Abstract

This study aims to predict GCC financial stress on oil market, and GCC Stock and bond markets while considering the effect of the 2008 financial crisis, 2014 oil drop price and the 2019 novel COVID-19 outbreak. For this purpose, we use a new approach for predicting the financial stress, based on the One-Dimensional Convolutional Neural Network (1D-CNN). This article introduces a parameters optimization method, which provides the best parameters for 1D-CNN to improve the prediction performance of the financial stress indices. The results suggest that indexes of financial stress help to improve forecasting performance. It implies that the 1D-CNN model shows a better predictive performance in the out-of-sample findings.Regarding the influence of financial stress on hedging between Brent, and financial markets, the outcomes emphasize the role of oil in hedging stock market risks in positive market stress case. Another interesting result is that the out-of-sample estimates for stock–bond markets, hedging with oil have higher variability for negative (positive) financial stress. The findings highlight the predictive information captured by financial stress in accurately forecasting oil market volatility and financial markets, offering a valuable opening for investors to monitor oil market volatility using information on traded assets.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

News of the Covid-19 outbreak outside China immediately sent global financial markets plummeting as fear of infection began to escalate among countries. For example, the Gulf Cooperation Council (GCC) is predicted to be hit by a double whammy of human and economic losses as a result of the pandemic, as it will not only cause deaths but also pose a significant economic threat due to falling oil prices (Arezki et al., 2020). GCC economies are still dependent on oil as their main export and source of revenues, despite the considerable diversification efforts deployed in the recent years. These crises have had a significant impact on the returns of many asset classes, raising questions about their influence on optimal portfolio allocation. A market portfolio is an advantageous guideline that helps reduce risk and diversify investment in the best possible way among non-correlated assets (Mensi et al., 2017)). Co-movement not only has theoretical implications for understanding asset pricing, but also practical implications for asset allocation and risk management (Filzen & Schutte, 2017).

In addition, the novel coronavirus has particularly affected financial markets all over the world, thus exerting enormous financial “stress” on the growth and recovery of the economy as a whole. Financial stress plays a key role in determining the dynamics of share prices during crisis periods. Hence, researchers began to observe whether asymmetric dynamics appeared during turmoil periods in the financial markets to better understand the fluctuations of asset prices (Jurado et al., 2015; Uribe et al., 2017). As a matter of fact, some studies are very interested in the impact of financial crises on the link between the financial stress and oil market (Gkillas et al., 2020; Gupta et al., 2019), and gives proof of the leading role of the financial stress in financial markets. Nazlioglu et al., (2015) investigate the volatility transmission between oil prices and financial stress over the period of 1991–2014, suggesting that oil prices and financial stress have been dominated by a long-term volatility. However, there is a causality ranging from the oil prices to financial stress after the global crisis, and from financial stress to oil prices in the crisis. Studies by other researches show that oil gradually loses its hedging ability (Selmi et al., 2018).

This article considers the reaction of the GCC stock–bond hedging asset and the oil hedging to the influence of financial stress. Thus, oil and financial uncertainty can be predictors of each other's future trajectories. This has prompted academic researchers and market agents to focus on predicting financial and economic crises and crashes over the past few decades.

Deep learning is a recent trend in machine learning that offers higher flexibility in learning nonlinear dynamics in large datasets. Convolutional Neural Networks (CNN) are one of the most effective and widely used deep learning approaches. CNN models are able to filter noise in the input data and extract more valuable knowledge for the final prediction model. Convolutional neural network (CNN) is another well-known deep learning and has also been applied in the prediction of COVID-19 cases (Mohimont et al., 2021). Several strands of literature have focused on oil prices’ modeling and forecasting. One group of studies has utilized classical approaches (Aromi & Clements, 2019).

Motivated by these notions, our current study comparatively evaluates the use of machine learning model in hedging with financial stress to achieve well-diversified portfolios for the negative (positive) financial stress.

By doing so, the paper provides new insight to the relative roles of financial stress over oil market volatility and financial markets whether distinguishing between these components improves the accuracy of forecasts for both cases of financial stress. This is especially important for investor, particularly those with earnings that are highly sensitive to energy price fluctuations, as the size of the hedge positions and the implementation of conditional hedging strategies are determined by forecasts. The principal novelty in our empirical study consists of verifies whether the relative effectiveness of hedging driven by machine learning models (1D-CNN) is significantly influenced by the presence of financial stress and the financial markets, specifically during the oil price crashes and the COVID-19 pandemic. Based on machine learning algorithms, these papers analyze portfolio diversification based on different financial stress cases, and we propose the impact of the regime of financial stress based on hedging predicting relations among stock–bond markets.

More interestingly, we aim to contribute to the literature on financial stress forecasting to help investors make decisions. Firstly, we utilize the 1D-CNN model to forecast financial stress. This is an early entry on artificial intelligence. The role of the modeling using the 1D-CNN process focuses on building accurate prediction, statistical analysis, and optimization models. The predication of financial stress during economic and political instability helps understand the effect of financial shocks on investors across GCC countries and offers invaluable insights for policymakers and portfolio managers when diversifying their portfolios. Therefore, the findings of this study demonstrated that machine learning can effectively predict financial stress and help policymakers make appropriate decisions during crises.

Secondly, we examine risk-minimization strategies providing useful information and guidance on portfolio management, and oil-price and asset-price hedging to the impact of financial stress. Specifically, this study analyze and compare the optimal allocation of the portfolio under different situations of financial stress between the oil market and stock–bond markets. This way we provide robust evidence on the potential gains of the proposed forecast hedging strategies taking for the negative (positive) financial stress, using a learning machine (1D-CNN) to the hedging in oil market and financial markets using historical empirical data.

Also, we comparative evaluate the hedging effectiveness in oil and stock–bond markets driven by the proposed learning machine relative to other forms of machine learning as well as econometric approaches. Our study sheds new light on the potential of Brent to act as effective hedges for equity (bond) portfolios in the GCC countries. Moreover, the results of our research provide investors with new ways to design appropriate hedging strategies, using financial stress levels, for portfolio risk management.

