Abstract

Much of the work on the valuation of levered (and unlevered) warrants assumes that the volatility of the underlying state variable is constant. This paper extends the literature on warrant pricing to a more general assumption for the state variable process, the so-called constant elasticity of variance (CEV) process. The CEV model is well-known for its ability to capture some empirical observations found in the financial economics literature, namely the asymmetry between equity returns and volatility and the implied volatility skew. Using the CEV process, we are able to reduce pricing bias as the volatility becomes a function of the underlying state variable. We price European-style call warrants without restrictions on the debt maturity. When warrants have the same maturity as debt, it is possible to obtain closed-form solutions for warrants prices. When the maturity of warrants is different from the maturity of debt, prices can be computed numerically through very efficient and simple to implement valuation methodologies.

Similar content being viewed by others

1 Introduction

As mentioned by Ingersoll (1987), warrants are similar to call options. Both give the holder the right, but not the obligation, to buy at or before (in case of American-style) or at (in case of European-style) a given set date, shares of stock of a particular company at an agreed price (the strike price). In general, there are two types of warrants: covered warrants (also known as bank-issued options) and equity warrants (also known as corporate warrants). The covered warrants are issued by a third party (usually a financial institution) and have no dilution effect. Conversely, the exercise of equity warrants leads to a dilution of the equity of the company, being this one of the biggest differences between this type of warrants and options. In a nutshell, equity warrants are only issued by companies.

Given their particular features, warrants have been greatly used recently. For example, Chuang et al. (2021) document that, by the end of 2015, there were 10,542 covered warrants on the Taiwan Stock Exchange. There is evidence of usage of warrants as part of underwriter’s compensation—see Dunbar (1995), Garner and Marshall (2014) and Khurshed et al. (2016), among others—, as stand alone capital raising instruments—e.g., Suchard (2005)—, in unit offerings—see, for instance, Schultz (1993), Byoun and Moore (2003), Gajewski et al. (2007) and Howe and Olsen (2009)—, etc.Footnote 1 Given the burgeoning interest on this type of financial instruments, the existence of a model able to price them accurately, taking the observed stylized facts into account becomes essential. Since covered warrants share, in essence, their characteristics with options, by the law of one price their prices should coincide with the prices of the options. The major difficulty arises in pricing corporate warrants. The creation of a model to price these last has been one the biggest challenges in the warrant valuation process.

In some cases, both academics and practitioners adopt the Black and Scholes (1973) stock option formula in order to value corporate warrants. As we will discuss later, this model ignores several stylized facts found in the financial literature and, as a result, its prices are, usually, very inaccurate. For instance, Chang et al. (2013) find that the market prices of warrants are generally much higher systematically than the Black–Scholes prices in Chinese warrant market.

In other cases, practitioners adopt somewhat obscure and unreasonable methods to value warrants, which gives rise to prices very far from reality. An interesting recent example is the case of the bankrupt rental-car company Hertz that has received much attention in the financial social media—e.g., March 2, 2021, and May 13, 2021, in Bloomberg and Financial Times news articles, respectively. The Financial Times article states that “The private equity consortium that will acquire Hertz says the company’s current public stockholders will get a package worth $7.36 for each share. About $2 of that figure is in cash as well as direct new shares in the reorganised Hertz. The balance comes in the form of warrants, offering the option to buy into the new Hertz at a given price. These are a derivative security whose valuation comes from the famed Black–Scholes equation, which contains a variety of inputs. With Hertz shares trading at $6 a piece, Wall Street does not seem to agree with the maths involved." The issue here is that private equity bidders and Hertz have used a stock price volatility input of 57.5% in the Black–Scholes equation to determine the $5.47 value of warrants, which is very close to the underlying stock price of $6. Clearly, this calculation has not convinced everyone. This example highlights the need of more realistic models to value warrants. Hence, the novel pricing solutions for levered (and unlevered) warrants proposed in this paper should be of interest not only for academics but also for practitioners in the banking and finance industry.

From a theoretical standpoint, Black and Scholes (1973) propose the valuation of a warrant as a call option on shares of firm’s equity rather than a call option on shares of common stock at half stated exercise price (they assume a dilution factor, i.e. the ratio of the number of outstanding warrants to outstanding shares of common stock prior to exercise, equal to one). However, the derivation of a formula taking the dilution effect correctly into account is done by Galai and Schneller (1978). Despite their great contribution to the warrant valuation process, the models proposed by Black and Scholes (1973) and Galai and Schneller (1978) have the shortcoming of using unobservable variables, namely the firm’s value (the sum of all warrants outstanding and common stock outstanding) and volatility. To overcome this issue, Schulz and Trautmann (1994) and Ukhov (2004) propose to solve a system of nonlinear equations in order to obtain the value of these variables and then use them to compute the warrant value.

Even though much of this early work assumes an equity-based approach (equity as the underlying state variable) and takes the dilution effect into account, there have been empirical investigations supporting the valuation of warrants as plain-vanilla call options on common stock ignoring the dilution effect (known as option-like valuation)—e.g., Schulz and Trautmann (1994), Sidenius (1996) and Bajo and Barbi (2010). For instance, Schulz and Trautmann (1994) find that option-like valuation provides correct prices for in-the-money and at-the-money warrants and, therefore, claim that in these cases there is no need to use the correct warrant valuation approach. Handley (2002) advocates that this framework is correct and consistent with the Efficient Market Hypothesis, where the stock price of the underlying firm is already incorporating dilution and, hence, there is no need to correction. Notwithstanding the practical usability of this model, it has the inconvenience that the stock cannot follow a lognormal distribution, even when the value of firm’s assets follows such distribution—see, for instance, Galai and Schneller (1978) and Crouhy and Galai (1994).

Although the models proposed by Black and Scholes (1973) and Galai and Schneller (1978) shed light on the valuation of warrants, they are not realistic since they do not consider debt into the firm’s value. The first model taking debt correctly into account is derived by Crouhy and Galai (1994), where the firm’s value is a sum of equity (aggregate of stock and warrants) and debt. They assume that warrants have a maturity shorter than debt’s expiration date and that firms reinvest the proceeds from warrants exercise. This model is extended by Abínzano and Navas (2013) to the cases where warrants have longer and the same maturity as debt. Like many other authors on warrant pricing, Crouhy and Galai (1994) and Abínzano and Navas (2013) develop their model under the assumption that the underlying state variable (firm’s value) follows a geometric Brownian motion (henceforth, GBM) with constant drift and variance parameters.

Nevertheless, Lauterbach and Schultz (1990) and Hauser and Lauterbach (1997) show, through an extensive empirical investigation, that the constant elasticity of variance (henceforth, CEV) model of Cox (1975) outperforms the Black and Scholes (1973) model when predicting warrant prices.Footnote 2 According to these authors, despite the analytical tractability of the Black–Scholes model, the assumption of a GBM with constant drift and volatility can lead investors to mispricing, since, apart from the problems with stochastic interest rates, early exercise prior to dividend payments, among others, it is well-known that equity volatility is far from being constant.Footnote 3

Bajo and Barbi (2010) find that even the stock-based approach can be more accurate if one incorporates the risk-shifting effect into the valuation by using the CEV model. According to the authors, the option-like valuation proposed by Schulz and Trautmann (1994) and Sidenius (1996) under the GBM assumption ignores the volatility spillover which is verified when the firm issues warrants. Since warrants are similar to call options, a negative (resp., positive) shock on the equity value leads to a stronger depreciation (resp., appreciation) of the warrant than of the stock price. To put it in another way, part of the risk assumed by the shareholders is shifted to the warrant holders which causes a lower stock price variability relative to an identical firm with no outstanding warrants.

Moreover, it is well documented—e.g., Jackwerth and Rubinstein (1996)—that after the crash of 1987, the empirical asset returns distributions are more left-skewed and changed from platykurtic to leptokurtic and, thus, the lognormal assumption is unable to consider these features. Therefore, the use of alternative stochastic processes can reduce pricing bias and help investors improving their decision-making process.

