Abstract

This study aims to validate a new model that explains the switching intentions of banking customers toward crowdlending based on the perceived investment value, the quality of the crowdlending platform, and two comparative technology adoption factors. The empirical investigation was conducted by conducting an online survey of a sample of 201 potential and actual users of two crowdlending platforms in the Kingdom of Saudi Arabia. The findings of the study highlighted that the switching intentions of potential crowdlenders was affected by perceived emotional and economic investment values, which may in turn be influenced by the relative advantage of this kind of investment and the platform’s information quality. The perceived relative complexity, however, had no significant impact on perceived investment value. This study extends our body of knowledge about the adoption of FinTech and specifically crowdlending by considering that the perceived investment value may include an emotional dimension, something that has been ignored in prior research. Finally, this investigation highlights the need for crowdlending platforms to employ communication strategies based on the notion of promoting the hedonic and economic values of this kind of investment and its relative advantages over traditional forms of investment, namely banking deposits.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

During recent years, the global economy has oscillated due to disruptions such as the global financial crisis in 2008. Financial technology (FinTech) has been one direction of development, since it supports the financial sector by combining financial services and technology to offer new services, such as crowdlending (Schueffel 2016; Candra et al. 2020; Yan et al. 2022).

Bollaert et al. (2021) mentioned that the principal conductor behind the first wave of FinTech expansion was its technological progress, which exposed the weaknesses of traditional financial intermediaries. Indeed, banks in Europe have decreased their financing for small to medium-sized enterprises (SMEs) and entrepreneurs, while emerging platforms like crowdlending have increased their financing capacity, thus providing new sources of capital for the markets (ECB 2017).

SMEs and entrepreneurs frequently need to raise financing to develop partnerships and enhance processes (Huang et al. 2018; Martínez-Cliement et al. 2021), and collective financing via FinTech has become an interesting way for them to raise funds in recent years (Martínez-Cliement et al. 2019; Yan et al. 2021).

FinTech services can target large populations who usually deposit their excess incomes in bank accounts. Nicoletti (2017) indicated that following the global financial crisis of 2008, many startups entered the FinTech market to provide new financial services to consumers, such as crowdlending, which permits investors and individuals to supply the money for companies to borrow based on their solvency. Maier (2016) observes that Crowdlending is a new financing alternative which uses technology to provide value to customers by allowing them to profit from the possibilities of direct financing of credits. It aims to directly link up prospective borrowers and investors via a crowdlending platform. Users have the possibility to contribute by investing into numerous credit requests. Maier (2016) highlights the difference between crowdlending and the remaining forms of crowdfunding. In this specific case the consumers seek to predominantly invest in in particular loan requests, via online platforms. In contrary, crowdfunding forms like “crowd equity” or “reward based crowdfunding” are share based investments.

This current research proposes, and subsequently verifies, an empirical model that explains switching intentions toward crowdlending based on perceived investment value, the quality of the information on a platform’s website, and two comparative technology adoption factors, namely relative advantage and relative complexity.

Thus, the purpose of this research is to validate this original model for explaining the switching intentions toward crowdlending in the emerging economy of Saudi Arabia. Moreover, this FinTech innovation may find a role in the Saudi Arabian market as a means to help achieve one of this country’s “Vision 2030” expectations, namely raising SMEs’ contribution to the country’s Gross Domestic Product to 35% (Jureidni 2017).

This investigation into crowdlending within the Saudi context is interesting for two reasons: First, it is important to know the popularity of these platforms in Saudi Arabia and learn about the expectations of Saudis when investing through crowdlending platforms. Second, the verification of the proposed original model reveals some predictors of the intention to invest through crowdlending, namely perceived investment value, relative advantage, relative complexity, and website information quality.

Many past studies have examined the role played by the new platforms in financing the economy and providing new sources of capital to the market. Bouncken and Kraus (2021) posited that these new platforms are elements of the digital economy, so it is critical for capital providers and entrepreneurs to create a successful brand image and reputation that stimulates trust for all participants in the sector. The crowdlending platforms have a relative advantage over the traditional banks and financial institutions, such as their efficiency in managing financial accounts. Moreover, crowdlending platforms leverage new technologies to make them safe, fast, and effective when handling an investment. In addition, crowdlending platforms provide opportunities to SMEs by enabling them to rapidly secure funding, while investors gain the opportunity to invest small amounts.

Other studies have debated the advantages of crowdlending compared to traditional financing sources. For example, it is considered an effective way to invest and secure funding (Maier 2016; Borrero-Domínguez et al. 2020), and it offers simple conditions and rapid service with competitive interest rates (Sjamsudin 2019). It is also more effective than traditional financing sources (Borrero-Domínguez et al. 2020) despite the limited availability of information compared to traditional institutions like banks (Xie et al. 2016; Giudici 2018; Gozali et al. 2020). Moreno-Moreno et al. (2019) noted that despite the important role of crowdlending as an alternative for meeting SMEs’ funding needs, it has not been studied enough.

Huang et al. (2018) indicated that crowdfunding in China is a modern, active vehicle for microbusinesses, SMEs, and entrepreneurs. Bollaert et al. (2021), meanwhile, studied the impacts of digitalization on access to finance and discussed how FinTech influences accessibility to financial funds and the regulatory challenges involved in this process.

Although a few research models explain crowdlending behaviors from the perspective of small investors, such as banking customers, the number of studies in this field remains relatively low, with them not covering enough plausible predictors and outcomes. It is been noted that this topic requires further effort to gather more knowledge about it (Borrero-Domínguez et al. 2020), especially for crowdlending behavior, which has not been sufficiently studied (Moreno-Moreno et al. 2019; Martínez-Cliement et al. 2021).

We make three contributions to the collective financing literature in this study: First, crowdlending has been recently introduced in the KSA, and to the best of our knowledge, this is the first study to investigate crowdlending in this emerging economy. Second, we developed an original model that explains behavioral intentions toward a FinTech service, specifically switching intentions toward crowdlending. Based on a literature review, the chosen exogenous variables comprised the perceived investment value, relative advantage, relative complexity and the quality of information on the crowdlending website. The proposed model is original because perceived investment value from the customer’s perspective has never been used as a variable to explain switching intentions toward crowdlending, nor has it been explained by other factors in this context. Moreover, we added a comparative perspective by including three variables with a comparative nature, namely switching intentions as a dependent variable and two exogenous variables in the form of the relative complexity and relative advantage of crowdlending. Ultimately, this study aspires to contribute knowledge by offering valuable information to researchers, entrepreneurs, and regulators in the FinTech field.

