Abstract

Pre-war baseball attendance data afford a unique opportunity to assess how leisure spending fared not only through deflation but also after such shocks as the Spanish Flu of 1918 and the 1929 Wall Street Crash. Long-run analysis via a vector error correction model (VECM) reveals significant cointegration of baseball attendance with both prices and output. A long-run positive relationship with prices offers evidence of a negative impact of deflation on leisure spending, suggesting that deflation is indeed more to be feared than inflation. There are also apparent parallels between the post-pandemic boom in leisure spending in 1919 and the post-2020 experience.

Similar content being viewed by others

Introduction

Sports attendance, be it baseball or any other organized league, is inevitably affected by team performance as well as a myriad of other factors such as the appeal of its star players, the venue itself and the availability of other entertainment options. However, what is sometimes forgotten is that it is also a product of the overall economic environment and the discretionary income available to a team’s fans. Such effects may not be meaningful determinants of game-to-game attendance, but their impact emerges over the longer-term as business cycles run their course. In this regard, pre-war baseball attendance data afford a unique opportunity to assess how leisure spending is affected by not only macroeconomic fluctuations but also such shocks as the Spanish Flu of 1918 and the unprecedented aftermath of the 1929 Wall Street Crash. This is also an era when in-person attendance was still the only way to see the game, making the turnstile data studied in this paper the key source of team profitability.Footnote 1 Furthermore, there are parallels with 2020 insofar as baseball attendance plunged at the time of the Spanish Flu before experiencing a dramatic post-pandemic resurgence.

Another interesting feature of the pre-war era is that it was a time when inflation and deflation were, for the most part, equally likely. Deflation previously dominated much of the nineteenth century quite aside from the more famous 1930s episode in the midst of the Great Depression. Indeed, concerns with continued downward pressure on prices under the gold standard led to repeated attempts to remonetize silver (Burdekin & Siklos, 2013) culminating in William Jennings Bryan’s unsuccessful presidential bid in 1896. Baseball attendance data, available from 1890 onwards, span successive episodes of inflation and deflation that end with the ravages of the Great Depression in the 1930s. Empirical analysis reveals significant cointegration of baseball attendance with both prices and output over the 1890–1940 period, which includes the last full year prior to the entry of the United States (U.S.) into the Second World War in 1941 (and ensuing induction into the armed forces of many top baseball players). The positive relationship with prices in the long-run analysis implies the expected negative impact of deflation on leisure spending.

Trends in Pre-War Baseball Attendance

Professional baseball began with the formation of the National Association of Professional Base Ball Players in May 1871. The National League followed in 1876, expanding to 12 teams in 1892 after absorbing the rival American Association and Players’ League’ strongest four teams. Most National League teams then enjoyed a profitable run with Quirk and Fort (1992, p. 310) noting that every single team was operating in the black by 1895–1896. Whereas the National League contracted back to eight teams after the 1899 season, this was more than offset by the establishment of a new American League (formed out of the regional Western League). This eight-team American League operated as a major league from 1901 onwards. The first ever World Series between the champions of the National League and American League took place at the end of the 1903 season, ushering in a period of strong attendance gains leaguewide that averaged 4.5% per year between 1901 and 1913 (Quirk & Fort, 1992, p. 313).

The steady upward trend in attendance shown in Fig. 1 reached its peak in 1909. The ensuing dropoff in attendance may, in part, reflect competition from new leisure activities such as motion pictures. By 1910, weekly U.S. movie attendance equated to nearly one-third of the population, rising to around 50% by 1920. Butsch (2000, p. 150) documented the impact on traditional vaudeville and theater operations at this time with movies replacing theatrical performances in 1,400 former playhouses by 1911. The typical nickel price for movies was itself well below the cost of a baseball ticket, which Seymour and Mills (1971, p. 68) give as averaging 66 cents between 1909 and 1916. Baseball was also modernizing at this time, however, insofar as teams were gradually moving from the old wooden structures to more durable and larger facilities built from concrete and steel. Shibe Park in Philadelphia, which opened in 1909 and had a capacity of 33,000, was the first of this new generation of baseball stadiums.