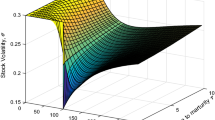

Overall, there are several advantages in applying the CEV model to price financial derivatives. It is consistent with two facts empirically supported in the literature, namely: the inverse relation between the implied volatility and the strike price of an option contract (implied volatility skew or implied volatility smile) documented, for example, by Dennis and Mayhew (2002), and the asymmetry between equity return and volatility, explained by a combination of financial leverage, volatility feedback and operating leverage, as showed, for instance, in Beckers (1980), Christie (1982), Bekaert and Wu (2000) and Choi and Richardson (2016). The CEV model allows analytical tractability and volatility is modeled without the need of introducing an additional stochastic process as in the case of Heston (1993) stochastic volatility model. It is, synchronously, a local volatility and a “complete-market” model and, therefore, allows the construction of synthetic portfolios.

Since the lognormal assumption with constant volatility in the Black and Scholes (1973) model is unable to accommodate the aforementioned stylized facts, the main aim of this paper is to generalize the models in the literature under GBM to the CEV framework where the volatility is no longer constant, but rather becomes a function of the underlying state variable. To accomplish this purpose, we use the closed-form solutions proposed by Schroder (1989) for the elasticity parameter \(\beta <2\) and Heston et al. (2007) for \(\beta >2\). We price warrants with no restriction of debt maturity, i.e., warrants can have the same, shorter or longer maturity than debt. When warrants have the same maturity as debt, it is possible to obtain analytical solutions for warrants prices. When warrants and debt have different maturities, prices can be computed via numerical procedures.Footnote 4

The present paper contributes to the literature in different ways. First, we propose analytical solutions, under the CEV process, for pricing warrants with the same maturity as debt. For this purpose, we follow Abínzano and Navas (2013) whose solution was derived under a lognormal assumption. We also follow Schroder (1989) and Heston et al. (2007) to compute the prices under the CEV model. Although not trivial, our framework is flexible enough and can be extended or modified in order to analyze the existence of dark matter in corporate warrants—see, for instance, Bakshi et al. (2022). Second, we propose numerical solutions for pricing warrants with longer or shorter maturity than debt under the CEV diffusion. In this case, to compute the warrant prices with the Abínzano and Navas (2013) model, we use Monte Carlo simulation and solve the system of nonlinear equations, simultaneously. Third, we demonstrate, through an extensive numerical analysis, the implication of an incorrect specification of the underlying state variable process for the valuation of warrants. Our results show that, in general, the investors are subject to a very significative pricing bias assuming the GBM for the state variable. For comparative purposes, we also extend the several models available in the literature such as Ukhov (2004) model, classical warrant valuation, among others, to the CEV process.

The remainder of this paper is organized as follows. Section 2 shortly overviews the general setup of the CEV model and addresses the problem of simulating asset prices under the CEV process. Section 3 derives the warrant pricing models under the CEV model. Section 4 presents some numerical examples and compares the results under the CEV framework against those of GBM setup. Finally, Sect. 5 concludes the paper. All the accessory results are relegated to the appendixes collected in the supplementary file.

2 The CEV diffusion model

This section briefly reviews the building blocks of the CEV model and describes the Euler-Maruyama scheme that is required to approximate the path of the asset values for the cases where no closed-form warrant pricing solutions are available.

2.1 Setup of the model

Taking the equivalent martingale measure \({\mathbb {Q}}\) as given, we assume that the asset price \(\{V_t, t\ge 0\}\) (under \({\mathbb {Q}}\) that takes as numeraire the money market account) is a time-homogeneous nonnegative diffusion process solving the following stochastic differential equation:

with the local volatility function given by

for \(\delta\) \(\in\) \({\mathbb {R}}_{+}\), \(\beta\) \(\in\) \({\mathbb {R}}\) and where r represents the constant risk-free interest rate, \(\sigma (V_t)\) represents the local volatility function (i.e., the instantaneous volatility per unit of time of asset returns), which is assumed to be continuous and strictly positive for all \(V \in (0,\infty )\), \(dW_t^{{\mathbb {Q}}} \in {\mathbb {R}}\) is a standard Brownian motion under \({\mathbb {Q}}\), initialized at zero and generating the augmented, right continuous and complete filtration \({\mathbb {F}} = \{\mathcal {F}_t:t\ge 0\}\).

We recall that the CEV specification given by Eqs. (1) and (2) nests the lognormal assumption of Black and Scholes (1973) and Merton (1973) (\(\beta =2\)) as well as the absolute diffusion (\(\beta =0\)) and the square-root diffusion (\(\beta =1\)) processes of Cox and Ross (1976) as special cases. We further note that whenever \(\beta <2\) (resp., \(\beta >2\)), the local volatility function (2) is a decreasing (resp., increasing) function of the asset price, thus being able to generate downward-sloping (resp., upward-sloping) volatility skews that are observed in the market. The elasticity of return variance with respect to price is equal to \(\beta -2\) given that \(dv(V_t)/v(V_t)=(\beta -2)dV_t/V_t\), where \(v(V_t)=\delta ^2V_t^{\beta -2}\) is the instantaneous variance of asset returns. The model parameter \(\delta\) is a positive constant that can be interpreted as the scale parameter fixing the initial instantaneous volatility at time \(t=0\), \(\sigma _V=\sigma (V_0)=\delta V_0^{\beta /2-1}\). This calibration procedure is standard in the literature and it ensures that CEV models with different values of \(\beta\) have the same variance at the beginning of the simulation period, which allows us to make valid comparisons between different CEV models. Additional background on the CEV diffusion process can be consulted, for instance, in Davydov and Linetsky (2001), Dias and Nunes (2011), Larguinho et al. (2013), Dias et al. (2015) and Dias et al. (2020).

2.2 Simulation of asset values

Unlike the GBM process, where the asset value \((V^\prime _T)\) can be written analytically (thus yielding an exact solution), in the case of the CEV process such simple representation is not available. Nevertheless, it is still possible to use Monte Carlo simulation by discretizing the time interval and simulating the state process dynamic on this discrete-time grid—see, for example, Broadie and Kaya (2006). The straightforward Euler-Maruyama discretization scheme, described in Kloeden and Platen (1992), can be used to approximate the path of the asset value on a discrete-time grid.

Let \(0=t_0<t_1<...<t_n=T\) be a partition of n evenly-spaced time points \(t_i:= t_0 + i \Delta t\), for \(i=0,1,...\), and with \(\Delta t:= \left( T - t_0 \right) /n\). The discretization of the asset value under the CEV model is written as:

We recall that the scale parameter \(\delta\) is readjusted so that the initial instantaneous volatility is the same across different models. Thus, we can rewrite the last expression as

It is well-known that Eq. (1) applies only up to the stopping time

Following the insights of Lindsay and Brecher (2012), the treatment of the process after the stopping time depends on the underlying financial problem. In this case, the stopping time (5) indicates the time of bankruptcy of the company. The probability that \(V^\prime _t\) hits the boundary point 0 for markets exhibiting forward skew patterns \((\beta >2)\) is zero and, thus, \(V^\prime _t\) will never go to negative values in this particular case. However, when \(\beta <2\), \(V_t^\prime\) hits zero with positive probability. Therefore, when negative values are encountered during the simulation, \(V_t^\prime\) is simply set to 0 from that time-step onward.

3 Pricing levered warrants

This section is concerned with the extension of the warrant pricing models available in the literature under the lognormal framework to the more general CEV process. In particular, the following models are considered: the classical warrant valuation model, the Schulz and Trautmann (1994) and Ukhov (2004) model, the Crouhy and Galai (1994) model and the levered warrant models for the cases of warrants with different maturities relative to debt.

3.1 Classical warrant valuation

After Black and Scholes (1973) proposed the valuation of warrants as a call option on equity, adjusted by the dilution factor, this method became standard on the warrant valuation process. As recalled by Abínzano and Navas (2013), this model is usually known as the “correct warrant valuation”. In this model, it is assumed that the underlying state variable is the firm value. The goal now is to extend the classical warrant valuation model to the CEV process. Since this model does not consider debt, the value of the firm in this case is equal to its equity value.

Assume a firm is financed by N shares of common stock and M European-style call warrants. Each warrant entitles the owner to receive k shares of stock at time \(t=T\) upon payment of X dollars. The company is financed only by these two sources of funding. Assume also that \(V_t\) and \(\sigma _V\) are the firm value and firm returns volatility at time t, and \(S_t\) and \(\sigma _S\) denote the stock price and stock volatility, respectively, at time t.Footnote 5 Let \(w_t\) denote the price of each warrant at time t.

