Abstract

Pillar One and Pillar Two would introduce new rules for the taxation of multinational enterprises (MNEs). This paper assesses the impact of these proposals on MNEs’ investment costs. The analytical framework extends the forward-looking effective tax rates (ETR) model of Devereux and Griffith (International Tax and Public Finance 10: 107–126, 2003) to consider the ETRs for an investment performed by an entity belonging to an MNE group accounting for the possibility that MNEs use their organisational structure to shift profits to low tax jurisdictions. The model incorporates a stylised version of the tax provisions proposed under Pillar One and Pillar Two. The results, covering over 70 jurisdictions, account for differences in tax bases and rates, and are empirically calibrated to map the global activities of in-scope MNEs. The global GDP-weighted average change in the EATRs from Pillar One and Pillar Two is estimated to be 0.4 percentage points, representing a small impact compared to the weighted average EATR in the sample (24%) as well as the 6 percentage point reduction observed in the period 1999–2017 across OECD countries. Overall, the analysis suggests that both Pillars would reinforce each other in lifting the floor of the ETR distribution, thus reducing tax rate differentials across jurisdictions.

(Source: OECD Secretariat)

(Source: OECD Secretariat calculations)

Similar content being viewed by others

Notes

The analysis presented in this paper may not represent the latest discussions of the Inclusive Framework on BEPS on the two-pillar solution, but rather focuses on the proposals outlined at the time of publication of the Pillar One and Pillar Two Blueprint reports.

Extractives and Regulated Financial Services are excluded from the scope of Pillar One. Note also that the reallocation percentage has changed since the Blueprint from 20 to 25% as indicated in the statement.

The interest in considering both the IIR and UTPR is relevant when considering revenue estimates. Since this paper is focussed on the impact on investment costs, the distribution of revenues through these rules is not a first order consideration. Revenue estimates are available in (OECD, 2020a, 2020b, 2020c, 2020d, 2020e, 2020f, 2020g). Note that as will be discussed in the calibration section, jurisdictions below 15% are assumed to raise their tax rates to the minimum to absorb any revenue loss to Pillar Two. Implicitly, this mimics the effect of the UTPR with the difference being that under the UTPR carved-out profits should not be subject to top-up taxation.

The profit shifting share, \(\lambda\), is assumed to be the same for both types of profit; however, this assumption could be generalised in future work assigning different profit shifting propensities to routine and residual profit.

Note that the cost of capital will be affected by Pillar One if the routine return defined by the proposal is sufficiently low that it bites into the gross normal return.

In the empirical part discussed below, it is assumed that profits can potentially be shifted to any jurisdiction with a statutory rate below the statutory rate in the domestic jurisdiction.

In general, it would be possible to calibrate the model differently, e.g., reflecting investments in jurisdiction A by MNEs with a UPE in jurisdiction B, depending on the purpose of the analysis.

The statutory CIT rate for Saudi Arabia is considered to be 20%, which is the statutory CIT rate faced by non-Saudi investors. This corresponds to the rate a 100% foreign-owned company would face in Saudi Arabia. This rate can be higher in certain sectors of activity. While Saudi Arabia levies a zero-rate CIT on the share of profits owned by Saudi investors in sectors other than oil and gas, other tax liabilities arise for domestic investors, i.e., Zakat. Given the focus of the proposals on the taxation of foreign profits and given data limitations, the analysis abstracts from modelling of Zakat liabilities.

It would be possible to aggregate these assets based on their average weight in jurisdictions’ capital stock. This would be pursued as part of future work. The equal averaging used in this paper ensures alignment with the methodology in Corporate Tax Statistics (OECD, 2020a, 2020b, 2020c, 2020d, 2020e, 2020f, 2020g).

The economic depreciation rate of tangible assets is a weighted average rate of the economic depreciation of movable and immovable tangible assets using 2018 US capital stocks.

Share of shifted profits.

It might be the case that profits are shifted to locations with higher statutory tax rates where the effective rate that applies to these profits are lower than that in the parent jurisdiction. This might be the case when preferential tax regimes are in place, e.g. patent boxes. Given that these preferential regimes are not modelled in this framework, profit shifting behaviour is assumed, as in most of the empirical literature, to respond to statutory tax rates.