The main novelty of this study lies in integrating the concept of investment value for potential micro-investors who are currently banking customers by gaining the opportunity to invest their savings in micro-investments rather than deposit accounts. The adaptation of our chosen theory also considers the information quality of the FinTech platform. This is important because the process of adopting an innovation is an ongoing mental process in which potential customers gather information to understand the uncertainties and risks associated with an innovation (Rogers 1983).

This paper is organized as follows: First, we present a literature review and discuss definitions of collective financing before developing the research hypotheses. The following section then describes the data set and research methods, which is then followed by a section for the results and analysis. Section“Implications, Limitations, and Future Directions” then conceptualizes the study’s findings through discussion before we conclude this paper by discussing the study’s implications and limitations, as well as directions for future research.

Literature review

Theoretical approach and rationale model: the diffusion of innovation theory

The process of adopting an innovation is an ongoing mental process in which potential customers gather information about that innovation in order to manage uncertainties and risks. The diffusion of innovation theory (TDOI) is a well-established framework that can act as a foundation for models attempting to explain the adoption of innovation and behaviors when switching from traditional services to innovative alternatives, because its main variable, relative advantage, has a comparative nature. The TDOI highlights a diffusion process in which innovations are relayed across customers over time, starting with the most innovative customers and proceeding to other customers who may adopt it later. This theory initially focused on explaining individual-level characteristics and profiles, because the adoption of new products or ideas cannot possibly happen simultaneously across a social system. Instead, the typically observed reality is that diffusion is a gradual process that starts with a few consumers (“Innovators”) who have characteristics that support the very early adoption of the innovation. The TDOI postulates that the second group (the “Early Adopters,” who are mainly composed of opinion leaders) can be influential in demonstrating that the innovation works. This is critical in developing the condition for the third group (the “Early Majority”) to decide to use the innovation. Next, the fourth group (the “Late Majority”) tend to have very skeptical attitudes toward change and only adopt the new product when it has already satisfied most people. The final group (the “Laggards”) comprises people who are too skeptical and conservative to ever adopt any innovation (Abikari et al. 2022). Each of these profiles requires a different strategy for accelerating their adoption of a new innovation (Rogers 1983).

The TDOI has also highlights the influence of some attributes of innovation, namely relative advantage, complexity, compatibility, trialability, and observability. These are important components of consumers’ evaluations and perceptions, which in turn can determine the adoption rate for a new product (Rogers et al. 2005). For example, when a new product or technology has a low complexity, a noticeable relative advantage, clear observability, compatibility, and easy trialability, the TDOI predicts that the innovation will be adopted relatively quickly (Rogers 1983). To explain these terms a little, the relative advantage is the extent to which a new technology or product is seen to outperform the traditional equivalents. Compatibility is the extent to which a new product or service is perceived as fitting with one’s needs, knowledge, and value, while complexity reflects the difficulty in using or learning about the new product or service. Trialability refers to being able to experience a new product or service, such as through a time-limited trial, before purchase. The final attribute proposed by the TDOI is observability, which reflects the ease by which others can perceive the outcomes of an innovation (Rogers 1983).

Consumers perceive all these innovation characteristics, and these perceptions determine consumers’ overall acceptance of a new product/service and the pace of adoption. We propose adapting the TDOI’s idea to a financial context, namely crowdlending, as follows:

-

First, following Rogers’ theory, a new model of FinTech adoption was developed and applied to the context of crowdlending. We focused on the most popular variables of the TDOI with a comparative nature, namely relative advantage and complexity. Indeed, we assume that a potential micro-investor will already have traditional opportunities for investment, so the decision to switch to a new alternative will likely be based on an internal comparison of investment options. Moreover, even in an absolute evaluation, complexity and advantage are shared among all models of technology acceptance, although they may take names like ease of use or effort expectancy.

-

Second, rather than simply testing the direct impact of the innovation’s attributes on the adoption of it, we test their impact on the perceived investment value, which in turn will directly influence switching intentions.

-

Third, we add an independent variable, namely information quality, to capture the importance of information diffused through a crowdlending platform’s website as a factor that influences the perceived value and in turn switching intentions.

The concept of perceived investment value

The concept of perceived value has attracted attention in recent years because it appears to be a rich, broad, and complete measure of a customer’s subjective overall assessment.

Jiang et al. (2022) indicated that customers’ perceived value reflects their preferences and assessments with regards to the characteristics of a product or service, the performance of these characteristics, and the outcomes after adopting the product or service. This construct is conceived in marketing theories as a set of subjective consumer perceptions about the consumption experience for a product or a service (Zeithaml 1988; Holbrook 1999). Holbrook (1999) assumed that the perceived consumption value is based on subjective preferences that are relativistic, comparative, and situational (Holbrook 1999). Zeithaml (1988), meanwhile, focused on duality in the form of comparing, or ratio-linking, the benefits received from a product with the sacrifice that the consumer needs to make to acquire the product. She posited that the perceived value is a positive influence when the benefits outweigh the required sacrifice. This idea was further developed by integrating numerous interrelated dimensions in the retailing context (Babin et al. 1994). In the financial field, Puustinen et al. (2013) took this multidimensional perspective and considered the consumers’ perspective of investment value, concluding that it includes hedonic and utilitarian dimensions. They justified this approach through the fact that for individuals, “investing offers emotional value, as some consumers enjoy evaluating alternative investments” (Puustinen et al. 2013, p. 43). Thus, an investment’s outcomes may include intrinsic emotional rewards based on symbolic meanings for the investing consumer. Our study suggests that the work of Puustinen et al. (2013) could be a great foundation for broadening the rational economic perspective of behavioral finance, especially in new investment contexts that are innovative and non-institutional. Indeed, investing through crowdlending platforms can be a source of intrinsic and extrinsic value. The latter is focused on the economic profitability of form of investment, while the former highlights the ratio between gains and sacrifices (Zeithaml 1988). The intrinsic value of crowdlending is of an emotional nature, something that has been ignored in the financial marketing literature. It includes positive feelings, emotions, and feelings of pleasure that are valued by the crowdlending investor. It can therefore be viewed as an affective response to the experience of lending through this new channel or an expectation of realizing returns that are superior to those of the more familiar investment opportunities.

Antecedents and consequences of perceived crowdlending investment value (PCIV)

Relative advantage and complexity

To shed some light on the antecedents of perceived investment value and its association with switching intentions, the proposed conceptual model adapts the common concepts of Rogers’s TDOI that are used in most popular approaches that deal with the adoption or acceptance of new technologies, namely relative advantage and relative complexity.