In what follows, we show the insights behind the classical warrant valuation model described in Ingersoll (1987). If the M warrants are exercised at time \(t=T\), the firm receives an amount of money of MX and issues Mk new shares of stock. Thus, if it is known that the warrants will be exercised at the maturity date T, then each share of stock will be worth \(S_T=(V_T + MX) / (N + kM)\). At the point where the warrants holders are indifferent about exercising \((kV_T=NX)\) each k shares are worth X, so the warrants are exercised only if \(kS_T\ge X\), just as with plain-vanilla call options. If the warrants owners strictly prefer exercising \((kV_T> NX)\), then the common stock is worth less than the value of the firm’s assets. Note that this shortfall simply measures the value of the warrants. The same is generally true prior the maturity of the warrants. Therefore, the value of each warrant at maturity, T, is given by

The time-T payoff (6) implies that the time-t warrant value is equal to \(1/(N+kM)\) call option on kV, with strike price NX and maturity at time T \((\ge t)\), i.e.

where \(c_t(A_t,K,T)\) is the time-t value of a plain-vanilla call option on the asset price \(A_t\), with strike K and maturity at time T \((\ge t)\) given by

as shown by Schroder (1989) and Heston et al. (2007) for \(\beta < 2\) and \(\beta > 2\), respectively, with \(\Gamma (a,z)\) and \(\Gamma (a)\) being, respectively, the upper incomplete gamma function and the Euler gamma function given in Abramowitz and Stegun (1972, Eqs. 6.5.3 and 6.1.1), \(Q(\gamma ;v,\xi )\) representing the complementary distribution function of a non-central chi-square law with v(\(\ge 0\)) degrees of freedom and non-centrality parameter \(\xi\)(\(\ge 0\)), andFootnote 6

and

Therefore, the warrant price can be expressed as

Unless the investor is able to obtain a good estimate of \(V_t\) and \(\sigma _V\), the classical warrant valuation model is difficult to use, since these variables are unobservable.

3.2 Schulz and Trautmann (1994) and Ukhov (2004) model

To overcome the problem of unobservable variables in the classical warrant valuation model, Schulz and Trautmann (1994) and Ukhov (2004) follow a different approach allowing the use of observable variables \((\sigma _S\text { and } S_t)\) when computing the value of the warrant. Even though the stock volatility is not observable, it can be easily estimated from historical stock prices or determined as the implied volatility in the options prices quoted in the market.

Assume a firm is financed only by equity, where warrants and stocks are contingent claims on firm value. In this sense, the firm volatility is a weighted average of volatilities of the two claims. Since a warrant is similar to an option, it is riskier than the stock. Hence, the volatility of the stock is less than the volatility of the entire firm. Define \(\varepsilon _S\equiv \Delta _SV_t/S_t\) as the elasticity of the stock price with respect to the firm value, where \(\Delta _S\) is the hedge ratio for the stock given by \(\Delta _S=\dfrac{\partial S_t}{\partial V_t}\).

We can relate \(V_t\) and \(\sigma _V\) to \(S_t\) and \(\sigma _S\) through the following equationFootnote 7

where \(\delta =\sigma _VV_t^{1-\frac{\beta }{2}}\). To compute \(\Delta _S\), we need to calculate \(\Delta _w=\partial w_t/\partial V_t\) given that \(V_t=NS_t+Mw_t\), where \(w_t\) is given by Eq. (14). It is straightforward to notice that \(\Delta _w\) is similar to the hedge ratio of a call option derived by Larguinho et al. (2013, Eq. A7) and Dias et al. (2020, Corollary 1). Thus, \(\Delta _w\) is given by

where \(p(\gamma ;v,\xi )\) is the probability density function of a non-central chi-square distribution as given by Johnson et al. (1995, Eq. 29.4). Using the fact that a share of stock is also a contingent claim on the firm (there exists a hedge ratio that measures stock price changes when firm value, V, changes 1 dollar), then we can write \(N\Delta _S+M\Delta _w=\Delta _V=1\). Hence, \(\Delta _S\) can be obtained by substituting \(\Delta _w\) into the following expression

To compute the warrant price (under the CEV process) using only observable variables \((S_t \text { and } \sigma _S)\), we need to:

1. Solve (numerically) the following system of nonlinear equations for \((V_t^*, \sigma _V^*)\),

where \(w_t\) is given by Eq. (14).

2. The warrant price, \(w_t\), is calculated as

3.3 Crouhy and Galai (1994) model

Even though the previous model overcomes the problem of unobservable variables, it still has the inconvenience of not considering debt into the valuation process. To solve this, Crouhy and Galai (1994) propose a model which incorporates debt correctly albeit based on unobservable variables. To this end, they assume a firm financed by N shares of stock, M European-style call warrants and debt D. The debt is a zero-coupon bond with face value F and maturity at time \(T_D\). The proceeds from exercising the warrants are assumed to be reinvested in the company, thus increasing its size. They also assume a perfect market condition and that there are no economies of scale and, thus, the distribution of returns for one unit of investment is stationary and independent of the firm size. Furthermore, it is assumed that r is known and constant.

To derive their formula, they also consider that there is a benchmark firm with the same investment policy as the underlying firm, but financed entirely by common stock.Footnote 8 Crouhy and Galai (1994) study only the case where warrants have shorter maturity than debt, i.e. \(T<T_D\). At \(t=0\), the benchmark firm issues \(N^\prime\) shares of stock at a price \(V_0^\prime /N^\prime =S_0^\prime\), whereas the underlying firm issues N shares of stock, M warrants and a zero-coupon bond. Then, for \(0\le t<T\) we can write

where \(S_t,w_t\text { and }D_t\) are, respectively, the values of a share of stock, warrant and debt of the levered firm.

In the extension of this model to the CEV process, all the assumptions of Crouhy and Galai (1994) are assumed to hold, except that the underlying state variable follows now a CEV process. If the warrants are not exercised at \(t=T\), the value of the levered firm, \(V_{T_D}\), will be equal to the value of the unlevered firm, \(V^\prime _{T_D}\), at \(t=T_D\). On the other hand, if the warrants are exercised at \(t=T\), the amount MX received from the exercise of the warrants will be reinvested and the value of the levered firm at \(t=T_D\) becomes \(V_{T_D}=V^\prime _{T_D}(1+MX/V_T^\prime )\), while the value of unlevered firm remains \(V^\prime _{T_D}\). The ratio \(MX/V_T^\prime\) measures the scale expansion of the firm’s assets at time T.

The traditional procedure in the financial economics literature is to exercise the warrants if the stock price immediately prior to the warrants’ expiration date is greater than the strike price. Crouhy and Galai (1994) show that this approach can be misleading if the share price prior to expiration differs from the price after this date. They argue that such discontinuity in price stems from the fact that the exercise of warrants, which results in a scale of expansion of the firm, may reduce the probability of default and, consequently, increase the value of debt which causes a reduction in the share price. Therefore, the warrants should be exercised if the post-expiration value of the k diluted shares is greater than X.

No matter whether warrants are exercised or not, after time T the firm’s value is composed only of common stock and debt. Thus, the post-expiration value of a share of stock, \(S_T\), can be written as follows:

where \(D_T^W\), \(D_T^{NW}\), \(S_T^W\) and \(S_T^{NW}\), represent the value of debt and a share of stock at time T if warrants are exercised and if warrants are not exercised, respectively. Given that \(S^W_T\) is an increasing function of \(V^\prime _T\), the exercise criteria can be determined finding a threshold value of the firm, \(\bar{V}_T^\prime\), such that \(kS_T^W(\bar{V}^\prime _T)\equiv X\).