The remainder of this paper is structured as follows. Section 2 briefly outlines the related literature. Section3 deals with the econometric methodology. Section4 presents the data set employed. Section 5 reports and discusses the main empirical findings. Finally, Sect. 6 provides some concluding remarks.

2 Literature Review

The crude oil market is complicated and requires a great deal of data. As a result, the price of oil influences the prices of commodities in a variety of marketplaces. As a result, forecasting oil price crashes and spikes has gotten a lot of attention from academics, policymakers, and investors in the last two decades. This time period is notable for its political conflicts, financial and economic crises, upheavals, international wars, pandemics, and other events.

Several strands of literature have concentrated on the modeling and forecasting of oil prices. When controlling for oil market volatility, Demirer et al. (2020) provided critical information for investors and market agents. Other recent studies have used the HAR-RV approach to investigate the forecasting structure of realized volatility for oil price returns (Chen et al., 2020; Gkillas et al., 2020). Moreover, Leng and Li (2020) investigated the dynamic forecasting structure of crude oil prices using Bayesian frameworks. The results of their comparative analysis revealed that both approaches effectively quantified crude oil predictability information. Similarly, Hui et al. (2020) investigated dynamic forecasting for crude oil prices under market crash risk using an asymmetric mean to revert fundamental shocks. They demonstrated a breach in the boundary condition when the oil price fell sharply during the 2008 financial crisis and the 2014 oil shocks.

Besides, as a number of studies on the predictive power of hedging models report mixed results, applying the proposed framework functions as an insurance tool, minimizing the negative consequences of structural breaks and model misspecification, resulting in improved forecasting (Patton & Sheppard, 2009). As a result, we provide a flexible framework in the hedging process in the face of model uncertainty. Some of them use hedging ratios directly as model responses for training and testing, but only a few of them are successful in outperforming naive parametric models (see Hull & White, 2017; Ruf & Wang, 2019). Based on the work of Cao et al. (2020), we develop a simple network to forecast the change in volatility surface, which may provide some insight into learning-based delta hedging research.

A few empirical studies forecasting other commodity prices and financial stress have documented the superiority of machine learning models in its forecasting structure. Nguyen-Ky et al. (2018) and Alameer et al. (2020). Polat (2020) investigates the influence of oil price volatility on the financial stress index in the United States using a structural VAR approach and shows that the oil price volatility shock has a statistically positive and durable effect on financial stress. Furthermore, Gkillas et al. (2020) discover that financial stress improves oil price forecasts. The author’s use various financial stress indexes and emphasize that special attention should be paid to financial volatility originating in the United States in order to correctly predict the oil price dynamics.

However, although the above-mentioned work has provided wealthy suggestions to investigate the link between the financial stress and oil markets, no one concerns the forecasts of financial stress on oil and financial markets using machine learning approaches is scant, particularly during the COVID-19 pandemic. To the best of our knowledge, this empirical research is the first to forecast financial stress during the COVID-19 pandemic using advanced machine learning techniques. We augment our analysis with popular robustness tests.

3 Empirical Methodology

Accordingly, this paper aims at looking into the impact of the regime of financial stress based on hedging predicting relations among oil and GCC stock–bond markets.

For our modeling purpose, we use a three-step framework. The first one consists in constructing a financial stress index (FSI) for GCC economies that can be used as a tool to help monitor, identify, and resolve any potential crisis. They are better equipped to maintain the financial and economic stability. The second step consists assessing the role of financial stress predictability of oil market, the stock markets and the bond ones. More specifically, we illustrate a novel approach for financial stress trend prediction based on One-Dimensional Convolutional Neural Network (1D CNN) models (Kiranyaz et al., 2015). CNN is excellent for filtering out noise in input data and extracting more beneficial features for the final forecasting model. Finally, based on machine learning algorithms, these papers analyze portfolio diversification based on different financial stress cases. We estimate the hedging ratio and hedging effectiveness prediction models in the case of the positive (negative) financial stress. This is what sets our work apart from the existing literature on this topic, which in turn will help improve the investors in risk management, portfolio optimization, and hedging choices.

3.1 Construction of the Financial Stress Index

A financial stress index measures the current state of instability of the financial system by combining a number of individual stress indicators representative of the major financial market segments into a single index. There are four steps in the construction of FSIs that must be carefully considered: the selection of financial markets to include, the selection of specific market stress indicators, the transformation of market-specific stress indicators, and finally the aggregation of these stress indicators in the composite financial stress index. The first and second steps are primarily related to data availability and data collection, while the last two are associated with the choice of methodology, and are discussed in more detail with the FSI methodology.

The dataset used to construct the Financial Stress Indices is based on weekly observations extracted from the DataStream database over the period from January 1, 2007 to October 28, 2020, covering the global financial crisis, oil shock and the most recent events in the region such as the coronavirus crisis. The sample includes the Gulf countries: Bahrain, Saudi Arabia, Kuwait, Oman, Qatar, and the United Arab Emirates, all selected based on data availability.

For calculating the FSI, we use seven indicators for each country (Table 1). These indicators of the advanced economies and financial index are the Stock market returns, Stock volatility, EMPI, β-banking sector, Sovereign spreads, Inverted term spreads, and TED spreads. Examining these sub-components can help identify the types of financial stress that have been associated with greater output consequences (Cardarelli et al., 2011). The FSI is constructed by the equal variance-weighted average. Under this method, each component is computed as a deviation from its mean, and weighted by the inverse of its variance (similar to Kaminsky & Reinhart, 2000). The equal weighting variance approach is a very effective method for constructing financial indices owing to the simplicity of the calculations, and the precision with which it represents and indicates the stress and turbulence episodes (for instance, Kliesen et al., 2012; MacDonald et al., 2018; and Mezghani & Boujelbène-Abbes., 2021).

According to this approach, an FSI is generated, giving equal prominence to each component variable computed as \(Y_{t} = \frac{{\left( {X_{t} - \overline{X}_{t} } \right)}}{\sigma }\), where Yt is the degraded and standardized series, Xt is the average of the series, and σ is the standard deviation of the series. In this paper, the components of the FSI are as follows:

where, Yjt is standardised financial variables at time t, and n represents the number of standardised variables used in constructing FSI for each country (Vermeulen et al., 2015).

