted event set) with the public’s intolerance of risk spillover from the financial sector. Power [23] characterises VaR as the embodiment of the shareholder value mode of performance-to-risk-based capital allocation in banks. He argues that VaR’s origins in the organisational need for an overview of transactions’ exposure, resulted in organisational and institutional significance far exceeding its regulatory role.

Hellwig [1] suggests that risk-based capital requirements have led to significant declines in regulatory capital and increased systemic interconnectedness and thereby, systemic vulnerabilities. Furthermore, that risk-based regulation incentivises shifting and translating risks out of the portfolio, often transforming them into more complex risks. He further argues whether public interests are to be served then reforms to regulation must refocus on capital requirements not calibrated to banks’ risk models. This relates to the concerns of Hutter [16], whereby the risk device becomes an illusion of objectivity that distances regulators from the outcomes. Although Hutter’s [16] paper addresses regulation in a broader context, she identifies the inherent conflict between public and private interest groups that regulation needs to navigate. She suggests that risk-based models are used as a ‘seemingly objective means of adjudication’ [16] between the two interest groups. We interpret her challenge to examine how ‘ideas translate into action’ [16] as a need to examine the reality of the implementation of risk-based regulation in market risk. We, therefore, use ideas from Hutter [16] to examine practitioners’ perceptions of the relationships between internal and regulatory VaR/ES and between regulatory capital and the risk models.

We explore, using risk-based regulation insights from Hutter [16], the experiences of practitioners on the relationship between internal and regulatory VaR/ES risk models and between VaR/ES risk models and regulatory capital. We examine practitioners’ expectations about the implementation of FRTB and whether it will result in further decoupling. In this qualitative study, we utilise these insights from Hutter to examine the practitioners’ perspectives on the operationalisation of market risk regulation using a series of semi-structured interviews with relevant actors in the field.

We conducted twenty semi-structured interviews with a range of VaR stakeholders in Ireland and the UK from January 2018 to January 2019. The rationale for focusing on these two markets is that there is strong integration between Irish and UK banking institutionsFootnote 2 and that, culturally, lending practices, societal norms and legal frameworks in the two jurisdictions have strong similarities. The Irish and UK banking sectors are an interesting paradox in that they are part of the European banking system but are differentiated by their financial openness [85]. Buch and Heinrich [85] also find that Ireland, the UK, and Luxembourg have more liberal regimes concerning foreign banks. Interestingly, Nesvetailova and Palan [76] connect the events of the financial crisis with Liberal Market Economy capitalism associated with Anglo-Saxon banking cultures. However, Konzelmann et al. [86] find that the divergent experiences of countries with this culture defy this conclusion. They distinguish between the effects of the crisis on the USA and the UK compared with Canada and Australia as two other major Anglo-Saxon economies. Ireland and New Zealand complete their list of Anglo-Saxon economies. They find key differences in the form of liberalisation but also in the nature of the regulatory systems between the couplets: USA and UK, versus Canada and Australia. Kwok and Tadesse [87] make the conjecture that countries whose culture promotes stronger uncertainty avoidance are more likely to have a bank-based financial system configuration, as opposed to the markets-based system associated with Anglo-Saxon financial systems. Although the choice of jurisdiction is interesting for the reasons outlined above, it may also be considered a limitation of the study. Future studies could explore the views of practitioners in alternative jurisdictions.

The respondents included market risks managers, traders, treasury managers, regulatory executives and representatives from professional risk management bodies. We have grouped the respondents into the following categories, summarised in Table 1. The interviews of the informants were generally carried out face-to-face with the information transcribed for further analysis. Where this was possible, this allowed for the development of trust between the interviewer and the informants. The informants were provided with assurances of confidentiality, non-disclosure of their name or their employers and secure storage of information. The views expressed are assumed personal views rather than those of their employers.

The final profile of the participants is shown in Table 2.

Following transcription, we analysed the interviews in accordance with O’Dwyer [88]: data reduction; data display; and data interpretation. Braun and Clarke [89] discuss how qualitative semi-structured interviews can be used dually to explore participants’ experiences and realities together with how these realities have been informed or influenced by discourse and societal, institutional organisational norms.

This study has taken participants from roles within the banking organisations immediately interfacing with VaR, end-users that engage with the outcome of the VaR models but not their development or calibration, and those outside of the organisation but involved with market risk supervision (regulation) or market risk practitioner advocacy. The interview participants possess considerable experience in implementing regulatory changes and tacit knowledge of organisational practices [90,91,92]. The importance of having interactional expertise is highlighted by Spears [93], as a means to gain trust and establish confidence to engage with an implicit epistemology. It is advantageous, therefore, that the first author has industry experience but conversely, this positional bias, not uncommon in research interviews, demands rigorous self-critique [94]. We found the pool of potential participants with exposure to market risk regulation and VaR to be a relatively small, homogeneous group. Recognising that the concept of saturation is contestable [95], we contend that our sampling had reached a point where no new information would be yielded from further exploration.

Findings and discussion

In this section we analyse participant responses under the key research aim of examining (1) decoupling between internal and regulatory VaR/ES risk models, decoupling between risk models and capital, and the relationship with bank risk-taking behaviour, and (2) the impact of the impending implementation of FRTB on these relationships Noting the key concern that decoupling of market risk regulation and internal market risk practices could undermine the efficacy of regulatory reform, we pay heed to references to behavioural influences.