Since it is assumed that the proceeds from the exercise of the warrants are reinvested, the last expression of \(S_T\) can be easily determined if we look at the equity of the levered firm as a call option on the firm value immediately after warrants’ expiration, with strike F, and maturity at time \(T_D\), that is

where \(c_t(A_t,K,T)\) is a call option on the asset price \(A_t\), with strike K and maturity at time T. We recall that under the CEV diffusion, the volatility of the reference firm at time T becomes \(\sigma (V_T^\prime )={\delta V_T^{\prime }}^{\frac{\beta }{2}-1}\), where \(\delta =\sigma _{V^\prime }{V_t^\prime }^{1-\frac{\beta }{2}}\). Thus, under the assumption that \(V_t^\prime\) follows the CEV process described by Eq. (1), we can write \(S_t\) at any time t \((<T)\) as

where \({\mathbb {E}}_{{\mathbb {Q}}}[R|\mathcal {F}_t]\) denotes the (time-t) expected value of the random variable R, conditional on \(\mathcal {F}_t\) and computed under the equivalent martingale measure \({\mathbb {Q}}\), \(\mathbbm {1}_{\{B\}}\) is an indicator function of the event B and \(f(V_T^\prime ,T;V_t^\prime ,t)\) is the probability density function of \(V_T^\prime\) conditional on \(V^\prime _t\) at time \(t<T\) presented in Schroder (1989, Eq. 1) and Emanuel and MacBeth (1982, Eq. 7) for \(\beta < 2\) and \(\beta > 2\), respectively, and written as

where \(\tilde{k}\) is given by Eq. (9),

and

Using the same reasoning which led to \(S_t\), the value of debt at any time t, with \(t<T\), is obtained as

where \(p_t(A_t,K,T)\) is a put option on the asset price \(A_t\), with strike K and maturity at time T \((\ge t)\) expressed as

The price of the warrant is obtained substituting \(S_t\) and \(D_t\) into the equation

3.4 Levered warrant model for warrants with the same maturity as debt

Even though the Crouhy and Galai (1994) model is more realistic than the classical warrant valuation and the Schulz and Trautmann (1994) and Ukhov (2004) approaches, it still has two limitations: it only considers the case where warrants have longer maturity than debt and it is based on unobservable variables \((V^\prime _t\) and \(\sigma _{V^\prime })\). Abínzano and Navas (2013) complement the literature on warrant pricing studying the two other cases: \(T_D<T\) and \(T=T_D\). Moreover, following the insights of Ukhov (2004), they propose algorithms based only on observable variables for the three cases of maturity of warrants (being the case \(T_D>T\) an extension of the Crouhy and Galai (1994) model).

In this subsection, we extend the case with \(T=T_D\) to the CEV process. Thus, all the remaining assumptions of Crouhy and Galai (1994) are assumed to hold, except the maturity of warrants and debt (i.e., in this case, warrants and debt have the same maturity). Similarly to Crouhy and Galai (1994), we also consider a benchmark firm with the same investment policy as the underlying firm, but financed entirely by common stock, as given by Eq. (20). Following an identical reasoning which led to the expression of the warrant in the classical warrant valuation, we can write \(w_T\) as

where \(E_T\) is the value of equity at T—just after the maturity of debt and prior to the exercise of the warrants—given by \(E_T=\textrm{max}(V_T^\prime -F,0)\) and \(\lambda = 1/(N+kM)\). We can rewrite Eq. (30) as

Therefore, at time \(t=T\), the warrant holder receives the same payoff as the owner of \(\lambda\) European-style call option on \(kV_t^\prime\), with strike \(kF+NX\) and maturity at time T. Under the CEV process, the value of the warrant is given by:

The warrant expression given by Eq. (32) is a function of unobservable variables, \(V_t^\prime\) and \(\sigma _{V^\prime }\). To relate these variables to \(S_t\) and \(\sigma _S\), we follow the approach proposed by Ukhov (2004) defining \(\sigma _S=V_t^\prime /S_t\Delta _S\sigma _{V^\prime }\), where \(\Delta _S=\partial S_t/\partial V_t^\prime\). Since the firm value is now \(V_t^\prime =NS_t+Mw_t+D_t\), to obtain \(\Delta _S\) we have the following expression:

where \(\Delta _D=\partial D_t/\partial V_t^\prime\).

To compute \(\Delta _S\) we need to know \(\Delta _w\) and \(\Delta _D\). Following (Larguinho et al. (2013), Eq. A7) and (Dias et al. (2020), Corollary 1), we define \(\Delta _w\) as given by Eq. (15), where \(w_t\) is given by Eq. (32). To compute \(\Delta _D\), we first need to define \(D_t\). We know that at time \(T_D=T\), the debtholders receive \(\textrm{min}(F,V_T^\prime ) = F-\textrm{max}(F-V_T^\prime ,0)\). Thus, \(D_t\) can be written as

where \(p_t(A_t,K,T)\) is a put option on the asset price \(A_t\), with strike K and maturity at time T.

Armed with the expression of \(D_t\), we can compute \(\Delta _D\) following Larguinho et al. (2013), that is

Finally, the price of the warrant under the CEV process and using only observable variables is computed by:

1. Solving (numerically) the following system of nonlinear equations for \((V^{\prime *}_t,\sigma _{V^{\prime *}})\):

where \(c_t(A_t,K,T)\) is a call option on the asset price \(A_t\), with strike K and maturity at time T, \(w_t\) is given by Eq. (32) and

with \(\Delta _w\) and \(\Delta _D\) being the delta hedge of warrant and delta hedge of debt as given by Eqs. (16) and (35).

2. Substituting the variables \((V^{\prime *}_t,\sigma _{V^{\prime *}})\) obtained above into the following expression:

3.5 Levered warrant model for warrants with shorter maturity than debt

In this case, and as in Abínzano and Navas (2013), we first use the Crouhy and Galai (1994) model as an expression for the warrants’ value depending on unobservable variables \((V^\prime _t \text { and } \sigma _{V^\prime })\). Then, following Ukhov (2004), we relate the unobservable variables \(V_t^\prime\) and \(\sigma _{V^\prime }\) to observable variables \(S_t\) and \(\sigma _S\) using the expression

where \(S_t\) is given by Eq. (23).

The warrant pricing algorithm is as follows:

1. Solve (numerically) the following system of nonlinear equations for \((V_t^{\prime *}, \sigma _{V^\prime }^*)\):

with \(\bar{V}_T^\prime\) being the value of \(V_T^\prime\) that satisfies

2. The warrant price at time t \((<T)\) is given by

where \(D_t\) is calculated as

3.6 Levered warrant model for warrants with longer maturity than debt

In this particular case, we consider long-term warrants with maturity longer than debt’s expiration date, i.e. \(T>T_D\). The warrant holder has the right to pay X at time T and receive k shares, each one with a value \(V_T/(N+kM)\), where \(V_T\) is the value of the firm at time T. Following Crouhy and Galai (1994), we consider a benchmark firm with the same investment policy, but financed only by common stock, that is

At time \(t=T_D\), if the value of the levered firm is greater than the face value of the zero-coupon bond, F, the bondholders receive F whereas the shareholders and warrant holders receive the residual value of the company, that is \(V^\prime _{T_D}-F\). On the other hand, if the firm value is lower than the face value of the zero-coupon bond, shareholders and warrant holders get nothing (i.e., the firm defaults), while the bondholders get what is left of the company, \(V_{T_D}\). This can be summed up as follows:

In this connection, the firm value at time \(t=T\) can be defined in the following manner:

The warrants should be exercised only in the case \(k\frac{V^\prime _T+MX-F}{N+kM}\ge X\). Thus, through straightforward calculations, the warrant value at time \(t=T\) is as follows:

Working recursively, we can define \(w_{T_D}\) as:

Note that the benchmark firm volatility at time \(T_D\) is given by \(\sigma (V_{T_D}^\prime )={\delta V^\prime _{T_D}}^{\frac{\beta }{2}-1}\), with \(\delta =\sigma _{V^\prime }{V_t^\prime }^{1-\frac{\beta }{2}}\), for \(t<T_D\). Therefore, assuming that \(V_t^\prime\) follows a CEV process and there are no arbitrage opportunities, it follows that

where \(f(V^\prime _{T_D},T_D;V^\prime _t,t)\) is the probability density function of \(V^\prime _{T_D}\) conditional on \(V^\prime _t\).

