Abstract

Achieving the Paris Agreement’s global temperature goal of keeping warming well below 2 °C and ideally 1.5 °C requires limiting fossil fuel production. In the United Nations climate change negotiations, this need is only beginning to be acknowledged. Nevertheless, as some countries have already adopted supply-side climate policies, initial cooperative activities have started, and calls grow for a fossil fuel treaty, questions arise about the prospects and possible effects of international cooperation on limiting fossil fuel supply. Combining qualitative insights on possible participants in a supply-side coalition with a quantitative analysis based on integrated assessment general equilibrium modelling, this article addresses these questions. Through k-means clustering based on fossil reserves per capita, fossil fuel rents and existing supply-side policies, we first identify which (groups of) countries are most likely to lead the formation of an international supply-side coalition, and which (groups of) countries are likely to follow. Drawing on these insights, we develop several scenarios for the evolution of international supply-side coalitions and compare these to a business-as-usual scenario. By doing so, we demonstrate the global and regional environmental, trade and macroeconomic effects of international cooperation on limiting fossil fuel supply and combining fossil supply restrictions with carbon pricing to meet the Paris goals. Our findings underscore the importance of pursuing supply-side and ambitious demand-side climate policies in parallel, and identify the scope and coverage, size of the coalition, and incentives for participation as key design elements for an international supply-side coalition.

Similar content being viewed by others

1 Introduction

Moving away from fossil fuel-based energy systems is imperative if we are to effectively tackle the climate crisis. The synthesis report of the Intergovernmental Panel on Climate Change’s (IPCC) Sixth Assessment cycle found that “projected CO2 [carbon dioxide] emissions from existing fossil fuel infrastructure without additional abatement would exceed the remaining carbon budget for 1.5 °C” (IPCC, 2023, 20). Two years earlier, the Production Gap Report found that “fossil fuel production must start declining immediately and steeply to be consistent with limiting long-term warming to 1.5 °C” (SEI et al., 2021, 3), and the International Energy Agency posited that “[t]here are no new oil and gas fields approved for development in our [1.5 °C] pathway, and no new coal mines or mine extensions are required” (IEA, 2021a, 21).

While international climate change negotiations for many years ignored the necessity to tackle fossil fuels, in no small part due to resistance by major fossil fuel producers (Depledge, 2008), there are signs of change. During the 2021 United Nations Framework Convention on Climate Change (UNFCCC) Conference of the Parties (COP26) in Glasgow, Parties committed to “[accelerate] efforts towards the phasedown of unabated coal power and phase-out of inefficient fossil fuel subsidies …” (UNFCCC, 2022, para. 36; see van Asselt & Green, 2022). One year later, at COP27 in Sharm El-Sheikh, some Parties, led by India, sought to include a call for phasing out all fossil fuels in a COP decision. Although they failed to do so (Lewis et al., 2022), at COP28 parties included a call for “transitioning away from fossil fuels in energy systems” (UNFCCC, 2023, para. 28).

In the meantime, some countries have moved ahead by adopting climate-motivated policies that restrict the supply of fossil fuels. These include moratoria and bans on the extraction of coal, oil and/or gas, phasing out subsidies for fossil fuel production and restrictions on fossil fuel finance (Lazarus & van Asselt, 2018). Although such unilateral policies signal countries’ willingness to restrict fossil fuel supply to achieve their climate change goals, they may lead to negative spill-over effects, with restrictions on production in one jurisdiction offset by an increase elsewhere (Erickson & Lazarus, 2014). The extent to which such leakage effects materialise remains debated (e.g., Collier & Venables, 2014), but they could be counteracted through international cooperation (Harstad, 2012). Moreover, international cooperation offers a way for countries to support each other to plan for a just transition away from fossil fuels, and thereby avoid stranded assets and stranded nations (Bos & Gupta, 2018).

In recent years, international cooperative initiatives on supply-side climate policy have been launched outside the UNFCCC context. In 2021, several countries, led by Denmark, launched an initiative aimed at phasing out oil and gas production, the Beyond Oil and Gas Alliance (BOGA) (BOGA, 2023). Similarly, fossil fuels are targeted by the Powering Past Coal Alliance (PPCA), led by the United Kingdom and Canada, which seeks to phase out coal-fired power—though this initiative is silent about coal mining (PPCA, 2023). In parallel, there is a vibrant civil society-led campaign for a Fossil Fuel Non-Proliferation Treaty, which would halt new fossil fuel production, phase out existing production, and offer support for a clean energy transition. By the end of 2023, several small island nations and one fossil fuel producer (Colombia) had endorsed the idea of such a treaty (Fossil Fuel Non-Proliferation Treaty, 2023).

Against this backdrop, researchers have begun to examine the possible design of an international agreement on fossil fuel supply (Burke & Fishel, 2020; Newell & Simms, 2020; Newell et al., 2022; van Asselt & Newell, 2022). Although such studies yield insights into how international cooperation would ideally look like, they do not offer details of the possible effects of such cooperation. Furthermore, while studies have looked at the likelihood of supply-side restrictions on fossil fuels at the domestic level (Lujala et al., 2022), and identified which countries are likely to join a supply-side coalition (Le Billon et al., 2022), no study has linked the likelihood of countries joining a supply-side coalition to the design of such a coalition. Other researchers have examined the impacts of fossil fuel extraction bans using four Integrated Assessment Models (IAMs) in idealised settings (Andreoni et al., 2023). However, to date such studies have failed to account for real-world policy barriers for supply-side coalitions and have not provided detailed quantification of the macroeconomic impacts of such strategies. Here we fill this gap by: (1) analysing the factors influencing countries’ willingness to join a fossil fuel supply-side coalition; (2) using the results of this analysis to develop real-world and policy-relevant scenarios as input into a comprehensive multi-sectoral, multi-regional general equilibrium model (GEM-E3) (Paroussos et al., 2020) to assess the macro-economic impacts of supply-side policies; and (3) provide a detailed analysis of GDP impacts of supply- and demand-side climate policies in major economies on the global level.

The article is structured as follows. First, the article analyses factors that may affect the likelihood of countries joining an international supply-side coalition, with a view to identifying possible participants (Sect. 2). The article then explores several scenarios for the development of an international supply-side coalition, and identifies the main environmental and macroeconomic effects in these scenarios (Sect. 3). Next, the article discusses the implications for further international cooperation on supply-side climate policy (Sect. 4), before drawing conclusions (Sect. 5).

2 Participation in an international supply-side coalition

2.1 International cooperation on fossil fuel supply

International cooperation on fossil fuel supply can take different forms. Van Asselt and Newell (2022) distinguish between two ideal-type models. First, under a “club model”, several like-minded countries come together to develop a non-legally binding international agreement on restricting fossil fuel production. This would allow so-called first-mover countries (e.g., Belize and Spain, which have already adopted supply-side policies; see Carter & McKenzie, 2020) to flexibly establish institutional arrangements and streamline further negotiations. Moreover, the club model could accommodate contributions to move away from fossil fuels by subnational and non-state actors, such as cities, regions, NGOs, and businesses. Second, under the “treaty model”, a greater number of participants would sign up to a legally binding treaty to restrict fossil fuel production. This model, foreseen by proponents of a Fossil Fuel Non-Proliferation Treaty and a Coal Elimination Treaty, is characterised by a high degree of institutionalisation, including a decision-making body and a dedicated secretariat (Burke & Fishel, 2020; Newell & Simms, 2020; Newell et al., 2022). Although a club arrangement may be faster to negotiate and allows for flexibility, it would not be legally binding and lack a clear enforcement mechanism. Moreover, greater participation in a treaty would—all else being equal—lead to deeper cuts in fossil fuel production. Having said that, van Asselt and Newell (2022) conclude that a club would likely be a stepping stone towards a multilateral supply-side agreement.