Relationship between internal and regulatory risk models and capital

First, we explore the interview participants’ views of VaR and its role within the Basel II regulatory framework. Second, we examine the practitioner’s perception of the performance of internal and regulatory risk models. We are interested in whether they treat these as integrated or discrete and whether there are any differences in the criticisms levied. Then finally, the third emergent theme within the examination of the relationship between internal and regulatory VaR centres on perceptions around the efficacy of current regulations (pre-implementation of FRTB) to deliver stability in the global banking system.

VaR within Basel II

Cannata and Quagliariello [59] find that the criticism levelled at VaR was mired in a misunderstanding about the implementation of Basel II. VaR’s role in determining market risk regulatory capital under Basel II had not been implemented in most jurisdictions at the time of the financial crisis. Indeed, a significant body of work has explored the inhomogeneous implementation of Basel guidelines across various jurisdictions [96,97,98,99]. Some of the respondents identify the issue of translation of Basel II into jurisdictional regulations (Capital Requirements Directive (CRD) and Capital Requirements Regulation (CRR) in Europe) and their subsequent implementation, in their defence of VaR:

Many stones were cast at Basel II and internal models and all that stuff. I think it’s slightly unfair, if you look at it, certainly what I’m familiar with, Basel II was not really introduced until 2007 in terms of CRD, if you look across Europe, most institutions didn’t approval until 2008, 2009, certainly in the Irish context you could see that as problems emerged, backstop things with the SA, so it’s completely ludicrous to blame Basel II. (P12)

However, a more dominant argument is that VaR met their (particularly the R cohort) expectations of what the model was supposed to do:

On the whole, I’d be pretty positive around it [VaR] just in terms of the information it gives you. I think the problem with VaR is what people expect it to do. So, when you say 99% VaR, that’s saying that on 1% of occasions it’s going to be worse than that. It doesn’t tell you how bad that’s going to be. (R1)

This quote highlights that for them, VaR did not fail in the sense that their expectations were a 99% confidence levelFootnote 3 value and not an indication of the worst-case scenario. The implication is that the public expectation of the model as a fail-safe means of determining adequate capital for a worst-case scenario was not the expectation of practitioners. This is suggestive of a risk-based regulatory regime incongruent to reconcile private bank interest with the public interest. It characterises VaR as a risk mechanism aligned with the expectations of bank interests. This does little to honour the expectation expressed by Hutter [16] that the risk model would objectively adjudicate between interest groups.

Modelling market risk: internal and regulatory VaR

For most of the R cohort, misuse or poor interpretation and understanding of the VaR figures led to poor portfolio management, but they did not consider the model itself to be causal in the events of the financial crisis. This is reflective of Beck’s [100] expert-lay discordances as discussed in O’Regan and Killian [75], whereby their risk expertise is both prized and exclusionary even within the banking system. Furthermore, it rationalises and justifies continued trust in the risk model as a key component of their belief systems, by identifying application and interpretation errors [101]. This is a manifestation of Hutter’s [16] concerns around awareness of the risk model limitations.

There’s always a disconnect between people who model stuff and it’s a mathematical problem and people who live in the real world and see the consequences of this. (T7)

I wouldn’t say [VaR] hasn’t performed well, it’s totally based on the information you put into it: you put the assumptions into it, and it gives you a number back. (R2)

I think VaR as a measure has an unduly bad reputation. It was an easy tool, most people even with a basic background [mathematically], it’s very intuitive, you can set it up in an excel sheet, it’s not difficult to calculate the returns of a data series. So, a lot of people could very quickly get a grasp of what historical VaR was. (R3)

However, in the defensive arguments around VaR, it is clear that they are talking about its usefulness in terms of its internal role. We find varying degrees of acknowledgement of the decoupling of internal VaR and regulatory VaR in terms of both its legitimacy and its practical performativity:

VaR as a measure of risk level or certain changes in risk level from period to period: absolutely fine. But the idea that you can give it a regulatory imprimatur and say that everybody should do this. (T3)

I think what was a major shock was the degree to which it broke down. They understood that this model, as the vast majority of models in finance, is an approximation and needs clever use and needs people who understand limitations to use them. Extending them into the more general world, the problem with VaR is largely the breakdown between people who work day to day on the modelling and understand it and the people who are really 2 steps removed from it. (T10)

The second quotation suggests that the VaR output is unsuitable for external digestion. We further find practitioners’ acceptance of VaR’s performance internally while othering its performance in the regulatory role. The appropriation of VaR by regulators for the determination of market risk regulatory capital was welcomed by practitioners as it enabled reductions in capital requirements based on a calculative technology’s quantification of the risk in their portfolios. Yet, any apparent failing in its regulatory role is given a detached position. This discursive positioning provides an insight into the extent to which practitioners have not fully integrated the internal and regulatory roles of VaR and view the regulatory version as external to them and their risk management practice. This is consistent with the strategic response of buffering as described in Oliver’s organisational response framework [82].

Market risk regulations and stability

The philosophical moorings of the model may not have been considered when the BCBS appropriated banks’ VaR models for the determination of market risk regulatory capital.