Now that we have an expression relating the value of the warrant to \(V_t^\prime\) and \(\sigma _{V^\prime }\), we need to establish a relationship between observable variables and unobservable variables in order to implement Ukhov’s algorithm. Since the capital structure of the levered firm at any time prior to debt expiration consists of warrants, debt and common stock, we know that \(NS_t+Mw_t=V_t^\prime -D_t\) holds for all \(t<T_D\). Thus, we can look at the right-hand side of the equation as a call option on \(V^\prime\) at time t, with strike F and maturity at time \(T_D\) \((\ge t)\), because at time \(T_D\) the warrant holders and the shareholders will receive jointly \(V_{T_D}^\prime -F\) if \(V_{T_D}^\prime >F\) and zero otherwise. That is, \(NS_t+Mw_t=c_t(V^\prime _t,F,T_D)\).

The algorithm to compute the price of the warrant is as follows:

1. Solve (numerically) the following system of nonlinear equations for \((V^{\prime *}_t,\sigma _{V^\prime }^*)\):

2. The warrant price at time t, with \(t<T_D\), using \(V^{\prime *}_t\) and \(\sigma _{V_t^\prime }^*\) is obtained as

4 Numerical analysis

This section presents computational results for warrants prices under the CEV diffusion. To determine the implications of the correct specification of the underlying state variable process for the valuation of warrants, the obtained results under the CEV modeling setup are compared with the ones calculated via the lognormal model. In particular, we consider the following models on the computation of warrants prices: the Black and Scholes (1973) and Merton (1973) (BSM) stock option pricing model for the lognormal process and the Schroder (1989) and Heston et al. (2007) (SHLW) stock option pricing model for the CEV process, the classical warrant valuation model (CWM), the Schulz and Trautmann (1994) and Ukhov (2004) (STU) model, the classical warrant valuation model with debt (CWMD), the Crouhy and Galai (1994) (CG) model, and the levered warrant models for warrants with different maturities relative to debt.

To compute the warrants prices we borrow the models’ parameters from Abínzano and Navas (2013), but augmented by the \(\beta\) parameter. More specifically, we let \(N = 100\), \(S \in \{75,100,110\}\), \(M \in \{10,50,100\}\), \(k=1\), \(X=100\), \(\sigma _S\in \{0.25,0.40\}\), \(r=0.0488\), \(F=1000\) and \(\beta \in \{0,1,2,3\}\), where \(\beta = 2\) corresponds to the models presented in Abínzano and Navas (2013) under the lognormal assumption. With the three level of stock prices, we are able to value out-of-the-money (OTM), at-the-money (ATM) and in-the-money (ITM) warrants. It is also assumed a non-dividend paying stock. Following MacBeth and Merville (1980) and Davydov and Linetsky (2001), the scale parameter \(\delta\) is selected so that the initial instantaneous volatility is the same across different models.

When numerical procedures are necessary to compute the warrants prices—as in the case of the levered warrant models for warrants with longer and shorter maturities than debt—, we employ Monte Carlo simulation, more specifically, the Euler–Maruyama scheme to simulate the asset values under the CEV model.Footnote 9 In each of these cases, we use 1,000,000 paths and 1000 time-steps. We also use Monte Carlo simulation with the same number of paths and time-steps for the case of the levered warrant model based on unobservable variables when warrants have the same maturity as debt.

We construct three tables for the lognormal models based on the relationship between the maturities of warrants and debt. In case of the CEV model, we construct nine tables based on the different \(\beta\) parameters and the relationship between the maturities of debt and warrants, that is three tables for each case of maturity. Given space constraints, we only present here, as an example, Table 1 that contains the results for the case with \(T = T_D\) and \(\beta =0\). The remaining eleven tables are relegated to appendixes B, C and D of the supplementary file.

Each table has six panels, which reflect the two levels of volatility and three degrees of dilution. As mentioned before, warrant prices are obtained using six different models. The first column of each table shows the stock price, S, of the underlying firm. The second column uses the BSM formula in case of the lognormal process or SHLW stock option pricing formula in case of the CEV process to compute the warrant prices \(w_{BSM}\) and \(w_{SHLW}\), respectively. The third column uses the CWM to calculate the price of the warrant assuming that the firm has no debt. Since this model uses unobservable variables, we approximate the firm’s value by \(V_t = \widetilde{E}_t=NS_t + Mw_{BSM}\) for the lognormal model (\(\beta =2\)) and \(V_t = \widetilde{E}_t=NS_t + Mw_{SHLW}\) for the CEV model. In both cases, we approximate firm’s volatility by \(\sigma _V=\sigma _S\).

The fourth column uses the STU model to compute the warrant price. In this model, only observable variables are used. In the fifth column, we once again implement the CWM model, but now assuming that \(V_t =\widetilde{E}_t+Fe^{-rT_D}\). Thus, it is assumed that the investors ignore debt when valuing warrants but are able to obtain a good approximation of the firm value. The sixth column reports the prices obtained using the models proposed by Abínzano and Navas (2013) and Crouhy and Galai (1994) in case of \(\beta =2\), and the ones proposed in this paper under the CEV setup, which incorporate debt correctly but are based on unobservable variables.

Finally, columns 7–9 report the values obtained using the models proposed by Abínzano and Navas (2013) (for the lognormal process) and the models proposed in this paper under the CEV framework, all based only on observable variables. Column 7 reports the firm value, column 8 shows the firm volatility and column 9 documents the warrant price.

Additionally, we construct three tables (highlighted below) based on the relationship between the maturities of the debt and the warrants to illustrate the absolute percentage pricing errors the investor is subject if he/she incorrectly assumes the GBM for the state variable. For this purpose, we consider the models which incorporate debt correctly into the valuation process whether based on observable variables or not. All the numerical results are obtained through the Python programming language, version 3.7.4.

4.1 Warrants with the same maturity as debt

The prices of the warrants are obtained assuming that the debt has the same maturity as warrants, i.e., \(T=T_D=3\). Tables 1, B.1, B.2 and B.3 illustrate the computational results for warrants prices obtained for \(\beta \in \{0,1,2,3\}\), respectively. Table 2 gives the absolute value of the percentage difference between the GBM warrant price and the CEV warrant value relative to the GBM price.

We start our analysis by comparing the prices obtained under both diffusion processes (CEV and GBM). Examination of the data reveals that OTM (resp., ITM and ATM) call warrants under the CEV model with \(\beta \in \{0,1\}\) are worth less (resp., more) than under the lognormal model. Much more pronounced differences are revealed for OTM warrants. The differences in ATM call warrants are not all that significant when the volatility is low for \(\beta \in \{0,1\}\), but it becomes more significant for the high volatility case. We also note that the absolute percentage differences in OTM warrants decrease (resp., increase) as the proportional dilution rises for LWM1V (resp., LWM1S) when \(\beta < 2\) (see Table 2). Similarly, the absolute percentage pricing errors in ITM and ATM warrants increase as the dilution rises for both models when \(\beta < 2\).

If the evolution of the firm’s returns is characterized by an inverse leverage effect with \(\beta =3\), OTM (resp., ITM and ATM) warrants prices tend to be higher (resp., lower) under the CEV diffusion than under the lognormal model when the volatility is low. When the volatility is high, the prices of warrants, in general, (for all the levels of moneyness) under the CEV model are lower than under the GBM. For example, in Tables B.2 and B.3, panel B3 (high volatility, high dilution), we observe that prices of ITM warrants obtained through LWM1S under GBM and CEV models are, respectively, 39.7961 and 34.4344. The absolute percentage difference is \(13.47\%\) (see Table 2—\(\beta =3\), panel B3). The absolute percentage differences in OTM warrants prices tend to decrease (resp., increase) as the dilution rises for LWM1V (resp., LWM1S) when the volatility is low. When the volatility is high, the absolute percentage differences are more pronounced in the case of high dilution. After having showed the mispricing the investors are subject assuming the GBM for the underlying state variable, we proceed by comparing the prices computed using the different valuation models extended in this work to the CEV setup.

