Abstract

In this interdisciplinary, conceptual article with implications in marketing financial products and services, we study real estate and capital markets characterized by a predatory paradigm and economic agents’ dark financial profiles (DFPs). These are estimated by three orthogonal components—disconnection, irrationality, and deceit. We identify the best interactional patterns of borrower-lender profiles, ones that expectedly minimize the risk of default. We resort to discretized, predator–prey Lotka–Volterra equations where lenders act as predators and borrowers as prey, incorporating market trends and learning effects. To mathematically operationalize our framework, we use combinatorics with high, medium, and low levels of the three components of DFPs. We find 27 salient lender-borrower interactional scenarios and observe three different patterns: explosive, conducive, and implosive. Our theoretical findings indicate that equal (ir)rationality (in financial terms) between lenders and borrowers is a necessary but insufficient condition to maintain harmonious, long-term relationships. We use eutectic theory to map the agents’ profiles by introducing another variable: Expected return [E(Rp)] versus risk [σ], using the Capital Asset Pricing Model (CAPM) as a base. We find six market segments: the inactive predators and prey, the loose, the greedy, the vulnerable, and the stable. We identify the optimal combination of borrowers–lenders interaction under risk, given market trends and learning effects. We propose a path for future research that would see the application of analytical tools such as factor analysis, k-means clustering algorithm, χ2 and non-parametric Kruskal–Wallis and Dunn’s multiple comparison tests to verify differences among the hypothesized segments.

Similar content being viewed by others

Notes

Developed by the Fair Isaac Corporation to assess credit worthiness.

In marketing, this could be approximated as a life-stage line, as US consumers typically improve their standards of living with age, and tend to invest more accordingly.

The well-established formula is: E(Rp) = Rf + β · (ERm − Rf) where: E(Rp) = expected return of the investment portfolio, Rf = risk-free rate, β = beta of the investment, ERm = expected market return, (ERm − Rf) = market risk premium.

These numbers are like the well-known Pareto 80–20 ratio.

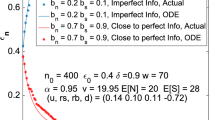

Note that the model cannot go beyond the limits set by the semi-dotted vertical lines all around the figure. For example, on the far left, the excess of k will lead to too many predatory behaviors, which will eventually mean the death of all the prey, which are the predators’ source of survival. On the far right, as k approaches zero, the population of predators is overwhelmed by the growth of the prey behaviors, which will exhaust all resources that sustained the prey’s lives. At both extremes, the economic ecosystem crashes.

Of note, borrowers are not consumers, at least not until they buy a product. Hence, this article is about borrowers’ behaviors, not consumers’ behaviors.

References

Al-Weshah, G. 2017. Marketing intelligence and customer relationships: Empirical evidence from Jordanian banks. Journal of Marketing Analytics 5 (3/4): 141–152.

Andrade, E.B., and T..-H.. Ho. 2009. Gaming emotions in social interactions. Journal of Consumer Research 36 (4): 539–552.

Argo, J.J., D.W. Dahl, and K. White. 2011. Deceptive strategic identity support: Misrepresentation of information to protect another individual’s public self-image. Journal of Applied Social Psychology 41 (11): 2753–2767.

Baker, M., and J. Wurgler. 2007. Investor sentiment in the stock market. Journal of Economic Perspectives 21 (2): 129–151.

Bandura, A. 1977. Social learning theory. Englewood Cliffs: Prentice-Hall.

Barber, B.M., and T. Odean. 2001. Boys will be boys: Gender, disconnected, and common stock investment. The Quarterly Journal of Economics 116 (1): 261–292.

Bargh, J.A., and E.L. Williams. 2006. The automaticity of social life. Psychological Science 15: 1–4.

Baumeister, Roy F., and Todd F. Heatherton. 1996. Self-regulation failure: An overview. Psychological Inquiry 7 (1): 1–15.

Bertrand, J., and L. Weill. 2021. Do algorithms discriminate against African Americans in lending? Economic Modelling 104: 105219.