Note that the use of the micro-level estimate might be downwards biased due to the lack of universal coverage of profits in low-tax jurisdictions as well as the presence of non-linearities not accounted for in the estimation. The macro-level estimate is biased towards the higher end of the spectrum and might also be an overestimate due to the failure to control for firm-specific characteristics (Clausing 2016, 2018, 2020).

As is the case for other profit measures discussed in this note, routine profit can be interpreted equivalently as a profit measure or as a return on investment, given that the analysis considers a capital investment of one unit.

To see this, consider the case where the firm-specific profitability ratio, \({\varphi }_{i}\), equals 12.5% and the profitability threshold is defined as \(\overline{\varphi }=10\mathrm{\%}\). In this case, the share of routine returns in total profit is equal to 80% and the share of non-routine profits in total profits is equal to 20%.

The calibration of \(\widehat{r}\) matches jurisdiction level averages based on firm level data; although it captures variation in profitability across jurisdictions, a firm level calibration could be developed using more comprehensive microdata.

Note that the effect of nexus elements of the Pillar One proposal are not accounted for in this paper.

All in all, the share of residual profits varies across jurisdictions depending on the average share of residual to total profits of firms’ in scope. Once the share of residual profit is determined it is reallocated to market jurisdictions to be ultimately taxed at a weighted rate of 26%.

The agreed rate for the GloBE rules are 15% with jurisdictional blending.

Note that the effect of this assumption on the results is modest. Low-taxed profits not taxed under an IIR would nonetheless be subject to top-up tax under the UTPR. The difference between the country raising its tax rate or it being subject to top-up tax is the increase in investment costs coming from the increased taxation of carved-out profits. Given that carved-out profits are found to be modest, the increase in investment costs coming from this assumption is not significant. See Chapter 3 in OECD (2020a, 2020b, 2020c, 2020d, 2020e, 2020f, 2020g).

While other variables such as investment may be desirable, the only variables available to us were based on tangible assets failing to account for importance of intangible assets in the asset mix. Profits were also another variable considered but the presence of losses can potentially bias the weights. Furthermore, EATRs are calculated for a firm in profit and loss-making provisions are not accounted for. Considering positive profits could also be an option but would fail to consider that Pillar One does not affect firms in a loss-making position.

Among firms in-scope, the existence of an SBIE would mean that only a share of the profits for these firms would be subject to Pillar Two. This is accounted for in the ETR estimation.

The same data limitations outlined for Pillar One in footnote 31 apply also for Pillar Two.

To illustrate the limited impact of the design scope of Pillar One being modelled, the turnover of firms in-scope of Pillar One as defined above only account for 10% of the turnover of all MNEs in the analysis.

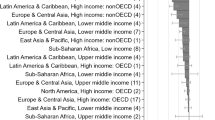

Note that the positive effect of the reform on ETRs on investments by in-scope firms in low and middle income jurisdictions turns negative when considering the global average; this effect is driven by the jurisdiction-specific weighting of in and out of scope firms, which occurs before GDP-weighting across jurisdictions.

To account for the assumption that Pillar Two only applies to MNEs with revenues above EUR 750 million, the impact of Pillar Two is weighted by the share of turnover from MNEs above the EUR 750 million threshold. While this subset of MNEs still includes over 90% of the turnover of all firms in the economy, only those with low-taxed profits will be affected by Pillar Two.

Pillar One (Amount A only) considers a 10% profitability threshold on Profit/Turnover, 20% reallocation percentage to market and a scope that is restricted to ADS and CFB activities. Pillar Two considers a 12.5% rate with jurisdiction blending and a 10% carve-out on depreciation expenses (approximated using the value of tangible assets), see Sect. 1.4 for additional modelling assumptions. The combined effect expressed here does not account for the interaction between the two pillars. However, this effect is deemed to be very small, given the modest impact of Pillar One. This is supported by findings from the revenue estimate that arrive at similar conclusions (see Chapter 2 in OECD (2020a, 2020b, 2020c, 2020d, 2020e, 2020f, 2020g)).

References

Barrios, S. et al. (2012), International taxation and multinational firm location decisions.

Becker, J., & Riedel, N. (2012). Cross-border tax effects on affiliate investment-evidence from European multinationals. European Economic Review, 56(3), 436–450. https://doi.org/10.1016/j.euroecorev.2011.11.004

Beer, S., Mooij, R., & Liu, L. (2020). International corporate tax avoidance: A review of the channels, magnitudes and blind spots. Journal of Economic Surveys, 34(3), 660–688. https://doi.org/10.1111/joes.12305

Cadestin, C., et al. (2018). Multinational enterprises and global value chains: The OECD analytical AMNE database. OECD Publishing, Paris.

