Abstract

The economic impact of the COVID-19 pandemic placed many small businesses across the US in financial distress. In response to this, in March 2020 the US government introduced, as part of the CARES Act, the Paycheck Protection Program (PPP) intended to provide relief to small businesses and to preserve jobs during the pandemic. The latter resulted in three waves of funding distributed to small businesses through SBA approved lenders, mainly represented by US banks. By using a panel dataset of 4610 banks over the period Q1 2019–Q4 2020 and by employing a difference-in-differences approach (DiD), I investigate whether participation in the Paycheck Protection Program affected community banks’ credit risk-taking behaviour in the post-PPP period, compared to their non-community banking counterparts in the US. I find that the Paycheck Protection Program led community banks to decrease their risk appetite outside of the program relative to non-community banks, consistent with their greater exposure to the commercial real estate sector, heavily hit by the pandemic. My results are robust to a battery of robustness tests and identification strategies. In this research article, I offer novel evidence on the indirect impact of the Paycheck Protection Program as a government-funded stimulus program administered through banks by investigating the indirect effect of the Paycheck Protection Program on the risk-taking of US community banks that dominate lending of PPP loans as a result of their competitive advantage in soft information-intensive small business lending. Such evidence is informative to policymakers as they weigh the merits of various program options to combat the economic damage imposed by the COVID-19 pandemic and as they consider the design of economic stimulus programs in response to future economic crises.

Similar content being viewed by others

1 Introduction

Responding to the unforeseen challenges created by the COVID-19 pandemic has placed pressure on businesses and governments across the world. Within this context, adverse economic impacts, due to enforced restrictions implementing social distancing and isolation, have led several non-essential businesses to significantly reduce their operations or close permanently. Due to the recent nature of the pandemic, some of the short and long-term effects are still largely unknown. In the specific context of the US, unemployment figures illustrate the severity of the pandemic and the impact it had upon businesses. In this regard, the US Bureau of Labor Statistics (2020) reports that the US unemployment rate rose from 4.5% in March 2020, shortly before the crisis, to 14.7% in April 2020. The latter figure represents the highest rate and largest over-the-month increase in the history of the US (US Bureau of Labor Statistics, 2020). As such, these figures not only have anticipated the widespread and rapid emergence of the pandemic, but also have signalled the upcoming and unpredictable economic disruption on a large-scale in the US. However, the degree to which businesses have been affected up to this point is not equal. Indeed, there has been a large disparity between businesses of different sizes and the impact experienced as a result of the pandemic. In this regard, small businesses were hit hard by the COVID-19 crisis (Bartik et al. 2020), with employment declining by more than 18% at firms with under 50 employees by April 2020. As a result, financial aid was needed, particularly for small businesses, in order to safeguard and preserve their performance and continuity under stressed scenarios.

In response to the pandemic, the US government introduced the Paycheck Protection Program (PPP) that represents one component of the 2020 Coronavirus Aid Relief and Economic Security (CARES) Act introduced in March 2020. The Paycheck Protection Program (PPP) was intended to provide relief to small businesses and to preserve jobs during the COVID-19 pandemic. The PPP represents a unique setting in that it is a government-funded stimulus program that is not directly intended for, but is administered through, banks. PPP loans charged only 1% interest with maturities of two to five years. Participating banks receive fees upon origination of PPP loansFootnote 1 and the latter are guaranteed by the US government through the Small Business Association (SBA), effectively making them risk-free.Footnote 2 The Paycheck Protection Program was agreed towards the end of Q1 2020 and PPP loans were available for distribution from the beginning of Q2 2020. Due to the noticeably larger impact on small businesses, the intention of the program was to supply subsidized credit, guaranteed by the Small Business Administration (SBA), to support small businesses to survive during the pandemic-associated lockdowns. Indeed, PPP loans were designed to provide small firms with an incentive to retain workers on the payroll, up to the point that PPP loans could also be forgiven if all employees’ retention criteria are met, and the funds are used for eligible expenses. To facilitate the distribution of PPP loans, the latter were administered and disbursed mainly by small, community US banks (Bartik et al. 2020; Li and Strahan 2020).

Although the existing studies investigated whether the program has achieved its intended objectives of job preservation and mitigation of the negative economic effects of the pandemic (Barrios et al. 2020; Autor et al. 2022a, 2022b; Granja et al. 2022), the extant literature has not exhaustively addressed whether the program resulted in consequences at the bank level. In this paper, I provide novel evidence on the consequences of the PPP for banks by examining whether participation in the program is associated with differential risk-taking of community banks outside of the PPP, compared to their larger non-community banking counterparts. Such evidence is informative to policymakers as they weigh the merits of various program options to combat the economic damage imposed by the COVID-19 pandemic and as they consider the design of economic stimulus programs in response to future economic crises.

I tackle this research question by undertaking a causal identification approach to examine the effects of the PPP on the risk-taking behaviour of community banks relative to their larger non-community banks operating in the US. While theoretically, a priori, I should expect to find no significant differential behaviour towards risk-taking between community and non-community banks, as both the former and the latter would be driven by the same perceived increased risk-bearing capacity resulting from PPP-induced reduction in bank risk ratios, empirically I do. Indeed, ideally, all banks (of all sizes) might be pushed to increase risk-taking outside of the program as a result of PPP participation due to the risk-free treatment of PPP loans. However, in the run-up to the pandemic, US small community banks had higher exposures in commercial real estate (CRE) portfolios and have suffered as a direct result of the pandemic-driven price drop in CRE. Indeed, the COVID-19 crisis hit the commercial real estate sector hard in the US. In this regard, the International Monetary Fund noted, in its May 2021 report on CRE trends, that “the impact of a decline in CRE prices is especially true for small and community banks, which tend to have the highest CRE loan exposures” (Fendoglu 2021). Consequently, the structural shifts in CRE demand pose considerable uncertainly around the outlook for the sector and suggest that further price declines may be possible, with a severe negative impact on community banks’ CRE loans, revenues, and capital. Therefore, greater exposure of community banks to CRE lending might have potentially incentivized lower risk-taking outside of the program due to the prospected negative impacts nurtured by the suffering of the CRE sector. In contrast, larger non-community banks had been more prudent in their CRE lending compared to the period prior to the 2007–2008 global financial crisis, with their exposures declining notably when the pandemic broke out. Therefore, lower exposure of non-community banks to CRE lending might have potentially incentivized greater risk-taking outside of the program due to PPP-induced reduction in bank risk sensitivity from a risk ratio standpoint.

To address my research question I exploit a unique dataset comprising 4610 banks, observed on a quarterly basis, whose data have been collected from Call Reports in the period Q1 2019–Q4 2020 to investigate the impact of the Paycheck Protection Program upon the credit risk-taking behaviour of community US banks, compared to their non-community counterparts. Following Bose et al. (2021), in order to rule out the possibility that omitted variables and reverse causality can affect my estimation results, I test for this by using three different identification strategies. Firstly, I employ a difference in differences (DiD) approach to examine the impact of the Paycheck Protection Program on the risk appetite of community vs non-community banks since the former’s relatively greater exposure to CRE lending might have decreased their incentive to take on additional risk outside of the program. Therefore, to the purpose of my difference in differences (DiD) approach, I construct my treated and control groups on this basis, where community banks represent my treated group while non-community banks reflect my control group. Secondly, I employ an instrumental variable approach and use two-stage least squares (2SLS) regression analysis to address potential endogeneity across control variables. Thirdly, I conduct coarsened exact matching (CEM), a method for improving the estimation of causal effects by reducing imbalance in covariates between treated and control groups, and propensity score matching (PSM) between community and non-community banks to show no significant differences between these two groups in terms of other observable variables in the pre-PPP period.

