Abstract

We relax the strong rationality assumption for the agents in the paradigmatic Kyle model of price formation, thereby reconciling the framework of asymmetrically informed traders with the Adaptive Market Hypothesis, where agents use inductive rather than deductive reasoning. Building on these ideas, we propose a stylised model able to account parsimoniously for a rich phenomenology, ranging from excess volatility to volatility clustering. While characterizing the excess-volatility dynamics, we provide a microfoundation for GARCH models. Volatility clustering is shown to be related to the self-excited dynamics induced by traders’ behavior, and does not rely on clustered fundamental innovations. Finally, we propose an extension able to account for the fragile dynamics exhibited by real markets during flash crashes.

Similar content being viewed by others

Notes

The idea, which will be formalized in what follows, is that the market maker revises his own belief about fundamental price volatility such that the price volatility expectation matches the price volatility estimate constructed from past price history. We shall see that this implies a feedback loop between past and future price volatility leading to the volatility clustering effect observed in empirical data.

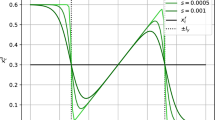

Let us mention here that \(\tau _{\text {fast}}\) can have a more interesting behavior if the noise trader is cost-averse. We shall come back to this in Sect. 4.2

We will clarify what we mean by large times below when we analyze the dynamics more precisely.

This terminology originates from physics, where the fluctuating field is evaluated on its average value, neglecting therefore the fluctuations around it. This is exactly what we are doing here, where we are identifying the field with the noise trader’s volatility.

References

Arthur WB (1994) Inductive reasoning and bounded rationality. Am Econ Rev 84:406

Ascari G, Zhang Y (2022) Limited memory, time-varying expectations and asset pricing, working paper

Axtell RL, Farmer JD (2022) Agent-based modeling in economics and finance: past, present, and future. J Econ Literat

Bachelier L (1900) Théorie de la spéculation. Annales scientifiques de l’École Normale Supérieure 17:21

Bacry E, Delour J, Muzy JF (2001) Multifractal random walk. Phys Rev E 64:026103

Black F, Scholes M (1973) The pricing of options and corporate liabilities. J Polit Econ 81:637

Blume L, Easley D (2009) The market organism: Long-run survival in markets with heterogeneous traders. J Econ Dyn Contr 33:1023

Bollerslev T (1986) Generalized autoregressive conditional heteroskedasticity. J Econom 31:307

Bottazzi G, Giachini D (2019) Far from the madding crowd: collective wisdom in prediction markets. Quant Financ 19:1461

Bouchaud J-P, Bonart J, Donier J, Gould M (2018) Trades, quotes and prices: financial markets under the microscope. Cambridge University Press

Bouchaud J-P, Ciliberti S, Lempérière Y, Majewski A, Seager P, Ronia K (2017) Black was right: price is within a factor 2 of value. SSRN Electr J

Bouchaud J-P, Potters M (2003) Theory of financial risk and derivative pricing. Cambridge University Press

Bouchaud J-P (2008) Economics need a scientific revolution. Nature 455:1181

Bouchaud J-P, Mézard M (2000) Wealth condensation in a simple model of economy. Phys A Stat Mech Appl 282:536

Bouchaud J-P, Gefen Y, Potters M, Wyart M (2004) Fluctuations and response in financial markets: the subtle nature of ‘random’ price changes. Quant Financ 4:176

Cont R (2007) Long memory in economics. Springer, pp. 289–309

Cont R (2001) Empirical properties of asset returns: stylized facts and statistical issues. Quant Financ 1:223

Cordoni F, Lillo F (2022) Transient impact from the Nash equilibrium of a permanent market impact game, arXiv preprint arXiv:2205.00494

Cutler D, Poterba J, Summers L (1988) What moves stock prices?. In: NBER working papers 2538 (National Bureau of Economic Research, Inc)

Diebold FX (2004) The nobel memorial prize for Robert F Engle. Scand J Econ 106:165

Dindo P, Massari F (2020) The wisdom of the crowd in dynamic economies. Theor Econ 15:1627

Engle RF (1982) Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation. Econometrica 50:987

Farmer R, Bouchaud J-P (2020) Self-fulfilling prophecies, quasi non-ergodicity and wealth inequality. Working Paper 28261. National Bureau of Economic Research

Follmer H, Horst U, Kirman A (2005) Equilibria in financial markets with heterogeneous agents: a probabilistic perspective. J Math Econ 41:123

Fosset A, Bouchaud J-P, Benzaquen M (2020) Endogenous liquidity crises. J Stat Mech Theory Exp

Gatheral J, Jaisson T, Rosenbaum M (2018) Volatility is rough. Quant Financ 18:933

Ghoulmie F, Cont R, Nadal J-P (2005) Heterogeneity and feedback in an agent-based market model. J Phys Cond Matter 17:S1259

Giachini D (2021) Rationality and asset prices under belief heterogeneity. J Evol Econ 31:207

Gualdi S, Cimini G, Primicerio K, Di Clemente R, Challet D (2016) Statistically validated network of portfolio overlaps and systemic risk. Sci Rep 6:39467

Hommes C (2021) Behavioral and experimental macroeconomics and policy analysis: a complex systems approach. J Econ Liter 59:149

Hommes C, Zhu M (2014) Behavioral learning equilibria. J Econ Theory 150:778

Inoua SM (2020) News-driven expectations and volatility clustering. J Risk Financ Manag 13:17