Later on, we split the financial stress into positive and negative financial stress as well as the determinants of predicting under bear and bull market status, using a common filtration CF, and are defined as:

Such that the decomposition, FSI = FSI+ + FSI−, holds exactly for any n. accordingly, negative and positive financial stress relates to the financial stress bad and good state. The later part discusses how both positive and negative states might spillover differently across the markets in order to create best-performing cases in the predictability.

3.2 Out-of-Sample Predictability, Using 1D-CNN Model

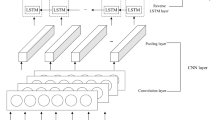

In the section, we are technically illustrating an alternative approach, the nonparametric 1D-CNN model, so that we estimate the set of hedging for the same purpose. This multivariate statistical/machine learning method is capable of performing a nonlinear projection and functional mapping in the N-th dimensional space. In their original form, CNNs are a typical class of deep neural networks. The movement direction of the 1D-CNN filter is unidirectional, and it has a strong feature-learning ability.

The model understands how to extract features from observational sequences, and how to map hidden layers to different types of software (malware or benign).

where X: x1,..., xN indicates the input of the network, and Y: \(\hat{y}\) is the output. Therefore,

the network learns a mapping from the input space X to the output space Y.

The key block of the convolutional network is the convolutional layer. A group of trainable filters is the parameters of this layer (scan windows). Each filter operates in size through a tiny window. The scanning window sequentially traverses the whole picture during the forward propagation of the signal (from the first layer to the last layer) according to the tiling principle, andit measures the dot products of two vectors: the filter values, and the outputs of the chosen neurons.

The network uses filters that are enabled when there is an input signal of some kind. A series of filters is used for each convolutional layer, and each generates a different activation map.

where k is the convolution kernel, j is the size of kernels, M is the number of inputs \(x_{i}^{I - 1}\), b is the kernel bias, f () is the neuron activation function, and (.) represents the convolution operator.

The sub-sampling layer is another feature of a convolutional neural network. It is usually positioned between successive convolution layers, so it may occur periodically. Its purpose is to reduce the spatial size of the vector gradually to reduce the number of network parameters and calculations, as well as to balance over fitting.

3.3 Portfolio management and hedging strategies

We next analyze whether this predictability can be exploited in portfolio strategies that account for short-selling constraints and other restrictions in the GCC market.

We calculate optimal hedge ratios and optimal portfolio weights among oil returns and across markets for each negative and positive case of the FSI. Particularly, we quantify the impact of the negative and positive financial stress on minimizing unwanted risk without reducing expected returns.

Theoretically, several studies (Arouri et al., 2012) show that the low hedge ratios indicate that the asset can be qualified as cheap hedging. In addition, a higher volatility of a hedging ratio implies a higher hedging costbecause investors will rebalance their portfolios more frequently (Junttila et al., 2018).

In order to minimize risk, the dynamic hedge ratio, based on conditional information available at t, is as follows:

where β12,t is the risk-minimizing hedge ratio for oil and Stock–Bond market prices, \(h_{12,t}\) is the conditional covariance between oil and Stock–Bond markets at time t, and \(h_{22,t}\) is the conditional variance of the oil market, and Stock–Bond market index.

In the case of optimal portfolio weights, the estimated covariance matrices taken from the BEKK–GARCH model are used to compute the optimal portfolio holdings that minimize the portfolio risk, assuming the expected returns are zero. Applying the methods of Kroner and Ng (1998), the optimal portfolio weight of the two assets (oil and stock market index; oil and Bond markets) at each negative and positive level of the financial stress is given as

where \(\omega_{12,t}\) is the weight of the Stock–Bond markets and the oil one at time t in a one-dollar portfolio; \(h_{12,t}\) is the conditional covariance between oil market and Stock–Bond ones;\(h_{11,t}\) is the conditional variances of the Stock–Bond and oil markets, while the weight of asset j is computed as \(\left( {1 - \omega_{12,t} } \right)\).

Finally, we analyze the hedging effectiveness of sample variables. Hedging effectiveness is the reduction in the variance of the hedged portfolio compared to the unhedged one. The performance of the optimal coverage ratio is measured by the Hedging efficiency index (HE).

The choice of any hedging strategy depends on the investor's objective.

Following Ku et al., (2007), the hedging effectiveness of the constructed portfolios can be assessed by comparing the realized hedging errors, which are determined as follows:

where the variances of the hedge portfolio (\(VAR_{hedged}\)) are from the variance of the returns of the weighted portfolio of stock and bond markets (PF II), whereas the variance of the unhedged portfolio (\(VAR_{unhedged}\)) is the variance of the returns on the benchmark portfolio (PF I). A higher HE ratio implies a greater hedging effectiveness in terms of the portfolio—variance reduction, which thus implies that the associated investment policy can be considered as a better hedging strategy.

4 Data, and Descriptive Statistics

This study makes use of weekly data for the four variables over the period ranging from January 1, 2007 to October 28, 2020 representing a total of 723 trading days. This period include major events as: the 2008 global financial crisis, the 2008 oil shock, the 2014 oil drop and covid-19 crisis. The two indices in USD included in this study are the Dow Jones conventional GCC (DJGCC) and Dow Jones conventional Bond index (DJCBP). All data are obtained from the DataStream database. The Brent crude-oil price series is extracted from the Energy Information Administration (EIA). We construct the GCC financial stress index (FSI), covering the weekly period from 2007 to 2020. Start and end dates are solely dictated by the availability of financial stress measurement data. Extending the sampling period with more crisis episodes will allow the analysis to provide results that are more reliable. Data has been collected from two sources: Datastream Databases, and Central Bank of the GCC Republic.

For the purpose of the study, the data was split into two parts—the in-sample and the out-sample data for the negative (positive) financial stress. The first time period, from January 2007 through October 2020 is considered as the in-sample period parameter estimation.