The starting point [with VaR] depends on why you are doing it. (T6).

This highlights that model use is both informed and constituted by its purpose [102]. Externally, the regulatory role and internal role of VaR were assumed to be seamless, thus contributing to the external perception of VaR’s role in banks as a form of self-regulation and further, as evidence of regulatory capture. We examine the participants’ responses for any acknowledgement of failed self-regulation or regulatory capture.

Conclusion: over the last 10 years is that the dangers are far greater when regulators leave institutions to themselves. But the crisis illustrates sitting on the fence and saying heterogeneity is a great thing, as what predated the … in the run-up to 2006 … well we accept banks, left to manage their risks, why would they want their businesses to blow up, surely we can rely upon that, but I think that’s proven to be a little bit … optimistic! (P12) Basel II allowed banks bring in their own models, so you had divergence, that’s why you had Bear Stearns and Lehmans, now we're going back to SA - level playing field. (T5)

These responses indicate a belief in modelling autonomy under Basel II and allude to a form of self-regulation. The first quote suggests the existence of a moral hazard, concomitant with the use of proprietary models. With the appropriation of VaR into regulation, banks continued to use their bespoke risk models. There was a limited requirement to realign with the regulatory public interest mandate. The ‘return to SA’ refers to the Basel I Standardised Approach which was not risk-based and viewed as a crude measure, at odds with the sophisticated risk models in use internally [1]. This infers the practitioner’s perception of the FRTB framework as a return to a more prescriptive, capital-based form of market risk management. Triana [13] suggests regulatory adoption of VaR was motivated by aspirational association with these progressive modelling approaches, a position that is voiced by one respondent:

I think it was regulatory capture. Using a formulaic approach like they had in the standardised method made them look like the dumb people in the class. So, they said, we’re going to be smart too, we’re going to try and use the most modern method and they want to be able to say that they were aware of developments in the ’science’. But there is no science. Regulatory capital is all about loss in a dry spell and in that circumstance, every single assumption underlying VaR goes out the window. (P8)

The P contributor characterises the relationship between the regulated and the regulator as regulatory capture. However, this quote shows the perception of the adopted regulatory use of banks’ VaR modes as a manifestation of an inferiority complex. It infers that they were beguiled by the allure of sophisticated mathematical models when their priority should have remained with capital sufficiency. This statement indicates a clear belief that VaR was not capable of delivering the stabilising capital required. Hutter [16] argues that any discussion on the limitations of risk-based regulation must link back to broader considerations about the efficacy of regulation and a cost–benefit analysis. If, as suggested by Power [23], this is translated to a shareholder value logic, then public interest won’t be served.

Manish and O’Reilly [103] examine whether banking regulation follows a public interest philosophy or an economic theory approach. They conclude, based on the resultant increased disparity in wealth distribution, that it is the latter. They assert that this form of regulation predicates regulatory capture. A broad interpretation of regulatory capture can be understood as special interest groups exerting significant influence over regulatory bodies. A more narrow interpretation is where regulated entities manipulate the regulatory agencies [104]. Temporal observation of the evolution of the FRTB regulatory framework illustrates the difficulties in making ideals manifest. Investigating the reason for the deviation between the original aspirations of Basel II and the resultant regulatory guidelines, Lall [105] has strong resonance with the theory of regulatory capture. Mattli and Woods [106] find that the conditions needed for regulatory change that serves the common interest to dominate regulatory capture where vested interests are served include knowledge of the ‘social cost of capture’. Using Power, the pragmatic adoption of VaR may be seen as an alignment with the economic theory approach. Although there is insufficient support for the interpretation of regulatory capture espoused by Dal Bó [104], the conditions for Young’s ‘common ideation’ are present. The closed organisational roof concept deployed by Killian and O'Regan [75] in their examination of accounting professionals is present in how risk practitioners delineate those who understand VaR and those outside that understanding. However, practitioners’ descriptions primarily relate to the internal role of VaR and the experts and non-experts within the organisation, rather than delineating the internal from the external. Therefore, in the case of VaR, we cannot interpret this as an indication of an exclusionary expert technology used to self-regulate.

We further pursue practitioners’ perceptions around the proficiency of the regulatory mechanisms to deliver stability. We find an awareness of the inherent conflict within a regulatory capital regime between public and private interests.

Regulator believed that banks were undercapitalised in terms of the trading book. Mixture of both: regulator want to protect the people from the banks, obviously, they don’t want the situation again where they have to bail out banks which obviously impacts on the taxpayer as well. Regulator sees themselves as the guardian of the people almost, they understand it better than the people on the streets. (R1)

The big one is, regulator need to do something. Regulators have gone too far … big debate … someone like me who works in the system … how far should they go? … finding the sweet spot, between banks the economy. (P12Footnote 4)

Here we find recognition of the balancing act required by regulators: protecting the interests of society while enabling banks to perform the role required by the economy and meeting their commercial needs [16]. We find awareness of the social cost of failed regulation, but we also find that the responsibility of regulation is externalised in their discussions. This is not consistent with Power’s precept of self-regulation as a form of regulatory coercion. The regulatory role of VaR is othered by practitioners, along with the responsibility for regulatory failings.

