Abstract

With the growing popularity of the regime-switching Lévy processes model in option pricing, the coupled tempered fractional diffusion equation generated from this process has garnered considerable attention. However, solving this equation is challenging due to its coupling with a Markov generator matrix, which prevents the coefficient matrix derived from the fully implicit scheme from having a Toeplitz-like structure. Currently, there is no fast algorithm with guaranteed theoretical performance for this problem based on a fully implicit scheme. Therefore, this paper proposes a novel banded preconditioner specifically designed for the regime-switching Carr-Geman-Madan-Yor (CGMY) model. The effectiveness of the preconditioner is ensured by providing related theoretical analyses. It is shown that the eigenvalues of the preconditioned matrix cluster around one under specific parameter settings. Additionally, the condition number of the preconditioned matrix is bounded by a constant without any specific parameter requirements. The proposed preconditioner and theoretical analyses can be extended to the regime-switching CGMYe model as well. Finally, the accuracy of the considered models and the effectiveness of the proposed banded preconditioner are demonstrated through three numerical examples, including an empirical example.

Similar content being viewed by others

Data Availability

No datasets were generated or analyzed during the current study.

References

Asiimwe, P., Mahera, C.W., Menoukeu-Pamen, O.: On the price of risk under a regime switching CGMY process. Asia-Pacific Finan. Markets 23, 305 (2016)

Bao, J., Zhao, Y.: Option pricing in Markov-modulated exponential Lévy models with stochastic interest rates. J. Comput. Appl. Math. 357, 146–160 (2019)

Bertaccini, D.: Reliable preconditioned iterative linear solvers for some numerical integrators. Numer. Linear Algebra Appl. 8, 111–125 (2001)

Bertaccini, D., Golub, G.H., Serra-Capizzano, S.: Spectral analysis of a preconditioned iterative method for the convection-diffusion equation. SIAM J. Matrix Anal. Appl. 29, 260–278 (2007)

Black, F., Scholes, M.: The pricing of options and corporate liabilities. J. Polit. Econ. 81(3), 637–654 (1973)

Boyarchenko, S., Levendorskii, S.: Non-Gaussian Merton-Black-Scholes theory. World Scientific, Singapore (2002)

Cartea, A., del Castillo-Negrete, D.: Fractional diffusion models of option prices in markets with jumps. Phys. A 374(2), 749–763 (2007)

Chan, R., Jin, X.: An introduction to iterative Toeplitz solvers. SIAM, Philadelphia (2007)

Chen, M., Deng, W.: High order algorithms for the fractional substantial diffusion equation with truncated Lévy flights. SIAM J. Sci. Comput. 37(2), A890–A917 (2015)

Chen, W., Wang, S.: A penalty method for a fractional order parabolic variational inequality governing American put option valuation. Comput. Math. Appl. 67(1), 77–90 (2014)

Chen, W., Xu, X., Zhu, S.: A predictor-corrector approach for pricing American options under the finite moment log-stable model. Appl. Numer. Math. 97, 15–29 (2015)

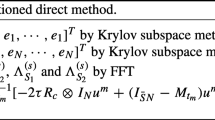

Chen, X., Ding, D., Lei, S., Wang, W.: An implicit-explicit preconditioned direct method for pricing options under regime-switching tempered fractional partial differential models. Numer. Algor. 87, 939–965 (2021)

Chen, X., Wang, W., Ding, D., Lei, S.: A fast preconditioned policy iteration method for solving the tempered fractional HJB equation governing American options valuation. Comput. Math. Appl. 73, 1932–1944 (2017)

Elliott, R.J., Osakwe, C.J.U.: Option pricing for pure jump processes with Markov switching compensators. Financ. Stoch. 10, 250 (2006)

Guo, X., Li, Y., Wang, H.: Tempered fractional diffusion equations for pricing multi-asset options under CGMYe process. Comput. Math. Appl. 76, 1500–1514 (2018)

Heston, S.L.: A closed-form solution for options with stochatic volatility with applications to bond and currency options. Rev. Financ. Stud. 6, 327–343 (1993)

Hu, J.: The estimate of \(\Vert {M^{-1}N}\Vert _{\infty }\) and the optimally scaled matrix. J. Comput. Math. 2(2), 122–129 (1984)

Khaliq, A.Q.M., Liu, R.H.: New numerical scheme for pricing American option with regime-switching. Int. J. Theor. Appl. Finance 12, 319–340 (2019)

Kou, S.G.: A jump-diffusion model for option pricing. Manage Sci. 48(8), 1086–1101 (2002)