Attendance vs. Number of Games Each Year, 1989–1940. Data are from Baseball-Reference.com (2022)

Even though stadium capacities remained relatively small by modern-day standards, Online Supplemental Appendix Table 1 shows that there were still plenty of empty seats even at the times of highest average attendance. The largest stadium in use before the First World War was the Polo Grounds with a capacity of 54,555, home to the New York Yankees through 1922. Average attendance per game at the Polo Grounds varied between a low of 919 and a high of 16,746. Its successor, Yankee Stadium, opened in 1923 as the inaugural triple-decked ballpark with a capacity of 56,937. Notwithstanding the Yankees’ success on the field, average attendance nonetheless failed to ever come close to this capacity limit and Online Supplemental Appendix Table 1 details how average attendance per game ranged between 8,826 and 15,385.

A new attendance challenge arose in the form of competition from the upstart Federal League during 1914–1915, closely followed by U.S. entry into the First World War in 1917. Although the season was not suspended like during the Second World War, players were leaving the league to join the war effort at the same time that ticket prices were being rounded up to account for the new 10% tax on amusements that was imposed in 1917. The ensuing Spanish Flu pandemic that hit in 1918 was accompanied by the sharpest drop in attendance (Fig. 1). Games continued but the virus affected the players as well as the fans with even the legendary Babe Ruth coming down with the virus in May 1918. Although Babe Ruth thankfully recovered to lead the Boston Red Sox to World Series victory later that year, as documented by Roberts and Smith (2020, p. 1), the decision to keep playing may have come at considerable cost:

“When the World Series resumed at Fenway Park on September 9, an increasing number of civilian cases appeared in Boston. Undoubtedly, crowded public events—three World Series games, parades, rallies, and a draft registration drive—fueled the plague. The contagion afflicted passengers riding ferries, trollies, and subway cars. And it infected the patrons of dance halls, theaters, saloons and Fenway Park … Belatedly, on September 11, 1918, the last day of the Series, William Woodward, the city’s health commissioner, issued a warning: people should avoid ‘crowded cars, elevators, or buildings’—that would have included Fenway Park, though he did not urge people to stay home entirely … Nonetheless, over the course of two days, a precipitous decline in attendance at Fenway Park reveals that something prevented the Red Sox faithful from showing up.”

Data displayed in BallparksofBaseball.com (2022) show that leaguewide attendance plunged from 4,762,705 in 1917 to 2,830,613 in 1918, before more than doubling post-pandemic to 6,532,439 in 1919. Although the 1918 drop was partly due to a shortened season (140 games instead of the prior 154), the remarkable rebound in baseball attendance in 1919 took place over an identical 140 game season.

As shown in Fig. 1, baseball attendance continued to trend upward after 1919 in spite of the reputational damage arising from the infamous “Black Sox” bribery scandal after the 1919 World Series. Indeed, in 1920, the New York Yankees became the first team to draw over one million fans in a single season. However, like so much else in the U.S. economy, baseball was not able to escape the damage from the massive downturn coming on the heels of the 1929 Wall Street Crash. Babicz and Zeiler (2017, p. 105) summarized the situation as follows: “Just as it had on the economy and the American psyche, the Great Depression had a damaging impact on baseball. Many fans could no longer afford to go to a baseball game.”

Attendance bottomed out in 1933 at levels below those of 1909 and the 1930 numbers were not exceeded until after the Second World War. The impact of the Great Depression on team finances is exemplified by the experience of Connie Mack’s Philadelphia Athletics, which won the World Series in 1929 and 1930 before losing the World Series final in seven games in 1931. Babicz and Zeiler (2017, p. 104) noted that the Athletics were especially vulnerable to the worsening economic conditions because, unlike owners of other top teams, Mack had no outside sources of income.Footnote 2 By 1933, the economic collapse was forcing the team to reduce payroll and the loss of their top players saw the Athletics fall from the top of the baseball world to last place by 1935. They remained in the cellar through 1943 and did not become contenders again until the 1970s (after their move to Oakland, California).

Deflation, the Spanish Flu, and Leisure Spending

Even though the post-Civil War U.S deflation was relatively mild overall, it did significant damage to the agricultural sector, not only because farmers tend to be net debtors, but also due to agricultural prices falling more than in proportion with the aggregate price level. Friedman (1992, p. 70) noted that, although the U.S. aggregate price level declined by approximately 1.7% per year from 1875–1896, the wholesale prices of agricultural commodities were estimated to have fallen by as much as 3% per year. This nineteenth century deflation (like that experienced in the United Kingdom) occurred when growing scarcity of gold put downward pressure on the money supply and prices alike under the classical gold standard. The deflationary pressures did not ease until the invention of the cyanide process and new gold discoveries in South Africa provided for renewed expansion in the world’s gold supply (Friedman, 1992).