Out-of-sample hedging effectiveness is evaluated over the second time period, the 85% trading days in the sample period are chosen as the training set to train model, and the remaining 15% part of data is used as a testing set. We adapted a sliding window with retraining approach where we chose a 5 year period for training and the following 1 year for testing, i.e. training period: 2007–2018, testing period: 2019. Then we moved both training and testing periods one year ahead, retrained the model and tested with the following year,i.e. training period: 2008–2019, testing period: 2020. As a result, each year between 2007 and 2020 is tested using repeated retraining. The models developed through in-sample data will be tested for forecasting performance on out-sample data for different levels of financial stress.

Each dataset is then used to train a Convolutional Neural Network model to test the main determinants to forecast financial stress index. Specifically, there are five major steps, namely data collection, all data are divided into testing and training sets according to the data collection time, as well as returns forecasting, and the testing set is used to test the models and calculate the mean squared error (MSE) and mean absolute error (DM) (Fig. 1).

Overview of the empirical design

Figure 2 reflects the dynamic changes of FSI, Oil and GCC financial markets all along the period ranging from 1/12/2006 to 28/10/2020. The series contain increased fluctuations during the 2008 crisis, the 2014 oil drop choc and the COVID'19 health crisis in which there have been many negative repercussions on the world economy. According to the series of returns, it is clearly be noticed that the financial stress and oil market are characterized by high fluctuations especially in the oil drop periods and COVID’19 choc.

Weekly returns of the GCC stock markets and bond markets

In addition, GCC stock markets and bond markets fell because of the oil drop, mainly due to the decline in demand brought about by the global economic crisis, Shale revolution and the appreciation of the US dollar. These factors have weighed heavily on global economic growth, particularly the exporting countries (the decline in their foreign exchange reserves and in their currency). Indeed, most of stock–bond indices are characterized by high fluctuations especially in the period of COVID’19 pandemic. This finding is in line with the existing literature (e.g., Balcilar et al., 2020; Belhassine, 2020; Nazlioglu et al., 2015; Qin et al., 2020; and Mezghani & Boujelbène, 2018) showing that volatility and risk spillover effects from the oil market to other financial markets intensified during the period of the turbulent crisis.

Table 2 reports the descriptive statistics on the positive and negative GCC Financial Stress for oil market, stock markets and bond markets weekly returns. It also shows that GCC positive financial stress the average returns of oil market and GCC stock markets have a negative value, implying that the oil market and stock markets present a downward trend during this period. DJIGC shows the lowest mean volatilities and standard deviations in all three categories, whereas Brent exhibit the highest average volatilities and relatively high risk. The higher volatility of oil prices runs contrary to Gkillas et al., (2020), who argued for financial stress improving oil price forecasts. It is common knowledge that, skewness is a simple measure of asymmetry, and kurtosis is a measurement for peaked or flatted distribution relative to a normal one. According to the skewness and kurtosis indicators, as well as the Jarque–Bera test, all the series significantly deviate from the normal distribution.

Subsequently, the pairwise correlation is tested between return series and illustrated in Table 3. It is clearly noticeable that the correlation is accentuated between the Brent and indices returns for both cases financial stress. The highest correlation is observed between GCC Stock and Brent markets for positive and negative financial stress. These results may imply some opportunities for hedging or diversification in some cases.

Similarly, the magnitude of the correlation is negatively and least for negative financial stress case between Brent and bond markets, − 0.05, followed by DJGCC and DJCBP, − 0.11, which implies that the financial stress as a safe haven asset offer a possible diversification advantage for investors.

5 Empirical Results and Discussion

This section presents results from the predictability of the positive and negative financial stress over the oil and GCC financial markets during the crisis period and its implications on hedging strategies.

5.1 Predictability of Financial Stress on Oil and Financial Markets

In this section, we aimed to identify the predictability of the positive and negative financial stress, and to screen for more effective predictors. Figures 3 and 4 shows the importance of efficiency for each positive (negative) financial stress cases in the financial markets obtained from the 1D-CNN model. Figures 3 and 4 are prediction graphs of oil and financial returns prediction model on the positive (negative) financial stress. Each graph has two sub-graphs, and the upper sub-graph is the comparison between predicted values and actual values, where the prediction results of each prediction model are marked with different colors and curve types; the lower sub-graph is the comparison of prediction errors. As for see, the blue line refers to the original financial returns. The orange line indicates the predicted price from the proposed CNN.

Results testing the positive financial stress impact on oil and financial markets

Results testing the negative financial stress impact on oil and financial markets

For positive financial stress, we show that the positive financial stress affects largely the oil market and stock–bond markets, the majority of markets follow the same trend as with the financial stress, there was almost a superposition of the two graphs the original and the predictive one which affirms the financial stress is significantly predicts financial markets in the turbulence period. Therefore, The Brent is a strong predictor of the stock–bond markets.

There was almost an overlay of the two charts the original and the predictive, which claims that this index significantly predicts financial stress during the turbulent period. The results are consistent with existing studies (e.g., Aye et al., 2015; Elder & Serletis, 2011) that find evidence for the recessionary impacts of oil price uncertainty on both real and financial activity.

For negative financial stress, the oil market is mainly a reaction to negative financial stress.

Interestingly, the prediction performance improvement of the stock–bond markets are more significant on the financial stress. The results show that the algorithm of the scheme is feasible and effective, and it can better predict the changes in the financial markets. So, financial indicators help and support traders every day during their trading processes. FSI has a strong effect on improving the forecasting effect of oil volatility. Increased instability of the financial system may affect worldwide economic activities.

Finally, in order to check the statistical significance of 1D-CNN’s superiority over the full model and the nested sampling models, we have applied the Diebold and Mariano (1995) (DM) predictive accuracy test. Table 4 shows the estimated mean squared error (MSE) for sampling models. We note that the DM statistics are significantly positive, suggesting that the iterated combination approaches exhibit significantly better out-of-sample performance in the prediction of different financial stress regimes. Overall, researchers and investors should closely oil market in order to benefit from predicting financial stress and realizing better performance in portfolio diversification.

5.2 Out-Sample Implications for Portfolio Management and Hedging Strategies

This subsection explores the financial significance of asset allocation and risk management results for the financial markets and oil market in the case of the positive (negative) financial stress. We estimate Out-of-Sample Predictability of financial stress according to the strategies previously studied.