This decision can be justified for two reasons: Firstly, these two variables are commonly used under various names by the most popular innovation/technology models, namely Davis’s (1989) technology acceptance model (TAM), the unified theory of acceptance and use of technology of Venkatech et al. (2012) and Rogers’s (1983) diffusion of innovation theory. More specifically, the first uses the concepts of ease of use and utility; the second uses, among other things, the concepts of effort expectancy and performance expectancy; and the third uses the terms “relative advantage” and “complexity.” Secondly, the choice of these variables among the aforementioned ones can be explained through the significance of their comparative nature, which fits well with the comparative context of our research. Indeed, the dependent variable is switching intentions toward a FinTech innovation, because potential customers have the option of using traditional vehicles to invest, or crowdlending.

Numerous studies have verified that relative advantage is a significant predictor for the adoption of, or resistance to, a new product, service, or experience (Abbas et al. 2017; Reddick et al. 2019; Oweis and Al Reddick 2019; Garrouch and Timoulali 2020; Mombeuil and Uhde 2021; Kaur and Arora 2023). Yang and Zhang (2022) examined how FinTech’s payment facilitation and adoption have affected household consumption in China, with them finding a decrease in consumption inequality and an increase of household consumption after adopting FinTech. The authors also noted that the traditionally time-consuming agencies were being replaced by the new platforms, which are characterized by their simplicity and appropriateness.

Theoretically speaking, the relative advantage is an antecedent to perceived value, as the latter is by definition a balance between the benefits and sacrifices (Zeithaml 1988). This link has recently been empirically verified in an online/mobile retailing context (Garrouch and Timoulali 2020) and the mobile payment field (Wang 2022). Buchak et al. (2018) indicated that the digitalization of finance opens up more options that could facilitate entrepreneurs’ access to finance and provide new alternatives for investors. We propose the assumption that relative advantage influences the perceived investment value of crowdlending. This initial hypothesis is further delineated into two sub-hypotheses based on the two essential dimensions of perceived value, namely intrinsic and extrinsic value (Holbrook 1999; Babin et al. 1994; Puustinen et al. 2013). The former is a perception of value from an economic viewpoint, while the latter relates to valuing the consumption experience in itself due to the emotions that can be felt during and after the process. This has also been referred to as hedonic value (Babin et al. 1994) and emotional value (Puustinen et al. 2013).

At a macro level, it has been noted that firms put forward FinTech products that offer great value in a context that is characterized by less rigorous banking rules and uncompetitive banking industries (Yang and Zhang 2022). In addition, it can improve the sustainability of banking institutions (Yan et al. 2022).

At a micro-level, the consumers/users of FinTech products perceive higher value when there is a high performance expectancy (Yan et al. 2021), which is a similar concept to relative advantage. Thus, we expect that relative advantage comprises positive advantages in terms of the emotional and/or functional value.

No prior studies have examined these two dimensions of perceived investment value for the crowdlending field, so the present research endeavors to fill this gap. Hence, the following hypotheses were developed:

H1.a

Relative advantage influences the perceived economic investment value of crowdlending.

H1.b

Relative advantage influences the perceived emotional investment value of crowdlending.

In the diffusion of innovation theory, complexity is positioned as a perception of the possible difficulties when using a new product, service, experience, or practice (Rogers 1983), so it relates to ease of use or effort expectancy. Digitalization has affected markets in several ways. Markets are traditionally influenced by information asymmetry, agency problems, and the complexity of monitoring contracts (Jain and Raman 2022).

During recent years, traditional intermediaries have adopted rigorous rules for financial products, leading to greater complexity for SMEs when looking to obtain financing. In contrast, Bollaert et al. (2021) indicated that the appearance of new digital technologies in finance has facilitated “access to finance.” In order to sustain activities and improve performance, banks have applied new techniques like green finance and FinTech (Guang-Wen and Sidik 2022). Furthermore, technological innovation played an interesting role during the COVID-19 pandemic in maintaining the sustainability of financial institutions. More specifically, digital and mobile banking can decrease the complexity of transactions by reducing the need to visit banks in person, which has a physical cost for consumers. The costs associated with financing through banks and other financial institutions and the inability to invest any amount discourage many potential investors from joining the market. The complexity or ease of use is also a common factor that explains the acceptance and adoption of innovations, and it is included in the most well-known theories and frameworks, such as UTAUT (Venkatesh et al. 2012; Senanu and Narteh 2023), TAM (Davis et al. 1989), and the diffusion of innovation theory (Rogers 1983). It has recently been verified as an antecedent to perceived value in the mobile payment industry (Wang 2022; Shaw et al. 2022) and online/mobile shopping apps (Garrouch and Timoulali 2020; Jiang et al. 2022). In the general mobile FinTech context, the findings of Yan et al. (2021) show the significant impact of effort expectancy on the perceived value of mobile FinTech. While most prior studies have focused on absolute assessments of complexity, we expect that emotional value will be affected negatively by relative complexity, which can be a source of stress and anxiety for FinTech users. The economic aspect follows the notion that customers perceive utilitarian value based on the balance between benefits and sacrifices. Nevertheless, complexity is a sacrifice of sorts when using a product or service, so the economic value is diminished by relative complexity. The aim of the following hypotheses is to propose the expected relation between relative complexity and the dimensions of perceived investment value in the crowdlending context.

H2.a

Relative complexity influences the perceived economic investment value of crowdlending.

H2.b

Relative complexity influences the perceived emotional investment value of crowdlending.

The information quality of a platform

The proposed model is further enriched through another variable to reflect the specific evaluation that users make when first contacting a particular crowdlending platform, and this is the information quality of the crowdlending platform. This variable is an important characteristic, because concrete information should be provided about the actual investment procedure with a real crowdlending platform. Ribeiro-Navarrete et al. (2021) investigated disclosure patterns and the experiences of investors based on the information communicated by platforms, while Yan et al. (2021) found that during the COVID-19 pandemic, the mobile financial service platforms played an interesting role in ensuring economic resilience. Yan et al. (2022) indicated that digitalization could improve productivity and growth and promote sustainable economies.

The quality of information provided by a platform, usually through its website, is one way to reduce uncertainty and cultivate trust toward the crowdlending platform (Alharbey and Hemmen 2021). A website’s efficiency and quality, as well as customers’ perceptions of information quality, are important for appealing to investors and retaining them as regular customers. In the banking sector, it is essential for a banker to have the “authority to satisfy most SME financial needs” (Madill et al. 2002, p. 93) when a firm wants to get a loan. The new platforms, however, publish their fees, guarantees, and durations even before an entrepreneur requests them. Website transparency and quality can be interesting factors that affect switching behavior, so websites must provide comprehensive information in an easily understandable format (Kim and Nihem 2009). Mensah and Amenuvor (2022) investigated the relation between marketing communications strategy and consumer purchasing behaviour in the financial services industry. Based on a responses from 360 users of several financial institutions in Ghana, they found that the consumer purchase behaviour is affected positively by the marketing communication strategies. Platform quality is therefore a crucial factor shaping intentions toward crowdlending platforms (Maier 2016), which ultimately affect a platform’s success. The overall crowdlending procedures should demonstrate professionalism to attract and retain lenders and borrowers. The characteristics of website quality have been determined by researchers and grouped into various types, such as ease of use, service quality, and service security. Moreover, a customer’s initial opinion of a platform can influence the subsequent development of trust and successful communication.