Impact of the impending implementation of FRTB on risk model and capital relationships

Having explored practitioners’ perceptions of the current (pre-FRTB) relationship between market risk regulation, internal market risk measurement and management, and capital, we now explore practitioners’ responses to questions on the likely impact of the implementation of FRTB. The two key emergent themes under this area of examination are the succession of VaR by ES and the pre-eminence of capital. We explore each of these in turn.

ES succeeds VaR

The headline change under FRTB is the demotion of VaR as the means of determining market risk regulatory capital. We explore practitioners’ perception of the characterisation of VaR post-crisis, and their views on its downgraded prominence in FRTB post-crisis regulatory reform. Industry commentators vilified the role of VaR within the Basel II regulatory framework. Joe Nocera, business columnist with the New York Times, reflects on the sentiment around VaR in 2009:

Given the calamity that has since occurred, there has been a great deal of talk, even in quant circles, that this widespread institutional reliance on VaR was a terrible mistake [107].

Pablo Triana, a former derivatives trader, Financial Times columnist and Professor of Finance at Esade, described VaR as: ‘The number that killed us’ and ‘VaR may have been the single most influential metric in the history of finance’ in his column in the Financial Times. At the behest of the Chancellor of the Exchequer (UK), the Turner review was commissioned to review the causes of the financial crisis and to make recommendations about the changes necessary to ensure a stable banking system. The review identifies dependence on VaR as one of the key issues.

Capital required against trading book activities should be increased significantly (e.g. several times) and a fundamental review of the market risk capital regime (e.g. reliance on VaR measures for regulatory purposes) should be launched [108].

There is an acknowledgement by regulators that the market risk regulatory system required reform post-crisis. However, the FRTB framework, notionally at least, maintains the authorised use of proprietary risk models. However, additional criteria are introduced. Also notable is the replacement of VaR with expected shortfall, arguably a deinstitutionalisation of VaR. One of the regulatory/advocacy participants described the impetus for removing dependence on VaR from the FRTB framework:

Just after the crisis, there was, within the Basel Committee, there was of a crisis of confidence in the internal model – the feeling that the models were ‘the devil’s work’, they were the reason why the banks went crazy and got into all these complex products, and there was a sense that some of the local supervisors didn’t understand the models so they couldn’t [sic have] supervised very well. (P13)

This echoes concerns by Ackermann [10] that the risks of these complex structures (securitisations) were not fully understood and that there should have been a regular reflection on the risk models’ adequacy and usefulness. Despite the apparent change in the risk model and demotion of VaR in FRTB, several participants argued that the same risk forecasting engine will be deployed.

So, I find it ironic that people should think that ES is a new thing. I mean ES is on the same distribution. (P8)

Any criticism that you level at VaR you can level ES because the criticisms of it, … its the same analytical framework. (T10)

Demoting VaR within the FRTB framework allows regulators to distance themselves from VaR and to demonstrate recognition of the criticism of VaR. This is important to the perceived legitimacy of the regulator in being seen to act in the public interest [109]. Although ostensibly succeeded by ES in the layered risk calculation of the FRTB framework, VaR remains part of the backtesting requirements. It must be noted that practitioners broadly welcome the changes to market risk modelling introduced under FRTB. For example:

As a framework, it is conceptually better than the VaR and SVaR.Footnote 5 (RM15).

Despite FRTB’s positive perception, practitioners view the complexity of the FRTB framework as an impetus for decoupling internal VaR and regulatory risk management. Practitioners consider that the complexity of FRTB makes it unwieldly for use for internal risk allocation and have no imminent plans to migrate for other internal risk management purposes:

They will probably manage on VaR and calculate capital on whatever FRTB says because it’s very difficult to manage positions with FRTB calculations. (R15)

Undecided whether internal risk measure will change in line with FRTB. (R3)

This is not a surprise to the regulators. We find a benign attitude of regulators to the decoupling of internal VaR and FRTB’s regulatory risk measure:

So, at the moment we have what we call a ‘use test’. So, banks are meant to use the same model that they use for capital requirement as the basis of their internal risk management. And what we’ve done in framing the new framework is slightly loosen that use test to talk more about the engine that drives the model being the same, but the risk measure isn’t necessarily going to be the same. So, I would expect that banks will continue to use VaR for day-to-day risk management purposes. (P13)

This adds further weight to the characterisation of the regulatory position as pragmatic rather than using self-regulation as a guise for coercive isomorphism.

Pre-eminence of capital

FRTB is part of a wider suite of reforms under Basel III. Other capital requirements under Basel III (such as Pillar II capital requirements) have shifted the culture away from the ‘minimum capital requirements’ associated with the introduction of Basel II, to a ‘fail-safe’ level of capital. Many of these elements have already been implemented in European banks. We find that practitioners perceive that the regulators will determine the appropriate level of overall capital rather than self-determined capital requirements. This further underlines a practitioner experience that recognises the primacy of capital decoupled from risk models, under the Basel III and FRTB reforms.