A crucial first question for any form of international cooperation is who would—and should—participate. Countries may have different reasons for participating in—or opting out of—an international agreement. Nations that are highly vulnerable to the impacts of climate change, such as Least Developed Countries and Small Island Developing States, may want to join a supply-side coalition because they consider phasing out fossil fuel production as crucial for their future, and because many such countries produce relatively small (if any) amounts of fossil fuels (Le Billon et al., 2022). For example, in March 2023, six Pacific Island nations launched the Port Vila Call for a Just Transition to a Fossil Fuel Free Pacific, in which they appealed for a Fossil Fuel Non-Proliferation Treaty (Port Vila Call, 2023). Similarly, some “first movers” can also be considered likely participants, especially if an international coalition does not require them to go beyond what they have already implemented domestically. By contrast, fossil fuel producers and countries with large hydrocarbon reserves and resources are generally considered the least likely to join supply-side coalitions (Andreoni et al., 2023; Carter & McKenzie, 2020; Gaulin & Le Billon, 2020).

Seeking to support these assumptions about participation with data, Lujala et al. (2022) analyse the likelihood of countries adopting supply-side constraint initiatives based on a combination of fossil fuel, economic, institutional, and climate-related factors and, on that basis, identify the likelihood of countries joining a supply-side coalition (Le Billon et al., 2022). First, they account for the importance of the fossil fuel sector in terms of rents and reserves in each country. Second, they consider economic factors such as levels of national income and debt. Third, they consider the institutional drivers of democracy, corruption, and post-conflict contexts. Finally, they consider vulnerability to climate change. Similar to Carter and McKenzie (2020), they find that countries with higher levels of fossil fuel rents are less likely to adopt constraints to the production of fossil fuels. Furthermore, members of the Organization of the Petroleum Exporting Countries (OPEC) are less likely to adopt ambitious supply-side constraints, while countries with a strong civil society that supports supply-side policies are more likely to support specific supply-side policies.

Building on these studies, and with a view to providing input into the modelling presented in Sect. 3, we have clustered countries according to the likelihood of joining a supply-side coalition. Section 2.2 explains how we have conducted this analysis, and presents the country-region clusters.

2.2 Clustering countries according to likelihood of joining a supply-side coalition

To subdivide countries into groupings based on their likelihood to join a supply-side coalition, we conduct a k-means cluster analysis (Kaufman & Rousseeuw, 2005), which allows us to identify variation in the economic, structural, and policy characteristics of GEM-E3 model countries and regions (see Fragkos & Fragkiadakis, 2022; and Annex Table A1). A cluster analysis has three key advantages. First, clustering is a reliable and widely used method to analyse aggregate characteristics and divide observations into mutually exclusive groups (Grimmer et al., 2021). Grouping country-regions based on other methods along several variables would require us to decide on cut-off points and potentially lead to subjective results. Second, cluster analysis helps reveal hidden or non-obvious patterns within the data that may not be apparent through visual inspection alone. Finally, cluster analysis results are reproducible, meaning that different analysts or researchers applying the same algorithm to the same dataset should arrive at similar clustering results.

We considered k-means clustering appropriate given the literature on comparative politics (Ahlquist & Breunig, 2009; Wolfson et al., 2004) and the continuous nature of the data. We draw on three variables to organise countries into groups. Drawing on previous literature (Guy et al., 2023), we organise countries into clusters that we rank by the standardised average weighted value of each variable, namely fossil fuel reserves (weight 3), existence of national supply-side policies (weight 2) and fossil fuel rents (weight 1). Based on the average values for each variable, we differentiate each group by their likelihood of joining a supply-side coalition. For simplicity’s sake, we refer to these groups as “Frontrunners”, “Followers”, “Laggards”, and “Reluctants”, respectively.

First, previous literature suggests that having large national fossil fuel reserves is one of the key impediments to international cooperation on fossil fuel supply (Carter & McKenzie, 2020; Gaulin & Le Billon, 2020). Countries that have large hydrocarbon reserves will be less inclined to join a supply-side coalition as the value of the reserves would likely be foregone, while countries without them may be more amenable to joining. Reserves are assigned the highest weight since we are interested in forward-thinking policy planning, and reserves constitute a strong disincentive to restrict fossil fuel production due to the risk of stranded assets (Ansari & Holz, 2020; Hansen, 2022). We account for fossil fuel reserves based on 2020 data from the US Energy Information Administration (EIA, 2023). We used data on the reserves of oil, coal, and total fossil fuels based on three key variables: (1) the reserves are measured in terms of proven recoverable reserves of barrels of oil (billions) or coal (million short tons); (2) we account for the total size of regional fossil fuel reserves by calculating their gross aggregated energy content in Exajoules (EJ); and (3) we measure all reserves per capita (millions) based on population data from the World Bank (2023a) and transform based on the natural logarithm to adjust for the size of the regions.

Second, following Lujala et al. (2022), who suggest that domestic policy initiatives may reflect appetite for participation in an eventual international supply-side agreement, we also consider national fossil fuel supply-side policies. We include them as a key indication of a country’s political and institutional willingness to cooperate on an international supply-side treaty. We account for the policies using Fossil Fuel Policy Tracker (2023) data on bans, moratoria, and limitations at the national level for fossil fuel supply.Footnote 1 The variable is expressed as dichotomous, whether a policy is in place (1 = yes) or not (0 = no), which is measured as an average across the country-region. The variable for all fossil fuels is expressed as an average of policies across coal and oil/gas.

Third, existing research suggests that fossil fuel rents are significant supply-side policy barriers (Guy et al., 2023, Lamb & Minx, 2020). We control for current economic rents from fossil fuels as dependency to the fossil fuel sector may deter further action due to economic disincentives (Dietz et al., 2020; Van de Graaf & Verbruggen, 2015). We employ fossil fuel rents as a share of gross domestic product (GDP) based on 2020 World Bank data for each fossil fuel, and as a total of fossil fuels. Lastly, while we concur with Lujala et al. (2022) that climate vulnerability can be another factor influencing the adoption of supply-side policies, uncertainties about future climate impacts can still be very large. Moreover, climate vulnerability may be associated with confounders, such as economic marginalisation and weak infrastructure. For these reasons, we did not consider this factor.

Since our data is continuous, we decided to employ k-means clustering (instead of hierarchical cluster analysis, which is more appropriate for categorical data), which was conducted in R. K-means clustering is an unsupervised method that starts by randomly selecting k-cluster centres in the feature space. It assigns each data point to the nearest cluster centre based on Euclidean distance. The result is a set of k-clusters, where each data point is assigned to the cluster with the closest centre, aiming to minimise the within-cluster sum of squares. The appropriate number of clusters is chosen by the researcher based on the “elbow” method, which indicates the point where additional clusters result in diminishing returns. Alternatively, the “silhouette” method measures the similarity of data points within each cluster compared to other clusters, determining the ideal number of clusters by maximising the silhouette coefficient. We decided on four clusters given the results of the “elbow” and the “silhouette” method.

The make-up of the clusters differs depending on the specific fossil fuel that is considered (see Table 3). For instance, in the analysis of total fossil fuels, we find that the cluster consisting of EU28, China, Indonesia, South Africa, the USA, and the “Rest of the World” are most likely to lead a supply-side coalition due to relatively low per capita reserves of fossil fuels, existing policies and relatively low fossil fuel rents. Argentina, Brazil, India, Japan, Korea, Mexico, and Turkey, which have small per capita reserves, no supply-side policies, and low fossil fuel rents, are classified as “Followers”. The following group of “Laggards” consists of Canada, Oceania (Australia and New Zealand), and the “Rest of Europe” (including Norway), which have larger per capita reserves, have adopted supply-side policies, and relatively low fossil fuel rents. The cluster comprising Russia, Saudi Arabia, and the “Rest of energy producers” is the least likely to join a supply-side coalition for all fossil fuels (i.e., “Reluctants”) since its members boast very large per capita reserves, have shown little willingness to restrict fossil fuel production, and fossil fuel rents make up a large part of their economy. The results of the scoring exercise fed into the policy scenarios (see Sect. 3).