This variable has been an important predictor in models that focus on customers’ continuance intentions toward a new technology (Delone and Mclean 2003; Kang and Namkung 2019; Bouhlel et al. 2023). Kang and Namkung (2019) investigated the impact of information quality as a central determinant of a consumer’s information processing path in terms of purchase frequency through a new commerce platform. In addition, perceived information quality has been associated with satisfaction with new e-services platforms (Tam and Oliveira 2017; Al-Maroof and Salloum 2021), trust, and the intention to invest in crowdfunding platforms (Alharbey and Hemmen 2021).

Perceived quality influences perceived value (Kim and Niehm 2009), such that there is a strong relationship between information quality, service quality, and perceived value. Indeed, service quality is affected by information quality, while perceived value is connected to service quality. Platform quality, information quality, and service quality are therefore crucial factors for attracting lenders and borrowers to use a crowdlending platform.

Our study builds upon the existing debate about this subject. Moreover, no prior studies have examined the impact of this variable on the perceived value of crowdlending investment. We assume that a platform’s information quality contributes to forming and maintaining perceptions about the value of investing in a crowdlending platform, which is the main direct determinant of switching intentions.

Accordingly, the third set of hypotheses was developed as follows:

H3.a

A crowdlending platform’s information quality influences the perceived economic investment value of crowdlending.

H3.b

A crowdlending platform’s information quality influences the perceived emotional investment value of crowdlending.

Switching intentions as an outcome of perceived value

Fama and French (2007) stated that we cannot estimate investors’ intentions to invest in shares based purely on the return and risk. Several investigations have used consumer behavior theories and tools in the search for a more comprehensive perspective for investment, the choices that influence it, and the broad financial behaviors (Fama and French 2007). Our targeted behavioral intention in this case is switching intentions toward crowdlending, something that has been scarcely studied in the FinTech context, making it a source of research novelty (Maier 2016). In addition, “matching supply and demand in crowdlending requires double switching behavior: both from companies away from their bank, and from consumers from other forms of investment” (Maier 2016, p. 144).

Cronin et al. (2000) stated that perceived value is a good estimator of repurchase intentions, more so than customer satisfaction or service quality, with the authors concluding that perceived value is an interesting antecedent to customer satisfaction and behavioral intentions. The notion of an investment’s perceived value is interesting within the service industry, because it is a central goal for several institutions in order to maintain a solid competitive advantage. The concept of perceived value could also be used to comprehend individual behavior in several contexts, such as financial services (Puustinen et al. 2013). It can also be used to reflect the post-use assessment and its influence on future intentions. Moreover, this concept has been verified as a predictor of behavioral intentions toward digital financial services (Puustinen et al. 2013; Berraies et al. 2017) and FinTech payments (Lee et al. 2015; Chen et al. 2019; Garrouch 2021, 2022; Garrouch et al. 2023). Yan et al. (2021) examined the factors that affect the intentions of mobile financial service users during the COVID-19 pandemic in Bangladesh. To verify their hypotheses, the authors distributed a structured questionnaire survey to 227 potential mobile financial service users. They found that some determinants—such as social influence, perceived trust, and perceived value—affect the intention of users to use mobile financial service platforms.

Many studies have looked at switching intentions, but there is no consensus in their findings. To illuminate the effect of perceived investment value on switching intentions, the subsequent research hypotheses were formulated:

H4.a

The perceived economic investment value of crowdlending has a positive impact on switching intentions.

H4.b

The perceived emotional investment value of crowdlending has a positive impact on switching intentions.

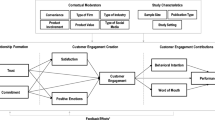

The conceptual model is summarized in Fig. 1 below.

Conceptual model

Method and data

Research design and sample

The population comprises all Saudi citizens and residents who have a bank account and the potential to have savings. This population was targeted in the survey sample by using a filter question about having monetary savings and a bank account. The sampling procedure was based on an online survey distributed through email and social media accounts and groups in two ways:

-

The survey link and informed consent was posted on social media groups with a professional leaning and a tendency to discuss investment possibilities. Three students who had graduated from a master’s course in business administration helped to post survey links to these social media groups.

-

Using snowball sampling, current MBA students working in different Saudi companies were asked to share the survey through their professional networks and ask recipients to in turn share the link.

Before answering any other questions, participants were asked a filter question about monetary savings (a yes or no question). They were then asked to watch a short video about crowdlending and visit the websites for Saudi crowdlenders “Manafa” and “Forus.”

The flowchart of the used method is simplified and summarized in a flowchart represented in Fig. 2.

Flowchart of research methodology

The resulting sample comprised 201 valid observations, the demographics of which are given in Table 1.

Measures

Five-point, multi-item scales were extracted from the literature as follows: A crowdlending platform’s information quality was measured according to three items adapted from the scale of Tam and Oliveira (2017). Three items proposed by Maier (2016) were used to measure switching intentions toward crowdlending, while perceived investment value was measured based on six items extracted from the scale of Puustinen et al. (2013). Relative advantage and comparative complexity were assessed through an adaptation of the items employed by Chung (2014) based on Rogers’ (1983) framework. Indeed, three items were used for each of these measurements. The adaptation primarily involved contextualizing each item to the crowdlending situation. For the complexity and relative advantage items, we added a comparative element, such as in the following sample item: “Compared to traditional ways of investing…”. All scales were assessed based on a five-point Likert scale. The final questionnaire was pretested by five experts and 10 surrogates, thus allowing us to verify that the items were understandable, well presented, and aligned to the measured concept, with us adapting the survey per their recommendations.

Data analysis

Reliability was verified in two ways, namely exploratory analysis with the Cronbach’s alpha and confirmatory analysis using the composite reliability. The measurement scales were first purified through an exploratory analysis using SPSS. We started the exploratory factorial analysis using the principal component analysis technique, followed by an exploratory reliability assessment through the Cronbach’s alpha. Any items with low communality values (i.e., below 0.5), as well as those that were represented in two or more factors or contributed to low reliability (i.e., the Cronbach’s alpha was significantly higher if the item was deleted) were removed.