Ultimately Pillar II is going to be what the regulator decides it’s going to be. You stick in your calculation, and they say we don’t like it and here is an add-on. It then becomes almost a gaming situation where the risk management people, it comes back to Keynes beauty contest; the risk management people decide ok you don’t go with the minimised amount of capital, you don’t go to calculate it accurately or you go bold to get as close as possible to what the regulator is expecting. (T10)

They [regulators] are not looking at it from a simplistic model, if they don’t[sic] think the answer they are getting from any model is not the right one they have the discretion to put a Pillar II add-on on top of your capital. (T6)

If the models are giving an outlier answer, you’ll get add-ons that will get you there. They just increase the capital in the system and the capital in the system needed to increase. (T6)

The clear indication from practitioners’ responses is that FRTB promotes capital rather than the risk model as the conduit for ensuring bank stability and incentivising prudential risk behaviour. Practitioners find that FRTB discourages banks from holding complex products, heralding a return to a simpler form of banking. Note that the reforms under Basel III including FRTB are so comprehensive that collectively they have been dubbed Basel IV [30, 31, 110].

Basel IV is driving banks to simplicity. (T6).

I think standing back from it banks are returning to Banking 101 where banks are thinking what banks really should do is help people build homes and set up current accounts and move money around the place and that’s it! We don’t want to see any trading activity in banks other than stuff that is incidental trading risk that you get on your balance sheet by virtue of the fact you’re doing that kind of maturity transformation. (T7)

Retail banks should be sticking to the knitting and doing what their retail customer needs. (T5)

I think in practice that really means if you’re trading complex stuff, you’re going to have a higher capital requirement and there will be incentives there to stick to the centre. (P13)

The complex nature of securitised structures and other highly leveraged products were viewed to be central to the socialisation of losses in the 2007–2009 financial crisis. FRTB is perceived by practitioners to discourage complexity in bank portfolios and, in combination with other reforms under Basel III, promote capital over risk modelling as the conduit for incentivising prudential risk-taking. Interestingly, Acharya and Richardson [111] argue that it wasn’t the complex products in themselves that led to the scale of the financial crisis but ‘banks’ efforts to circumvent these capital-adequacy requirements caused the financial crisis’, where they describe the balancing of assets and liabilities and the role of capital requirements as part of Banking 101.

I think clearly people will move towards what the regulator requires, and if they move [towards capital-based regulation] people will reflect on that basis. (T10)

Conclusion

Our objective in this examination of the perspectives of bank practitioners is to develop a deeper understanding of their experienced realities of internal market risk management VaR, regulatory VaR/ES risk models and regulatory capital. Under Basel II, the market risk regulatory capital mechanism is VaR, but as VaR relates to a family of models rather than a single model, there can be a significant disparity between approaches taken for internal and regulatory purposes. Previous studies have recognised the decoupling of internal and regulatory VaR through the use of different models for internal and regulatory market risk modelling. However, our study explores how this is experienced in practice and how this may change with the implementation of FRTB. We further question whether there is a decoupling between VaR/ES risk models and regulatory capital under FRTB and Basel III regulatory reforms.

We find widespread recognition and acceptance of decoupling between regulatory risk models and VaR risk models used in internal risk management practice. This is at odds with the narrative presented by external commentators, whose criticism of VaR assumes these roles are fully integrated. We further find that this decoupling is known and regarded benignly by regulatory bodies. Where we add further insight is the positioning of practitioners with respect to regulatory VaR. This is most evident in the discussions on the apparent failure of VaR in the financial crisis. In the internal organisational role of VaR, practitioners find that it performed in line with their expectations. They position the regulatory role of VaR as external and other, distancing themselves from the outcome of its use in this context.

The apparent deinstitutionalisation of VaR as the regulatory risk model under FRTB is acknowledged by the regulatory/advocacy participants, but for participants within the banks, the relationship between the internal VaR model and the regulatory mechanism is already decoupled so this presents no imminent challenge to their internal risk management practices.

While we find a generally positive reception to the layered FRTB framework in conjunction with Basel III reforms, it is widely recognised as a capital measure that takes the impetus away from the choice of risk model; that is, we find that practitioners perceive the decoupling of capital and the risk models. There is a strongly held belief that these regulatory reforms will incentivise migration to simpler products through high capital implications for complex products, ultimately upholding a public interest mandate. Capital is perceived as the conduit for managing risk behaviour under FRTB, usurping the role of any risk model. Furthermore, the study participants suggest that the complexity of the FRTB calculative framework is expected to reduce opportunities for capital minimisation and indeed obfuscate the role of the proprietary risk model itself within the regulatory framework. One of the implications of this study is the need for greater recognition of the decoupling of market risk regulation and internal market risk modelling and management. If regulatory reform designed to enhance the stability of the global financial banking system assumes full integration, then the decoupling recognised in this study will undermine the efficacy of that reform and dilute the impact on risk-taking behaviour.

This research highlights the importance of qualitative research in the realisation of regulatory ideals, particularly the operationalisation of regulatory philosophy. In turn, this flags the need for research that examines the behavioural impact of regulation through the experienced realities of practitioners in the field beyond apparent compliance. There will be opportunities for further exploration of the decoupling of regulatory and internal risk management practices following the implementation of FRTB.

Notes

Under Basel I and before the market risk amendment to Basel II.

The study was carried out prior to Brexit.

That is, a statistical probability that 99% of the time under prescribed assumptions, the portfolio losses will not exceed VaR.