Plot A presents principal component analysis (PCA) results for oil, B for coal, and C for all fossil fuels. In each plot, the colours correspond to the likelihood of that cluster joining a supply-side coalition. The clusters are coded as “Frontrunners” (dark green), “Followers” (light green), “Laggards” (orange), and “Reluctants” (dark red). For additional information, including country-region codes, data used in the cluster analysis, variable averages for clusters, and further information on Fig. 1, see the Supplementary Materials.

Cluster plots for all fossil fuels, oil, and coal

3 The environmental and macroeconomic effects of international supply-side coalitions

3.1 Methods

To quantify the macroeconomic impacts of supply-side policies, we use the recursive dynamic CGE model GEM-E3, which simultaneously represents 20 regions and 65 production sectors (Paroussos et al., 2020). It is a comprehensive model of the global economy, covering interlinkages between productive sectors, consumption, price formation of commodities, labour and capital, trade and investment dynamics. GEM-E3 formulates the supply and demand behaviour of economic agents with market-derived prices to clear markets, allowing for a consistent evaluation of distributional effects of policies. Industries operate within a market regime with perfect competition to maximise profits. Production functions consider the possibilities of substitution between capital, labour, energy, and materials in each sector. Household demand, savings, and labour supply are derived from utility maximisation using a linear expenditure system formulation. All regions and sectors are linked through endogenous bilateral trade flows based on the hypothesis that domestic and imported goods are imperfect substitutes (Armington, 1969). GEM-E3 is calibrated using the GTAP (Global Trade Analysis Project, 2019) dataset that provides a self-consistent accounting of firms’ production structures, households’ consumption, trade, capital formation, and sectoral value added (Fig. 2). The model has been enhanced with a bottom-up representation of electricity production, road transport, and heating demand in buildings, based on the explicit integration of energy technologies and detailed modelling of energy efficiency, and technology learning (Fragkos & Fragkiadakis, 2022). The model has been recently enhanced with a detailed representation of coal, oil, and gas supply by region linked with specific production sectors, where hydrocarbon reserves determine the evolution of fossil fuel production and thus the international fuel prices. As a result, GEM-E3 is now capable of simulating scenarios with supply-side policies differentiated by region and fuel.

GEM-E3 structure

We designed a series of scenarios to assess the environmental and macroeconomic effects of supply-side coalitions. Table 1 includes the seven scenario descriptions, combining assumptions for fossil fuel supply and climate policy. All scenarios follow the SSP2 socioeconomic developments but incorporate the short-term GDP impacts following the COVID-19 pandemic and the subsequent recovery. The NPi scenario assumes implementation of currently legislated climate policies, while no supply-side restrictions are imposed. The BAN_COAL, BAN_OIL, and BAN_FOSSIL scenarios assume staged phase-outs of supply restrictions of coal, oil, and all fossil fuels, respectively, following the clusters of countries (see also Table 2). We did not model a BAN_GAS scenario individually, as a coalition to stop gas production alone (i.e. without simultaneously phasing down oil and coal) seems less relevant given the relatively lower carbon intensity of gas, and the potential of increasing emissions by triggering gas-to-coal or gas-to-oil substitutions (Andreoni et al., 2023). Finally, we combined supply-side policies with carbon taxation (and other policies targeting fossil fuel consumption) to evaluate potential synergies between supply- and demand-side policies (BAN_1150), while we also added for comparison two scenarios that achieve the Paris goal of staying well-below 2 °C (1150) and 1.5 °C based only on demand-side measures (leading to more ambitious short-term emission reductions than current trends entail).

Fossil fuel production constraints are modelled with different speeds based on the country-region clusters identified in Sect. 2 for the different fuels. Fossil fuel production phase-outs by region are modelled as a forced reduction of fossil fuel extraction by up to 70% relative to 2020 fossil production in a 20-year period, with Frontrunners starting in 2025 and other groups following with five-year intervals (Table 2). The scenario assumptions are kept relatively cautious about the technical and socio-political feasibility of phasing out fossil fuels, by assuming that governments (and companies) are unwilling or unable to completely shut down their hydrocarbon extraction industries. Despite this, the speed and depth of the hydrocarbon production phase-out foreseen in the scenarios would be historically unprecedented and highly ambitious compared to currently implemented climate policies and Nationally Determined Contributions under the Paris Agreement. By creating scarcity in fossil fuel markets, supply-side policies would increase the international market price of fossil fuels. Consequently, in the case of a non-global policy, production limits would decrease fossil fuel consumption even outside the borders of the country or country coalition that implements them.

3.2 Results

This section describes the main environmental and macroeconomic impacts as simulated with GEM-E3.

3.2.1 Emissions implications

The introduction of newly legislated climate policies dominated by demand-side policies globally would lead to a limited reduction of global CO2 emissions in the NPi scenario from around 32 Gt CO2 in 2020 to 24 Gt in 2050, mostly driven by climate action in developed economies. This result is in line with the latest multi-model assessments of current climate policies (van de Ven et al., 2023). In the short to medium term, emission reductions are also driven by the increase in gas, oil, and coal prices from their low levels in 2020. The well-below 2 °C scenario (1150) and the 1.5 °C scenario imply a sharp reduction of global CO2 emissions in the first half of the century, reaching net-zero CO2 emissions between 2060 and 2075 (with contributions from land use that are not shown in Fig. 3). Banning only coal extraction (BAN_COAL) decreases CO2 energy-related emissions by 7% in 2040, 19% in 2050, and 8% in 2070 compared to the NPi scenario, while cumulative emissions are reduced by only 7% relative to the NPi scenario by 2100, which lies in the middle of multi-model projections reported in (Andreoni et al., 2023). The limited emission reductions are due to the substitution with unbanned fossil fuels (gas, oil) and the fact that NPi already implies a gradual reduction of coal use under current policies. Phasing out oil extraction (BAN_OIL) reduces global CO2 emissions even more than the BAN_COAL scenario, especially in the second half of the century, with cumulative emissions declining by about 13% below NPi levels. As oil continues to be a major source of energy (especially for transport) in the NPi scenario, phasing out oil extraction (BAN_OIL scenario) has large impacts on oil use from NPi levels and hence on emission reductions achieved.

Global CO2 energy-related emissions by scenario

Supply-side scenarios that limit the production of all fossil fuels tend to bridge the current level of climate efforts with the well-below 2 °C emission pathways. In the BAN_FOSSIL scenario, global CO2 emissions in 2050 are reduced by 16% in 2040, 45% in 2050, and 60% after 2060, relative to the NPi scenario, a level consistent with the 52–76% range of CO2 emission reduction relative to 2019 reported in IPCC (2022). In the period 2040–2070, emission reductions achieved in the BAN_FOSSIL scenario are even higher than in the cost-optimal 1150 scenario, implying that supply-side policies, if widely implemented across regions and fossil fuels, can pave the way towards decarbonisation even in the absence of carbon pricing. However, long-term emissions are higher in supply-side scenarios relative to mitigation scenarios based on demand-side policies. After 2050, global emissions in BAN_FOSSIL scenario stabilise at around 10 Gt CO2/yr (a level consistent with the 5–16 Gt CO2/yr range for residual emissions reported by Clarke et al. (2022) for 2 °C scenarios, but somewhat lower than the study of Andreoni et al., 2023), whereas carbon tax-based scenarios reach net-zero emissions. The BAN_FOSSIL scenario does not reach a carbon budget consistent with well-below 2 °C, as extraction bans do not foster carbon capture and storage (CCS) linked to fossil fuels, biomass with carbon capture and storage (BECCS) and other negative emissions technologies (NETs). CCS can be used to operate coal and gas power plants with low emissions intensity and decarbonise industrial sectors that require high-temperature thermal inputs and are hard to electrify. NETs are needed to offset residual CO2 emissions from hard-to-abate energy sectors (e.g., cement, aviation, shipping), and non-CO2 emissions from agriculture and other sources, and possibly to reach net-negative emissions to recover from temperature overshoot. Therefore, although a policy with extensive cuts to fossil fuel production would reduce emissions from fossil fuels to zero (at potentially prohibitive costs, as presented in Sect. 3.2.4), net-zero CO2 and greenhouse gas emissions would still not be reached solely with supply-side policies.