The proposed measurement model was assessed using structural equation modeling with the AMOS 24 software. This assessment was based on the measurement model’s goodness of fit indicators, such that the ratio between the chi-square and degrees of freedom needed to be below 5, while the GFI (goodness fit index), NFI (normed fit index), and IFI (incremental fit index) had to be above 0.9. In addition, the RMSEA (root mean square error) needed to be compared against a threshold of 0.08.

The reliability and convergent validity are verified when the item loadings and their respective composite reliabilities are greater than 0.7. In addition, the value of AVE (average variance extracted) should be above 0.5.

Regarding discriminant validity, the AVE’s square root was also compared to the inter-construct correlation for each construct, with the result being positive if the AVE was higher than the inter-construct correlation.

The final step was to analyze the model parameter estimates and their respective significances. When the latter was below 0.05 and the parameter estimates supported a hypothesis, that hypothesis was accepted.

Results and analysis

Measurement model

The exploratory factorial analysis resulted in a one-dimensional structure for each of the following scales: relative advantage, relative complexity, platform’s information quality, and switching intention. This is in line with the original structure shown in the studies from which we extracted these scales. However, the perceived investment value of crowdlending showed a two-dimensional structure, such that the first dimension represented the economic value and the second denoted the emotional value. The reliability of all these variables and dimensions were assessed via the Cronbach’s alpha values, all of which were above 0.7, except the emotional value with an alpha of 0.623 (Table 2). This could be explained by it being the first use of this dimension of value in the crowdlending context, which tends to be dominated by utilitarian factors.

Regarding the measurement model’s goodness of fit, the chosen indicators reveal that it is acceptable. Indeed, the ratio between the chi-square and degrees of freedom was 1.75, which is below 2. The goodness of fit index (GFI) was 0.912, the NFI was 0.915, and the IFI was 0.968. All these indicators were above 0.9, confirming that the model was an acceptable fit. In addition, the RMSEA (0.052) was below 8%.

The reliability and convergent validity were also verified. Indeed, Table 2 shows that the item loadings had values above 0.7, while the composite reliability indicators were also higher than 0.7. Moreover, the AVE values were above 0.5, with the exception of the economic value dimension with an AVE that was close to the required threshold of 0.5, specifically 0.495.

Regarding discriminant validity, we compared the AVE’s square root with the inter-construct correlation for each construct, with the results showing that the AVEs were higher than the inter-construct correlations (Table 3).

Hypotheses testing

The model path coefficients and significance allowed us to verify or reject the proposed hypotheses. These indicators are displayed in Table 4.

The impact of relative advantage on perceived value was verified for both dimensions of it. Indeed, the perceived relative advantage of crowdlending has a positive and significant impact on both emotional value (B = 0.403, P = 0.000) and economic value (B = 0.58, P = 0.000).

Thus, H1a and H1b were accepted. In contrast, H2a and H2b were rejected because relative complexity does not have a significant impact on either economic value (P = 0.643) or emotional value (P = 0.766).

The crowdlending platform’s quality had a significant impact on both dimensions of value, specifically economic (B = 0.215, P = 0.019) and emotional (B = 0.304, P = 0.002) value, so H3a and H3b were accepted.

The impact of perceived investment value on switching intentions toward crowdlending was subdivided into two facets, the influences of perceived economic value and perceived emotional value. Both of these had a significant and positive impact. More specifically, the significance of the path between the dependent variable with emotional value was below 0.05 (P = 0.025) with a positive parameter estimate (B = 0.177). In addition, the parameter estimate for the impact of economic value was positive (B = 0.600) with a significance below the threshold (0.000). H4a and H4b were therefore accepted.

Discussion

Overall, the proposed model was deemed acceptable because it shows good adjustment indicators with most of its paths being significant. The only hypotheses to be rejected were the ones linking relative complexity with the perceived crowdlending investment value. Indeed, both dimensions of value were not influenced by relative complexity as perceived by the potential crowdlending users.

This result is not in line with the assumptions of the diffusion of innovations theory, which considers complexity as hindering the favorable reception of a new technology (Chung 2014; Wang 2022). This unusual result leads to a question: Does complexity act as an absolute variable or as a relative one within the FinTech context? This question needs further discussion, because this current study is among the first to use complexity in a comparative way. The anticipated result was that if crowdlending was perceived to be more complex than the traditional forms of investment, consumers would be dissuaded from taking advantage of this FinTech option. In contrast, the findings show that relative complexity is not necessarily a barrier to adoption, suggesting that complexity maybe influential in an absolute rather than comparative manner. Thus, excessive complexity may be a dissuading element without needing to compare its level to other alternatives.

Another novelty of this result lies in the finding that relative complexity does not diminish the emotional value of investing through crowdlending. This disagrees with prior studies that link complexity with affective reactions, such as when low complexity in webpages was found to be associated with positive affective reactions. Nevertheless, this could be explained by the nature of the dependent variable in this path. Indeed, perceived value could be considered as the result of an evaluation or judgement, or perhaps a preference, rather than a behavioral reaction (Zeithaml 1988; Holbrook 1999). Thus, users develop an emotional and economic evaluation of this new form of investment without considering the psychological effect of subjective sacrifices, such as dealing with the complexity of the tool. However, this factor may be more influential when engaging in a real experience of investment through a crowdlending platform. Unfortunately, we only asked the sample to visit the sites, so it is unlikely that they went through the actual investment procedure. For those who are used to a platform’s services, the relative complexity would become less influential as repeating the same tasks tends to reduce the difficulty associated with them.

The impact of the relative advantage of crowdlending investment services on perceived value was verified. Although this path has not been studied in prior research studies, this result agrees with other studies that have tested the impact of similar concepts on perceived value in the context of financial services and FinTech. Indeed, prior studies have suggested that convenience and efficiency are among the principal relative advantages of new technologies and services (Lin and Lu 2015; Nel and Heyns 2017), having been studied as determinants of utilitarian values (Lin and Lu 2015; Wang 2022). More specifically, Wang (2022) verified the impact of relative advantage on the utilitarian and hedonic dimensions of perceived value within the context of mobile payment. The hedonic value that derives from relative advantage can be explained through the fact that an innovation’s relative advantage tends to trigger positive affective feelings among users. For example, if the user is spared from time and effort, his or her feelings of pleasure and satisfaction may be enhanced (Li et al. 2020). This has been verified by studies that proved that technological convenience affects the perception of emotional/hedonic value (Wang 2022). Thus, the results of our study provide evidence that facilitating access to finance through digitalization positively influences the intentions of Saudi users to adopt crowdlending platforms. Accordingly, it can be concluded that these users play an interesting role in the implementation of new technologies, namely crowdlending platforms in this case, in the context of emerging countries. To seize this opportunity, many factors should be considered as influencing the switch from micro-investment, savings accounts, and FOREX investment to crowdlending. These factors are discussed in the following paragraphs based on our findings.