Former risk manager.

Stressed VaR.

References

Hellwig, M.F. 2010. Capital regulation after the crisis: Business as usual? MPI Collective Goods Preprint. (2010/31).

Lastra, R.M., and G. Wood. 2010. The crisis of 2007–2009: Nature, causes, and reactions. Journal of International Economic Law 13 (3): 531–550.

Llewellyn, D.T. 2013. A strategic approach to post-crisis regulation-the need for pillar 4. Stability of the Financial System: Edward Elgar Publishing.

Van Der Pijl, K., and Y. Yurchenko. 2015. Neoliberal entrenchment of North Atlantic capital. From corporate self-regulation to state capture. New Political Economy. 20 (4): 495–517.

Froud, J., M. Moran, A. Nilsson, and K. Williams. 2011. Opportunity lost: Mystification, elite politics and financial reform in the UK. Socialist Register. 2011: 47.

Anginer, D., A.C. Bertay, R. Cull, A. Demirgüç-Kunt, and D.S. Mare. 2021. Bank capital regulation and risk after the Global Financial Crisis. Journal of Financial Stability. 2021: 100891.

Laeven, L., L. Ratnovski, and H. Tong. 2016. Bank size, capital, and systemic risk: Some international evidence. Journal of Banking and Finance. 69: S25–S34.

Cuadros-Solas, P.J., C. Salvador, and N. Suárez. 2021. Am I riskier if I rescue my banks? Beyond the effects of bailouts. Journal of Financial Stability. 56: 100935.

Acharya, V., I. Drechsler, and P. Schnabl. 2014. A pyrrhic victory? Bank bailouts and sovereign credit risk. The Journal of Finance. 69 (6): 2689–2739.

Ackermann, J. 2008. The subprime crisis and its consequences. Journal of Financial Stability. 4 (4): 329–337.

Langley, P. 2013. Anticipating uncertainty, reviving risk? On the stress testing of finance in crisis. Economy and Society. 42 (1): 51–73.

Mehta, A., M. Neukirchen, S. Pfetsch, and T. Poppensieker. 2012. Managing market risk: Today and tomorrow. Chicago: McKinsey & Company.

Triana, P. 2011. The number that killed us: A story of modern banking, flawed mathematics, and a big financial crisis. Hoboken: Wiley.

Nocera, J. 2009. Did managers of risk outsmart themselves? International Herald Tribune. Accessed on 03 Jan 2009.

Heaney, V. 2012. The monster of VaR has not gone away. Financial Times.

Hutter, B.M. 2005. The attractions of risk-based regulation: Accounting for the emergence of risk ideas in regulation. London: CARR.

Jasanoff, S. 2005. Technologies of humility: citizen participation in governing science. Wozu Experten? VS Verlag für Sozialwissenschaften, pp. 370–89.

Porter, T.M. 2020. Trust in numbers: The pursuit of objectivity in science and public life. Princeton: Princeton University Press.

Ayres, I., and J. Braithwaite. 1992. Responsive regulation: Transcending the deregulation debate. Oxford: Oxford University Press.

Baker, A. 2010. Restraining regulatory capture? Anglo-America, crisis politics and trajectories of change in global financial governance. International Affairs. 86 (3): 647–663.

Hakenes, H., I. Schnabel. 2014. Regulatory capture by sophistication

Baud, C., and E. Chiapello. 2017. Understanding the disciplinary aspects of neoliberal regulations: The case of credit-risk regulation under the Basel Accords. Critical Perspectives on Accounting. 46: 3–23.

Power, M. 2007. Organized uncertainty: Designing a world of risk management. Oxford: Oxford University Press.

Danielsson, J. 2003. On the feasibility of risk based regulation. CESifo Economic Studies. 49 (2): 157–179.

Mayes, D., and G.E. Wood. 2007. The structure of financial regulation. New York: Routledge.

Goodhart, C. 2011. The Basel Committee on Banking Supervision: A history of the early years 1974–1997. Cambridge: Cambridge University Press.

Barth, J.R., S.M. Miller. 2017. A primer on the evolution and complexity of bank regulatory capital standards. Mercatus Working Paper, Mercatus Center at George Mason University, Arlington, VA

BCBS. 2017. Basel III: Finalising post-crisis reform. Bank of International Settlements

Koch, S., S. Schneider, R. Schneider, and G. Schröck. 2017. Bringing Basel IV into focus. Chicago: McKinsey.

Nicolaus, D. 2017. Basel IV: Banks should act now on capital and strategic planning. https://home.kpmg/xx/en/home/insights/2017/12/basel4-capital-and-strategic-planning-fs.html2017. https://home.kpmg/xx/en/home/insights/2017/12/basel4-capital-and-strategic-planning-fs.html.

PWC. 2017. 'Basel IV': Big bang or the endgame of Basel III? https://www.pwc.com/gx/en/financial-services/assets/basel-iv-big-bang.pdf.

Danielsson, J., P. Embrechts, C. Goodhart, C. Keating, F. Muennich, O. Renault, et al. 2001. An academic response to Basel II. ESRC Research Centre, LSE Financial Markets Group

Artzner, P., F. Delbaen, J.M. Eber, and D. Heath. 1999. Coherent measures of risk. Mathematical Finance. 9 (3): 203–228.