The scenario combining supply-side policies with medium-level carbon pricing (BAN_1150 scenario) achieves even larger CO2 emission reductions than the well-below 2 °C scenario and can pave the way towards the 1.5 °C goal without requiring very high carbon pricing. In particular, the BAN_1150 scenario can reduce the global carbon budget over 2020–2100 to around 920 Gt and thus close about 45% of the additional gap to achieve the 1.5 °C goal relative to the well-below 2 °C. The combination of carbon pricing with a fossil fuel phase-out (BAN_1150) causes a faster decline of emissions by 2070, because the production constraints created are more ambitious than the implicit constraint produced by carbon pricing. Thus, integrating fossil fuel production phase-outs with global carbon pricing increases mitigation efforts early on and reduces the long-term reliance on NETs that are currently expensive, commercially immature and unavailable at scale.

3.2.2 Price impacts

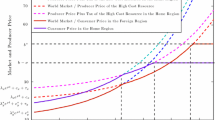

Although both supply- and demand-side policies decrease fossil-related CO2 emissions, the underlying mechanism is different: carbon pricing increases the consumer price of carbon-intensive goods and fuels but reduces fuel prices at the international market level due to reduced global demand. By contrast, supply-side policies trigger fossil fuel supply scarcity and increase the market price of the banned hydrocarbon. The speed and magnitude of price increases driven by supply-side policies depends on the share of global hydrocarbon production subject to the ban and the extent the supply constraints force a reduction in global fuel demand. Global oil prices show a limited increase in the NPi scenario from around 80 2015$/barrel in 2025 to 110 2015$/barrel in 2050 (in line with the recent International Energy Agency’s World Energy Outlook (IEA, 2022)), as global oil demand continues to be at high levels. In the 1150 scenario, the global oil price declines by 6% in 2030 and 26% in 2050 relative to NPi levels driven by reduced global oil demand due to carbon pricing. In a high oil demand scenario in the absence of strong carbon pricing (BAN_OIL and BAN_FOSSIL), supply-side measures will cause a high oil price increase, as shown in Fig. 4, with the global oil price growing to about 250 2015$/barrel and further to about 400 2015$/barrel after 2065, in line with Andreoni et al. results. By contrast, when combining supply and demand-side measures (BAN_1150) the oil price increase would be much smoother, as oil demand is declining due to carbon pricing. In the BAN_FOSSIL scenario, the greatest impact for all fuels is seen when the Laggards and Reluctants initiate their ban, because only a coalition representing a large enough share of global hydrocarbon production has a meaningful effect on prices. For coal, where Frontrunners and Followers are a larger group, the effect on prices is visible early on, while for oil the supply-side measures in Frontrunners have a limited effect on prices, whereas when Followers join the agreement, we observe steep price increases. The entry of Laggards and Reluctants in the coalition implementing phase-out measures is necessary for oil prices to increase. By contrast, the increase in the coal price is more limited when supply-side policies exclusively target coal (Fig. 5); this is due to the relatively easy replacement of coal in the BAN_COAL scenario with other energy forms (especially renewables for electricity production), which reduces the pressure on coal prices. By contrast, oil is more difficult to replace by other energy forms in the absence of carbon pricing, and this leads to a major increase in global oil prices in BAN_OIL case.

International oil price in different scenarios

International coal price in different scenarios

Coalition size matters also when demand- and supply-side policies are combined (i.e., the BAN_1150 scenario). Our analysis shows that international fuel prices under the BAN_1150 scenario are higher than in the demand-side scenarios (1150), but lower than in the supply-side scenarios with the same production constraints (BAN_FOSSIL). This is because in the BAN_1150 scenario the production bans reduce the global supply of fossil fuels, but at the same time the carbon tax also significantly reduces their demand.. Consequently, the market equilibrium is found at a price in between the supply-side-only and demand-side-only scenarios. Whether this equilibrium is closer to the former or the latter depends on the relative “strength” of the policies, i.e. how much fossil fuel demand is reduced by the carbon tax relative to how much supply is constrained by production bans. In our combined scenario (BAN_1150), the carbon tax is the primary policy instrument for emission reductions, which produces a price profile closer to the demand-side-only scenario (Figs. 4–5).

The increase in international prices reduces primary fossil fuel consumption substantially. Our analysis suggests that phasing out a single fuel may cause an increase in the use of other fuels if it is not coupled with additional emission reduction policies (e.g., carbon pricing). This substitution effect would become even more important if gas supply is constrained. This might even cause an increase in global emissions as more carbon-intensive coal and oil replace more expensive—but less carbon-intensive—gas.

3.2.3 Energy system transition indicators

Through increasing the market prices of fossil fuels, the supply-side scenarios accelerate the clean energy transition globally by enhancing the economic incentive to phase out fossil fuels and scale up renewable energy and energy efficiency. As shown in Figs. 6–9, the supply-side scenarios outperform carbon pricing in terms of electrification, renewable energy penetration, fossil fuel phase-out, and energy efficiency improvements.

Global electricity production mix by technology

The global electricity generation mix (Fig. 6) is influenced by technology dynamics, carbon taxation, and fossil fuel prices. Driven by accelerated technology learning and cost reductions, the renewable energy share grows in the NPi scenario from 23% in 2015 to 42% in 2030 and further to 54% in 2050, mainly due to the uptake of solar and wind power. This comes at the expense of unabated fossil-fired generation, with the share of fossil fuels declining from 66% in 2015 to 36% in 2050 in the NPi scenario. This transition is further accelerated in case of supply- and/or demand-side measures; in the BAN_COAL scenario, an increased coal market price reduces coal competitiveness, with the coal share in global power generation declining from 12% in NPi to only 1% in BAN_COAL in 2050. The share of renewable energy accelerates in the BAN_FOSSIL scenario to 80% in 2050, which is driven also by the limited deployment of CCS technologies in the absence of carbon pricing. By contrast, CCS technologies account for 16% of global power production in 2050 in the 1150 scenario, as carbon pricing provides incentives to deploy CCS in coal, gas, and biomass-fired power plants.

The transition accelerates in supply-side-driven scenarios, with the share of renewable energy increasing even more than in demand-side carbon price-driven scenarios. This is mostly a result of the balance between CCS and renewable energy, as described above. Figure 7 shows that the supply-side scenarios increase both the speed and magnitude of renewable energy expansion with its share of global electricity generation increasing rapidly from 28% in 2020 to 45% in 2030 and further to 80% in the BAN_FOSSIL scenario, mostly driven by the large-scale uptake of wind and solar power. The combination of supply- and demand-side policies leads to even faster renewable energy growth, accounting for 84% of global power generation in 2050 and reaching shares higher than 90% after 2050.

Share of renewable energy in global electricity production

Fossil fuel use is projected to decline in the NPi scenario driven by the emergence of renewable energy and energy efficiency, but the transition is substantially accelerated in the supply-side scenarios. The share of fossil fuels in primary energy consumption is projected to decline rapidly from 83% in 2020 to 57% in BAN_COAL and 51% in BAN_OIL scenarios in 2050. Limiting oil production has higher impacts than coal, as oil products are widely used in the NPi scenario even by 2050. When imposing supply-side constraints on all fossil fuels, their use is projected to decline massively due to higher fuel prices, with their share in primary energy consumption amounting to only 39% in 2050 and 28% in 2060 (Fig. 8). Similar trends can be observed in demand-side scenarios with declining fossil fuel use due to carbon pricing, but in these scenarios the amount of fossil fuels used beyond 2050 is higher due to the introduction of CCS options.