5.2.1 Hedging Price Forecast

In this section, we instead investigate the opportunity for hedging financial stress from considering oil and stock–bond markets ex ante. For this purpose, we evaluate the out-of-sample performance of the optimal portfolios of statistical learning machines to explain which hedge strategy allows us to achieve a more effective hedge policy.

The study is especially attractive because the out‐sample analysis is performed over the period of the recent coronavirus crises and could thus prove which different financial stress cases work better in periods of market uncertainty. Chong and Lam (2010) suggested that out-of-the-sample evaluation of models is more appropriate because traders are more concerned with future performance. To efficiently hold diversified portfolios and manage risk, we analyze the BEKK-GARCH model, Out of sample estimates of portfolio weights, hedge ratios in the positive (negative) financial stress, respectively are presented in Table 5.

In the negative financial stress, we find that the optimal weights exceed 0.5, with the exception of the DJGCC/DJCBP portfolio. This indicates that for every one dollar invested in DJCBP/Brent, investors should invest 0.8748 dollars in DJCBP and the remaining budget (0.1252 dollars) in oil market. As for stock markets, it reveals that the optimal allocation for Brent in a one-dollar DJGCC/Brent portfolio should be 0.5702 dollars in stock and 0.4298 dollars in oil market. In the positive financial stress, we observe that the proportion invested in oil market increases for all stock–bond markets. The highest optimal weight is for the DJCBP/Brent and the lowest is for the DJGCC/DJCBP. Our results demonstrate that oil offers the best performance on hedging the risk in stock–bond markets (Mezghani et al., 2021). The responsiveness of stock markets to oil price shocks is highly dependent on whether the country is a net oil-importing or oil-exporting economy (Hashmi et al., 2021; Jiang & Yoon, 2020; Mokni, 2020).

Moreover, the Out-of-sample estimates of optimal hedge ratio values are relatively low in the negative (positive) financial stress. It varies from 0.0283 (0.0573) for DJCBP/Brent portfolio to 0.1886 (0.2456) for DJGCC/Brent in the negative (in the positive) financial stress. This indicates that the bond market can be hedged by taking a short position in the oil market and a long position in bonds. The values of the hedge ratios are generally low, indicating a highly effective hedge in the considered GCC stock markets. This result is consistent with the findings of Khalfaoui et al., (2015), who find a low of hedge ratios in the case of G-7 countries. For the DJGCC/Brent portfolio, the hedge ratio is 0.1886 at the negative case and 0.2456 at a positive case and reveals that one-dollar long position (purchase) in the stock market should be shorted by 1886 cents of Brent in the negative case and 2456 cents in the positive case.

For negative (positive) financial stress, the hedge ratios are negative for stock indices and bond markets. The negative values arising from the inverse relationship between bond and stock indices suggest that the hedge is formed by taking either long or short positions for both assets (i.e. bond and stock indices).

Moving to the HE results, where a higher HE index indicates a higher hedging effectiveness, we see that, DJCBP/Brent produces higher HE values than DJGCC/Brent for each of the negative (positive) financial stress, suggesting that oil is a more valuable hedge for bonds than stocks. This result is in accordance with previous works (Basher & Sadorsky, 2006; Mensi et al., 2013).With this evidence, it appears clear that the 1D-CNN model lead to better forecasts of the hedging strategies and a greater risk reduction in the negative (positive) financial stress cases. Specifically, Xu et al., (2020) investigate oil as a hedging asset and investigate the dynamic correlation of crude oil and stock market price fluctuations in the four economies of the United States, Japan, China, and Hong Kong. Crude oil can be utilized as a hedging asset for underlying assets under certain conditions, according to empirical research.

5.2.2 The Dynamic of Hedge Ratio, Optimal Portfolio Weights and Hedging Effectiveness

Figures 5 and 6 shows the Out-of-sample estimates of dynamic hedge ratio, optimal portfolio weights and hedging effectiveness from the estimates of the 1D-CNN model outperform the effectiveness in terms of variance reduction in the out‐sample analysis for different financial stress cases.

Dynamic of optimal weight ratios and hedge ratio under positive financial stress

Dynamic of optimal weight ratios and hedge ratio under negative financial stress

For positive and negative financial stress, this figure illustrates a higher variability of the estimated hedge ratio for the financial markets and oil markets. The trajectories of these markets show significant changes during the 2008 financial crisis and 2014 oil price drop, and especially the COVID-19 pandemic crisis.

Figure 5 and 6 presents the Out-of-sample estimates of time-varying optimal weights of oil and stock–bond markets in an optimal portfolio. It can be seen that the weights of the constituents of the stock-oil and bond-oil portfolios are fluctuating a lot over a period of time. This does not mean that the portfolio manager has to rebalance the portfolio at each point of time which may lead to increased transaction costs. Portfolio managers can look for average weights of the constituents of a portfolio over a period of time and rebalance the portfolio by purchasing the under-weighted asset and selling the over-weighted asset. As a result, there is scientific evidence that oil can be utilized as a hedge and safe haven asset against asset classes other than stock markets. According to Bahloul and Gupta (2018), the oil market is frequently regarded as an alternative investment. Furthermore, financial stress and crude oil prices are influenced by a variety of factors, including economic considerations and investor behavior (Nazlioglu et al., 2015).

More importantly, HE is higher in the positive financial stress than in the negative financial stress (Fig. 7). In the positive financial stress, HE is the highest for DJCBP/Brent (80%) and the lowest for DJGCC/Brent (50%) for the whole period. This result persists during the financial crises, crude oil price crash and the COVID-19 spread. These results suggest that internalization of the time-varying hedging effectiveness estimation is valuable to such strategies. These results imply that nonlinear models exhibit a higher hedging effectiveness. This greater out‐sample effectiveness of nonlinear models could occur because they offer more accurate forecasting than more parsimonious models (Marcucci, 2005).