Clausing, K. (2016). The effect of profit shifting on the corporate tax base in the United States and beyond. National Tax Journal, 69(4), 905–934. https://doi.org/10.17310/ntj.2016.4.09

Clausing, K. (2018). Profit Shifting before and after the tax cuts and jobs act. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.3274827

Clausing, K. (2020). How big is profit shifting? SSRN Electronic Journal. https://doi.org/10.2139/ssrn.3503091

Davies, R., Siedschlag I. and Studnicka Z. (2021), The impact of taxes on the extensive and intensive margins of FDI.

Devereux, M., & Griffith, R. (2003). Evaluating tax policy for location decisions. International Tax and Public Finance, 10(2), 107–126. https://doi.org/10.1023/A:1023364421914

Dowd, T., Landefeld, P., & Moore, A. (2017). Profit shifting of U.S. multinationals. Journal of Public Economics, 148, 1–13. https://doi.org/10.1016/J.JPUBECO.2017.02.005

Egger, P. et al. (2009b), Firm-specific forward-looking effective tax rates.

Egger, P. et al. (2009a), Bilateral effective tax rates and foreign direct investment.

Eurostat. (2008). NACE Rev. 2 - Statistical classification of economic activities in the European Community, Eurostat Methodologies and Working papers, Eurostat, Luxembourg. https://ec.europa.eu/eurostat/documents/3859598/5902521/KS-RA-07-015-EN.PDF

Feld, L. and Heckemeyer J. (2011), Fdi and taxation: A meta-study.

Griffith, R., Miller, H., & O’Connell, M. (2014). Ownership of intellectual property and corporate taxation. Journal of Public Economics, 112, 12–23. https://doi.org/10.1016/j.jpubeco.2014.01.009

Grubert, H. and Altshuler R. (2013b), fixing the system: An analysis of alternative proposals for the reform of international tax.

Grubert, H., & Altshuler, R. (2013a). Fixing the system: An analysis of alternative proposals for the reform of international tax. National Tax Journal, 66(3), 671–712.

Grubert, H., & Slemrod, J. (1994). The effect of taxes on investment and income shifting to Puerto Rico. National Bureau of Economic Research, Cambridge, MA,. https://doi.org/10.3386/w4869

Hanappi, T. (2018), “Corporate effective tax rates: Model description and results from 36 OECD and Non-OECD Countries”, OECD Taxation Working Papers, No. 38, OECD Publishing, Paris, https://doi.org/10.1787/a07f9958-en.

Heckemeyer, J., & Overesch, M. (2017). Multinationals’ profit response to tax differentials: Effect size and shifting channels. Canadian Journal of Economics/revue Canadienne D’économique, 50(4), 965–994. https://doi.org/10.1111/caje.12283

Huizinga, H., & Laeven, L. (2008). International profit shifting within multinationals: A multi-country perspective. Journal of Public Economics, 92(5–6), 1164–1182. https://doi.org/10.1016/J.JPUBECO.2007.11.002

Johansson, Å. et al. (2017), Tax planning by multinational firms: Firm-level evidence from a cross-country database, OECD, http://www.oecd.org/eco/workingpapers.

Jorgenson, D. and Hall R. (1967), “Tax policy and investment behavior”, American Economic Review, Vol. 57/3.

Maffini, G., Xing J. and Devereux M. (2019), The impact of investment incentives: Evidence from UK Corporation Tax Returns.

de Mooij, R. and Ederveen S. (2006), What a difference does it make? Understanding the empirical literature on taxation and international capital flows.

De Mooij, R. and Liu L. (2018), At a cost: The real effects of transfer pricing regulations.

OECD (2019), Programme of work to develop a consensus solution to the tax challenges arising from the digitalisation of the economy, OECD/G20 Inclusive framework on BEPS, OECD, Paris, https://www.oecd.org/tax/beps/programme-of-work-to-develop-a-consensus-solution-to-the-tax-challenges-arising-from-the-digitalisation-of-the-economy.pdf.

OECD (2020g), “Technical note on the methodology to assess the tax revenue effects of Pillar Two” No. CTPA/CFA/WP2/NOE2(2020g)1.