To the best of my knowledge, this is the first study that investigates the impact of the Paycheck Protection Program on bank credit risk-taking behaviour through the lens of US community banks. I am aware of only one study by Ballew et al. (2022) that shows that the extent of banks’ PPP participation is associated with relatively greater risk-taking outside of the program since PPP participation involves the expansion of risk-free loans which receive a zero-risk weight in the determination of risk-weighted assets and does not require loan loss provisions or capital. This mechanically reduces bank risk ratios and incentivizes greater risk-taking outside of the program, even if the actual risk level remains constant (FDIC, 2020). However, my paper differs from Ballew et al. (2022) as I investigate the influence of PPP participation on the risk-taking outside of the program of US community banks, main actors in the disbursement and the administration of PPP loans, compared to their non-community banking counterparts.

To preview my findings, I provide novel evidence that US community banks decrease their risk appetite relative to their non-community banking counterparts after the introduction of the Paycheck Protection Program.Footnote 3 Indeed, I find that the extent of community banks’ PPP participation is associated with relatively lower risk-taking outside of the program, consistent with their greater exposure to the commercial real estate sector when the pandemic went off.

Overall, I believe addressing this research question is of crucial importance for policy makers in order to draw appropriate conclusions on the direct and indirect effects of the PPP to consider the design of future stimulus programs. Moreover, my evidence is of interest to bank regulators that monitor bank risk-taking as my findings indicate that PPP participation is associated with changes in bank risk appetite related to bank size. Therefore, regulators should consider bank participation in the program as part of their ongoing monitoring procedures. Finally, the extant literature highlights heterogeneity in bank risk-taking responses based on the design of direct stimulus programs (Rodnyansky and Darmouni 2017; Chakraborty et al. 2020). I contribute to extending this literature by investigating an important type of stimulus package, i.e., one that is administered through, but not intended for, banks and its indirect effects at the bank level. I therefore present my findings as a spur to future research aimed at identifying the indirect channels through which government-funded stimulus programs result in consequences at the bank level.

The remainder of this paper is organised as follows. In Sect. 2, I provide detailed information on the US Paycheck Protection Program. In Sect. 3, I review the relevant literature and develop my hypothesis. In Sect. 4, I introduce the data. In Sect. 5, I present the empirical methodology and the variables used. In Sect. 6, I discuss the results. In Sect. 7, I provide a battery of robustness tests. Lastly, in Sect. 8, I conclude.

2 The CARES Act and the Paycheck Protection Program (PPP)

The CARES Act was introduced on Tuesday 24th March 2020 by the US government in response to the effects of the COVID-19 pandemic across the US. The Act authorizes over $2 trillion dollars of outlays intended to provide emergency assistance for individuals, families, and businesses hit by the COVID-19 pandemic. The CARES Act provides a source of liquidity for businesses, incentives to keep workers employed, and other relief to help individuals and businesses withstand the impacts of the pandemic. The nature of COVID-19 makes comparisons with other global crises impossible (Fernandes 2020). Contrasting to the last 2007–2008 financial crisis, a much larger share of Federal Reserve interventions involves directed support to the real economy, involving joint operations with the Treasury Department, providing various kinds of first-loss protection as authorized under the CARES Act. The CARES legislation includes several temporary reversals of the Dodd-Frank Act’s limitations on uses of the Treasury Department’s Exchange Fund and the FDIC’s powers to increase bank guarantees (Jackson and Schwarcz 2020).Footnote 4

The CARES Act originally allocated $800 billion for corporate loans to small- and mid-sized businesses. The Paycheck Protection Program (PPP) is one component which was initially allocated $349 billion for the distribution of PPP loans. The demand for PPP loans was so enormous that the original $349 billion was exhausted within two weeks and there were no more funds to be allocated by April 16, 2020. During this first round of funding the money was allocated through the SBA to banks on a first come first served basis and demand quickly exceeded supply. This led the initial figure to be increased to $933 billion as a result of a second and third wave of funding, solely for PPP loans, which were available to claim until March 31, 2021. More specifically, in the second wave of funding the Congress added more than $300 billion to the program on April 27, 2020. The extension of the program provided new categories of loans; these allowed a second PPP loan round (Second Draw) for businesses that had already used their first PPP loans. This Second Draw also involved an opportunity for small businesses that did not receive their First Draw during the first round of PPP loans to receive it as a result of the allocation process being first come first served. In order to be eligible for a Second Draw PPP loan, a small business must have 300 employees or fewer and must be able to prove that they experienced at least a 25% reduction in gross revenues for any one quarter in 2020, compared to the equivalent quarter in the previous year. After this second wave of PPP loans ran out in August 2020, the Congress made a third and final round of funding of $284 billion available up until March 31, 2021, through The Consolidated Appropriations Act (CAA). Overall, these three rounds of PPP loans resulted in a package of total $933 billion of PPP loans made available to support small businesses’ survival in the marketplace. Furthermore, through the CAA, the process of applying for forgiveness for a loan less than $150,000 has been simplified. The representative of the loan must sign and submit to the lending institution a certification that lists the number of employees they were able to retain as a result of the PPP loan disbursed, the amount of the loan spent on payroll costs and the total value of the loan (MGO 2021).

PPP loans aim to provide an incentive for small businesses to retain workers on the payroll. If all employee retention criteria are met and the funds are used for eligible expenses, the SBA will forgive the loan. The SBA (2020) outlines that, in order to apply for loan forgiveness, borrowers of loans must ensure that employee and compensation levels are maintained, at least 60% of the proceeds are spent on payroll costs, and the remainder are used for other eligible expenses. Some examples of eligible expenses provided by the SBA (2020) include mortgage interest, rent, utilities, and worker protection costs related to the pandemic, among others.Footnote 5 Businesses are eligible for PPP loans if they have 500 employees or less or if they operate within a specific industry and meet the SBA employee-based size standards for that industry (Federal Register 2020). PPP loans are permitted to be sold in the secondary market any time after the loan has been fully disbursed. In order to obtain a PPP loan, no collateral or personal guarantees are required, and neither the SBA nor participating lenders will charge the recipients any fees in relation to the loan (SBA, 2020). The interest rate on PPP loans is 1%, which was deemed appropriate due to the low cost of funds for borrowers and as an attractive rate for lenders, relative to the cost of funding for comparable maturities. Any PPP loans issued prior to June 5, 2020, have a maturity of 2 years and any PPP loans issued after this date have a maturity of 5 years. Borrowers will not have to make any payments for the first six months following the date of disbursement, however interest will accrue during this period. The SBA will pay lenders fees for processing PPP loans in the following amounts: 5% for loans of no more than $350,000, 3% for loans of more than $350,000 and less than $2,000,000, and 1% for loans of at least $2,000,000 (Federal Register 2020).