This research has shown that the perceived platform quality has a positive impact on both dimensions of perceived investment value. This agrees with the results of Kim and Niehm (2009), who showed that there is a strong relation between information quality, service quality, and perceived value. This result also confirms the findings of prior studies in different fields that linked quality to perceived value (Zeithaml 1988; Hong et al. 2020).

The link between switching intentions and value was verified in this study. This result accords with a large number of prior studies in different fields (Hong et al. 2020; Wang 2022), such as for financial services (Puustinen et al. 2013; Berraies et al. 2017) and FinTech payment services (Lee et al. 2015; Chen et al. 2019; Garrouch 2021). Our results, however, are specific to the crowdlending context, which has not been studied through the lens of the influence of perceived value. Specifically, emotional value emerged as a factor that contributes to intentions to switch to investing through crowdlending platforms. Moreover, the findings suggest that the perceived economic value has a significant effect on users’ switching intentions toward crowdlending platforms. This can be regarded as an extension to prior studies that have evaluated the impact of value on the abstract definition of behavioral intentions (Puustinen et al. 2013; Lee et al. 2015; Berraies et al. 2017; Chen et al. 2019; Hong et al. 2020; Garrouch 2021, 2023; Wang 2022; Garrouch et al. 2023).

In summary, users decide to use these new platforms based on the relative advantage, perceived platform quality, and perceived value rather than the relative complexity.

Implications, limitations, and future directions

Theoretical implications

This study contributes to the financial technology literature by proposing a model that explains perceived investment value and switching intentions toward a FinTech offering. To the best of our knowledge, the model tested in this study represents the first initiative to empirically examine perceived investment value in the crowdlending context. In addition, our research highlights the most important factors in attracting crowdlending users and enhancing the perceived value of the service.

This study also clarifies and verifies the relationships among crowdlending’s innovation attributes and perceived investment value, which is two-dimensional in nature here. While this concept has been studied by Puustinen et al. (2013) to develop a multidimensional assessment, it has not been used in a FinTech context like crowdlending. The importance of perceived investment value should not be underestimated, because it can mediate between the innovation attributes and its acceptance by potential users. This idea was partly confirmed in our study when we established the impact of two attributes, namely relative advantage and complexity, in addition to the very important factor of platform quality.

Moreover, relative advantage, relative complexity, and information quality concur with the TDOI. It should also be noted that the links between economic value, emotional value, and switching intention were validated for the FinTech context. More specifically, emotional value emerged as a factor that contributes to switching intentions toward investing through crowdlending platforms. This finding enriches the mainstream literature by shedding light on the importance of intrinsic values and motivations in the financial field as decisive factors driving FinTech adoption.

Another point that arose concerns whether complexity should be considered in a comparative or absolute form. The comparative approach of relative complexity did not seem to be influential, suggesting that it may be more relevant to consider an absolute assessment. Although prior research has exclusively used the absolute measure, our research is among the first to demonstrate the suitability of using this approach.

Finally, the current research shows how developing countries like the KSA may use FinTech to diversify their sources of financing, especially as in the KSA, oil is the principal source of revenue and bank financing is high.

Managerial implications

This study has numerous managerial implications. First, it gives some ideas for bankers, investors, regulators, and governments in that the new platforms offer advantages over banks and financial institutions because they connect borrowers and lenders directly. Crowdlending platforms could also take advantage of the weaknesses of traditional intermediaries in order to create a good level of perceived value.

Second, the findings are of practical interest to crowdlending users. Indeed, as the relative advantage is the main innovation attribute affecting perceived value and in turn switching intentions, it is recommended to create a communication strategy that focuses on the main advantages of crowdlending compared to other more traditional investment opportunities, such as bank deposits and stock investments.

These advantages could range from higher returns to lower psychological and financial costs. If the targeted segment of potential micro-investors are people with savings in their bank accounts, using comparative arguments in persuasive advertisements seems a better way to encourage them to progressively switch from bank deposits to crowdlending investments. The arguments could become more complicated and analytical when trying to convince investment professionals, who have a greater range of alternatives to compare with crowdlending options. Thus, this segment needs direct marketing and more elaborate website links to illustrate some multi-dimensional comparisons between these different forms of investment.

Third, the quality of a platform in terms of information quality should always be well established and assessed regularly by crowdlending managers to ensure that the quality of information meets users’ expectations. The simplicity and presentation of information are crucial aspects of information quality for entrepreneurs and investors. Thus, when the content on a website is not difficult to read and not overly complex, and the format of the platform is not difficult to navigate, users perceive a higher level of information quality.

Finally, our findings show that emotional value is one of the factors supporting switching intentions toward crowdlending for micro-investors. Advertisements and sponsored social media influencers should therefore include this facet in their scripts and contents.

Limitations and future directions

This research requires further development due to a few limitations. Although the sample had a fairly acceptable size that allowed us to use the maximum likelihood method in structural equation modelling, it could be larger still in order to achieve better external validity. In addition, a balance between demographic categories was not achieved because female subjects comprised barely a quarter of the sample. Another limitation was not including specific dimensions of investment value—such as efficiency value, self-esteem value, and altruism value—which already exist in investment value scales. Thus, we propose some future research avenues to overcome the current limitations:

-

First, extend the sample in order to highlight the differences between many categories, such as actual users versus potential users, males versus females, entrepreneurs versus non-entrepreneurs, and so on.

-

Second, adopt and adapt the full range of measures of investment value, which includes many dimensions.

-

-Third, verify the possible mediating effects of perceived value dimensions rather than only verifying the separate direct impacts.

References

Abbas, M., M.S. Nawaz, J. Ahmad, M. Ashraf, and E. Kostadinova. 2017. The effect of innovation and consumer related factors on consumer resistance to innovation. Cogent Business & Management 4 (1): 1312058.

Abikari, M., P. Öhman, and D. Yazdanfar. 2022. Negative emotions and consumer behavioural intention to adopt emerging e-banking technology. Journal Financial Services Marketing. https://doi.org/10.1057/s41264-022-00172-x.

Alharbey, M., and S. Van Hemmen. 2021. Investor intention in equity crowdfunding. Does trust matter? Journal of Risk and Financial Management 14 (2): 53.

Al-Maroof, R.S., and S.A. Salloum. 2021. an integrated model of continuous intention to use of google classroom. In Studies in systems, decision and control, vol. 295, 311–335. Cham: Springer.