Hedging effectiveness under negative and positive financial stress

As a result, according to optimal portfolio weights and hedge ratios, oil assets are a useful tool for reducing portfolio risk in the studied markets. The investors, however, should choose more stocks than oil assets to form an optimal portfolio in case of oil importing countries, while in the case of oil-exporting countries, investors should select more oil than stocks assets to form an optimal portfolio. It's worth noting that our research confirm from that of Gkillas et al., (2020), who discovered that the FSI can aid predicting performance with multiple extended HAR models. The authors specifically incorporated financial stress indicators into the forecasting system.

6 Robustness Tests: Predictability at Monthly Horizon

The results reported in the previous section suggest that oil offers greater diversification potential and lower total portfolio allocation risk. To further validate our results, we investigate the dynamic evolution of portfolio weight and hedge ratio, using monthly data of the financial market index and oil index from 2007 to 2020 in order to compare the results with those found during the period of the financial crisis, the oil crisis and the covid-19 pandemic. Thus, we find that all the results of hedging strategies are robust to model refits (see Table 5).

The results in Table 6 show that in a negative GCC financial stress, DJCBP/Brent has the highest optimal weight (77.85%), followed by DJGCC/Brent (75.88%). The optimal weight for DJCBP suggests that investors in Brent should invest 77.85 cents in DJCBP and the remaining 22.15 cents in Brent for an optimal one-dollar DJCBP/Brent.

Comparing the optimal weights of the positive GCC financial stress, we note that the optimal weights in DJCBP/Brent are constantly higher than the corresponding weights in negative financial stress. Thus, investors in DJCBP should invest more in the oil market than investors in DJGCC for an optimal positive financial stress. It indicates that our results are also robust to the choice of distribution.

On the other hand, Table 6 shows the robustness of our results on the hedge ratios for negative financial stress and positive financial stress. Table 6 shows that negative GCC financial stress maintain, on the highest hedge ratio (44.42%) in an optimal DJCBP/Brent.

We observe similar results for the optimal hedge ratios for positive GCC financial stress, the most expensive hedge ratio (17.61%) in an optimal DJCBP/Brent. These findings imply that a one-dollar long position in DJCBP should be hedged with a short position of 44.42 and 17.61 cents in the oil market, for negative (positive) financial stress respectively, indicating that these markets are expected to occupy a long position on these bond, and bypass the oil market, as shown in Table 5. These results provide evidence that investors can hedge portfolio risk by buying more oil asset.

In addition, the stock and oil markets have negative values of hedge ratios for negative and positive financial stress, suggesting that investors should take short positions in stock markets and long positions in the oil market. For instance, the optimal hedge ratios of -0.582 imply that a one-dollar long position in DJGCC should be hedged with another long position of 0.582 cents in the oil market for negative financial stress.

Interestingly, we note that the average optimal hedge ratio between the stock market and bond market is very low, which means that one dollar long on the stock market should be shorted by only a few cents on the bond market.

In addition, Table 6 shows that the largest hedge effectiveness measure is DJCBP/Brent, which indicates that including DJCBP in the oil market significantly reduces the portfolio risk by 0.6389 (0.7018) as opposed to the unhedged portfolio for negative (positive) financial stress respectively. On the other hand, DJGCC/DJCBP offers near no diversification benefits in both negative and positive GCC Financial Stress.

In summary, this confirms that the both cases of financial stress does enhance the predictive performance of the model for the oil market in a time-varying framework.

Finally, the robustness check validates the estimates of dynamics of hedge effectiveness, using monthly financial markets and oil market. The results indicate that in the positive financial stress index, the hedge effectiveness are high, and range from 91 to 99%, implying that investors should have more oil than the financial markets in their portfolio to minimize risk without reducing expected returns (Mezghani et al., 2021) (Fig. 8).

Monthly Hedging effectiveness under negative and positive financial stress

7 Conclusion

Forecasting financial stress is important for practitioners and policymakers alike, because a thorough understanding of financial linkage breakdown during a crisis can greatly aid administration strategy selection and contingency planning. In this paper, we predicts financial stress while controlling for the Financial Crisis, oil shocks and the covid-19 pandemic, which provides important implications for portfolio managers when diversifying their portfolios by investing in GCC countries. Our study adds to the debate by clarifying how does forecasting financial stress affect oil and financial markets? For this purpose, we have applied and compare the time-varying optimal portfolio allocation between the oil market and stock–bond markets for the negative and positive financial stress. Specifically, this provides insights into portfolio optimization between the oil price, stock markets and bond ones, and smoothing the strategies of portfolio risk.

This study selects the most significant financial market indicators, which can be used to predict financial stress tail events, using a novel technique based on the one-dimensional convolutional neural network (1D-CNN). The empirical results indicate that the financial stress has a strong effect on improving the forecasting effect of oil market. Increased instability of the financial system may affect worldwide economic activities. As one of the most important energy sources, crude oil is obviously inseparable from economic activity (Naeem et al., 2020). The key message to be taken home from the alternative specifications, financial stress does have predictive value for oil, where different types of investors benefit from monitoring different regional sources of financial stress.

These findings have prominent implications for investors and portfolio managers. Investing in Brent as a complement to stock (bond) market investments offers a better way for the investor to diversify their portfolio when their expectations are heterogeneous in terms of financial system instability and risk tolerance. Moreover, we have especially looked into whether the oil market and financial markets could serve as efficient hedging instruments against the aggregate financial stress risks by calculating first the optimal hedge ratios, and then calculating the optimal weights in portfolios consisting of these assets for each negative and positive case of the FSI. Regarding the portfolio hedging of DJGCC/Brent and DJCBP/Brent, the results of average optimal weights indicate the importance of oil for making an optimal portfolio consisting of stocks and bonds. For the positive case of financial stress, DJGCC/DJCBP and DJCBP/Brent have average optimal weights above 0.5, which shows that investors should spend more than fifty percent of their investment on the stock market, and the remaining percentage on the bond market. Moreover, the findings of the hedge ratio are slightly different, but its results also emphasize the role of oil in hedging portfolio risk. Even more, we prove that for bond markets, the optimal hedge strategy is not effective to reduce the level of risk.

The robustness test shows a similar to the result ‘‘oil prices indicate efficient performance in the estimation for positive and negative financial stress’’.