Share of fossil fuels in primary energy consumption

Figure 9 shows that supply-side policies can accelerate the electrification of end uses in the transport, buildings, and industrial sectors (e.g., through the uptake of electric vehicles, heat pumps, and electrified industrial processes). As the power mix is already to a large extent decarbonised by 2030/2040, the electrification of energy services is a robust and efficient strategy to reduce emissions from the demand sectors where other mitigation options are scarce. The NPi scenario shows a modest increase in the electrification of end-uses, which is further accelerated in the supply- and demand-side policy scenarios. In the 1150 scenario, the electricity share in global final energy consumption increases from 20% in 2020 to 33% in 2050, while the increase is much higher in the BAN_FOSSIL scenario (39% in 2050 and 47% in 2060) and in the scenario combining supply- and demand-side policies (BAN_1150). The accelerated deployment of other low-carbon fuels (e.g., green hydrogen, advanced biofuels) in GEM-E3 scenarios means that electrification levels are somewhat lower than the ones of (Andreoni et al., 2023).

Share of electricity in global final energy consumption

3.2.4 Macroeconomic impacts

Figure 10 presents the global CO2 emission and GDP impacts in 2030 and 2050 for the alternative policy scenarios relative to the NPi scenario. As expected, in a general equilibrium framework, any deviation from the optimal allocation of resources in the NPi scenario will cause a decline in global GDP. In demand-side scenarios, high carbon prices increase the production costs and prices throughout the economy, causing a negative effect on domestic consumption and production in the strict closure of general equilibrium models, assuming a crowding-out effect on investment (Fragkos & Fragkiadakis, 2022). The demand-side scenarios assume the imposition of a universal carbon price equalising marginal abatement costs across regions and sectors, which leads to the lowest mitigation costs to achieve the specific climate target. This explains the low GDP losses in the 1150 scenario (0.8% of global GDP in 2050), which however achieves large emission reductions (42% lower from NPi in 2050).

Global CO2 and GDP impacts of policy scenarios in 2030 and 2050

The supply-side scenarios tend to have relatively higher mitigation costs than demand-side ones, as they are not based on cost-optimality to meet climate goals. Rather, supply-side scenarios integrate fossil fuel supply restrictions that tend to increase the market price of fossil fuels with negative macroeconomic effects, as increased fossil prices pass through to the prices of all products through supply chain and trade effects. The scenarios with constraints for only one fossil fuel (coal or oil) can reduce global CO2 emissions by 16–19% below NPi levels in 2050, partly bridging the gap between current policy ambition and a Paris-compatible transition. However, their cost impacts differ significantly. BAN_COAL results in negligible GDP losses globally (0.2% below NPi levels in 2050, ranging from − 0.6% to + 0.1% across G20 economies), while BAN_OIL has more profound negative economic impacts, with global GDP declining by 2.8% in 2050 relative to NPi. This points to the different contributions of coal and oil in the future economy. In the NPi scenario, a decline in coal demand is driven by existing climate and air quality policies. The BAN_COAL scenario accelerates the transition towards renewable energy by replacing coal-fired power, which is already more expensive than wind power and solar PV in most countries, resulting in marginal macroeconomic effects. By contrast, oil still plays an important role in the global economy by 2050 in the NPi scenario, and the supply-driven shocks markedly increase the international oil price with detrimental effects especially for major oil importers. The BAN_COAL scenario is more efficient relative to BAN_OIL (in terms of mitigation costs per unit of carbon avoided) because it closely follows the logic of carbon pricing by penalising coal—the most carbon-intensive fuel. Combining supply- and demand-side policies in the BAN_1150 scenario leads to even larger emission reductions (approximately 52% from NPi levels) while minimising GDP losses (globally at 1.7%). This is achieved through carbon pricing, which effectively decreases the demand for fossil fuels and consequently reduces the strain on fuel market prices caused by supply-side policies. In conclusion, demand-side scenarios that achieve the Paris Agreement goals are more cost-effective than supply-side scenarios, but the combination of supply and demand-side scenarios can exploit synergies between policies to deliver the greatest CO2 emissions cuts while minimising mitigation costs.

Supply-side scenarios are less cost-effective than demand-side scenarios since they incentivise a narrower portfolio of mitigation options than carbon pricing, and do not include CCS, BECCS, and NETs. Less reliance on CCS linked to fossil fuels and NETs can speed up the low-carbon transformation. The prescribed linear reduction for fossil fuel production applied to regional groups does not exactly follow a least-cost-option-first approach, even if more carbon-intensive fossil fuels are phased out earlier in our scenario design. These factors are magnified by the fact that we compare fossil fuel production phase-outs with idealised, first-best carbon pricing. A “real-world” set of demand-side policies would be characterised by a (potentially inefficient) mix of carbon pricing, efficiency standards, sectoral policies, and technology bans, likely reducing the cost-effectiveness of demand-side policies.

With supply-side measures, the revenues of hydrocarbon producers are influenced by two opposing forces: higher international fossil prices increase revenues per output, but shrinking production reduces the total volume of hydrocarbons. The first effect is found to be larger in magnitude, especially when the supply-side coalition becomes larger. The value of extracted hydrocarbon resources increases in the BAN_FOSSIL scenario with most of the revenue increase benefiting the large fossil fuel-producing regions, such as Russia, Saudi Arabia, and Middle East and North Africa. If carbon pricing and supply-side policies are implemented together (BAN_1150), the net value of extracted resources is higher than in the carbon tax scenario (1150), but the increase is not sufficient to completely compensate the losses relative to NPi, as the effects are dominated by the reduced fossil consumption.

Figure 11 presents the GDP impacts of alternative scenarios by major region in 2050. In most regions, the BAN_OIL scenario has the largest negative impacts as the increased market price of oil increases the import bills of major importers. In addition, the oil price increase is transferred throughout the economy via supply chains and trade, increasing the prices of all products, thus reducing private consumption and production of firms among both oil importers and exporters that face a relatively large reduction in their GDP. By contrast, the scenario with supply-side policies applying to all fossil fuels (BAN_FOSSIL) leads to increased GDP in major oil and gas exporters (such as Russia, Saudi Arabia, and other energy producers in the Middle East), driven by the increased hydrocarbon export revenues (discussed above) as these regions are considered Reluctants and join the supply-side coalition later. The picture is different for major fuel importers, such as India, and the EU, that face relatively high GDP losses, respectively (Fig. 11).

GDP impacts of policy scenarios in major regions in 2050

As discussed above, the 1150 scenario entails moderate cost impacts globally as it is based on cost-optimal mitigation policies. However, it results in regressive effects, with low- or middle-income and usually more carbon-intensive countries (e.g., India, Russia, Saudi Arabia) facing higher mitigation costs than developed and already carbon-efficient economies (e.g., EU, United States). This is an issue often raised in international climate policy negotiations, and requires effective policies that combine emissions reductions with targeted compensation or financial provision to countries that will face higher decarbonisation costs (Bauer et al., 2020). Our analysis shows the potential of supply-side policies to mitigate the regressive impacts of carbon pricing; as shown in Fig. 11, the BAN_1150 scenario has positive macroeconomic impacts for major hydrocarbon exporters (that face the highest GDP losses in the 1150 scenario), while it increases the mitigation costs for developed economies like the EU and the USA. Overall, the BAN_1150 scenario leads to less regressive economic impacts across regions relative to the carbon pricing-focused 1150 case. Performing a simple statistical analysis on the GEM-E3 results shows that in the 1150 scenario the higher the GDP per capita of a region, the lower the mitigation costs (as a percentage of GDP), with a correlation of 0.63; this correlation is significantly reduced to only 0.19 in the BAN_1150 scenario, implying that the two variables are much less correlated and thus the regressive distributional impacts of the 1150 scenario are greatly reduced in BAN_1150. In addition, the coefficient of variation, which shows the relative variance of GDP per capita across regions, is projected to decline from 0.75 in the 1150 scenario to 0.73 in the BAN_1150 scenario in 2050, indicating more progressive outcomes than the 1150 scenario.

The mitigation scenarios have limited impacts on aggregate employment, driven by two contradictory trends. On the one hand, declining economic activity tends to reduce employment. On the other hand, the economy moves toward a more labour-intensive structure as renewable technologies and energy efficiency have higher labour intensity on average compared to fossil fuels (Fragkos et al., 2018). The trade-off between jobs lost in some sectors (e.g., fossil fuel supply,) and jobs creation in others (e.g., renewable electricity, biofuels, construction) would lead to a modest impact on economy-wide employment.