Although output effects of the 1918–1919 Spanish Flu appeared to be only short-lived, the aforementioned plunge in baseball attendance suggests there may have been a much more major effect on leisure spending.Footnote 3 The dramatic resurgence of baseball attendance that followed in 1919 may itself reflect the same sort of pent-up demand that received so much attention in 2021–2022. This would certainly be in keeping with the description by Wicker (1966, p. 236) of how rising bank loans in the aftermath of the pandemic financed a “speculative orgy of 1919.”

The 1919 boom proved short-lived as Federal Reserve tightening was accompanied by deflation in 1920 and shrinking commercial loans. In describing the contraction of 1920–1921, Friedman and Schwartz (1963, p. 231) stated that the Federal Reserve’s discount rate hike in January 1920 “was not only too late but also probably too much … The contraction … became extremely severe in its later stages, when it was characterized by an unprecedented collapse in prices.” The subsequent recovery from the bottom in 1921 to the peak of the boom in 1929 featured inflows of gold that fueled inflation via “redundant bank credit which had to be forced into use in the only field that would absorb it” (Noyes, 1930, p. 187).

The year 1929 marked a clear turning point, not only for the stock market, but also for other trends in money, credit and economic activity. The empirical work herein makes allowance for a shift at this time as well as with the 1918 Spanish Flu. The ensuing deflation during the Great Depression of the 1930s, like that of 1920–1921, was marked by an abrupt shift to monetary contraction, including the astonishing one-third drop in the U.S. money supply between 1930 and 1933 emphasized by Friedman and Schwartz (1963).

Pre-War Baseball Attendance vs. Macroeconomic Conditions

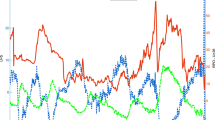

The empirical analysis relates attendance per game to a set of four macroeconomic variables: real gross domestic product (GDP) per capita (obtained by dividing real GDP by population), a producer price index (1982 = 100), the unemployment rate, and the Dow Jones stock market index. Each of these series was obtained from Global Financial Data (2022) and represents essentially the only relevant series available over the full 1890–1940 sample. The attendance data are from Baseball-Reference.com (2022). Figure 2 shows how the resurgence in baseball attendance after the 1918 Spanish Flu continued until the collapse in economic activity after 1929 followed by a recovery in both attendance and real GDP from the bottom reached in 1933. Although the decline in the producer price index (PPI) began earlier (Fig. 3), it too bottomed in the early 1930s before bouncing back. Figures 2 and 3 show the dramatic accompanying moves in the Dow Jones and the unemployment rate, with the stock market abruptly giving back a decade’s worth of gains at the beginning of the 1930s while the unemployment rate abruptly jumped to around 25% before gradually recovering to just below 15% on the eve of the Second World War.

The output and unemployment effects allow for effects of real economic conditions. Periods of declining growth and rising unemployment would be expected to reduce spending on baseball tickets as well as in the economy more broadly. The skyrocketing unemployment following the onset of the Great Depression, for example, was accompanied not just by a near 20% drop in real GDP but also by a 40% drop in total baseball attendance between 1930 and 1933. This plummeting attendance, in turn, quickly caused team operating margins to swing from profit to loss, with a -23.9% loss being seen at the 1933 lows (Burk, 2001, p. 41).

The PPI is preferred to the consumer price index (CPI) owing to the variations in CPI coverage over the 1890–1940 sample period, with this latter index being limited to retroactive coverage of a set of food prices over the 1890s, for example. Even during the 1920s, the Federal Reserve itself focused primarily on commodity prices, not consumer prices, in gauging price stability (Noyes, 1930, p. 182). One way in which declining aggregate prices would be expected to hurt baseball attendance is via induced reductions in worker wages. This certainly manifested itself during the Great Depression, as evidenced by a 33.6% reduction in manufacturing wages between 1929 and 1932 that carried with it a 14.9% reduction in real weekly earnings (Wolman, 1933).