Participating lenders can provide PPP loans to successful applicants which are 100% guaranteed by the SBA. The CARES Act also requires that PPP loans receive a zero percent risk weighting in relation to banks’ risk-based capital requirements. Therefore, the zero-risk weight attached to PPP loans implies that more regulatory capital is freed up for banks to add risker assets to their balance sheets. Indeed, Section 1102 of the CARES Act requires banking organizations to apply a zero percent risk weight to PPP loans guaranteed by a US government agency for purposes of the banking organization’s risk-based capital requirements, thus neutralizing the regulatory capital effects of participating in the Paycheck Protection Program (PPP).Footnote 6 However, banks face a tangible equity capital requirement that imposes a constraint on the bank to engage in further risky lending, even if the zero percent risk weighting on PPP loans under regulatory capital rules does not. Specifically, according to Basel III banking regulations, a non-risk-based leverage ratio (LR) requirement co-exists alongside the risk-based capital framework with the aim to “restrict the build-up of excessive leverage in the banking sector to avoid destabilising deleveraging processes that can damage the broader financial system and the economy”.Footnote 7 This leverage ratio, computed as the ratio between tier 1 capital divided by non-risk-weighted total assets, is intended to reinforce the risk-based capital requirements with a simple, non-risk-based “backstop” (BIS, 2017). Therefore, under the Paycheck Protection Program (PPP), while risk-based capital ratios do not impose a constraint for banks to add risker assets to their balance sheet due to the zero percent risk weighting on PPP loans, the leverage ratio, in contrast, constrains bank ability to engage in further risky lending as the latter requires banks, bound by the LR, to hold more equity capital in a context where banks are expected to maintain a leverage ratio in excess of 3% under the Basel III capital framework.

3 Influence of the PPP on community banks: related literature and hypothesis development

Many researchers have studied bank size and the resulting impact on the provision of credit, illustrating that lending practices differ greatly between small and large banks. Cole et al. (1999) investigate the loan approval process across banks of different sizes, finding that, for large banks, decisions are primarily based on quantitative hard information extracted from financial statements. To the contrary, small banks’ lending decisions to extend credit rely more on qualitative soft information and on the existence of a prior firm-bank credit relationship. Findings by Stein (2002) support this idea, indicating that information type can be an explanatory factor in banks choosing to extend credit, and that soft information is better processed and understood by small banks. Reliance on hard information that can quickly be drawn from financial statements allows larger banks to make rapid lending decisions, which suits their more transactional customer base. Studies based on information type and its communicability indicate that soft information is not easily conveyed through typical channels used in large banking organisations. Instead, soft information is much more suited to face-to-face communication (i.e., ‘human touch’), inherently associated with smaller banks, such as US community banks. Far-reaching services and large volumes of customers make soft information extremely difficult to be communicated along the large hierarchical bank without dilution of its informative content. The lack of ability for large banks to be able to process soft information is consistent with findings of Berger and Udell (2002) who suggest that large banks shy away from small business lending due to its reliance on the production of soft information that is incongruent with their large organizational structure. As a result, small businesses are less likely to be granted credit by larger banks, since the latter would be unable to form deep and long-lasting credit relationship with small firms. Berger et al. (1995) further support this theory, providing evidence suggesting that large banks allocate smaller proportions of their assets to small business loans in comparison to smaller banks. As the Paycheck Protection Program’s ultimate goal is to provide access to credit for small businesses, it could be expected that US small, community banks, with pre-existing small business lending relationships, are directly impacted by the program in serving these eligible small businesses through the disbursement and the administration of PPP loans, compared to larger non-community banks.

This paper contributes to the recent existing studies investigating the impact of the Paycheck Protection Program in the US on PPP-distributing banks and PPP loan-receiving borrowers. In this regard, Anbil et al. (2023) find that funding from the Paycheck Protection Program Liquidity Facility (PPPLF) established by the Federal Reserve boosted PPP lending at smaller banks and greater certainty about funding availability boosted PPP lending at larger community banks during the period from April 2020 to June 2020. Lopez and Spiegel (2023) document that increased bank participation in the PPP and the PPPLF programs substantively encouraged growth in SME lending at the outset of the pandemic period and that the sensitivity of lending growth to participation in the PPP program was roughly equal across all banks and that there was a large discrepancy by size in the importance of the PPPLF program, with a significant role for lending growth in PPPLF participation among small and medium-sized banks, but an insignificant role for that program among large banks. Cassell et al. (2023) find that lender type significantly impacts how the benefits of the PPP are distributed and how dramatically they differ in their sensitivities lending practices to communities with poverty and minority status. Filomeni and Querci (2023) provide evidence on the effectiveness of the Biden-Harris reforms in reducing the racial bias on the Paycheck Protection Program as they observe an increased volume of PPP loans’ granted amount to minority-owned businesses in the post-Biden-Harris Administration reform period. Deming and Weiler (2023) show that PPP loans went disproportionately toward more job-dense regions in the US, effectively widening existing spatial labour market inequality, and that PPP loans flowed less toward those regions characterized by banking deserts, again reinforcing existing regional inequalities. Kellard et al. (2023) provide evidence of an indirect effect of PPP on private equity and venture capital by showing that firms that were in receipt of PPP loans appeared more attractive to both private equity and venture capital and were more likely to be subject to a takeover than those that were not since this would alleviate capital constraints, making future borrowing easier.

Li and Strahan (2020) analyse the supply of credit under the Paycheck Protection Program. They illustrate how small businesses with existing relationships with small, community banks experience increased accessibility to government-subsidized lending, such as PPP loans. The authors demonstrate that supply of PPP loans reflects of the intensity of relationship lending. They emphasise that banks use relationship lending to develop more detailed and improved information on customers which enables banks to assess the risk of small businesses more accurately. This improved customer knowledge and risk assessment allow banks to better manage their overall level of credit risk. Li and Strahan (2020) provide empirical evidence showing that lending to small businesses by small, community banks, mostly relying on soft information-intensive relationship banking, increases dramatically in April 2020 and that almost all this lending growth relates to their participation in the PPP program. Such findings are further corroborated by Glancy (2023) who demonstrates the importance of bank relationships for prompt access to PPP loans by showing that half of banks' PPP loans went to borrowers within 2 miles of a branch, mostly driven by relationship lending, and that relationship borrowers were able to receive credit 5–9 days earlier than other borrowers from the same bank. Bartik et al. (2020) document the supply and demand of PPP loans and describe how the Paycheck Protection Program’s take-up was largely dictated by banks’ lending decisions, concluding that the delivery of PPP loans via banks limited the access to PPP funds for some small businesses. Banks’ decisions to extend credit were not based on the social benefit a small business would achieve from obtaining a PPP loan. However, opting for a strategy where businesses most in need were targeted first, would have significantly slowed down the rate at which loans could be distributed to all businesses (Bartik et al. 2020). Echoing findings from Li and Strahan (2020), they stress the importance of pre-existing relationships between businesses and banks providing PPP loans. Indeed, they indicate that a pre-existing relationship with a lending bank prior to the program is a key determinant of the extent the small business will benefit from the PPP program. Bartik et al. (2020) also provide evidence of the observed lower PPP loans’ approval rates and volumes among the largest US banks. In this regard, the authors suggest that the domination of small, community banks in granting PPP loans is associated with their competitive advantage over nationwide banks in small business lending, since the latter are characterized by organizational complexity and face more severe communication frictions due to the greater distance between their headquarters and local branches (Berger et al. 2005; Filomeni et al. 2020, 2021; Filomeni et al. 2023a, b). Indeed, small banks’ decisions to extend credit are largely based on soft information-intensive relationship banking. The close bank-firm lending relationships established between small banks and small businesses are consistent with the lending patterns of PPP loans. As a result of a pre-existing relationship with a customer, small community banks are likely to benefit from both the hard and soft information collected on their borrowers throughout the life of the bank-firm relationship, even more during crisis times (Casu et al. 2022). Indeed, existing evidence concurs that PPP lending differs greatly between small and large banks due to the nature of PPP loans, relying on relationship lending and pre-existing lending relationships between small businesses served by small banks. Balyuk et al. (2021) highlight the presence of intermediary supply effects, that is, bank financial intermediaries shape the supply of PPP financing. Their evidence suggests that larger firms are likely to gain early access, but the pro-large firm effects are attenuated in small banks and when firms have prior banking relationships, consistent with the large literature in banking suggesting that small firms benefit from pairing up with small banks (e.g., Stein 2002; Berger et al. 2005, among others). Furthermore, the evidence that small banks play a much larger role in small business lending during the pandemic is further confirmed by the Federal Reserve Bank of San Francisco highlighting that small, community banks were active PPP participants, with almost 35% of their related lending provided through the program that accounted for 25.3%, of small business loans during the pandemic, about a quarter of the total lending to small businesses (Beauregard et al. 2020). Overall, the recent existing literature therefore provides evidence that small, community banks benefit from a competitive advantage over their larger non-community banking counterparts in disbursing PPP loans due to the latter being soft information-intensive. Such evidence is further supported by the Federal Deposit Insurance Corporation (FDIC) that describes community banks as ‘relationship bankers’ who have a close relationship with their customers and special knowledge and expertise of their local communities.