4 Implications for the development of international cooperation on supply-side climate policy

The results presented in Sect. 3 have several implications for the further development of international cooperation on supply-side climate policy.

First, the findings underscore the importance of “cutting with both arms of the scissors” (Green & Denniss, 2018): supply-side and demand-side policy should be seen as complementary, not as substitutes. The scenario that combines both stringent carbon pricing and production constraints for all fossil fuels (BAN_1150) gets closer to the 1.5 °C pathway than scenarios that rely solely on demand- (1150) or supply-side (BAN_FOSSIL) climate policy (Fig. 3). While it is theoretically possible to follow a 1.5 °C pathway with carbon pricing only, this requires a very high carbon price, with regressive economic impacts (Feindt et al., 2021; Fragkos et al., 2021). The scenario that combines supply- and demand-side policies (BAN_1150) also shows that the impacts on fuel market prices are less drastic compared to relying solely on fossil fuel supply cuts. Importantly, combining supply- and demand-side policies would support the goal of a deeper transition towards renewable energy and electrification, with less dependence on unproven, commercially immature, and expensive CCS and NETs. Implementing demand- and supply-side climate policy in conjunction has a less negative impact on global GDP than only implementing supply cuts, although those impacts are nonetheless still greater than in a purely cost-optimal demand-driven mitigation scenario. Furthermore, compared to a purely demand-side scenario, supply-side restrictions can result in positive outcomes for major hydrocarbon exporters and developing nations that often experience the most substantial adverse GDP consequences when subjected to stringent carbon pricing measures.

This raises the vexed, but crucial question of how demand- and supply-side climate policies can work together. Addressing this question is beyond the scope of this article, and in any case the answer will likely depend on the particular political and socioeconomic characteristics of different countries. Nevertheless, the IEA (2023) suggests generally that demand-side incentives (through carbon pricing and other policies limiting fossil fuel use) and clean energy investment are a prerequisite for fossil fuel supply cuts. Pursuing demand- and supply-side policies in the reverse order could lead to “prolonged high prices” and “reduce the chances of an orderly transition to net zero emissions by 2050” (IEA, 2023, 76).

Second, our findings point to the importance of the substantive coverage of an international supply-side coalition. In particular, linked to the ongoing discussions in the international climate negotiations, they underscore the different impacts of phasing out exclusively coal versus phasing out all fossil fuels. A supply-side coalition focused only on coal production would be limited in its effectiveness in reducing emissions, as coal is likely to already play a much smaller role in the energy mix given current climate policies and market dynamics, with wind and solar energy being cheaper already (IEA, 2021b). At the same time, the emission cuts achieved by restricting coal supply come at a very low cost (as shown by Fig. 10), with limited impact on GDP in all countries, while accelerating the phase-in of renewable energy. By contrast, phasing out oil production can offer similar emission reductions (and climate outcomes) as phasing out coal production, albeit at a much higher cost. The rise in oil prices would have a detrimental effect on all economies, particularly major importers, as it permeates through supply chains and trade, leading to an increase in prices of various products. Only covering gas might even increase emissions to the extent that gas is replaced by more emissions-intensive fossil fuels. This suggests that in case an “all fossil fuels” supply-side coalition is not feasible, agreeing on a coal production phase-out among a club of coal-producing countries (as proposed by Burke & Fishel, 2020, and supported by Collier & Venables, 2014) may still be worth the effort. The PPCA—which presently only covers the phase-out of coal-fired power generation, not coal mining—would arguably form a natural vessel for such an agreement. By doing so, it could counter one of the risks faced by the PPCA, namely that the coal that is not consumed by the power sector finds application in other sectors (Li et al., 2023).

Third, the size of the coalition matters. For coal production, the group of Frontrunners is already sizable, which in itself would already have an environmental impact. For oil, a significant impact is only achieved when the Reluctant, Saudi Arabia, joins. Although a frontrunner coalition—a club approach in the terminology of van Asselt and Newell (2022)—could pave the way for further cooperation, for instance by setting up the necessary institutional architecture to facilitate further cooperation, its environmental impact would be limited. Interestingly, while a scenario of Laggards and Reluctants joining may seem unrealistic, our results show that some major oil producers could stand to gain from restricting fossil fuel production. Indeed, there are net income gains for these producers despite the electrification of demand sectors and thus the reduction of global fossil fuel consumption. This raises the question whether some kind of “climate OPEC”—with oil producers cooperating to limit production and keep fuel prices high in the face of decreasing demand may be possible (see Dobson, 2020; Gault & Ait-Laoussine, 2020)—is feasible. With market power shifting increasingly to consumers, a supply-side agreement might help engineer a soft landing for the major oil producers by increasing their export revenues. At the same time, the prospect of decreasing demand due to the electrification of end-use sectors might also incentivise producers to sell as much oil as they can, while they can (Dobson, 2020), triggering the “green paradox” (Sinn, 2012).

Lastly, given that parts of the world—particularly developing countries with limited capacity that are highly fossil fuel-dependent—stand to lose out from restricting fossil fuel supply (e.g., Steadman et al., 2023), international cooperation should also provide for planning and financial support for a just transition (Kartha et al., 2018; Muttitt & Kartha, 2020). Even when combined with strong demand-side policies, a significant increase in oil prices is the likely consequence of restricting fossil fuel production. This may hit poor and vulnerable oil consumers especially hard. Planning for the assistance of relevant communities, including through domestic investments and international finance, is therefore key (Peterson, 2022). Financial support can be set aside by delivering on pledges to stop the provision of international finance for fossil fuels, something that major donors (including the United States, France, and Germany) agreed to at the end of 2021 (UK, 2021) and/or by further developing “Just Energy Transition Partnerships”, which so far have been launched for South Africa, Indonesia, Vietnam, and Senegal (European Commission, 2023). Overall, like international cooperation on demand-side climate policy, any international agreement restricting the supply of fossil fuels should therefore include requirements to plan for a just transition in participating countries, as well as a financial mechanism to support the least well-off countries in that transition (see also Newell & Simms, 2020; Newell et al., 2022).

5 Conclusions

Achieving the Paris Agreement goals requires action to address fossil fuels. International cooperation can help to avoid leakage effects from unilaterally adopted supply-side climate policies and ensure that countries are supported in their transition away from fossil fuels. In this article, we have examined the possible climate-related and economic effects of international cooperation on supply-side climate policy in two steps. First, by considering fossil fuel reserves, supply-side policies, and fossil fuel rents, we have employed cluster analysis to subdivide countries into four groups and rank them based on their likelihood to join a supply-side coalition. Second, using the country clusters as input for the development of a supply-side coalition, we have modelled the environmental and macroeconomic effects of different scenarios of international cooperation on supply-side policies.

Our study points to several findings. First, we find that an international supply-side coalition, when implemented in conjunction with strong demand-side measures, can support the achievement of the long-term temperature goal of the Paris Agreement, and speed up the transition towards a renewables-based energy system and the rapid phase-out of fossil fuels. A combination of both supply- and demand-side policies leads to a comparatively lower negative impact on global GDP than solely implementing supply cuts. Second, we show the impact of supply-side coalitions for different types of fossil fuels and the benefits of limiting several fossil fuels concurrently. While a coalition focused on coal production may be limited in its effect on global emissions since coal is losing its place in the global market even without supply cuts, an oil phase-out may result in higher economic costs, due to its ubiquity in global supply chains and production processes. Third, we demonstrate that the size of the coalition plays a pivotal role for the outcome. Supply-side coalitions are especially dependent on the prospect that major fossil fuel producers would join. While a club approach focused on like-minded countries may initially help pave the way for a broader coalition, broader participation ultimately is essential. Finally, we underline the importance of international cooperation for ensuring a just transition for developing countries, particularly those that are heavily dependent on imported fossil fuels, which will be economically most affected by increases in fossil fuel prices. Any international supply-side agreement should therefore link cuts to fossil fuel production in developing countries to a (financial) support mechanism.