Babin, B.J., W.R. Darden, and M. Griffin. 1994. Work and/or fun: measuring hedonic and utilitarian shopping value. Journal of Consumer Research 20 (4): 644.

Berraies, S., K. Ben Yahia, and M. Hannachi. 2017. Identifying the effects of perceived values of mobile banking applications on customers: Comparative study between baby boomers, generation X and generation Y. International Journal of Bank Marketing 35 (6): 1018–1038.

Bollaert, H., Florencio Lopez-de-Silanes, and Armin Schwienbacher. 2021. Fintech and access to finance. Journal of Corporate Finance 68: 101941.

Borrero-Domínguez, C., E. Cordón-Lagares, and R. Hernández-Garrido. 2020. Analysis of success factors in crowdfunding projects based on rewards: A way to obtain financing for socially committed projects. Heliyon 6 (4): e03744.

Bouhlel, O., K. Garrouch, and M.N. Mzoughi. 2023. Assessing the success of mobile banking in Saudi Arabia: Re-specification and validation of the DeLone and McLean model. International Journal of E-Services and Mobile Applications 15 (1): 1–24.

Bouncken, R.B., and S. Kraus. 2021. Entrepreneurial ecosystems in an interconnected world: Emergence, governance and digitalization. Review of Managerial Science 40 (1): 1–14.

Buchak, G., G. Matvos, T. Piskorski, and A. Seru. 2018. Fintech, regulatory arbitrage, and the rise of shadow banks. Journal of Financial Economics 130 (3): 453–483.

Candra, S., F. Nuruttarwiyah, and I.H. Hapsari. 2020. Revisited the technology acceptance model with E-trust for peer-to-peer lending in Indonesia (perspective from Fintech users). International Journal of Technology 11 (4): 710.

Chen, S.C., K.C. Chung, and M.Y. Tsai. 2019. How to achieve sustainable development of mobile payment through customer satisfaction—the SOR model. Sustainability 11 (22): 6314.

Chung, K.C. 2014. Gender, culture and determinants of behavioural intents to adopt mobile commerce among the Y Generation in transition economies: Evidence from Kazakhstan. Behaviour & Information Technology 3 (7): 743–756.

Cronin, J.J., M.K. Brady, and G.T.M. Hult. 2000. Assessing the effects of quality, value and customer satisfaction on consumer behavioral intentions in service environments. Journal of Retailing 76 (2): 193–218.

Davis, F.D., R.P. Bagozzi, and P.R. Warshaw. 1989. User acceptance of computer technology: A comparison of two theoretical models. Management Science 35 (8): 982–1003.

DeLone, W.H., and E.R. McLean. 2003. The Delone and Mclean model of information systems success: A ten-year update. Journal of Management Information Systems 19 (4): 9–30.

ECB. 2017. Survey on the access to finance of enterprises. European Central Bank. Available at https://www.ecb.europa.eu/stats/ecb_surveys/safe/html/index.en.html.

Fama, E.F., and K.R. French. 2007. Disagreement, tastes, and asset prices. Journal of Financial Economics 83 (3): 667–689.

Garrouch, K. 2021. Does the reputation of the provider matter? A model explaining the continuance intention of mobile wallet applications. Journal of Decision Systems 30 (2): 150–171.

Garrouch, K.F. 2022. Explaining the comparative perception of e-payment: Role of e-shopping value, e-payment benefits and Islamic compliance. Journal of Islamic Marketing 13 (7): 1574–1588.

Garrouch, K., and E. Timoulali. 2020. Mobile shopping intentions: Do trustworthiness and culture Matter? Journal of Distribution Science 18 (11): 69–77.

Garrouch, K., O. Bouhlel, and M.-N. Mzoughi. 2023. E-payment or cash on delivery: Do e-retailers' ethics, trust, and value matter. International Journal of Electronic Marketing and Retailing, Forthcoming and online first articles. https://www.inderscience.com/info/ingeneral/forthcoming.php?jcode=ijemr, last update, Accessed 16 Jan 2023.

Giudici, P. 2018. Fintech risk management: A research challenge for artificial intelligence in finance. Frontiers in Artificial Intelligence 1, 1–6.

Gozali, L., M. Masrom, T.Y.M. Zagloel, H.N. Haron, J.A. Garza-Reyes, B. Tjahjono, A.P. Irawan, F.J. Daywin, A.F. Syamas, S. Susanto, H.K.K. Aliwarga, and I.A. Marie. 2020. Performance factors for successful business incubators in Indonesian Public Universities. International Journal of Technology 11 (1): 156–166.

Guang-Wen, Z., and A.B. Siddik. 2022. The effect of Fintech adoption on green finance and environmental performance of banking institutions during the COVID-19 pandemic: The role of green innovation. Environmental Science and Pollution Research. https://doi.org/10.1007/s11356-022-23956-z.

Holbrook, M.B. 1999. Introduction to consumer value. In Consumer value: A framework for analysis and research, ed. M.B. Holbrook, 1–28. London and New York: Routledge.

Hong, J.P., B.Y. Kim, and S.H. Oh. 2020. The perceived experiential value and service quality of auto maintenance and repair service. Journal of Distribution Science 18 (1): 59–69.

Huang, Z., C.L. Chiu, S. Mo, and R. Marjerison. 2018. The nature of crowdfunding in China: Initial evidence. Asia Pacific Journal of Innovation and Entrepreneurship 12 (3): 300–322.

Jain, N., and T.V. Raman. 2022. A partial least squares approach to digital finance adoption. Journal Financial Services Marketing 27: 308–321. https://doi.org/10.1057/s41264-021-00127-8.

Jiang, X., N. Deng, X. Fan, and H. Jia. 2022. Examining the role of perceived value and consumer innovativeness on consumers’ intention to watch intellectual property films. Entertainment Computing 40 (1): 100453.

Jureidni, M. 2017. Small and medium enterprises: Pulse of the Saudi economy. Available at http://english.alarabiya.net/en/business/economy/2017/09/18/Small-and-medium-enterprises-Pulse-of-the-Saudi-economy.html

Kang, J.W., and Y. Namkung. 2019. The information quality and source credibility matter in customers’ evaluation toward food O2O commerce. International Journal of Hospitality Management 78: 189–198.

Kaur, S., and S. Arora. 2023. Understanding customers’ usage behavior towards online banking services: An integrated risk-benefit framework. Journal Financial Services Marketing 28: 74–98. https://doi.org/10.1057/s41264-022-00140-5.

Kim, H., and L.S. Niehm. 2009. the impact of website quality on information quality, value, and loyalty intentions in apparel retailing. Journal of Interactive Marketing 23 (3): 221–233.