OECD (2020a), “Corporate effective tax rates: Explanatory Annex”, https://www.oecd.org/tax/tax-policy/explanatory-annex-corporate-effective-tax-rates.pdf (accessed on 23 September 2019).

OECD (2020b), Corporate Tax Statistics database, https://oe.cd/corporate-tax-stats (accessed on 22 October 2019).

OECD (2020c), Corporate Tax Statistics. Corporate Effective Tax Rates: Explanatory Annex., https://www.oecd.org/tax/tax-policy/explanatory-annex-corporate-effective-tax-rates.pdf.

OECD (2020d), Tax challenges arising from digitalisation–economic impact assessment: Inclusive framework on BEPS, OECD/G20 base erosion and profit shifting project, OECD Publishing, Paris, https://doi.org/10.1787/0e3cc2d4-en

OECD (2020e), Tax challenges arising from digitalisation – report on pillar one blueprint: Inclusive framework on BEPS, OECD/G20 Base Erosion and Profit Shifting Project, OECD Publishing, Paris, https://doi.org/10.1787/beba0634-en

OECD (2020f), Tax challenges arising from digitalisation – report on pillar two blueprint: Inclusive framework on BEPS, OECD/G20 Base Erosion and Profit Shifting Project, OECD Publishing, Paris, https://doi.org/10.1787/abb4c3d1-en

OECD (2021a), Statement on a two-pillar solution to address the tax challenges arising from the digitalisation of the economy, OECD, Paris, https://www.oecd.org/tax/beps/statement-on-a-two-pillar-solution-to-address-the-tax-challenges-arising-from-the-digitalisation-of-the-economy-october-2021a.pdf.

OECD. (2021b). Tax challenges arising from the digitalisation of the economy–global anti-base erosion model rules (Pillar Two): Inclusive framework on BEPS. OECD.

Petkova, K., Stasio A. and Zagler M. (2020), On the relevance of double tax treaties.

Steinmüller, E., Thunecke G. and Wamser G. (2019), Corporate income taxes around the world: a survey on forward-looking tax measures and two applications.

Suárez Serrato, J. (2018). Unintended consequences of eliminating tax havens. National Bureau of Economic Research. https://doi.org/10.3386/w24850

Tørsløv, T., Wier, L., & Zucman, G. (2018). The missing profits of nations. National Bureau of Economic Research, Cambridge, MA. https://doi.org/10.3386/w24701

Turban, S., Sorbe, S., Millot, V., & Johansson, Å. (2020). A set of matrices to map the location of profit and economic activity of multinational enterprises. OECD Taxation Working Papers 52, OECD Publishing.

van ‘t Riet, M. and Lejour, A. (2018), Optimal tax routing: Network analysis of FDI diversion.

ZEW (2015), “Effective Tax Levels Using the Devereux/Griffith Methodology: Final Report 2016”, Project for the EU Commission TAXUD/2013/CC/120 Final Report 2016, Mannheim, https://www.zew.de/en/publikationen/effective-tax-levels-using-the-devereuxgriffith-methodology-final-report-2016/ (accessed on 18 April 2019).

Zwick, E. and J. Mahon (2017), Tax Policy and Heterogeneous Investment Behavior.

Acknowledgements

The authors would like to thank David Bradbury, Alessandra Celani, Pierce O’Reilly and Kurt Van Dender (all from the OECD Centre for Tax Policy and Administration), Asa Johansson, Valentine Millot, Stéphane Sorbe and Sébastien Turban (all from the OECD Economics Department), Ruud de Mooij, Michael Devereux, Pardis Nabavi, Tom Neubig, Gaëtan Nicodème, Michael Stimmelmayr and other seminar participants at the annual congress of the IIPF 2020 for their comments on earlier versions of this work. The authors would also like to thank delegates from the OECD Working Party No. 2 on Tax Policy Analysis and Tax Statistics for their valuable contributions. The work benefited also from valuable discussions with the IMF and the European Commission. Finally, the authors would like to thank Violet Sochay and Karena Garnier (both from the OECD Centre for Tax Policy and Administration) for excellent editorial support.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary Information

Below is the link to the electronic supplementary material.

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Hanappi, T., González Cabral, A.C. The impact of the international tax reforms under Pillar One and Pillar Two on MNE’s investment costs. Int Tax Public Finance 29, 1495–1526 (2022). https://doi.org/10.1007/s10797-022-09750-0

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10797-022-09750-0