Comparing first the models with no debt (SHLW, CWM and STU, columns 2–4) across the tables, we find that the differences between prices predicted by these models are not very significant in most of the cases. However, in a few cases, the differences are pronounced. For example, in Table B.3, panel B3 (high volatility, high dilution), we observe that the prices of ITM warrants are, respectively, \(37.1853, 32.6824\text { and } 28.0258\). SHLW prices are not affected by dilution. Conversely, CWM prices always decrease with dilution while STU prices decrease more slowly when \(\beta \in \{0,1\}\) and somewhat faster when \(\beta =3\) (especially high volatility), or even increase slightly (for ITM and ATM warrants with \(\beta \in \{0,1\}\)). CWM prices are always lower than SHLW prices. CWM prices are also lower than STU prices in most of the cases, except the case of medium and high dilution (high volatility) when \(\beta =3\), where CWM prices are higher than STU prices. Finally, comparing STU and SHLW prices, we find that when \(\beta =3\), SHLW prices are always greater than STU prices. Nonetheless, when \(\beta \in \{0,1\}\), SHLW prices are slightly higher for OTM warrants and somewhat lower for ATM and ITM warrants than STU prices.

The CWMD model represents the first attempt to incorporate debt into the analysis. The assumption is that the investor can obtain a reasonable estimate of the firm value, but is unable to develop a model which incorporates debt correctly. Thus, the firm value is now higher and drives up the value of the warrant. CWMD prices always decrease with dilution. As the \(\beta\) parameter increases, CWMD prices increase for OTM warrants and decrease for ATM and ITM warrants. For instance, the prices of CWMD ITM warrants in panel B3 for the three beta values \((\beta \in \{0,1,3\})\) are, respectively, 43.9914, 41.8500 and 36.2870.

We now address the models where the debt is properly incorporated. To obtain the warrants prices using LWM1V, we first define the reference firm volatility as \(\sigma _{V^\prime }=\sigma _S\) and the initial value of the benchmark firm as \(V_t^\prime = \widetilde{E}_t + Fe^{-rT_D}\). Next, we simulate by Monte Carlo the value of \(V_t^\prime\) from \(t=0\) to \(t=T\). In each round, the warrant value at time \(t=T\) is computed as \(w_T=\lambda \textrm{max}(kV^\prime _T-kF-NX,0)\) (see Eq. (31)). The warrant price at the current time t is the mean of the discounted payoffs of the warrant. Note that \(V_t^\prime\) is simulated through Eq. (3). LWM1S prices are obtained by solving the system of Eq. (36) to obtain the values of unobservable variables and then by substituting them and the remaining inputs into Eq. (38).

From columns 6 and 9 across the tables, we find that LWM1V prices can be greater or smaller than LWM1S, and these differences are, sometimes, significant. For example, in panel B3 of Table B.1, the prices of ATM warrants for LWM1V and LWM1S are 30.8797 and 33.0027. The firm value and volatility consistent with the market data in the latter case are 14, 123.65 and 46.10%, respectively. When \(\beta \le 2\), its values may have a positive or negative impact on warrant prices. However, for a given warrant, the impact appears to be always monotonic, that is as \(\beta\) increases from 0 to 2, the value of warrant either increases monotonically or decreases monotonically. There are several points that are noteworthy to highlight comparing LWM1S with other pricing models in the tables. LWM1S prices can be higher or smaller than SHLW prices and STU prices; we obtain higher prices with LWM1S than with CWM; we always obtain lower prices with LWM1S than with CWMD.

To sum up, we have the following remarks from this subsection. Warrants prices always decrease with dilution for OTM warrants. The value of \(\beta\) may have a positive or negative impact on warrant prices, but it appears to be always monotonic (at least when \(\beta <2\)). The absolute value of the percentage difference between the CEV warrant prices and GBM warrant prices relative to GBM prices, at least for the models considered (LWM1V and LWM1S), are more significant for OTM warrants in most of the cases. In this sense, a misspecified value of \(\beta\) can lead the investor to significant pricing errors in various cases, especially for OTM and ITM warrants.

4.2 Warrants with shorter maturity than debt

This subsection addresses the case \(T < T_D\), where \(T = 1\) and \(T_D = 3\). Since the maturity of warrants is shorter, the prices are now, obviously, lower than in the previous subsection. Tables C.1, C.2, C.3 and C.4 display the computational results for warrants prices with \(\beta \in \{0,1,2,3\}\), respectively. Table 3 gives the absolute percentage difference between the CEV warrant price and GBM warrant price relative to GBM price for the CG model and the levered warrant model based on observable variables (LWM2S).

Analysing the tables, we find that OTM (resp., ITM and ATM) warrants prices are lower (resp., higher) under the CEV model with \(\beta \in \{0, 1\}\) than under the GBM. As in the previous case, the differences are much more pronounced in OTM warrants. For example, in Tables C.1 and C.3, panel A3 (low volatility, high dilution), the values of OTM warrants computed via LWM2S under CEV and under GBM are, respectively, 0.9950 and 1.4413. The absolute value of the percentage difference in this case is 30.96% (see Table 3, panel A3). From Table 3, we can see that the maximum percentage difference from the lognormal case when the market exhibits downward sloping volatility smile pattern (i.e., \(\beta < 2\)), for the set of parameters used, is about 33%, which is not negligible.

When \(\beta = 3\) and volatility is low, we obtain higher (resp., lower) prices under the CEV model for OTM (resp., ITM) warrants than under GBM. In case of ATM warrants, prices can be higher or lower under CEV than under GBM, but the difference is almost insignificant. This is to be expected as the \(\delta\) value is adjusted to the value of \(\beta\) such that the instantaneous volatility of the percentage change in asset values is identical for the CEV process with different \(\beta\) values. When \(\beta = 3\) and volatility is high, prices can be higher or lower under the CEV model than under GBM depending on the model (levered or unlevered), dilution and moneyness. Nevertheless, when volatility is high, the absolute percentage differences are very pronounced in case of high dilution, even for ATM warrants. For instance, in Tables C.3 and C.4, panel B3, the prices of an ATM warrant under GBM and CEV computed through LWM2S are, respectively, 17.9520 and 12.0469. Overall, the absolute percentage differences are very pronounced in several cases and this figure can be as high as 62.46% (see Table 3, panel B3). We now proceed with comparing the prices obtained via the different models extended in this paper to the CEV process.

As usual, we begin with the unlevered models (SHLW, CWM and STU). CWM prices are always lower than SHLW and STU prices. SHLW prices are lower than STU prices for ITM and ATM warrants when \(\beta \in \{0, 1\}\) and \(\beta = 3\), the latter case only when the volatility is low and dilution is low or medium. In all the other cases, SHLW prices are higher than STU prices (however, the differences are not very high). We move on to CWMD and find the prices to be, in general, greater than the prices obtained with the other models (recall that firm value under CWMD is higher than under other unlevered models).

Now, we compare the prices obtained using the models which incorporate debt correctly, that is CG and LWM2S. When implementing the CG model, we take \(V^\prime _t=\widetilde{E}_t+Fe^{-rT_D}\) as the initial value of the benchmark firm and \(\sigma _{V^\prime }=\sigma _S\) as the initial volatility of firm returns. We then find the reference asset value, \({\bar{V}^\prime _T}\), above which the warrants are exercised. That is, we find the value of \(V^\prime _T\) that satisfies \([c_T(V^\prime _T+100M,1000,3)]/(N+M)=100\). Note that the volatility in this case is \(\sigma (V^\prime _T)={\delta V^\prime _T}^{\frac{\beta }{2}-1}\), where \(\delta =\sigma _{V^\prime }{V^\prime _t}^{1-\frac{\beta }{2}}\). Using \(\bar{V}^\prime _T\) obtained, we simulate by Monte Carlo (see Eq. (3)) the value of the benchmark firm, \(V^\prime _t\), from \(t=0\) to \(t=T\). In each round, the share value is obtained using the Eq. (22), and \(w_T=kS_T-X\) if warrants are exercised or \(w_T=0\) if warrants are not exercised. After a simulation wih 1, 000, 000 paths and 1, 000 time-steps, we obtain the values of \(S_t\) and \(w_t\). When implementing LWM2S, we use the simulation described above and solve the system of equations given by (40) such that the value of \(S_t\) given by the simulation coincides with the known value of \(S_t\) and the expression of \(\sigma _S\) is satisfied. LWM2S prices can be greater or lower than CG prices. However, LWM2S prices are always greater than CG prices when volatility is high and dilution is medium or high.