Deflation also makes baseball games relatively more expensive unless ticket prices are being adjusted to keep pace with the PPI. Analysis for the modern era suggests that baseball tickets are typically held back at below market-clearing levels and priced in the inelastic portion of the demand curve (Burdekin, 2012).Footnote 4 Although the data are insufficient to establish whether or not this was also true during the pre-war era, there are indications that ticket priced remained relatively stable. Bauer (2020) notes that there was a standard price during the 1880s for the National League of 50 cents for the bleachers and 75 cents for the grandstand. Teams did not even have the authority to set ticket prices individually at this time and there was a uniform minimum price (Bauer, 2020, p. 186). Furthermore, ticket prices remain essentially uniform across teams through the First World War. Seymour and Mills (1971, p. 51) referenced a general admission charge for the grandstand still standing at 75 cents when Pittsburgh’s Forbes Field opened in 1909, with average admission prices around 66 cents persisting through 1916 (Seymour & Mills, 1971, pp. 68). The final elimination in 1920 of the old 25-cent tickets (that had carried over from the days of the old American Association) boosted averages slightly, as had the introduction of some higher-priced seats that could reach $1.50 (Seymour & Mills, 1971, pp. 68–69). Haupert (2007) listed average ticket prices as standing at a single dollar in 1920.

The implied modest increase through 1920 occurred in the face of some significant inflation after 1912 that had led to a doubling of the PPI index between 1912 and 1919 (representing a PPI level more than 150% that seen in 1890 at the beginning of the sample period). Meanwhile, teams appear to have reacted to the financial catastrophe of the early 1930s, primarily by imposing cuts in player salaries and minor league systems, with Burk (2001, p. 41) also pointing to the compounding effect of the federal government’s 10% tax on gate revenue. This entertainment tax works against price cuts insofar as it requires higher ticket prices to produce the same after-tax revenue.

Finally, gains in the Dow Jones index could exert a positive effect on attendance insofar as fan behavior incorporates the forward-looking properties typically attributed to the stock market. That is, insofar as stock market gains reflect greater optimism about future economic conditions, this same favorable sentiment may carry over to the general population and induce some positive effects on willingness to spend and consume.

The cointegration techniques in the next section shed light on the long-run relationship between attendance per game and all four of these macroeconomic variables. There is evidence of significant positive relationships between attendance and both prices and output, with the positive relationship with the PPI being very much consistent with negative effects of deflation.

Long-Run Error-Correction Analysis

Longer-run co-movement between attendance and macroeconomic variables was assessed via a vector error correction model (VECM). A VECM considers possible cointegrating relationships among the variables and allows one to assess adjustment to deviations from long-run equilibrium. The data-generating process of the integrated variables is represented by a Gaussian vector autoregressive (VAR) model of finite order q:

where Xt is a (k × 1) vector of variables in the VAR system, Ai is a matrix of the estimated coefficients, and ut is the stochastic error term. Subtracting Xt-1 from both sides yields the relationship between the variables in VECM form:

where \(\Pi =\sum_{j=1}^{q}{\mathrm{A}}_{j}-{I}_{k}\), which controls the cointegration characters, and \({\Gamma }_{i}=-\sum_{j=1}^{q}{\mathrm{A}}_{j}\).

Engle and Granger (1987) showed that if the variables in Xt are integrated with order one, I (1) and the matrix \(\Pi\) in Eq. (2) has a rank r that is between 0 and full rank (\(0\le r<k\)), there exist some linear combinations of Xt that are stationary. Thus, Xt is cointegrated, and the variables in Xt can be viewed as processing an equilibrium relationship which causes them to move together over time. Furthermore, the matrix \(\Pi\) contains the long-run relationships among the variables, and its rank r is the number of linearly independent cointegrating vectors. Johansen (1995) defined two matrices \(\mathrm{\alpha }\) and β, both of dimension (k × r) and of rank r, yielding:

where β is itself the matrix of r cointegrating parameters, which summarizes the linear long-run relationship; and \(\mathrm{\alpha }\) is the matrix of weights with which each cointegrating vector enters the k equations of the VAR. Essentially, \(\mathrm{\alpha }\) is the adjustment coefficient in each of the r vectors, reflecting the direction and speed of long-run equilibrium adjustments. The rank test for cointegration involves estimation of the rank, r, which gives a sequence of trace and eigenvalue statistics obtained from the recursive estimation of the model.

In order to incorporate dummy variables that represent events and/or structural breaks, Eq. (2) can be re-written as follows (with Dt representing the dummy variable effect):

The variable of interest is attendance per game, which is defined as total attendance divided by total number of games in a year. Macroeconomic variables included in the VECM are the Dow Jones industrial average, per capita GDP, the unemployment rate, and the PPI. Augmented Dickey Fuller tests show all of these variables in their original form to be integrated with order one, i.e. I (1) (Table 2). With the variables being cointegrated under matrix β and adjustment matrix α, the corresponding VECM is:

where the first part is the constant vector, the second part represents the error-correction term, and the third part is the short-run dynamic process. This VECM approach explicitly incorporates short-run deviations from the long-run cointegrating relationship and allows one to assess how attendance responds to shocks to the different macroeconomic variables.