In the Introduction I have discussed that, while theoretically, a priori, I should expect to find no significant differential behaviour towards risk-taking between community and non-community banks, as both the former and the latter would be driven by the same perceived increased risk-bearing capacity resulting from PPP-induced reduction in bank risk ratios, empirically I do. Indeed, ideally, all banks (of all sizes) might be pushed to increase risk-taking outside of the program as a result of PPP participation due to the risk-free treatment of PPP loans. However, in the run-up to the pandemic, US small community banks had higher exposures in commercial real estate (CRE) portfolios and have suffered as a direct result of the pandemic-driven price drop in CRE, in a scenario where community banks with ex-ante higher CRE loan exposures experienced significantly higher CRE non-performing loan ratios and CRE loan charge-off rates, as shown in Fig. 1, panel 1. As CRE loans underperform and the resulting provisioning expenses are higher for community banks with a greater CRE exposure, they experience a stronger decline in pre-provision net revenues and regulatory capital, as shown in Fig. 1, panel 2.

Commercial real estate price decline and bank CRE loans, revenues and capital. Sources Federal Financial Institutions Examination Council Call Reports; MSCI Real Estate; and author calculations (Fendoglu 2021). The panels show the effect of a change in commercial real estate (CRE) prices on banks’ cumulative CRE non-performing loan rate, cumulative CRE net loan charge-off rate, net revenues before provisioning, and total regulatory capital. Banks with high (low) CRE exposure correspond to banks with an ex ante CRE-loans-to-total-assets ratio that is at the 75th (25th) percentile of the distribution of the ratio of CRE loans to total assets (which corresponds to 43(16) percentage points exposure). All estimated effects are statistically significant at 10 percent or less (panels 1a, 1b, and 1c report cumulative effects, for which average p-values are less than 10 percent)

In contrast, large banks have been more prudent in their CRE lending compared to the period prior to the 2007–2008 global financial crisis, with their exposures declining notably. Graphical confirmatory evidence is provided in Fig. 2 showing that larger non-community banks, on average, had lower CRE loan exposures compared to smaller community banks in the US prior to the pandemic and, as such, were less exposed to CRE lending when the pandemic broke out, thus potentially incentivizing their greater risk-taking outside of the program due to the PPP-induced reduction in bank risk sensitivity from a risk ratio standpoint.

Commercial real estate loans in the United States. Sources Call Reports; and author calculations (Fendoglu 2021). Panel 1 shows the ratio of total CRE loans to the sum of total business and CRE loans by US banks. Panel 2 shows total CRE loans made by banks of different sizes, with banks considered as small if their total assets do not exceed $5 billion during the sample period (2001:Q1–2020:Q3), as medium if their total assets exceed $5 billion at least once but do not exceed $100 billion, and as large if their total assets exceed $100 billion at least once. Panel 3 shows the total CRE loans-to-total assets ratio

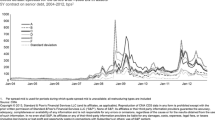

I therefore believe that the risk-free treatment attached to PPP loans, although it provides an incentive for banks to increase their risk-taking, affects US community and non-community banks differently, consistent with their different exposures to the commercial real estate sector in the run-up to the pandemic. Indeed, the commercial real estate (CRE) sector in the United States has been hit hard during the COVID-19 pandemic. Following lockdown measures introduced to contain the spread of the virus and the associated decline in social mobility, the demand for contact-intensive CRE spaces such as traditional brick-and-mortar retail, restaurants, hotels, and offices plunged significantly in 2020. Consequently, CRE transaction volumes and prices, particularly, in the hotel, retail, and office segments, declined sharply, as documented in Fig. 3.

Commercial real estate prices and transaction volumes during the COVID-19 crisis. Sources Green Street Advisors; Real Capital Analytics; and author calculations (Fendoglu 2021). Panel 1 shows the year-over-year percent change in CRE transactions in the United States and other regions. Panel 2 shows the percent change in average CRE prices, based on appraisal values for different CRE segments in the United States and Europe. Latest corresponds to 2020:Q3 or later, depending on data availability

Compared to other regions, the decline in CRE transactions and prices has been more pronounced in the United States making my empirical setting even more appropriate to perform my empirical analysis. The great exposure to the CRE sector made community banks more vulnerable to the pandemic-associated recessionary period and their recognition of projected capital losses led them to adopt a more prudential behaviour towards risk-taking despite the perceived increased risk-bearing capacity stemming from PPP-induced reduction in bank risk ratios.

I therefore expect to find community banks to experience a lesser impact on risk-taking as a result of PPP lending as summarised in the main hypothesis being tested in this paper, related to the effects of the PPP on the risk-taking behaviour of small, community banks outside of the program, compared to their larger non-community counterparts. My discussion of the relationship between bank size and bank risk-taking in the context of the US Paycheck Protection Program can be therefore summarized in my main hypothesis (H) as follows:

H: The Paycheck Protection Program led US community banks to decrease their risk-taking behaviour outside of the program, compared to their non-community banking counterparts.