Comparing LWM2S with other pricing models, we find that LWM2S prices can be greater or lower than SHLW prices, and when \(\beta =3\), these differences are very pronounced. For example, in Table C.4, panel B3, the prices of ITM warrants computed via SHLW and LWM2S are, respectively, 24.3436 and 18.6631. This is to be expected as SHLW ignores dilution. CWM prices are lower than LWM2S prices when \(\beta \in \{0,1\}\). When \(\beta =3\), CWM prices can be greater or lower than LWM2S prices. The prices obtained using STU also can be greater or lower than the ones obtained using LWM2S. Finally, we obtain higher prices with CWMD than with LWM2S in most of the cases. In summary, like in the previous subsection, prices always decrease with dilution for OTM warrants. In case of ITM and ATM warrants, prices can increase or decrease with dilution. Prices can be greater or lower under the CEV model than under the lognormal model depending on several factors, viz. moneyness, dilution, volatility, leverage, etc. As before, the elasticity parameter, \(\beta\), has a significant impact on the warrant value and, therefore, a misspecified value of \(\beta\) can lead the investor to significant pricing errors (especially for OTM warrants).

4.3 Warrants with longer maturity than debt

Now, we assume \(T=3\) and \(T_D=1\). Tables D.1, D.2, D.3 and D.4 show the computational results for warrants prices under the CEV model for \(\beta \in \{0,1,2,3\}\), respectively. Table 4 illustrates the absolute percentage difference between the CEV warrants prices and GBM warrants prices relative to GBM prices for the levered warrants models based on unobservable variables (LWM3V) and on observable variables (LWM3S).

As in the previous subsections, we start by comparing the results under both diffusion processes. The results, once again, indicate that OTM (resp. ITM and ATM) warrants are worth less (resp. more) under the CEV model than under GBM when \(\beta <2\). On the other hand, when \(\beta =3\), prices under CEV can be higher or lower than prices under GBM, depending on volatility and the specific model being used. For example, in Tables D.3 and D.4, panel B1, the prices of an OTM warrant computed via LWM3V and LWM3S under GBM are, respectively 18.5087 and 16.7596, and under CEV are 18.3539 and 17.2418. We also note that the absolute value of percentage difference between CEV prices and GBM prices relative to GBM prices for ATM warrants is significant in various a cases (especially high dilution).

We now compare the prices obtained through different valuation models under the CEV setup. Since the maturity of warrants is the same as in Sect. 4.1, warrants prices in this section obtained through unlevered warrants models (SHLW, CWM and STU) are the same as the ones obtained in that subsection. Moreover, since the maturity of the debt is now shorter, both firm value and debt value are now higher which may explain why the models incorporating debt produce higher values in this subsection than in Sect. 4.1. LWM3V prices are obtained in the following manner. First, we take \(V^\prime _t=\widetilde{E}+Fe^{-rT_D}\) and \(\sigma _{V^\prime }=\sigma _S\) as the initial value of the benchmark firm and its volatility, respectively. Next, we simulate by Monte Carlo the value of \(V_t^\prime\) from \(t=0\) to \(t=T_D\). In each run, the warrant value at time \(t=T_D\) is determined as a function of whether the value of \(V^\prime _{T_D}\) given by the simulation is above or below F, for which we use the expression of \(w_T\) given by (47).

To compute prices using LWM3S, we use the simulation described above and solve the system of nonlinear equations given by (50) such that the value of \(S_t\) given by the simulation coincides with the known value of \(S_t\) and the expression of \(\sigma _S\) is satisfied. Analyzing the data, we find that when \(\beta \in \{0,1\}\), LWM3S underprices LWM3V when dilution is low and overprices it when dilution is medium or high. The absolute difference between the models is more pronounced when LWM3S overprices than when it underprices. When \(\beta =3\), LWM3S only overprices when volatility is low and dilution is medium or high. In all the other cases (i.e., low volatility and low dilution or high volatility), LWM3S always underprices LWM3V, but the differences are not very high. We also find that LWM3S prices are always higher than SHLW, CWM and STU prices when \(\beta <2\). When \(\beta =3\), LWM3S seems to underprice SHLW more often and overprice CWM and STU more frequently. CWMD, in general, overprices other pricing models. Finally, warrants prices may either increase or decrease with dilution, but the impact appears to be always monotonic. In summary, when \(\beta \in \{0,1\}\), OTM warrants prices are lower under the CEV model than under GBM and ITM and ATM are higher. From the results, we conclude that the introduction of debt into the models plays an important role on warrant pricing and, therefore, this variable should be taken into account when valuing warrants. The absolute percentage pricing differences found in this paper could have been higher had different set of parameters (eg., higher \(\beta\)s in modulus, higher stock price, etc.) been used. In this sense, we can conclude that an incorrect specification of the underlying variable may lead investors to significant pricing errors.

5 Concluding remarks

This paper is concerned with the pricing of levered warrants under a state dependent volatility process, namely the CEV process. It complements the literature on warrant pricing since much of the previous work assumes that the underlying state variable follows a GBM process. We derive pricing solutions for warrants in closed-form for the case where the maturity of the warrant is the same as the maturity of the debt. Like the GBM case, when the maturity of warrants differs from the maturity of the debt, prices can be computed numerically. Given the fact that both the lognormal and CEV models were calibrated so that the instantaneous volatility at the initial firm value is the same across different models, the differences found throughout the numerical analysis stem purely from the relationship between volatility and price levels.

We conclude that, in general, investors are subject to a significative pricing bias assuming the GBM for the state variable and, thus, the CEV process should be preferred when valuing warrants. The relative difference between CEV prices and GBM prices (with GBM prices as reference) is more pronounced for OTM warrants. Since warrants prices are sensitive to the volatility specification of the CEV process, the pricing errors may be even larger if we assume different elasticity parameters. Dilution may have either a positive or negative impact on warrants prices, but the impact seems to be always monotonic. The debt assumes an important role on warrant pricing and, thus, models consistent with market data can be used to price warrants taking this variable correctly into account. Finally, the pricing bias problems discussed in the Introduction section of this paper regarding the Hertz company would be reduced had our formulas been available and used to value warrants.

Notes

Units are bundles of common stock and warrants sold together as a package.

See Veld (2003) for a general overview of the literature on empirical research under alternative stochastic processes.

A similar conclusion was drawn by Gemmill and Thomas (1997) for warrants on the London Stock Exchange.

It is important to point out that, even in the cases of analytical solutions (warrants with the same maturity as debt), we need numerical procedures to obtain the value of unobservable variables. Also note that unlike Lauterbach and Schultz (1990), who consider a firm financed only by equity, in this paper we incorporate debt correctly into the valuation process.

Note that since we are valuing the warrants at the current time t, the scale parameter \(\delta\) is selected so that \(\sigma _V=\sigma (V_t)\).

We recall that Eq. (8) corrects the misprint error of (2007, Page 367) highlighted in Veestraeten (2017) and Dias et al. (2020). Note also that \(\Gamma (v,x)/\Gamma (v)\) can be alternatively written as Q(2y; 2v, 0)—see, for instance, Dias et al. (2020, Footnote 5). As in Larguinho et al. (2013), Ruas et al. (2013), Dias et al. (2015), Nunes et al. (2015) and Dias et al. (2020), we adopt the Benton and Krishnamoorthy (2003) algorithm for computing the required non-central chi-square distributions.

Appendix A of the supplementary file contains further details on the derivation of this relation under the CEV model.

This is consistent with the well-known capital structure irrelevance of Modigliani and Miller (1958) under the assumption of perfect capital markets.

It is noteworthy to emphasize that numerical procedures are necessary in the three cases of maturities for the computation of values of unobservable variables (for models based on observable variables). However, when we mention numerical procedures here, we are referring to the ones implicit in the warrant formula itself and not in the approach proposed by Ukhov (2004).

References

Abínzano, I., & Navas, J. F. (2013). Pricing levered warrants with dilution using observable variables. Quantitative Finance, 13, 1199–1209.

Abramowitz, M., & Stegun, I. A. (1972). Handbook of mathematical functions. Dover.

Bajo, E., & Barbi, M. (2010). The risk-shifting effect and the value of a warrant. Quantitative Finance, 10, 1203–1213.

Bakshi, G., Crosby, J., & Gao, X. (2022). Dark matter in (volatility and) equity option risk premiums. Operations Research, 70, 3108–3124.