Finally, the predication of financial stress during economic and political instability helps understand the effect of financial shocks on corporations across countries and offers invaluable insights for policymakers and portfolio managers when diversifying their portfolios. What policy implications and investment advice can be derived from our forecasting analysis? On the one hand, when considering the influence of oil and financial markets, policymakers should explicitly focus on fluctuations in financial stress. In the meantime, taking into account the oil shocks and the Covid-19 pandemic is useful to analyze the importance of financial stress on the economic environment. Thus, Governments of oil exporting countries should put in place an information sharing framework for risk connectivity. Moreover, policymakers must make corresponding policy decisions over time due to the different time-varying characteristics of changes in financial stress, oil, and financial markets. Risk spillovers between the oil and equity markets should also be monitored by policymakers and investors. This is especially true during major crises. Furthermore, this will help encourage them to adopt alternative risk-avoiding steps during a particular time frame.

On the other hand, increased financial stress could trigger turmoil in the markets, further leading to extreme anomalies in the oil market. Investors who traded crude oil would become more passive. In this case, improved forecasting power for crude oil volatility could aid investors in resetting their portfolios ahead of time and avoiding greater economic losses, and the policymakers supervising the financial uncertainty could better prevent and control of financial market risks.

Finally, future research can explore more interpretable machine learning algorithms and more predictive macroeconomic variables and other popular safe havens like Bitcoin, which too has recently gained some popularity as a hedge against financial market risks.

References

Alameer, Z., Fathalla, A., Li, K., Ye, H., & Jianhua, Z. (2020). Multistep-ahead forecasting of coal prices using a hybrid deep learning model. Resources Policy, 65, 101588.

Arezki, R., Lederman, D., Abou Harb, A., El-Mallakh, N., Fan, R. Y., Islam, A. & Zouaidi, M. (2020). Middle east and north africa economic update, april 2020: How transparency can help the middle East and North Africa.

Aromi, D., & Clements, A. (2019). Spillovers between the oil sector and the S&P500: The impact of information flow about crude oil. Energy Economics, 81, 187–196.

Arouri, M., et al. (2012). On the impacts of oil price fluctuations on European equity markets: Volatility spillover and hedging effectiveness. Energy Economics, 34(2), 611–617.

Aye, G., Gupta, R., Hammoudeh, S., & Kim, W. J. (2015). Forecasting the price of gold using dynamic model averaging. International Review of Financial Analysis, 41, 257–266.

Bahloul, W., & Gupta, R. (2018). Impact of macroeconomic news surprises and uncertainty for major economies on returns and volatility of oil futures. International Economics, 156, 247–253.

Balcilar, M., Renton, G., Héroux, P., Gaüzère, B., Adam, S., & Honeine, P. (2020). Analyzing the expressive power of graph neural networks in a spectral perspective. In International Conference on Learning Representations.

Basher, S. A., & Sadorsky, P. (2006). Oil price risk and emerging stock markets. Global Finance Journal, 17(2), 224–251.

Belhassine, O. (2020). Volatility spillovers and hedging effectiveness between the oil market and Eurozone sectors: A tale of two crises. Research in International Business and Finance, 53, 101195.

Cao, J., Chen, J., & Hull, J. (2020). A neural network approach to understanding implied volatility movements. Quantitative Finance, 20(9), 1405–1413.

Cardarelli, R., Elekdag, S., & Lall, S. (2011). Financial stress and economic contractions. Journal of Financial Stability, 7, 78–97.

Chen, W., Ma, F., Wei, Y., & Liu, J. (2020). Forecasting oil price volatility using high-frequency data: New evidence. International Review of Economics & Finance, 66, 1–12.

Chong, T. T. L., & Lam, T. H. (2010). Predictability of nonlinear trading rules in the US stock market. Quantitative Finance, 10(9), 1067–1076.

Demirer, R., Gupta, R., Pierdzioch, C., & Shahzad, S. J. H. (2020). The predictive power of oil price shocks on realized volatility of oil: A note. Resources Policy, 69, 101856.

Diebold, F. X., & Mariano, R. S. (1995). Comparing predictive accuracy. Journal of Business and Economic Statistics, 13, 253–263.

Elder, J., & Serletis, A. (2011). Volatility in oil prices and manufacturing activity: An investigation of real options. Macroeconomic Dynamics, 15(S3), 379–395.

Filzen, J. J., & Schutte, M. G. (2017). Comovement, financial reporting complexity, and information markets: Evidence from the effect of changes in 10-Q lengths on internet search volumes and peer correlations. The North American Journal of Economics and Finance, 39, 19–37.

Gkillas, K., Gupta, R., & Pierdzioch, C. (2020). Forecasting realized oil-price volatility: The role of financial stress and asymmetric loss. Journal of International Money and Finance, 104, 102137.

Gupta, R., et al. (2019). Time-varying predictability of oil market movements over a century of data: The role of US financial stress. The North American Journal of Economics and Finance, 50, 100994.

Hashmi, S. M., Chang, B. H., & Bhutto, N. A. (2021). Asymmetric effect of oil prices on stock market prices: New evidence from oil-exporting and oil-importing countries. Resources Policy, 70, 101946.

Hui, C. H., Lo, C. F., Cheung, C. H., & Wong, A. (2020). Crude oil price dynamics with crash risk under fundamental shocks. The North American Journal of Economics and Finance, 54, 101238.

Hull, J., & White, A. (2017). Optimal delta hedging for options. Journal of Banking & Finance, 82, 180–190.

Jiang, Z., & Yoon, S. M. (2020). Dynamic co-movement between oil and stock markets in oil-importing and oil-exporting countries: Two types of wavelet analysis. Energy Economics, 90, 104835.

Junttila, J. P., et al. (2018). Commodity market based hedging against stock market risk in times of financial crisis: The case of crude oil and gold. Journal of International Financial Markets Institutions and Money, 56, 255–280.

Jurado, K., Ludvigson, S. C., & Ng, S. (2015). Measuring uncertainty. American Economic Review, 105(3), 1177–1216.