Bianco, K. 2008. The subprime lending crisis: Causes and effects of the mortgage meltdown. New York: Wolters Kluwer Law and Business.

Bollinger, B., and S. Yao. 2018. Risk transfer versus cost reduction on two-sided microfinance platforms. Quantitative Marketing & Economics 16 (3): 251–287.

Bossaerts, P., S. Suzuki, and J.P. O’Doherty. 2019. Perception of intentionality in investor attitudes towards financial risks. Journal of Behavioral and Experimental Finance 23: 189–197.

Boush, D.M., M. Friestad, and P. Wright. 2015. Deception in the Marketplace: The psychology of deceptive persuasion and consumer self-protection. New York: Routledge.

Bowlby, J. 1973. Attachment and loss. Separation: Anxiety and anger, vol. 2. New York: Basic Books.

Capozza, D.R., and R. Van Order. 2011. The great surge in mortgage defaults 2006–2009: The comparative roles of economic conditions, underwriting and dark financial profile. Journal of Housing Economics 20 (2): 141–151.

Castellano, R., and R. Cerqueti. 2018. A theory of misperception in a stochastic dominance framework and its application to structured financial products. IMA Journal of Management Mathematics 29 (1): 23–37.

Colander, D., H. Föllmer, A. Haas, M.D. Goldberg, K. Juselius, A. Kirman, T. Lux, and B. Sloth. 2009. The financial crisis and the systemic failure of academic economics. Critical Review 21 (2–3): 249–267.

Couch, J.F., M.D. Foster, K. Malone, and D.L. Black. 2011. An analysis of the financial services bailout vote. CATO Journal 31 (1): 119–128.

Crosno, J., R. Dahlstrom, and S.B. Friend. 2020. Assessments of equivocal salesperson behavior and their influences on the quality of buyer-seller relationships. Journal of Personal Selling and Sales Management 40 (3): 161–179.

Dallery, T., and T. van Treeck. 2011. Conflicting claims and sense of fairness adjustment processes in a stock-flow consistent macroeconomic model. Review of Political Economy 23 (2): 189–211.

Del Negro, M., and C. Otrok. 2007. 99 Luftballons: Monetary policy and the house price boom across US states. Journal of Monetary Economics 54: 1962–1985.

DePaulo, B.M., D.A. Kashy, S.E. Kirkendol, M.M. Wyer, and J.A. Epstein. 1996. Lying in everyday life. Journal of Personality and Social Psychology 70 (5): 979–995.

Desarbo, W.S., and E.A. Edwards. 1996. Typologies of compulsive buying behavior: A constrained clusterwise regression approach. Journal of Consumer Psychology 5 (3): 230–262.

Dubina, I.N., E.G. Carayannis, and D.F.J. Campbell. 2012. Creativity economy and a crisis of the economy? Coevolution of knowledge, innovation, and creativity, and of the knowledge economy and knowledge society. Journal of the Knowledge Economy 3 (1): 1–24.

Dutting, P., Z. Feng, H. Narasimhan, D. Parkes, and S.S. Ravindranath. 2019. Optimal auctions through deep learning. In International conference on machine learning, 1706–1715. https://arxiv.org/abs/1706.03459

Fama, E. 1970. Efficient capital markets: A review of theory and empirical work. Journal of Finance 25 (2): 383–417.

Frame, S., A. Lehnert, and N. Prescott. 2008. A snapshot of mortgage conditions with an emphasis on subprime mortgage performance. Federal Reserve. http://www.federalreserveonline.org/pdf/mf_knowledge_snapshot-082708.pdf.

Hain, J.S., B.N. Rutherford, and J.F. Hair Jr. 2019. A taxonomy for financial services selling. Journal of Personal Selling and Sales Management 39 (2): 172–188.

Herzenstein, M., S. Sonenshein, and U.M. Dholakia. 2011. Tell me a good story and I may lend you money: The role of narratives in peer-to-peer lending decisions. Journal of Marketing Research (JMR) 48: S138–S149.

Huang, Y., G. Kou, and Y. Peng. 2017. Nonlinear manifold learning for early warnings in financial markets. European Journal of Operational Research 258 (2): 692–702.