4 Data and descriptive statistics

Following Li and Strahan (2020), I construct a panel dataset on PPP lending at the bank level, combining information from the Call Reports with information provided by the US Small Business Administration (SBA) on the Paycheck Protection Program. The Call Report data capture bank lending to businesses both on and off the balance sheet. In addition to this, a requirement to report on PPP lending has been added, resulting in Call Reports from Q2 2020 detailing lending under the Paycheck Protection Program. From the Call Report I extract quarterly figures for each bank detailing total assets, total equity, net income, total loans, delinquent loans (30–89 days past due), total deposits, and risk-weighted assets. I conduct this for both 2019 and 2020 to create a dataset comprising 8 quarters and construct my measures of bank risk-taking behaviour and bank-specific control variables from this information. The SBA provides a breakdown of borrowing under the Paycheck Protection Program by state, as well as a list detailing loans in excess of $150,000. Using these breakdowns, I generate a complete list of PPP lending institutions and match this with my Call Report data. I match a total of 5322 lending banks, with my sample period spanning from Q1 2019 to Q4 2020. Out of this sample, I include 4610 banks in my main regression model, due to a number of banks being excluded as a result of missing information on one or more variables. More specifically, I separate banks into two size groups. The first group encompasses small community banks with total assets below $10 billion in any of the quarters of my sample period, according to the FDIC. Indeed, the Federal Deposit Insurance Corporation (FDIC) classifies banks with assets less than US $10 billion as community banks (Cole and Damm 2020). The second group instead comprises larger non-community banks with total assets exceeding (or equal to) $10 billion in any of the quarters of my sample period. My sample includes 5,212 community banks and 110 non-community banks.

Call Reports provide quarterly data on bank’s income statement, balance sheet, loan, deposit, and investment information as well as details of securitisation activities. All commercial banks and related financial institutions in the US are required to file Call Reports at the end of each quarter. The purpose of these reports is to help provide a picture of the financial stability and risk exposure of individual banks, as well as of the US banking industry as a whole. A description of the construction of the model variables, as well as their descriptive statistics is presented in Table 1. The fact that some variables used in the analysis (whose descriptive statistics are displayed in Table 1) show minimum values of zeros derives from a subset of banks in the sample that effectively reported very low loan exposures in their Call Reports, eventually turning to zero in any of the quarters of the sample period.

5 Impact of PPP lending on community banks’ risk-taking: empirical methodology

In this section, I examine the impact of PPP lending on credit risk-taking behaviour of small, community banks in comparison to their larger non-community banking counterparts. To identify the differential impact of PPP lending on bank risk-taking by bank size, I employ a DiD estimation method. I measure bank credit risk-taking behaviour (RWATA) using the ratio of risk-weighted assets to total assets (Avery and Berger, 1991; Shrieves and Dahl 1992; Berger and Udell 1994; Berger 1995; Aggarwal and Jacques 2001; Casu et al. 2011). Shrieves and Dahl (1992) indicate that this measure captures a bank’s allocation of assets across risk categories and the quality of its loans. This is supported by Avery and Berger (1991) who suggest that the relative risk-weights used in the risk-based capital standards framework are associated with risky behaviour and to some extent can predict future performance problems, such as portfolio losses and bank failures. The dependent variable will be the quarterly change in credit risk-taking behaviour (ΔRWATA). Further, I identify community banks following the FDIC that defines community banks as those with less than $10 billion in total assets. I then define a dummy for community bank size, i.e., ‘Community’, which takes value 1 if a bank in any of the quarters of my sample period has total assets below the threshold of $10 billion and 0 otherwise. To test my hypothesis (H), I follow Bose et al. (2021) and estimate the following DiD estimation model:

where \(i\) = 1, 2, …., N refers to the cross section of bank i at time \(t\); \({d}_{{quarter}_{t}}\) are quarterly fixed effects to control for time-specific effects; and \({\varphi }_{i}\) are bank fixed effects to control for time-invariant unobserved heterogeneity at the bank level. X is the vector of explanatory factors at bank-level and \({\varepsilon }_{i,t}\) represents the disturbance term for bank \(i\) in quarter \(t\). \({PPP}_{t}\) is a time dummy which takes value 1 for the period in which PPP loans were available, from Q2 2020 onwards, and 0 for quarters prior to Q2 2020. The DiD estimator \({PPP}_{t}* {Community}_{i,t}\), the main variable of interest, represents the impact of PPP lending on the risk-taking behaviour of US community banks in comparison to their non-community banking counterparts.

In all estimated models, I control for bank-specific characteristics that may influence bank risk-taking other than lending PPP loans. These are incorporated into vector X. Bank size (Size) is measured as the natural logarithm of total balance sheet assets (Mandel et al. 2012). Smaller community banks are more likely to meet the needs of small businesses to a higher standard than larger banks and are likely to have pre-existing relationships with small businesses prior to the PPP program. Larger banks are at a disadvantage in comparison to community banks as the time it will take them to process PPP loan applications is far greater due to their lack of pre-existing knowledge on small business customers. Bank capital (Bank Capital) is measured by the ratio of total common equity to total balance sheet assets (Casu et al. 2011). Laeven and Levine (2009) suggest that diversified owners may advocate more risk-taking due to less of their own personal wealth at risk in the bank. However, Demsetz and Lehn (1985) offer an alternative view, indicating that managers with bank-specific human capital and private benefits of control may, in fact, behave in a risk-averse manner. Return on assets (ROA) is included as a measure of performance and captured by the ratio of quarterly net income to total balance sheet assets. Casu et al. (2011) propose that banks with a low return on assets may engage in risky activities in an attempt to re-establish profitability. Delinquency rate (DR) is measured by the ratio of loans 30–89 days past due to total loans and securitisation attitude (SA) as the ratio of loans over deposits. Following Casu et al. (2011), loan ratio (TLTA) is measured as the ratio of total loans to total assets and reflects the size of a bank’s loan portfolio. A bank with a greater loan portfolio is expected to be less risk averse, as loans are deemed a bank’s major high-risk asset, following Casu et al. (2011) who describe how banks with larger loan portfolios are exposed to a greater degree of credit risk as a result of the risk-weighting associated with non-PPP loans. All time-varying, bank-specific factors are lagged by one quarter to reduce possible simultaneity problems with the dependent variable (Bose et al. 2021; Filomeni et al. 2023a, b). Table 1 reports a description of the model variables, as well as their descriptive statistics. Following Bose et al. (2021), banks with missing information on credit risk-taking behaviour and bank-specific controls are excluded from the sample. In addition, to avoid the effect of outliers driving my results, all variables in the regression model are winsorized at the 1% level. The final panel dataset has an unbalanced structure for 4,610 banks over the period Q1 2019–Q4 2020 at quarterly intervals.

6 Results

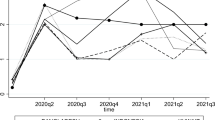

In this section, I report the impact of the Paycheck Protection Program on the risk-taking behaviour of community banks, compared to their non-community banking counterparts. My main empirical results are presented in Table 2. Specifically, in columns (1)–(2), I provide a reduced form of the full model specification of Eq. (1), without and with quarterly fixed effects, respectively. In columns (3)–(4), I provide the results for the full model specification of Eq. (1), without and with quarterly fixed effects, respectively. In all regression models shown in Table 2, my main variable of interest is the DiD estimator PPP * Community which measures the impact of PPP lending on the risk-taking of community banks relative to their non-community banking counterparts. By investigating the coefficient associated with the interaction term PPP * Community, I find a negative and significant impact of PPP lending on the risk-taking appetite of community banks. In terms of the economic magnitudes, I find that, on average, the quarterly change in bank insolvency risk for community banks decreases more (from 0.10% in pre-PPP period to − 2.9% in the post-PPP period) than the one for their non-community banking counterparts (from − 2.3% in pre-PPP period to − 4.0% in the post-PPP period). Graphical confirmatory evidence is provided in Fig. 4 showing the predicted outcomes of ΔRWATA for community vs non-community banks.Footnote 8

Predicted outcomes of ΔRWATA by bank type pre- & post-PPP

My evidence therefore indicates that, after the introduction of the Paycheck Protection Program in the US, community banks significantly decreased their risk-taking, compared to their larger non-community banking counterparts. Looking at the bank-level control variables, I find significant positive impacts of size and ROA on bank risk-taking.