Jiang X, Chen T, Zheng B (2013) Time-reversal asymmetry in financial systems. Phys A Stat Mech Appl 392:5369

Joulin A, Lefevre A, Grunberg D, Bouchaud J-P (2008) Stock price jumps: news and volume play a minor role. Wilmott Mag

Kesten H (1973) Equilibria in financial markets with heterogeneous agents: a probabilistic perspective. Acta Math 131:207

Kyle A (1985) Continuous auctions and insider trading. Econometrica 53:1315

Lasry J-M, Lions P-L (2007) Mean field games. Jpn J Math 2:229

Lehalle C-A, Neuman E, Shlomov S (2021) Phase transitions in Kyle’s model with market maker profit incentives. SSRN Electr J. https://doi.org/10.2139/ssrn.3799712

Leroy SF (2013) Can risk aversion explain stock price volatility? FRBSF Economic Letter

LeRoy S, Porter RD (1981) The present-value relation: tests based on implied variance bounds. Econometrica 49:555

Lillo F, Farmer J (2004) The long memory of the efficient market. Stud Nonlinear Dyn Econ 8:1

Lo AW (2004) The adaptive markets hypothesis. J Portf Manag 30:15

Lo AW (2008) Efficient markets hypothesis. New Palgrave Dict Econ 2:1

Mandelbrot B (1963) The variation of certain speculative prices. J Bus 36:394

Mantegna RN, Stanley HE (1999) Introduction to econophysics: correlations and complexity in finance. Cambridge university press

Marcaccioli R, Bouchaud J-P, Benzaquen M (2022) Exogenous and endogenous price jumps belong to different dynamical classes. J Stat Mech Theory Exp 2022:023403

Miccichè S, Bonanno G, Lillo F, Mantegna RN (2002) Volatility in financial markets: stochastic models and empirical results. Phys A Stat Mech Appl 314:756

O’Hara M (1998) Market microstructure theory. Blackwell Publishing Ltd

Poledna S, Martínez-Jaramillo S, Caccioli F, Thurner S (2021) Quantification of systemic risk from overlapping portfolios in the financial system. J Financ Stab 52:100808

Roşu I (2019) Fast and slow informed trading. J Financ Markets 43:1

Shiller R (1981) do stock prices move too much to be justified by subsequent changes in dividends? Am Econ Rev 71:421

Shiller R (1990) Market volatility and investor behavior. Am Econ Rev 80:58

Shiller RJ (2013) Speculative asset prices. Tech Rep 2013:6

Sornette D, Cont R (1996) Convergent multiplicative processes repelled from zero: power laws and truncated power laws. Journal De Physique I France 7:431

Steinbacher M, Raddant M, Karimi F, Cuena E, Alfarano S, Iori G, Lux T (2021) Advances in the agent-based modeling of economic and social behavior. SN Bus Econ 1:99

Subrahmanyam A (1991) Risk aversion, market liquidity, and price efficiency. Rev Financ Stud 4:416

Tversky A, Kahneman D (1974) Judgment under uncertainty: heuristics and biases. Science 185:1124

Vodret M, Mastromatteo I, Tóth B, Benzaquen M (2021) A stationary Kyle setup: microfounding propagator models. J Stat Mech Theory Exp 2021:033410

Vodret M, Mastromatteo I, Tóth B, Benzaquen M (2022) Do fundamentals shape the price response? A critical assessment of linear impact models. Quant Financ 0:1

Wehrli A, Sornette D (2022) The excess volatility puzzle explained by financial noise amplification from endogenous feedbacks. Sci Rep 12

Zumbach G (2009) Time reversal invariance in finance. Quant Financ 9:505

Acknowledgements

We warmly thank F. Moret who contributed to the early stages of the analysis with a cost-averse noise trader, as well as J.-P. Bouchaud, C. H. Hommes, R. Marcaccioli and Y. Zhang for interesting discussions. This research was conducted within the Econophysics & Complex Systems Research Chair, under the aegis of the Fondation du Risque, the Fondation de l’Ecole polytechnique, the Ecole polytechnique and Capital Fund Management.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors declare that they have no conflict of interest.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

A How to simulate the model

A How to simulate the model

Below we present a pseudo-code to perform simulations of the model presented in Sect. 2.

Note that the simulation is characterized by four (\(+1\) timescale, if the market is stable) timescales:

-

1.

t, over which trading take place.

-

2.

\(\tau _{\textrm{NT}}\), over which noisy order flow volatility fluctuates. This is a parameter which the modeler has to fix.

-

3.

\(\tau _\text {fast}\), over which the fast dynamics of price impact reaches the stationary regime. This parameter controls the fast dynamics of price impact, given by Eq. (6), which has been analyzed in Sect. 2.1.

-

4.

\(\tau _{\text {rev}}\), over which the market maker updates his belief about fundamental price volatility. This is a parameter which the modeler has to fix.

-

5.

\(\tau _{\text {slow}}\), over which the belief of the market maker converge in distribution, if the market is stable. In this case, this parameter controls the slow dynamics of market maker’s belief, given by Eq. (10) analyzed in Sect. 2.2.

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Vodret, M., Mastromatteo, I., Tóth, B. et al. Microfounding GARCH models and beyond: a Kyle-inspired model with adaptive agents. J Econ Interact Coord 18, 599–625 (2023). https://doi.org/10.1007/s11403-023-00379-8

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11403-023-00379-8