Huck, N., O. Mesly, and K. Afawubo. 2022. Who understands the US housing market? Applied Economics Letters. https://doi.org/10.1080/13504851.2022.2128174.

Iacoviello, M. 2008. Household debt and income inequality, 1963–2003. Journal of Money, Credit and Banking 40 (5): 929–965.

Jones, T., and G.S. Sirmans. 2015. The underlying determinants of residential mortgage default. Journal of Real Estate Literature 23 (2): 167–206.

Jones, T., and G.S. Sirmans. 2019. Understanding subprime mortgage default. Journal of Real Estate Literature 27 (1): 27–52.

Kamimura, A., G.F. Burani, and H.M. França. 2011. The economic system seen as a living system: A Lotka-Volterra framework. Emergence: Complexity and Organization 13 (3): 80–93.

Kenrick, D.T., V. Griskevicius, S.L. Neuberg, and M. Schaller. 2010. Renovating the pyramid of needs: Contemporary extensions build upon ancient foundations. Perspectives on Psychological Science 5 (May): 292–314.

Lee, C.J., and E.B. Andrade. 2011. Fear, social projection, and financial decision making. Journal of Marketing Research (JMR) 48: S121–S129.

Lisjak, M., and A.Y. Lee. 2014. The bright side of impulse: Depletion heightens self-protective behavior in the face of danger. Journal of Consumer Research 41 (1): 55–70.

Maas, P., and A. Graf. 2008. Customer value analysis in financial services. Journal of Financial Services Marketing 13 (2): 107–120.

Markowitz, H. 1952. Portfolio selection. Journal of Finance 7 (1): 77–91.

Mesly, O. 2015. Creating models in psychological research. USA: Springer International Publishing.

Mesly, O. 2020. Consumer spinning: Zooming on an atypical consumer behavior. Journal of Macromarketing 41 (2): 25–31.

Mesly, O., and N. Huck. 2022. Dark financial profile leading to debt traps—A theoretical framework. International Journal of Consumer Studies 47 (1): 419–433.

Mesly, O., and N. Huck. 2023. Financial market paradigm shifts and consumer financial spinning. Journal of Economic Issues 23 (4): 1062–1078.

Mesly, O., H. Mavoori, and N. Huck. 2022a. The role of financial spinning, learning, and predation in market failure. Journal of the Knowledge Economy 14 (1): 517–543.

Mesly, O., M.M. Petrescu, and A. Mesly. 2022b. Terminology matters: A review on the concept of economic predation. Journal of Economic Issues 56 (4): 859–987.

Mian, A.R., and A. Sufi. 2009. House prices, home equity-based borrowing, and the US household leverage crisis. NBER Working Paper Series. Working Paper 15283. http://www.nber.org/papers/w15283.

Mikulincer, M., and P.R. Shaver. 2007. Attachment in adulthood–structure, dynamics, and change. New York: The Guilford press.

Nosi, C., A.C. Pratesi, and A. D’Agostino. 2014. A benefit segmentation of the Italian market for full electric vehicles. Journal of Marketing Analytics 2 (2): 120–134.

Peltier, J.W., A.J. Dahl, and J. Schibrowsky. 2016. Sequential loss of self-control: Exploring the antecedents and consequences of student credit card debt. Journal of Financial Services Marketing 21 (3): 167–181.

Plutchik, R., and S.B. Platman. 1975. Personality connotations of psychiatric diagnoses. Journal of Nervous and Mental Disease 165: 418–422.

Prasolov, A.V. 2016. Some quantitative methods and models in economic theory. New York: Nova Science Publishers Inc.

Rapp, A., D.G. Bachrach, N. Panagopoulos, and J. Ogilvie. 2014. Salespeople as knowledge brokers: A review and critique of the challenger sales model. Journal of Personal Selling and Sales Management 34 (4): 245–259.

Rawn, C.D., and K.D. Vohs. 2011. People use self-control to risk personal harm: An intra-interpersonal dilemma. Personality and Social Psychology Review 15 (3): 267–289.