Lee, C., H. Yun, C. Lee, and C.C. Lee. 2015. Factors affecting continuous intention to use mobile wallet : Based on value-based adoption model. The Journal of Society for E-Business Studies 2 (1): 117–135.

Li, X., Q. Liao, X. Luo, and Y. Wang. 2020. Juxtaposing impacts of social media interaction experiences on ecommerce reputation. Journal of Electronic Commerce Research 21 (2): 75–79.

Lin, K.Y., and H.P. Lu. 2015. Predicting mobile social network acceptance based on mobile value and social influence. Internet Research 25 (1): 107–130.

Madill, J.J., L. Feeney, A. Riding, and G.H. Haines Jr. 2002. Determinants of SME owners’ satisfaction with their banking relationships: A Canadian study. International Journal of Bank Marketing 20 (2): 86–98.

Maier, E. 2016. Supply and demand on crowdlending platforms: Connecting small and medium-sized enterprise borrowers and consumer investors. Journal of Retailing and Consumer Services 33 (6): 143–153.

Martínez-Climent, C., R. Costa-Climent, and P. Oghazi. 2019. Sustainable financing through crowdfunding. Sustainability 11: 934.

Martínez-Climent, C., M. Guijarro-García, and A. Carrilero-Castillo. 2021. The motivations of crowdlending investors in Spain. International Journal of Entrepreneurial Behaviour and Research 27 (2): 452–469.

Mensah, K., and F.E. Amenuvor. 2022. The influence of marketing communications strategy on consumer purchasing behaviour in the financial services industry in an emerging economy. Journal Financial Services Marketing 27: 190–205. https://doi.org/10.1057/s41264-021-00121-0.

Mombeuil, C., and H. Uhde. 2021. Relative convenience, relative advantage, perceived security, perceived privacy, and continuous use intention of China’s WeChat Pay: A mixed-method two-phase design study. Journal of Retailing and Consumer Services 59: 102384.

Moreno-Moreno, A.M., C. Sanchis-Pedregosa, and E. Berenguer. 2019. Success factors in peer-to-business (P2B) crowdlending: A predictive approach. IEEE Access 7: 148586–148593.

Nel, J., and N. Heyns. 2017. The in-store factors influencing the use-intention of proximity mobile-payment applications. Management Dynamics 26 (2): 2–20.

Nicoletti, B. 2017. The future of FinTech. springer cham: Palgrave Macmillan. https://EconPapers.repec.org/RePEc:pal:psinst:978-3-319-51415-4.

Oweis, K.A., and O.F. Alghaswyneh. 2019. The antecedents of electronic banking adoption in Saudi Arabia: Using diffusion of innovation theory. Marketing and Management of Innovations 4: 160–171.

Puustinen, P., P. Maas, and H. Karjaluoto. 2013. Development and validation of the perceived investment value (PIV) scale. Journal of Economic Psychology 36: 41–54.

Reddick, C.G., G.P. Cid, and S. Ganapati. 2019. Determinants of blockchain adoption in the public sector: An empirical examination. Information Polity 24 (4): 379–396.

Ribeiro-Navarrete, S., D. Palacios-Marqués, C. Lassala, and K. Ulrich. 2021. Key factors of information management for crowdfunding investor satisfaction. International Journal of Information Management 59: 102354.

Rogers, E.M. 1983. Diffusion of innovations. New York: Free Press.

Rogers, E.M., U. Medina, M. Rivera, et al. 2005. Complex adaptive systems and the diffusion of innovations. Innovation Journal 10 (3): 29.

Schueffel, P. 2016. Taming the beast: A scientific definition of Fintech. Journal of Innovation Management 4 (4): 32–54.

Senanu, B., and B. Narteh. 2023. Banking sector reforms and customer switching intentions: Evidence from the Ghanaian banking industry. Journal Financial Services Marketing 28: 15–29. https://doi.org/10.1057/s41264-021-00135-8.

Shaw, N., B. Eschenbrenner, and B.M. Brand. 2022. Towards a mobile app diffusion of innovations model: A multinational study of mobile wallet adoption. Journal of Retailing and Consumer Services 64: 102768.

Sjamsudin, S.H. 2019. The impact of the development of Fintech on the existing financial services in Indon Tam esia. International Journal of Advanced Research in Technology and Innovation 1 (1): 14–23.

Tam, C., and T. Oliveira. 2017. Understanding mobile banking individual performance: The DeLone & McLean model and the moderating effects of individual culture. Internet Research 27 (3): 538–562.

Venkatesh, V., J.Y.L. Thong, and X. Xu. 2012. Consumer acceptance and use of information technology: Extending the unified theory of acceptance and use of technology. MIS Quarterly: Management Information Systems 36 (1): 157–178.

Wang, E.S.-T. 2022. Influences of innovation attributes on value perception and usage intentions of mobile payment. Journal of Electronic Commerce Research 23 (1): 45–58.

Xie, P., C. Zou, and H. Liu. 2016. The fundamentals of internet finance and its policy implications in China. China Economic Journal 9 (3): 240–252.

Yan, C., A.B. Siddik, N. Akter, and Q. Dong. 2021. Factors influencing the adoption intention of using mobile financial service during the COVID-19 pandemic: The role of FinTech. Environmental Science and Pollution Research. https://doi.org/10.1007/s11356-021-17437-y.

Yan, C., A.B. Siddik, L. Yong, Q. Dong, G.-W. Zheng, and M.N. Rahman. 2022. A two-staged SEM-artificial neural network approach to analyze the impact of FinTech adoption on the sustainability performance of banking firms: The mediating effect of green finance and innovation. Systems 10 (5): 148.

Yang, T., and X. Zhang. 2022. FinTech adoption and financial inclusion: Evidence from household consumption in China. Journal of Banking & Finance 145: 106668. https://doi.org/10.1016/j.jbankfin.2022.106668.

Zeithaml, V.A. 1988. Consumer perceptions of price, quality, and value: A means-end model and synthesis of evidence. Journal of Marketing 52: 2–22.

Funding

The authors extend their appreciation to the Deputyship for Research & Innovation, Ministry of Education in Saudi Arabia for funding this research work through the project number 8063.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

On behalf of all authors, the corresponding author states that there is no conflict of interest.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Riahi, Y., Garrouch, K. A model explaining perceived investment value and switching intentions toward FinTech: the case of crowdlending. J Financ Serv Mark (2023). https://doi.org/10.1057/s41264-023-00222-y

Received:

Revised:

Accepted:

Published:

DOI: https://doi.org/10.1057/s41264-023-00222-y