Both the Trace test and the maximum-eigenvalue test suggest that there exists at least one cointegrating equation between attendance and the macro variables (Table 3). Table 4 presents the estimated coefficients of the long-run cointegrating equations (β values from Eq. 5). The coefficient on attendance was normalized to one in each equation. Dummies for 1918 and 1929 were added to all specifications and each was found to be highly significant.

However, there is still the possibility of additional possible structural breaks in the PPI series. The Zivot-Andrews (1992) procedure allows a potential breakpoint to be estimated rather than preset. This testing procedure identified a break in 1920 (Fig. 4) and the model was accordingly re-estimated with an added exogenous dummy variable set equal to one from 1920 through the end of the sample. The estimated coefficients are shown in column (ii) of Table 4. The better-performing model that produces the smaller log likelihood, AIC and SBIC values is the one without the 1920 structural break dummy, however. Furthermore, the coefficient on the PPI is larger in column (i) than that of column (ii), suggesting that the dynamics of inflation/deflation are already incorporated in the PPI series. Although the significance of the variables did not change, more emphasis is, therefore, placed on the coefficient values in column (i). The associated long-run relationship between attendance per game and the macroeconomic variables is:

Zivot-Andrews Break Point Test Results for the PPI Series. This figure depicts test statistics from Zivot-Andrews tests on the PPI series. The null hypothesis is that PPI has a unit root process that excludes exogenous structural change. Critical values are 99%: -4.93; 95%: -4.42; and 90%: -4.11. The test results suggest that there is a break in the data trend in 1920

where both GDP and the PPI effects are significant at better than the 99% confidence level and the Dow Jones and unemployment effects are insignificant (despite having the expected positive and negative signs, respectively). The estimated coefficient on GDP suggests that following a one standard deviation positive shock to per capita GDP (Table 1), attendance per game must increase by 835.778 to bring the system of variables back to equilibrium. Following a one standard deviation increase in the PPI, attendance per game is expected to increase by 905.888 in the new equilibrium. In turn, this suggests that concerns about consumer spending should be focused more on risks of deflation rather than inflation.

Conclusions

This paper’s 1890–1940 dataset affords a unique opportunity to assess how leisure spending fared, not only through deflation, but also from such shocks as the Spanish Flu of 1918 and the 1929 Wall Street Crash. The negative impact seen in the 1918 pandemic year, and the ensuing rapid rebound, itself yields some apparent parallels with the post-2020 experience. More generally, the macroeconomic variables included in this study reveal significant long-run cointegration of baseball attendance with both prices and output. The magnitude of these effect is non-trivial. In the face of a one standard deviation positive shock to both output and prices at the same time, attendance per game is expected to increase by almost one standard deviation, or, equivalently, 1,740 more people coming to see the game.

The indicated long-run positive relationship with prices offers evidence of a negative impact of deflation on leisure spending, suggesting concerns with consumer spending should focus on risks of deflation rather than inflation. This implies that inflationary concerns emerging in the aftermath of the coronavirus pandemic need not be feared anything like as much as the deflationary pressures associated with the initial pandemic shock in 2020. At the same time, the ability of even top Major League Baseball teams to keep the turnstiles moving remains a product of the overall economic environment. Not even Babe Ruth could save the New York Yankees from suffering under the collapse of economic activity after the 1929 Wall Street crash.

Notes

Technically, the very first televised baseball game on August 26, 1939 falls just before the end of the 1890–1940 sample period. There was no regular network broadcasting until 1946, however, and the 1939 showing was really only of symbolic importance.

The owner of the New York Yankees, Jacob Ruppert had a major brewery and the Chicago Cubs owner was Philip K. Wrigley of chewing gum fame.

Burdekin (2021) also pointed to significant international stock market effects.

Although this implies that teams are setting ticket prices too low and could boost revenue by raising the price of entry, it is possible that teams are simply using admission as a “loss leader” and making their profits on concession sales (Krautmann & Berri, 2007). Meanwhile, Chang et al. (2016) pointed to teams seeking to maximize home field advantage by playing to as full a house as possible.