I interpret these results that community banks decrease their risk-taking attitude outside of the program in the post-PPP period relative to their non-community banking counterparts in the US, as a result of their greater exposure to the commercial real estate sector, severely hit by the pandemic-associated lockdowns, as discussed in the previous sections of this study. This more prudential attitude of community banks towards risk-taking outside of the program occurs in a scenario where the 0% risk weighting on PPP loans should encourage banks of all sizes to take on additional risk outside of the program to the same extent. Indeed, the increase in small business lending as a result of the PPP program increases the loan portfolio of participating banks, however, due to the 0% risk-weighting of PPP loans, the resulting credit risk associated with the loan portfolio is reduced by PPP loans. This provides an opportunity for banks to engage in riskier lending outside of the PPP, potentially generating higher returns as a result of their PPP engagement, consistent with Kim and Santomero (1988) who suggest that lower capital regulatory requirements lead to greater risk-taking behaviour from banks. However, I add to these findings by investigating the differential impact PPP lending has on the risk-taking of community vs non-community banks.

7 Robustness tests

To confirm my results on the negative relationship between risk-taking behaviour and PPP lending by community banks, I perform several robustness checks that leave my main findings unaffected.

7.1 Alternative measure of bank risk

This section uses alternative measures of bank risk to further corroborate my main empirical findings. In the main model specification of Eq. (1), bank risk is measured as the quarterly change in the ratio of risk-weighted assets to total assets (ΔRWATA). I now test my hypothesis by using alternative proxies for bank risk drawing from the extant literature.

Firstly, following Casu et al., (2011), I use the quarter-on-quarter growth rate in non-performing loans (ΔNPLTA), measured as the ratio of delinquent loans (30–89 days past due) to total assets. Casu et al. (2011) suggest that this ratio should reflect the true riskiness of a bank’s loan portfolio given its retrospective aspect. Table 3 reports the results of this analysis which confirm a decrease in risk-taking behaviour of community banks outside of the program in the post-PPP period, compared to their non-community banking counterparts.

Secondly, following Roy (1952), Laeven and Levine (2009), Houston et al. (2010), Beck et al. (2013), Delis et al. (2014), and Fang et al. (2014), I repeat the analysis and test my hypothesis by using the Z-score as a further proxy for bank insolvency risk. Specifically, the Z-score equals (ROA + CAR)/σ(ROA), where ROA is the rate of return on assets, CAR is the ratio of equity to assets, and σ(ROA) is an estimate of the standard deviation of the rate of return on assets, all measured with accounting data. Intuitively, this measure represents the number of standard deviations below the mean by which profits would have to fall so as to just deplete equity capital (Boyd et al. 2006; Houston et al. 2010). The Z-score therefore reflects the distance from insolvency (Roy, 1952) where a higher Z-score implies that larger shocks to profitability are required to cause the losses to exceed bank equity and, hence, indicates that the bank is more stable. Because the Z-score is highly skewed, I follow Laeven and Levine (2009) and use the natural logarithm of the Z-score, which is normally distributed. The results are shown in Table 4.

Overall, the aforementioned analyses, obtained by using alternative measures to proxy bank risk, leave my main findings unaffected, further corroborating the novel evidence provided in this paper that US community banks decrease their risk-taking relative to their larger, non-community banking counterparts after the introduction of the Paycheck Protection Program.

7.2 Addressing potential endogeneity concerns

This section addresses the potential endogeneity of the explanatory variables by employing the instrumental variable method (two-stage least squares—2SLS). I now assume that all control variables used in my model are endogenous and I use their values lagged twice as instrumental variables. The validity and importance of the instruments for the control variables are verified using a number of diagnostic tests. The results of these tests are reported in Table 5. Table 5 shows the estimation results of the 2SLS model. The results confirm that small, community banks exhibit a greater decrease in risk-taking in the post-PPP period, compared to non-community banks. Overall, these diagnostic tests do not specify issues regarding the application of the instruments used and provide evidence that further confirms my main empirical results.

7.3 Applying CEM and PSM matching

This section rules out the possibility that my main results could be driven by differences in banks’ fundamentals between the treated (community banks) and control (non-community banks) groups. Following Barth et al. (2021), to estimate the causal effect of the treatment, I now employ the coarsened exact matching (CEM) algorithm as matching method and then use the matched banks to estimate the same model specification shown in Eq. (1). CEM is a Monotonic Imbalance Bounding (MIB) matching method that involves pre-processing data by coarsening variables, implementing one-to-one exact matching, and reducing multivariate imbalance measures (Iacus et al. 2011; Iacus et al. 2012).Footnote 9 Barth et al. (2021) provide evidence that the CEM method has desirable statistical properties and leads to an improvement of the multivariate imbalance measure, compared to other existing matching methods (Iacus et al. 2012), such as propensity score matching (PSM) (Heckman et al. 1997, 1998). Moreover, Iacus et al. (2012) explain that CEM outperforms other existing matching methods in reducing imbalance, model dependency, estimation error, and bias. Indeed, CEM is a nonparametric model that considerably reduces potential bias and model dependency in comparison to other models, such as PSM (Ho et al. 2007; King and Nielsen 2019), accused of increasing imbalance, inefficiency, and statistical bias (King and Nielsen 2019). Matched samples are chosen so that community banks (treated group) are matched to non-community banks (control group) in the pre-PPP period using performance (ROA), delinquency rate (DR), loan ratio (TLTA), and bank capital (Bank Capital). By using the matching output from CEM, I then re-estimate the causal effect by including the CEM weights in my model specification shown in Eq. (1). The results of this robustness analysis, reported in Table 6, again confirm that participation in the Paycheck Protection Program led community banks to decrease their risk appetite outside of the program relative to their non-community banking counterparts, consistent with their greater exposure to the commercial real estate sector at the onset of the COVID-19 pandemic. Therefore, my empirical findings prove to be robust to CEM matching.

Moreover, to further corroborate my empirical findings, I implement propensity score matching (PSM) according to the nearest neighbour matching approach. According to the latter method, matched samples are chosen so that community banks are matched to the nearest neighbour of non-community banks in the pre-PPP period using the same covariates as in the CEM matching procedure. The quality of the matching appears good as there are no statistically significant differences in the pre-PPP mean values of risk-taking across community and non-community banks, suggesting that there is an adequate “like-for-like” comparison in the matching exercise. Indeed, when implementing the matching approach controlling for the above covariates, I do not find statistically significant differences between the risk-taking behaviour of the treated (community banks) and control (non-community banks) groups in the pre-PPP period. PSM results, reported in Table 7, therefore indicate that the difference between the treated and the control groups in the pre-PPP period is not statistically significant. Overall, such evidence suggests that the difference in bank risk-taking observed by community banks in the post-PPP period is not driven by differences in the two groups existing in the pre-PPP period and, therefore, my main empirical results prove to be robust also to PSM matching.