Beckers, S. (1980). The constant elasticity of variance model and its implications for option pricing. Journal of Finance, 35, 661–673.

Bekaert, G., & Wu, G. (2000). Asymmetry volatility and risk in equity markets. Review of Financial Studies, 13, 1–42.

Benton, D., & Krishnamoorthy, K. (2003). Computing discrete mixtures of continuous distributions: Noncentral chisquare, noncentral t and the distribution of the square of the sample multiple correlation coefficient. Comput Stat Data Anal, 43, 249–267.

Black, F., & Scholes, M. (1973). The pricing of options and corporate liabilities. Journal of Political Economy, 81, 637–654.

Broadie, M., & Kaya, Ö. (2006). Exact simulation of stochastic volatility and other affine jump diffusion processes. Operations Research, 54, 217–231.

Byoun, S., & Moore, W. T. (2003). Stock versus stock-warrant units: Evidence from seasoned offerings. Journal of Corporate Finance, 9, 575–590.

Chang, E. C., Luo, X., Shi, L., & Zhang, J. E. (2013). Is warrant really a derivative? Evidence from the Chinese warrant market. Journal of Financial Markets, 16, 165–193.

Choi, J., & Richardson, M. (2016). The volatility of a firm’s assets and the leverage effect. Journal of Financial Economics, 121, 254–277.

Christie, A. A. (1982). The stochastic behavior of common stock variances: Value, leverage and interest rate effects. Journal of Financial Economics, 10, 407–432.

Chuang, Y.-W., Tsai, W.-C., Weng, P.-S., & Yin, C. (2021). Do put warrants unwind short-sale restrictions? Further evidence from the Taiwan stock exchange. Journal of Futures Markets, 41, 325–348.

Cox, J. C. (1975). Notes on option pricing I: Constant elasticity of variance diffusions. Journal of Portfolio Management, 23(1996), 15–17.

Cox, J. C., & Ross, S. A. (1976). The valuation of options for alternative stochastic processes. Journal of Financial Economics, 3, 145–166.

Crouhy, M., & Galai, D. (1994). The interaction between the financial and investment decisions of the firm: The case of issuing warrants in a levered firm. Journal of Banking and Finance, 18, 861–880.

Davydov, D., & Linetsky, V. (2001). Pricing and hedging path-dependent options under the CEV process. Management Science Series A-theory, 47, 949–965.

Dennis, P., & Mayhew, S. (2002). Risk-neutral skewness: Evidence from stock options. Journal of Financial and Quantitative Analysis, 37, 471–493.

Dias, J. C., & Nunes, J. P. (2011). Pricing real options under the constant elasticity of variance diffusion. Journal of Futures Markets, 31, 230–250.

Dias, J. C., Nunes, J. P., & Cruz, A. (2020). A note on options and bubbles under the CEV Model: Implications for pricing and hedging. Review of Derivatives Research, 23, 249–272.

Dias, J. C., Nunes, J. P., & Ruas, J. P. (2015). Pricing and static hedging of European-style double barrier options under the jump to default extended CEV model. Quantitative Finance, 15, 1995–2010.

Dunbar, C. G. (1995). The use of warrants as underwriter compensation in initial public offerings. Journal of Financial Economics, 38, 59–78.

Emanuel, D. C., & MacBeth, J. D. (1982). Further results on the constant elasticity of variance call option pricing model. Journal of Financial and Quantitative Analysis, 17, 533–554.

Gajewski, J.-F., Ginglinger, E., & Lasfer, M. (2007). Why do companies include warrants in seasoned equity offerings? Journal of Corporate Finance, 13, 25–42.

Galai, D., & Schneller, M. I. (1978). Pricing of warrants and the value of the firm. Journal of Finance, 33, 1333–1342.

Garner, J. L., & Marshall, B. B. (2014). Underwriter compensation structure: Can it really bond underwriters? Financial Review, 49, 21–48.

Gemmill, G., & Thomas, D. (1997). Warrants on the London stock exchange: Pricing biases and investor confusion. European Finance Review, 1, 31–49.

Handley, J. C. (2002). On the valuation of warrants. Journal of Futures Markets, 22, 765–782.

Hauser, S., & Lauterbach, B. (1997). The relative performance of five alternative warrant pricing models. Financial Analysts Journal, 53, 55–61.

Heston, S. L. (1993). A closed-form solution for options with stochastic volatility with applications to bond and currency options. Review of Financial Studies, 6, 327–343.

Heston, S. L., Loewenstein, M., & Willard, G. A. (2007). Options and bubbles. Review of Financial Studies, 20, 359–390.

Howe, J. S., & Olsen, B. C. (2009). Security choice and corporate governance. European Financial Management, 15, 814–843.

Ingersoll, J. E. Jr. (1987). Theory of financial decision making. Rowman and Littlefield Publishers.

Jackwerth, J. C., & Rubinstein, M. (1996). Recovering probability distributions from option prices. Journal of Finance, 51, 1611–1631.

Johnson, N. L., Samuel, K., & Balakrishnan, N. (1995). Continuous univariate distributions (2nd ed., Vol. 2). Wiley.

Khurshed, A., Kostas, D., & Saadouni, B. (2016). Warrants in underwritten IPOs: The alternative investment market (AIM) experience. Journal of Corporate Finance, 40, 97–109.

Kloeden, P. E., & Platen, E. (1992). Numerical solution of stochastic differential equations. Springer-Verlag.

Larguinho, M., Dias, J. C., & Braumann, C. A. (2013). On the computation of option prices and Greeks under the CEV model. Quantitative Finance, 13, 907–917.

Lauterbach, B., & Schultz, P. (1990). Pricing warrants: An empirical study of the Black–Scholes model and its alternatives. Journal of Finance, 45, 1181–1209.

Lindsay, A. E., & Brecher, D. R. (2012). Simulation of the CEV Process and the Local Martingale Property. Mathematics and Computers in Simulation, 82, 868–878.

MacBeth, J. D., & Merville, L. J. (1980). Tests of the Black–Scholes and cox call option valuation models. Journal of Finance, 35, 285–301.

Merton, R. C. (1973). Theory of rational option pricing. Bell Journal of Economics and Management Science, 4, 141–183.

Modigliani, F., & Miller, M. H. (1958). The cost of capital, corporation finance and the theory of investment. American Economic Review, 48, 261–297.

Nunes, J. P., Ruas, J. P., & Dias, J. C. (2015). Pricing and static hedging of American-style knock-in options on defaultable stocks. Journal of Banking and Finance, 58, 343–360.

Ruas, J. P., Dias, J. C., & Nunes, J. P. (2013). Pricing and Static Hedging of American options under the jump to default Extended CEV model. Journal of Banking and Finance, 37, 4059–4072.

Schroder, M. (1989). Computing the constant elasticity of variance option pricing formula. Journal of Finance, 44, 211–219.

Schultz, P. (1993). Unit initial public offerings: A form of staged financing. Journal of Financial Economics, 34, 199–229.

Schulz, G. U., & Trautmann, S. (1994). Robustness of option-like warrant valuation. Journal of Banking and Finance, 18, 841–859.

Sidenius, J. (1996). Warrant pricing—is dilution a delusion? Financial Analysts Journal, 52, 77–80.

Suchard, J.-A. (2005). The use of stand alone warrants as unique capital raising instruments. Journal of Banking and Finance, 29, 1095–1112.

Ukhov, A. D. (2004). Warrant pricing using observable variables. Journal of Financial Research, 27, 329–339.

Veestraeten, D. (2017). On the multiplicity of option prices under CEV with positive elasticity of variance. Review of Derivatives Research, 20, 1–13.

Veld, C. (2003). Warrant pricing: A review of empirical research. European Journal of Finance, 9, 61–91.

Funding

Open access funding provided by FCT|FCCN (b-on). This work was supported by Fundação para a Ciência e Tecnologia, grant 2022.11993.BD.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary Information

Below is the link to the electronic supplementary material.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Glória, C.M., Dias, J.C. & Cruz, A. Pricing levered warrants under the CEV diffusion model. Rev Deriv Res 27, 55–84 (2024). https://doi.org/10.1007/s11147-023-09199-1

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11147-023-09199-1