Roseboom, P.H., S.A. Nanda, V.P. Bakshi, A. Trentani, S.M. Newman, and N.H. Kalin. 2007. Predator threat induces behavioral inhibition, pituitary-adrenal activation and changes in amygdala CRF-binding protein gene expression. Psychoneuroendocrinology 32: 44–55.

Roy, S., and D.M. Kemme. 2012. Causes of banking crises: Deregulation, credit booms and asset bubbles, then and now. International Review of Economics and Finance 24: 270–294.

Salmon, T.C. 2001. An evaluation of econometric models of adaptive learning. Econometrica 69 (6): 1597–1628.

Samuelson, P.A. 1971. Generalized Predator-Prey oscillations in ecological and economic equilibrium. Proceedings of the National Academy of Science 68 (5): 980–983.

Seiler, M., V. Seiler, and M. Lane. 2012. Mental accounting and false reference points in real estate investment decision making. Journal of Behavioral Finance 13 (1): 17–26.

Sengupta, J., D.W. Dahl, and G.J. Gorn. 2002. Misrepresentation in the consumer context. Journal of Consumer Psychology 12 (2): 69–79.

Sharpe, W.F. 1964. Capital asset prices: A theory of market equilibrium under conditions of risk. Journal of Finance 19: 425–442.

Shiller, R.J. 2005. Irrational exuberance. New York: Crown Publishing Group, A Division of Random House Inc.

Shultz, C.J., and M.B. Holbrook. 2009. The paradoxical relationships between marketing and vulnerability. Journal of Public Policy and Marketing 28 (1): 124–127.

Siebert, R.B., and M.J. Seiler. 2022. Why do buyers pay different prices for comparable products? A structural approach on the housing market. Journal of Real Estate Finance & Economics 65 (2): 261–292.

Song, F., and A.V. Thakor. 2010. Financial system architecture and the co-evolution of banks and capital markets. The Economic Journal 120: 1021–1055.

Tang, T.-S. 2010. The costs of lead bank–distressed borrower relationships: Evidence from commercial lending in Taiwan. The Service Industries Journal 30 (9): 1549–1563.

Trivedi, M. 1999. Using variety-seeking-based segmentation to study promotional response. Journal of the Academy of Marketing Science 27 (1): 37.

Todorov, A., and A.D. Engell. 2008. The role of the amygdala in implicit evaluation of emotionally neutral faces. Scan 3: 303–312.

Veld, C., and Y.V. Veld-Merkoulova. 2008. The risk perceptions of individual investors. Journal of Economic Psychology 29 (2): 226–252.

Verplanken, B., and A. Sato. 2011. The psychology of impulse buying: An integrative self-regulation approach. Journal of Consumer Policy 34 (2): 197–210.

Wijeratne, A.W., F. Yi, and J. Wei. 2009. Bifurcation analysis in the diffusive Lotka-Volterra system: An application to market economy. Chaos, Solitons and Fractals 40 (2): 902–911.

Yu, J. 2016. Tropical combinatorics and applications. NSF Award Abstract #1600569. https://www.nsf.gov/awardsearch/showAward?AWD_ID=1600569. Accessed 5 Mar 2021.

Acknowledgements

We thank professor Silvester Ivanaj for his assistance in preparing this article.

Funding

The authors have no relevant financial or non-financial interests to disclose.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors have no conflicts of interest to declare that are relevant to the content of this article.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix: Summary of the interactional DFP scenarios

Appendix: Summary of the interactional DFP scenarios

See Table 3.

The scenario set by [o = O, r = R, d < < D] offers the best possibility among the six scenarios of the mutually beneficial interactions. Both the lender and the borrower evolve, and they evolve equally and with optimal mutual benefits.

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Mesly, O., Mavoori, H. Mapping borrowers’ and lenders’ interactions according to their dark financial profiles. J Market Anal (2023). https://doi.org/10.1057/s41270-023-00263-1

Revised:

Accepted:

Published:

DOI: https://doi.org/10.1057/s41270-023-00263-1