There is scope for further studies combining qualitative insights into international cooperation on supply-side climate policy, and quantitative modelling to assess their economic and climate repercussions. First, we have considered three parameters (fossil fuel reserves, the adoption of supply-side policies, and fossil fuel rents), whereas other factors may play a role as well, such as political willingness (Lujala et al., 2022), countries’ leadership aspirations (Parker & Karlsson, 2017), and international peer pressure. Our results offer an initial indication of which countries may participate in a supply-side coalition. However, further studies could use a broader set of quantitative and qualitative factors determining the likelihood of countries joining a supply-side coalition as a basis for the design of scenarios, while exploring different compositions of groups based on such political factors. Second, our findings are based on one IAM—the GEM-E3 model. Further studies could draw on multiple IAMs and macroeconomic models exploring the same policy scenarios to improve the robustness of our results. Third, model parameterisations—e.g., the speed of a fossil fuel phase-out—may influence the results, which could be addressed by a comprehensive sensitivity analysis (e.g., on price elasticities, technology upscale constraints, role of specific technologies). In this context, additional scenarios can also be explored, especially on the role of gas supply restrictions combined with constraints on oil supply. Fourth, the analysis can be expanded to cover more regions and countries to provide insights for national contexts as the aggregate regions modelled in GEM-E3 include heterogeneous national contexts. Fifth, scenarios in future studies might explore the dynamics of an international supply-side coalition in a more endogenous manner without pre-specifying the country-region clusters, while the modelling framework can also be extended to explicitly represent nature. Lastly, future research could help to shed light on how the use of revenues generated through carbon pricing could impact the economic effects depending how they are reinvested, how such revenues could help mitigate regressive impacts by targeting affected communities and countries, and how these options may vary under scenarios focusing on carbon pricing, fossil fuel production restrictions, or a combination thereof. Ideally, such an analysis would examine the regional distribution of these revenues as well as their ability to accelerate an orderly clean energy transition.

Data availability

Data available on request from the authors.

Change history

14 March 2024

A Correction to this paper has been published: https://doi.org/10.1007/s10784-024-09635-z

Notes

The Fossil Fuel Policy Tracker is, to our knowledge, the most comprehensive data source on supply-side policies per fuel type. The sources it uses vary from official ones (e.g., government reports) to unofficial ones (e.g., news items). The database also collects information about past supply-side policies, meaning that some policies may no longer be in place.

Abbreviations

- BECCS:

-

Biomass with carbon capture and storage

- BOGA:

-

Beyond Oil and Gas Alliance

- CCS:

-

Carbon capture and storage

- COP:

-

Conference of the Parties

- CO2 :

-

Carbon dioxide

- EIA:

-

Energy Information Administration

- EJ:

-

Exajoule

- GDP:

-

Gross domestic product

- Gt:

-

Gigatonne

- IAM:

-

Integrated Assessment Model

- IPCC:

-

Intergovernmental Panel on Climate Change

- NET:

-

Negative emissions technology

- OPEC:

-

Organization of the Petroleum Exporting Countries

- PCA:

-

Principal Component Analysis

- PPCA:

-

Powering Past Coal Alliance

- PV:

-

Photovoltaics

- UNFCCC:

-

United Nations Framework Convention on Climate Change

References

Andreoni, P., Aleluia Reis, L., Drouet, L., Dessens, O., Fragkos, P., Pietzcker, R., Pye, S., Rodrigues, R., & Tavoni, M. (2023). Fossil extraction bans and carbon taxes: Assessing their interplay through multiple models. iScience, 26(4), 106377.

Ansari, D., & Holz, F. (2020). Between stranded assets and green transformation: Fossil-fuel-producing developing countries towards 2055. World Development, 130, 104947.

Bauer, N., Bertram, C., Schultes, A., Klein, D., Luderer, G., Kriegler, E., Popp, A., & Edenhofer, O. (2020). Quantification of an efficiency–sovereignty trade-off in climate policy. Nature, 588(7837), 261–266.

Billon, P. L., Gaulin, N., & Lujala, P. (2022). COP27: Which countries will push to end fossil fuel production? And which won’t? The Conversation. http://theconversation.com/cop27-which-countries-will-push-to-end-fossil-fuel-production-and-which-wont-193471.

BOGA. (2023). Beyond Oil & Gas Alliance. https://beyondoilandgasalliance.org/.

Bos, K., & Gupta, J. (2018). Climate change: The risks of stranded fossil fuel assets and resources to the developing world. Third World Quarterly, 39(3), 436–453.

Carter, A. V., & McKenzie, J. (2020). Amplifying “keep it in the ground” first-movers: Toward a comparative framework. Society & Natural Resources, 33(11), 1339–1358.

Clarke, L., Wei, Y.-M., Navarro, A. de la V., Garg, A., Hahmann, A. N., Khennas, S., Azevedo, I. M. L., Löschel, A., Singh, A. K., Steg, L., Strbac, G., & Wada, K. (2022). Energy systems. In P. R. Shukla, J. Skea, R. Slade, A. Al Khourdajie, R. van Diemen, D. McCollum, M. Pathak, S. Some, P. Vyas, R. Fradera, M. Belkacemi, A. Hasija, G. Lisboa, S. Luz, & J. Malley (Eds.), Climate Change 2022: Mitigation of Climate Change. Working Group III Contribution to the IPCC Sixth Assessment Report (pp. 613–746). Cambridge University Press.

Collier, P., & Venables, A. (2014). Closing coal: Economic and moral incentives. Oxford Review of Economic Policy, 30(3), 492–512.

Depledge, J. (2008). Striving for no: Saudi Arabia in the climate change regime. Global Environmental Politics, 8(4), 9–35.

Dietz, T., Shwom, R. L., & Whitley, C. T. (2020). Climate change and society. Annual Review of Sociology, 46(1), 135–158.

Dobson, M. (2020). Revisiting OPEC’s democratic roots in the age of climate emergency. E-International Relations. https://www.e-ir.info/2020/01/17/revisiting-opecs-democratic-roots-in-the-age-of-climate-emergency/.

EIA. (2023). International—U.S. Energy Information Administration (EIA). US Energy Information Administration. https://www.eia.gov/international/data/world.

Erickson, P., & Lazarus, M. (2014). Impact of the Keystone XL pipeline on global oil markets and greenhouse gas emissions. Nature Climate Change, 4(9), 778–781.

European Commission. (2023, 22 June). The EU and the International Partners Group announced a Just Energy Transition Partnership with Senegal combining climate and development goals. European Commission. https://ec.europa.eu/commission/presscorner/detail/en/ip_23_3448.

Feindt, S., Kornek, U., Labeaga, J. M., Sterner, T., & Ward, H. (2021). Understanding regressivity: Challenges and opportunities of European carbon pricing. Energy Economics, 103, 105550.

Fossil fuel treaty non-proliferation treaty. (2023). The fossil fuel non-proliferation treaty initiative. The fossil fuel non-proliferation treaty initiative. https://fossilfueltreaty.org/.

Fossil Fuel Policy Tracker. (2023). Moratoria, bans, limits. https://doi.org/10.1787/281c98e5-en.

Fragkos, P., & Fragkiadakis, K. (2022). Analyzing the macro-economic and employment implications of ambitious mitigation pathways and carbon pricing. Frontiers in Climate, 4, 785136.

Fragkos, P., Fragkiadakis, K., Sovacool, B., Paroussos, L., Vrontisi, Z., & Charalampidis, I. (2021). Equity implications of climate policy: Assessing the social and distributional impacts of emission reduction targets in the European Union. Energy, 237, 121591.

Gaulin, N., & Le Billon, P. (2020). Climate change and fossil fuel production cuts: Assessing global supply-side constraints and policy implications. Climate Policy, 20(8), 888–901.

Gault, J., & Ait-Laoussine, N. (2020). OPEC: Still an ‘instrument of change’? Journal of World Energy Law & Business, 13(4), 343–352.