Farag, H.M. 2017. Bracing for the FRTB: Capital, business and operational impact. Journal of Securities Operations and Custody. 9 (2): 160–177.

BCBS. 2015. Fundametal review of the trading book: interim impact analysis. Bank for International Settlements

BCBS. 2013. Fundamental review of the trading book: A revised market risk framework

BCBS. 2016. Fundamental review of the trading book: A revised market risk framework. Bank for International Settlements

Diebold, F.X., A. Hickman, A. Inoue, T. Schuermann. 1997. Converting 1-day volatility to h-day volatility: scaling by is worse than you think. Penn Institute for Economic Research Working Papers, pp. 97–030.

McNeil, A.J., and R. Frey. 2000. Estimation of tail-related risk measures for heteroscedastic financial time series: An extreme value approach. Journal of Empirical Finance. 7 (3–4): 271–300.

Danielsson, J., and J.-P. Zigrand. 2006. On time-scaling of risk and the square-root-of-time rule. Journal of Banking and Finance. 30 (10): 2701–2713.

Alexander, C. 2009. Market Risk Analysis, Value at risk models. New York: Wiley.

Wang, J.N., J.H. Yeh, and N.Y.P. Cheng. 2011. How accurate is the square-root-of-time rule in scaling tail risk: A global study. Journal of Banking and Finance. 35 (5): 1158–1169.

Balter, J., and A. McNeil. 2018. On the Basel Liquidity Formula for Elliptical Distributions. Risks. 6 (3): 92.

Lall, R. 2015. Timing as a source of regulatory influence: A technical elite network analysis of global finance. Regulation and Governance. 9 (2): 125–143.

Young, K.L. 2012. Transnational regulatory capture? An empirical examination of the transnational lobbying of the Basel Committee on Banking Supervision. Review of International Political Economy. 19 (4): 663–688.

Carpenter, D., and D.A. Moss. 2013. Preventing regulatory capture: Special interest influence and how to limit it. Cambridge: Cambridge University Press.

Gunningham, N., and J. Rees. 1997. Industry self-regulation: An institutional perspective. Law and Policy. 19 (4): 363–414.

Albu, C.N., N. Albu, and D. Alexander. 2014. When global accounting standards meet the local context—Insights from an emerging economy. Critical Perspectives on Accounting. 25 (6): 489–510.

Black, J. 2003. Enrolling actors in regulatory systems: Examples from UK financial services regulation. Public Law. 2003: 63–91.

Mikes, A. 2011. From counting risk to making risk count: Boundary-work in risk management. Accounting, Organizations and Society. 36 (4): 226–245.

Ford, C. 2011. Macro-and Micro-Level Effects on Responsive Financial Regulation. University of British Columbia Law Review. 44: 589.

Beltratti, A., and G. Paladino. 2016. Basel II and regulatory arbitrage: Evidence from financial crises. Journal of Empirical Finance. 39: 180–196.

BCBS. 2010. Revisions to the Basel II market risk framework Bank of International Settlements

van der Heijden, M. 2019. Agencies without borders: Explaining partner selection in the formation of transnational agreements between regulators. Regulation and Governance. 15 (3): 725–744.

Leonida, L., and E. Muzzupappa. 2018. Do Basel Accords influence competition in the banking industry? A comparative analysis of Germany and the UK. Journal of Banking Regulation. 19 (1): 64–72.

Goldbach, R. 2015. Asymmetric influence in global banking regulation: Transnational harmonization, the competition state, and the roots of regulatory failure. Review of International Political Economy. 22 (6): 1087–1127.

Blundell-Wignall, A., P. Atkinson, and C. Roulet. 2014. Bank business models and the Basel system: Complexity and interconnectedness. OECD Journal: Financial Market Trends. 2013 (2): 43–68.

Conlon, T., J. Cotter, and P. Molyneux. 2020. Beyond common equity: The influence of secondary capital on bank insolvency risk. Journal of Financial Stability. 47: 100732.

Cannata, F., M. Quagliariello. 2009. The role of Basel II in the subprime financial crisis: guilty or not guilty? CAREFIN Research Paper. (3/09).

Moosa, I.A. 2010. Basel II as a casualty of the global financial crisis. Journal of Banking Regulation 11 (2): 95–114.

Walker, G.A. 2011. Basel III market and regulatory compromise. Journal of Banking Regulation 12 (2): 95–99.

BCBS. 2019. Minimum capital requirements for market risk. Bank for International Settlements

McCullagh, O., S. Killian, and M. Cummins. 2019. Value-at-Risk: The unanticipated power of a practice-based accounting measure. Precarious Presents, Open Futures 34 (2): 408.

Beder, T.S. 1995. VaR: Seductive but dangerous. FAJ. 51 (5): 12–24.

Berkowitz, J., and J. O’Brien. 2002. How accurate are value-at-risk models at commercial banks? The Journal of Finance. 57 (3): 1093–1111.

Pritsker, M. 1997. Evaluating value at risk methodologies: Accuracy versus computational time. Journal of Financial Services Research. 12 (2–3): 201–242.