Lei, S., Chen, X., Zhang, X.: Multilevel circulant preconditioner for high-dimensional fractional diffusion equations. East Asian J. Appl. Math. 6, 109–130 (2016)

Lei, S., Wang, W., Chen, X., Ding, D.: A fast preconditioned penalty method for American options pricing under regime-switching tempered fractional diffusion models. J. Sci. Comput. 75, 1633–1655 (2018)

Li, C., Deng, W.: High order schemes for the tempered fractional diffusion equations. Adv. Comput. Math. 42(3), 543–572 (2016)

Madan, D.B., Carr, P.P., Chang, E.C.: The variance gamma process and option pricing. Eur. Financ. Rev. 2, 79–105 (1998)

Meng, Q., Ding, D., Sheng, Q.: Preconditioned iterative methods for fractional diffusion models in finance. Numer. Meth. Part Differ. Equ. 31(5), 1382–1395 (2014)

Momeya, R.H., Morales, M.: On the price of risk of the underlying Markov chain in a regime-switching exponential Lévy model. Methodol. Comput. Appl. Probab. 18, 107 (2016)

Peiro, A.: Skewness in financial returns. J. Bank Financ. 23, 847–862 (1999)

Rachev, S.T., Menn, C., Fabozzi, F.J.: Fat-tailed and skewed asset return distributions: implications for risk management, portfolio selection, and option pricing. John Wiley and Sons, New Jersey (2005)

Saad, Y.: Iterative methods for sparse linear systems. SIAM (2003)

Serra-Capizzano, S., Bertaccini, D., Golub, G.H.: How to deduce a proper eigenvalue cluster from a proper singular value cluster in the nonnormal case. SIAM J. Matrix Anal. Appl. 27, 82–86 (2005)

She, Z., Lao, C., Yang, H., Lin, F.: Banded preconditioners for Riesz space fractional diffusion equations. J. Sci. Comput. 86(3), 1–22 (2021)

Stein, E.M., Stein, J.C.: Stock price distributions with stochastic volatility: an analytic approach. Rev. Financ. Stud. 4, 727–752 (1991)

Tour, G., Thakoor, N., Khaliq, A.Q.M., Tangman, D.Y.: COS method for option pricing under a regime-switching model with time-changed Lévy processes. Quant. Financ. 18, 673–692 (2018)

Wang, W., Chen, X., Ding, D., Lei, S.: Circulant preconditioning technique for barrier options pricing under fractional diffusion models. Int. J. Comput. Math. 92(12), 2596–2614 (2015)

Zhang, H., Liu, F., Turner, I., Chen, S.: The numerical simulation of the tempered fractional Black-choles equation for European double barrier option. Appl. Math. Model. 40, 5819–5834 (2016)

Zhang, H., Liu, F., Turner, I., Chen, S., Yang, Q.: Numerical simulation of a Finite Moment Log Stable model for a European call option. Numer. Algor. 75, 569–585 (2017)

Zhang, Q., Guo, X.: Closed-form solutions for perpetual American put options with regime switching. SIAM J. Appl. Math. 64, 2034–2049 (2004)

Zhou, Z., Ma, J., Sun, H.: Fast Laplace transform methods for free-boundary problems of fractional diffusion equations. J. Sci. Comput. 74, 49–69 (2018)

Acknowledgements

The author expresses gratitude for the issues and suggestions pointed out by the reviewers, which have significantly enhanced the rigor and readability of this paper.

Funding

The corresponding author is supported by the Natural Science Foundation of Guangdong Provincial Department of Education (2022KTSCX080) and National Natural Science Foundation of China (12301481). The first author is supported by Guangdong Basic and Applied Research Foundation (2020A1515110991) and National Natural Science Foundation of China (12101137).

Author information

Authors and Affiliations

Contributions

X. Chen wrote the main manuscript text and was responsible for debugging the program, and X. X. Gong and Z. R. She were responsible for creating the figures. Z. H. She provided the relevant theoretical analysis. All authors reviewed the manuscript.

Corresponding author

Ethics declarations

Ethical approval

Not applicable

Conflict of interest

The authors declare no competing interests.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Chen, X., Gong, XX., She, ZR. et al. A novel banded preconditioner for coupled tempered fractional diffusion equation generated from the regime-switching CGMY model. Numer Algor (2024). https://doi.org/10.1007/s11075-024-01769-0

Received:

Accepted:

Published:

DOI: https://doi.org/10.1007/s11075-024-01769-0

Keywords

- Banded preconditioner

- Tempered fractional partial differential equation

- European options pricing

- Regime-switching

- CGMY model