8 Conclusions

In this research article, I provide novel evidence on the consequences of the Paycheck Protection Program for US banks by examining whether participation in the program is associated with differential risk-taking of community vs non-community banks outside of the program. To the best of my knowledge, this is the first study that investigates the impact of the Paycheck Protection Program on bank credit risk-taking behaviour through the lens of US community banks. I offer novel contribution that community banks decrease their risk appetite relative to their non-community banking counterparts after the introduction of the Paycheck Protection Program in the US. Indeed, my empirical findings reveal that the extent of community banks’ PPP participation is associated with relatively lower risk-taking outside of the program, consistent with their greater exposure to the commercial real estate (CRE) sector, severely hit by the pandemic-associated lockdowns. Indeed, structural shifts in CRE demand pose considerable uncertainly around the outlook for the sector and suggest that further price declines may be possible, with a severe negative impact on community banks’ CRE loans, revenues, and capital, potentially incentivizing their lower risk-taking outside of the program.

The novel evidence provided in this paper is informative to policymakers as they weigh the merits of various program options to combat the economic damage imposed by the COVID-19 pandemic and as they consider the design of economic stimulus programs in response to future economic crises. Moreover, such evidence is of interest to bank regulators that monitor bank risk-taking as my empirical findings indicate that PPP participation is associated with changes in bank risk appetite related to bank size. Therefore, regulators should consider bank participation in the program as part of their ongoing monitoring procedures. Finally, the extant literature highlights heterogeneity in bank risk-taking responses based on the design of direct stimulus programs (Rodnyansky and Darmouni 2017; Chakraborty et al. 2020). I contribute to extending this literature by investigating an important type of stimulus package, i.e., one that is administered through, but not intended for, banks and its indirect effects at the bank level. I therefore present my findings as a spur to future research aimed at identifying the indirect channels through which government-funded stimulus programs result in consequences at the bank level.

Notes

While interest rate spreads were small under these loans, banks received SBA fee payments, which increased their non-interest income.

A PPP loan is an SBA-backed loan that helps businesses keep their workforce employed during the COVID-19 crisis (https://www.sba.gov/funding-programs/loans/covid-19-relief-options/paycheck-protection-program).

This argument only requires a change in bank managers’ perceived risk-bearing capacity and does not rely on assumptions regarding external parties’ awareness of the effects of the program.

For a helpful summary of the CARES Act provisions, see generally “Congress Passes CARES Act Fiscal Stimulus Package to Combat the Coronavirus Pandemic’s Economic Impact” by Davis Polk & Wardwell LLP (Mar. 27, 2020) available on https://www.davispolk.com/files/2020-03-26_senate_passes_cares_act_fiscal_stimulus_package.pdf

See 12 CFR 3.32(a)(1) (OCC); 12 CFR 217.32(a)(1) (Board); 12 CFR 324.32(a)(1) (FDIC).

See the BCBS press release of 12 January 2014 on BCBS (2014a), Basel III leverage ratio framework and disclosure requirements (available at http://www.bis.org/publ/bcbs270.htm).

The impact of explanatory variables on ΔRWATA is computed using the “margins” command in Stata, keeping all the other variables at the average.

CEM method is implemented using the “cem” command in Stata with the “k2k” option to contain the same number of treated and control units within all strata. Indeed, the “k2k” option compensates for the differential strata sizes by pruning observations from a CEM solution within each stratum until the solution contains the same number of treated and control units within all strata. Pruning occurs within a stratum by random matching inside CEM strata.

References

Aggarwal R, Jacques KT (2001) The impact of FDICIA and prompt corrective action on bank capital and risk: estimates using a simultaneous equations model. J Bank Financ 25(6):1139–1160

Anbil S, Carlson MA, Styczynski M-F (2023) The effect of the Federal Reserve’s lending facility on PPP lending by commercial banks. J Financ Intermed 55

Autor D, Cho D, Crane LD, Goldar M, Lutz B, Montes J, Peterman WB, Ratner D, Villar D, Yildirmaz A (2022) An evaluation of the paycheck protection program using administrative payroll microdata. J Public Econ 211

Autor D, Cho D, Crane LD, Goldar M, Lutz B, Montes J, Peterman WB, Ratner D, Villar D, Yildirmaz A (2022) The $800 Billion Paycheck Protection Program: where Did the Money Go and Why Did It Go There? J Econ Perspect 36(2):55–80

Avery RB, Berger AN (1991) Risk-based capital and deposit insurance reform. J Bank Financ 15(4–5):847–874

Ballew HB, Nicoletti A, Stuber SB (2022) The effect of the paycheck protection program and financial reporting standards on bank risk-taking. Manage Sci 68(3):2363–2371

Balyuk T, Prabhala N, Puri M (2021) Small bank financing and funding hesitancy in a crisis: evidence from the paycheck protection program. FDIC CFR WP pp 01

Barrios J, Minnis M, Minnis W, Sijthoff J (2020) Assessing the payroll protection program: a framework and preliminary results. In: Working Papers, Becker Friedman Institute for Research in Economics, pp 63

Barth JR, Lee KB, Shen X, Yoon Y (2021) Application of difference-in-differences strategies in finance the case of natural disasters and bank responses. Cheng FL, Alice CL (Eds) Encyclopedia of Finance, Springer, New York

Bartik AW, Cullen ZB, Glaeser EL, Luca M, Stanton CT, Sunderam A (2020) The targeting and impact of Paycheck Protection Program loans to small businesses. In: National Bureau of Economic Research, No. w27623

Bank for International Settlements (BIS) (2017) Basel III leverage ratio framework—Executive summary. October 25

Beauregard R, Lopez JA, Spiegel MM (2020) Federal Reserve Bank of San Francisco (FRBSF) Economic Letter, November 23, pp 35

Beck T, De Jonghe O, Schepens G (2013) Bank competition and stability: cross-country heterogeneity. J Financ Intermed 22(2):218–244

Berger AN (1995) The relationship between capital and earnings in banking. J Money Credit Bank 27(2):432–456

Berger AN, Udell GF (1994) Did risk-based capital allocate bank credit and cause a" credit crunch" in the United States? J Money Credit Bank 26(3):585–628

Berger AN, Udell GF (2002) Small business credit availability and relationship lending: the importance of bank organisational structure. Econ J 112(477):32–53

Berger AN, Kashyap AK, Scalise JM, Gertler M, Friedman BM (1995) The transformation of the US banking industry: what a long, strange trip it's been. Brook Pap Econ Act 2:55–218

Berger AN, Miller NH, Petersen MA, Rajan RG, Stein JC (2005) Does function follow organizational form? Evidence from the lending practices of large and small banks. J Financ Econ 76:237–269

Bose U, Filomeni S, Mallick S (2021) Does bankruptcy law improve the fate of distressed firms? The role of credit channels. J Corp Finan 68. https://doi.org/10.1016/j.jcorpfin.2020.101836