References

Babicz, M. C., & Zeiler, T. W. (2017). National pastime: U.S. history through baseball. Lanham, MD: Rowman & Littlefield.

BallparksofBaseball.com (2022). 1910–1919 Ballpark Attendance. Retrieved November 8, 2022, from https://www.ballparksofbaseball.com/1910-1919-mlb-attendance/

Bauer, R. (2020). Outside the lines of gilded age baseball: The finances of 1880s baseball. Rob Bauer Books.

Burdekin, R. C. K. (2012). Demand for attendance: Price measurement. In: S. Shmanske & L.H. Kahane (Eds.), The Oxford handbook of sports economics: Volume 2; Economics through sports, New York, NY: Oxford University Press.

Burdekin, R. C. K. (2021). Death and the stock market: International evidence from the Spanish Flu. Applied Economics Letters, 28(17), 1512–1520.

Burdekin, R. C. K., & Siklos, P. L. (2013). Gold resumption and the deflation of the 1870s. In: R.E. Parker & R. Whaples (Eds.), Routledge Handbook of Major Events in Economic History, New York, NY: Routledge.

Burk, R. F. (2001). Much more than a game: Players, owners, & American baseball since 1921. Chapel Hill, NC: University of North Carolina Press.

Butsch, R. (2000). The making of American audiences: From stage to television, 1750–1990. New York, NY: Cambridge University Press.

Chang, Y.-M., Potter, J. M., & Sanders, S. (2016). Inelastic sports ticket pricing: Marginal win revenue, and firm pricing strategy. Managerial Finance, 42(9), 922–927.

Engle, R. F., & Granger, C. W. J. (1987). Co-integration and error correction: Representation, estimation, and testing. Econometrica, 55(2), 251–276.

Friedman, M. (1992). Money mischief: Episodes in monetary history. New York, NY: Harcourt Brace Jovanovich.

Friedman, M., & Schwartz, A. J. (1963). A monetary history of the United States, 1867–1960. Princeton, NJ: Princeton University Press.

Global Financial Data. (2022). Retrieved November 8, 2022, from https://globalfinancialdata.com/

Haupert, M. J. (2007). The economic history of major league baseball. In: R. Whaples (Ed.), EH.Net Encyclopedia. Retrieved November 8, 2022, from https://eh.net/encyclopedia/the-economic-history-of-major-league-baseball/

Johansen, S. (1995). Likelihood-based inference in cointegrated vector autoregressive models. New York, NY: Oxford University Press.

Krautmann, A. C., & Berri, D. J. (2007). Can we find it at the concessions? Understanding price elasticity in professional sports. Journal of Sports Economics, 8(2), 183–191.

Noyes, C. R. (1930). The gold inflation in the United States 1921–1929. American Economic Review, 20(2), 181–198.

Quirk, J., & Fort, R. D. (1992). Pay Dirt: The Business of Professional Team Sports. Princeton, NJ: Princeton University Press.

Roberts, R., & Smith, J. (2020). When Babe Ruth and the great influenza gripped Boston. Smithsomian Magazine. Retrieved November 8, 2022, from https://www.smithsonianmag.com/history/when-babe-ruth-and-great-influenza-gripped-boston-180974776/

Seymour, H., & Mills, D. S. (1971). Baseball: The golden age. New York, NY: Oxford University Press.

Wicker, E. R. (1966). A reconsideration of Federal Reserve policy during the 1920–1921 depression. Journal of Economic History, 26(2), 223–238.

Wolman, L. (1933). Wages during the depression. National Bureau of Economic Research: Bulletin-Number 46. Retrieved November 8, 2022, from https://www.nber.org/system/files/chapters/c2256/c2256.pdf

Zivot, E., & Andrews, D. W. K. (1992). Further evidence on the great crash, the oil price shock, and the unit-root hypothesis. Journal of Business and Economic Statistics, 10(3), 251–270.

Acknowledgements

The authors thank Dick Sweeney and an anonymous referee for helpful comments.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary Information

Below is the link to the electronic supplementary material.

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Tao, R., Burdekin, R.C.K. & Berri, D. Effects of Deflation and Macroeconomic Shocks on Leisure Spending in the Pre-War Era: Evidence from Major League Baseball, 1890–1940. Atl Econ J 50, 119–132 (2022). https://doi.org/10.1007/s11293-022-09756-3

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11293-022-09756-3