Green, F., & Denniss, R. (2018). Cutting with both arms of the scissors: The economic and political case for restrictive supply-side climate policies. Climatic Change, 150(1), 73–87.

Grimmer, J., Roberts, M. E., & Stewart, B. M. (2021). Machine learning for social science: An agnostic approach. Annual Review of Political Science, 24(1), 395–419.

Hansen, T. A. (2022). Stranded assets and reduced profits: Analyzing the economic underpinnings of the fossil fuel industry’s resistance to climate stabilization. Renewable and Sustainable Energy Reviews, 158, 112144.

Harstad, B. (2012). Buy coal! A case for supply-side environmental policy. Journal of Political Economy, 120(1), 77–115.

IEA. (2021a). Net Zero by 2050. International Energy Agency. https://www.iea.org/reports/net-zero-by-2050.

IEA. (2021b). World Energy Outlook 2021. International Energy Agency. https://www.iea.org/reports/world-energy-outlook-2021.

IEA. (2022). World Energy Outlook 2022. International Energy Agency. https://www.iea.org/reports/world-energy-outlook-2022.

IEA. (2023). Net Zero Roadmap: A Global Pathway to Keep the 1.5 °C Goal in Reach. International Energy Agency. https://www.iea.org/reports/net-zero-roadmap-a-global-pathway-to-keep-the-15-0c-goal-in-reach

IPCC. (2022). Summary for policymakers. In IPCC (Ed.), Climate Change 2022: Mitigation of Climate Change. Intergovernmental Panel on Climate Change.

IPCC. (2023). Summary for policymakers. In IPCC (Ed.), Climate Change 2023: Synthesis Report. Intergovernmental Panel on Climate Change.

Kartha, S., Caney, S., Dubash, N. K., & Muttitt, G. (2018). Whose carbon is burnable? Equity considerations in the allocation of a “right to extract.” Climatic Change, 150(1), 117–129.

Kaufman, L., & Rousseeuw, P. J. (2005). Finding groups in data: An introduction to cluster analysis (1st edition). Wiley-Interscience.

Lamb, W. F., & Minx, J. C. (2020). The political economy of national climate policy: Architectures of constraint and a typology of countries. Energy Research & Social Science, 64, 101429.

Lazarus, M., & van Asselt, H. (2018). Fossil fuel supply and climate policy: Exploring the road less taken. Climatic Change, 150(1), 1–13.

Lewis, A., Mcfarlane, S., Volcovici, V., & Volcovici, V. (2022, November 29). COP27 climate summit missed chance for ambition on fossil fuels, critics say. Reuters. https://www.reuters.com/business/cop/cop27-climate-summit-missed-chance-ambition-fossil-fuels-critics-say-2022-11-28/.

Li, S. B., Bauer, N., & Jewell, J. (2023). Coal-exit alliance must confront freeriding sectors to propel Paris-aligned momentum. Nature Climate Change, 13, 130–139.

Lujala, P., Le Billon, P., & Gaulin, N. (2022). Phasing out fossil fuels: Determinants of production cuts and implications for an international agreement. Global Environmental Politics, 22(4), 95–128.

Muttitt, G., & Kartha, S. (2020). Equity, climate justice and fossil fuel extraction: Principles for a managed phase out. Climate Policy, 20(8), 1024–1042.

Newell, P., & Simms, A. (2020). Towards a fossil fuel non-proliferation treaty. Climate Policy, 20(8), 1043–1054.

Newell, P., van Asselt, H., & Daley, F. (2022). Building a fossil fuel non-proliferation treaty: Key elements. Earth System Governance, 14, 100159.

Parker, C. F., & Karlsson, C. (2017). The European Union as a global climate leader: Confronting aspiration with evidence. International Environmental Agreements: Politics, Law and Economics, 17, 445–461.

Paroussos, L., Fragkiadakis, K., & Fragkos, P. (2020). Macro-economic analysis of green growth policies: The role of finance and technical progress in Italian green growth. Climatic Change, 160(4), 591–608.

Peterson, L. (2022). Domestic and international climate policies: Complementarity or disparity? International Environmental Agreements: Politics, Law and Economics, 22(1), 97–118.

Port Vila Call. (2023). Port Vila Call for a Just Transition to a Fossil Fuel Free Pacific. https://www.pican.org/_files/ugd/923d4b_8c205a9319a645d4b4926155f49c6425.pdf.

SEI, IISD, ODI, E3G, & UNEP. (2021). The Production Gap. 2021 Report. Stockholm Environment Institute. https://productiongap.org/2021report/.

Sinn, H.-W. (2012). The green paradox: A supply-side approach to global warming. MIT Press.

Steadman, S., Gençsü, I., Mustapha, S., Colenbrander, S., & Tyson, J. (2023). Indebted: how to support countries heavily reliant on oil and gas revenues to secure long-term prosperity. Overseas Development Institute. https://cdn.odi.org/media/documents/ODI_report_Indebted-fossil_fuel_producers_and_debt.pdf.

UK. (2021, November 4). Statement on International Public Support for the Clean Energy Transition. UN Climate Change Conference (COP26) at the SEC – Glasgow 2021. https://webarchive.nationalarchives.gov.uk/ukgwa/20230313124743mp_/https://ukcop26.org/statement-on-international-public-support-for-the-clean-energy-transition/.

UNFCCC. (2022). Report of the Conference of the Parties serving as the meeting of the Parties to the Paris Agreement on its third session (FCCC/PA/CMA/2021/10/Add.1). https://unfccc.int/sites/default/files/resource/cma2021_10_add1_adv.pdf.

UNFCCC. (2023). Decision -/CMA.5. Outcome of the First Global Stocktake (FCCC/PA/CMA/2023/L.17). https://unfccc.int/documents/636584.

van Asselt, H., & Green, F. (2023). COP26 and the dynamics of anti-fossil fuel norms. Wires Climate Change, 14(3), e816.

van Asselt, H., & Newell, P. (2022). Pathways to an international agreement to leave fossil fuels in the ground. Global Environmental Politics, 22(4), 28–47.

Van de Graaf, T., & Verbruggen, A. (2015). The oil endgame: Strategies of oil exporters in a carbon-constrained world. Environmental Science & Policy, 54, 456–462.

van de Ven, D.-J., Mittal, S., Gambhir, A., Lamboll, R. D., Doukas, H., Giarola, S., Hawkes, A., Koasidis, K., Köberle, A. C., McJeon, H., Perdana, S., Peters, G. P., Rogelj, J., Sognnaes, I., Vielle, M., & Nikas, A. (2023). A multimodel analysis of post-Glasgow climate targets and feasibility challenges. Nature Climate Change, 13(6), 570–578.

Wolfson, M., Madjd-Sadjadi, Z., & James, P. (2004). Identifying national types: A cluster analysis of politics, economics, and conflict. Journal of Peace Research, 41(5), 607–623.

World Bank. (2023b). World Bank Open Data. https://data.worldbank.org.

World Bank. (2023a). World Bank data—Population, total. World Bank Open Data. https://data.worldbank.org/indicator/SP.POP.TOTL.

Acknowledgements

The authors acknowledge support from the European Union's Horizon 2020 Research and Innovation Programme under grant agreement no. 101003866 (NDC ASPECTS). We thank Ploy Achakulwisut, Michael Lazarus, Wolfgang Obergassel, Roberto Schaeffer, Dirk-Jan van de Ven, and the two anonymous reviewers for helpful comments.

Funding

The Funding was provided by Directorate-General XII, Science, Research and Development, 101003866

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors have declared no conflicts of interest for this article.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

The original online version of this article was revised: The wrong Supplementary file was originally published with this article; it has now been replaced with the correct file.

Supplementary Information

Below is the link to the electronic supplementary material.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

van Asselt, H., Fragkos, P., Peterson, L. et al. The environmental and economic effects of international cooperation on restricting fossil fuel supply. Int Environ Agreements 24, 141–166 (2024). https://doi.org/10.1007/s10784-023-09623-9

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10784-023-09623-9