Boyd J, De Nicolò G, Al Jalal A (2006) Bank risk taking and competition revisited: new theory and new evidence. In: IMF Working Paper No. 06/297

Bureau of Labor Statistics, U.S. Department of Labor, The Economics Daily (2020) Unemployment rate rises to record high 14.7 percent in April 2020 at https://www.bls.gov/opub/ted/2020/unemployment-rate-rises-to-record-high-14-point-7-percent-in-april-2020.htm

Cassell MK, Schwan M, Schneiberg M (2023) Bank Types, Inclusivity, and paycheck protection program lending during COVID-19. Econ Dev Q 37(3):277–294

Casu B, Clare A, Sarkisyan A, Thomas S (2011) Does securitization reduce credit risk taking? Empirical evidence from US bank holding companies. Eur J Financ 17(9–10):769–788

Casu B, Chiaramonte L, Croci E, Filomeni S (2022) Access to credit in a market downturn. J Financ Serv Res. https://doi.org/10.1007/s10693-022-00388-x

Chakraborty I, Goldstein I, MacKinlay A (2020) Monetary stimulus and bank lending. J Financ Econ 136(1):189–218

Cole RA, Damm J (2020) How did the financial crisis affect small-business lending in the United States? J Financ Res 43(4):767–820

Cole RA, Goldberg LG, White LJ (1999) Cookie-cutter versus character: The micro-structure of small business lending by large and small banks. New York University. Salomon Center Working Paper: S/99/12

Delis M, Hasan I, Tsionas M (2014) The risk of financial intermediaries. J Bank Financ 44:1–12

Deming K, Weiler S (2023) Banking Deserts and the Paycheck Protection Program. Econ Dev Q 37(3):259–276

Demsetz H, Lehn K (1985) The structure of corporate ownership: causes and consequences. J Polit Econ 93(6):1155–1177

Fang Y, Hasan I, Marton K (2014) Institutional development and bank stability: evidence from transition countries. J Bank Financ 39:160–176

Federal Deposit Insurance Corporation (FDIC) (2020) Loans. RMS Manual of Examination Policies. http://www.fdic.gov/regulations/safety/manual/section3-2.pdf

Fendoglu S (2021) Commercial real estate and financial stability: evidence from the us banking sector. In: Global financial stability notes No 2021/001

Fernandes N (2020) Economic Effects of Coronavirus Outbreak (COVID-19) on the World Economy IESE Business School Working Paper No. WP-1240-E, March 22

Filomeni S, Udell G, Zazzaro A (2020) Communication frictions in banking organizations: Evidence from credit score lending. Econ Lett 195C:109412. https://doi.org/10.1016/j.econlet.2020.109412

Filomeni S, Udell G, Zazzaro A (2021) Hardening soft information: does organizational distance matter? Eur J Financ 27(9):897–927. https://doi.org/10.1080/1351847X.2020.1857812

Filomeni S, Bose U, Megaritis A, Triantafyllou A (2023) Can market information outperform hard and soft information in predicting corporate defaults? Int J Financ Econ. https://doi.org/10.1002/ijfe.2840

Filomeni S, Modina M, Tabacco E (2023) Trade credit and firm investments: empirical evidence from Italian cooperative banks. Rev Quant Financ Acc 60:1099–1141. https://doi.org/10.1007/s11156-022-01122-3

Filomeni S, Querci F (2023) Did Biden-Harris’s Reforms on the Paycheck Protection Program Reduce Racial Disparity in Lending? Working Paper

Glancy D (2023) Bank relationships and the geography of PPP lending. finance and economics discussion series. Wash Board Gov Fed Res Syst. https://doi.org/10.1716/FEDS.2023.014

Granja J, Makridis C, Yannelis C, Zwick E (2022) Did the paycheck protection program hit the target? J Financ Econ 145(3):725–761

Heckman JJ, Ichimura H, Todd PE (1997) Matching as an econometric evaluation estimator: evidence from evaluating a job training programme. Rev Econ Stud 64(4):605–654

Heckman JJ, Ichimura H, Todd P (1998) Matching as an econometric evaluation estimator. Rev Econ Stud 65(2):261–294

Ho DE, Imai K, King G, Stuart E (2007) Matching as nonparametric preprocessing for reducing model dependence in parametric causal inference. Polit Anal 15:199–236

Houston JF, Lin C, Lin P, Ma Y (2010) Creditor rights, information sharing, and bank risk taking. J Financ Econ 96(3):485–512

Iacus SM, King G, Porro G (2011) Multivariate matching methods that are monotonic imbalance bounding. J Am Stat Assoc 106(493):345–361

Iacus SM, King G, Porro G, Katz JN (2012) Causal inference without balance checking: coarsened exact matching. Polit Anal 20(1):1–24

Jackson HE, Schwarcz SL (2020) Protecting financial stability: lessons from the coronavirus pandemic. Harv Bus Law Rev 11(2):193–232

Kellard NM, Kontonikas A, Lamla MJ, Maiani S, Wood G (2023) Making the world safe for investors: the unintended consequences of the paycheck protection program. Working Paper

Kim D, Santomero AM (1988) Risk in banking and capital regulation. J Financ 43(5):1219–1233

King G, Nielsen R (2019) Why propensity scores should not be used for matching. Polit Anal 27(4):435–454

Laeven L, Levine R (2009) Bank governance, regulation and risk taking. J Financ Econ 93(2):259–275

Li L, Strahan P (2020) Who Supplies PPP Loans (And Does it Matter)? Banks, Relationships and the COVID Crisis.NBER Working Papers 28286, National Bureau of Economic Research, Inc

Lopez JA, Spiegel MM (2023) Small business lending under the PPP and PPPLF programs. J Financ Intermed 53

Mandel BH, Morgan D, Wei C (2012) The role of bank credit enhancements in securitization. Fed Res Bank N Y Econ Policy Rev 18(2):35–46

MGO (2021) Third Wave of Paycheck Protection Loans available on https://www.mgocpa.com/article/third-wave-of-paycheck-protection-program-loans

Federal Register (2020) Business loan program temporary changes; paycheck protection program. In: A rule by the small business administration on April 15, 2020

Rodnyansky A, Darmouni O (2017) The effects of quantitative easing on bank lending behavior. Rev Financ Stud 30(11):3858–3887

Roy AD (1952) Safety first and the holding of assets. Econometrica 20(3):431–449

Shrieves RE, Dahl D (1992) The relationship between risk and capital in commercial banks. J Bank Financ 16(2):439–457

Small Business Administration (2020) Paycheck Protection Program available on https://www.sba.gov/funding-programs/loans/coronavirus-relief-options/paycheck-protection-program

Stein JC (2002) Information production and capital allocation: decentralized versus hierarchical firms. J Financ 57(5):1891–1921

Acknowledgements

I am grateful to the Editor Cheng-Few Lee and to two anonymous referees for their valuable insights and suggestions.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Filomeni, S. The impact of the Paycheck Protection Program on the risk-taking behaviour of US banks. Rev Quant Finan Acc 62, 1329–1353 (2024). https://doi.org/10.1007/s11156-023-01223-7

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11156-023-01223-7

Keywords

- Bank risk

- Paycheck Protection Program

- Covid-19 pandemic

- Community bank

- Relationship lending

- Soft information