Kaminsky, G. L., & Reinhart, C. M. (2000). On crises, contagion and confusion. Journal of International Economics, 51, 145–168.

Khalfaoui, R., et al. (2015). Analyzing volatility spillovers and hedging between oil and stock markets: Evidence from wavelet analysis. Energy Economics, 49, 540–549.

Kiranyaz, S., Ince, T., Hamila, R., & Gabbouj, M. (2015). Convolutional neural networks for patient-specific ECG classification. In 2015 37th Annual International Conference of the IEEE Engineering in Medicine and Biology Society (EMBC) (pp. 2608–2611). IEEE.

Kliesen, K. L., Owyang, M. T., & Vermann, E. K. (2012). Disentangling diverse measures: A survey of financial stress indexes, Federal Reserve Bank of St. Louis Review, 94(5), 369–398.

Kroner, K. F., & Ng, V. K. (1998). Modeling asymmetric comovements of asset returns. The Review of Financial Studies, 11(4), 817–844.

Ku, et al. (2007). On the application of the dynamic conditional correlation model in estimating optimal time-varying hedge ratios. Applied Economics Letters, 14(7), 503–509.

Leng, N., & Li, J. C. (2020). Forecasting the crude oil prices based on econophysics and bayesian approach. Physica a: Statistical Mechanics and Its Applications, 554, 124663.

MacDonald, et al. (2018). Volatility co-movements and spillover effects within the eurozone economies: A multivariate GARCH approach using the financial stress index. Journal of International Financial Markets Institutions and Money, 52, 17–36.

Marcucci, J. (2005). Forecasting stock market volatility with regime-switching GARCH models. Studies in Nonlinear Dynamics & Econometrics. https://doi.org/10.2202/1558-3708.1145

Mensi, W., Beljid, M., Boubaker, A., & Managi, S. (2013). Correlations and volatility spillovers across commodity and stock markets: Linking energies, food, and gold. Economic Modelling, 32, 15–22.

Mensi, W., Hammoudeh, S. M., Sensoy, A., & Kang, S. H. (2017). Dynamic risk spillovers between gold, oil prices and conventional, sustainability and Islamic equity aggregate and sectors with portfolio implications. Energy Economics, Forthcoming,. https://doi.org/10.1016/j.eneco.2017.08.031

Mezghani, T., Ben Hamadou, F., & Boujelbène Abbes, M. (2021). The dynamic network connectedness and hedging strategies across stock markets and commodities: COVID-19 pandemic effect. Asia-Pacific Journal of Business Administration, 13(4), 520–552. https://doi.org/10.1108/APJBA-01-2021-0036

Mezghani, T., & Boujelbène, M. (2018). The contagion effect between the oil market, and the Islamic and conventional stock markets of the GCC country: Behavioral explanation. International Journal of Islamic and Middle Eastern Finance and Management, 11(2), 157–181.

Mezghani, T., & Boujelbène-Abbes, M. (2021). Financial stress effects on financial markets: Dynamic connectedness and portfolio hedging. International Journal of Emerging Markets. https://doi.org/10.1108/IJOEM-06-2020-0619

Mohimont, L., Chemchem, A., Alin, F., Krajecki, M., & Steffenel, L. A. (2021). Convolutional neural networks and temporal CNNs for COVID-19 forecasting in France. Applied Intelligence, 51(12), 8784–8809.

Mokni, K. (2020). Time-varying effect of oil price shocks on the stock market returns: Evidence from oil-importing and oil-exporting countries. Energy Reports, 6, 605–619.

Naeem, M. A., Peng, Z., Suleman, M. T., Nepal, R., & Shahzad, S. J. H. (2020). Time and frequency connectedness among oil shocks, electricity and clean energy markets. Energy Economics, 91, 104914.

Nazlioglu, S., Soytas, U., & Gupta, R. (2015). Oil prices and financial stress: A volatility spillover analysis. Energy Policy, 82, 278–288.

Nguyen-Ky, T., Mushtaq, S., Loch, A., Reardon-Smith, K., An-Vo, D. A., Ngo-Cong, D., & Tran-Cong, T. (2018). Predicting water allocation trade prices using a hybrid artificial neural network-bayesian modelling approach. Journal of Hydrology, 567, 781–791.

Patton, A. J., & Sheppard, K. (2009). Evaluating volatility and correlation forecasts. Handbook of financial time series (pp. 801–838). Berlin Heidelberg: Springer.

Polat, O. (2020). Time-varying propagations between oil market shocks and a stock market: Evidence from Turkey. Borsa Istanbul Review, 20(3), 236–243.

Qin, L., Sun, Q., Wang, Y., Wu, K. F., Chen, M., Shia, B. C., & Wu, S. Y. (2020). Prediction of number of cases of 2019 novel coronavirus (COVID-19) using social media search index. International Journal of Environmental Research and Public Health, 17(7), 2365.

Ruf, J., & Wang, W. (2019). Neural networks for option pricing and hedging: a literature review. arXiv preprint arXiv:1911.05620.

Selmi, R., et al. (2018). Is Bitcoin a hedge, a safe haven or a diversifier for oil price movements? A comparison with gold,". Energy Economics, 74, 787–801.

Uribe, J. M., et al. (2017). Uncertainty, systemic shocks and the global banking sector: Has the crisis modified their relationship? Journal of International Financial Markets Institutions and Money, 50, 52–68.

Vermeulen, R., Hoeberichts, M., Vasicek, B., Zigraiov´a, D., Sm´ıdkov´a, K., & de Haan, J. (2015). Financial stress and financial crises. Open Economies Review, 26, 383–406.

Xu, S., Du, Z., & Zhang, H. (2020). Can crude oil serve as a hedging asset for underlying securities?—Research on the heterogenous correlation between crude oil and stock index. Energies, 13(12), 3139.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Springer Nature or its licensor holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Mezghani, T., Abbes, M.B. Forecast the Role of GCC Financial Stress on Oil Market and GCC Financial Markets Using Convolutional Neural Networks. Asia-Pac Financ Markets 30, 505–530 (2023). https://doi.org/10.1007/s10690-022-09387-3

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10690-022-09387-3