Angelidis, T., A. Benos, and S. Degiannakis. 2004. The use of GARCH models in VaR estimation. Statistical Methodology. 1 (1): 105–128.

Angelidis, T., S.A. Degiannakis. 2006. Backtesting VaR models: An expected shortfall approach. SSRN 898473.

Giot, P., and S. Laurent. 2004. Modelling daily value-at-risk using realized volatility and ARCH type models. Journal of Empirical Finance. 11 (3): 379–398.

Giot, P., and S. Laurent. 2003. Value-at-risk for long and short trading positions. Journal of Applied Econometrics. 18 (6): 641–663.

Rossignolo, A.F., M.D. Fethi, and M. Shaban. 2012. Value-at-risk models and Basel capital charges: Evidence from emerging and frontier stock markets. Journal of Financial Stability. 8 (4): 303–319.

Hermsen, O. 2010. The impact of the choice of VaR models on the level of regulatory capital according to Basel II. Quantitative Finance. 10 (10): 1215–1224.

Clemente, M., and T.J. Roulet. 2015. Public opinion as a source of deinstitutionalization: A “spiral of silence” approach. Academy of Management Review. 40 (1): 96–114.

Robson, K., H. Willmott, D. Cooper, and T. Puxty. 1994. The ideology of professional regulation and the markets for accounting labour: Three episodes in the recent history of the UK accountancy profession. Accounting, Organizations and Society. 19 (6): 527–553.

Killian, S., and P. O’Regan. 2016. Social accounting and the co-creation of corporate legitimacy. Accounting, Organizations and Society. 50: 1–12.

Nesvetailova, A., and R. Palan. 2010. The end of liberal finance? The changing paradigm of global financial governance. Millennium: Journal of International Studies. 38 (3): 797–825.

Callan, E., D. Wighton, K. Guha. 2007. Regulators urged to take back seat. Financial Times.

Seo, M.-G., and W.D. Creed. 2002. Institutional contradictions, praxis, and institutional change: A dialectical perspective. Academy of Management Review. 27 (2): 222–247.

Roulet, T. 2015. “What Good is Wall Street?” Institutional Contradiction and the Diffusion of the Stigma over the Finance Industry. Journal of Business Ethics. 130 (2): 389–402.

Azoulay, M., D. Härtl, Y. Mushkin, and A. Raufuss. 2018. FRTB reloaded: Overhauling the trading-risk infrastructure. Chicago: McKinsey & Company.

Orgeldinger, J. 2017. Critical analysis of the new Basel minimum capital requirements for market risk. Emerging Science Journal. 1 (1): 1–15.

Oliver, C. 1991. Strategic responses to institutional processes. Academy of Management Review. 16 (1): 145–179.

Miller, P., and M. Power. 2013. Accounting, organizing, and economizing: Connecting accounting research and organization theory. Academy of Management Annals. 7 (1): 557–605.

Rothstein, H., M. Huber, and G. Gaskell. 2006. A theory of risk colonization: The spiralling regulatory logics of societal and institutional risk. Economy and Society. 35 (1): 91–112.

Buch, C.M., and R.P. Heinrich. 2003. Financial integration in Europe and banking sector performance. The incomplete European market for financial services, 31–64. New York: Springer.

Konzelmann, S.J., M. Fovargue-Davies, G. Schnyder. 2010. Varieties of liberalism: Anglo-Saxon capitalism in crisis? SSRN 1929627.

Kwok, C.C., and S. Tadesse. 2006. National culture and financial systems. Journal of International Business Studies. 37 (2): 227–247.

O’Dwyer, B. 2004. Chapter 23: Qualitative Data Analysis: Illuminating a Process for Transforming a ‘Messy’ but ‘Attractive’ ‘Nuisance.’ In The Real Life Guide to Accounting Research, ed. C. Humphrey and B. Lee, 391–407. Oxford: Elsevier.

Braun, V., and V. Clarke. 2013. Successful qualitative research: A practical guide for beginners. New York: Sage.

Collins, H., R. Evans, and M. Gorman. 2007. Trading zones and interactional expertise. Studies in History and Philosophy of Science Part A. 38 (4): 657–666.

O’Regan, P., and S. Killian. 2014. ‘Professionals who understand’: Expertise, public interest and societal risk governance. Accounting, Organizations and Society. 39 (8): 615–631.

Morgan, M.S. 2012. The world in the model: How economists work and think. Cambridge: Cambridge University Press.

Spears, T.C. 2014. Engineering value, engineering risk: what derivatives quants know and what their models do

Schwandt, T.A., Y.S. Lincoln, and E.G. Guba. 2007. Judging interpretations: But is it rigorous? Trustworthiness and authenticity in naturalistic evaluation. New Directions for Evaluation. 2007 (114): 11–25.

Suddaby, R. 2006. From the editors: What grounded theory is not. Academy of Management Briarcliff Manor, New York, p 10510

Quaglia, L., and A. Spendzharova. 2017. Post-crisis reforms in banking: Regulators at the interface between domestic and international governance. Regulation and Governance. 11 (4): 422–437.

Rixen, T. 2013. Why reregulation after the crisis is feeble: Shadow banking, offshore financial centers, and jurisdictional competition. Regulation and Governance. 7 (4): 435–459.