The New Normalcy and the Pandemic Threat: A Real Option Approach

1

Fondazione Tor Vergata, University of Rome “Tor Vergata” and Open Economics, Via Columbia 2, 00130 Rome, Italy

2

JPMorgan (Retired), 900 Larsen Rd, Aptos, CA 95003, USA

*

Author to whom correspondence should be addressed.

†

Retired.

J. Risk Financial Manag. 2024, 17(2), 72; https://doi.org/10.3390/jrfm17020072

Submission received: 12 December 2023

/

Revised: 26 January 2024

/

Accepted: 6 February 2024

/

Published: 12 February 2024

(This article belongs to the Special Issue Empowering Financial Intelligence through Informatics: Trends, Challenges, and Innovations)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

:This paper delves into the evolving post-pandemic business arena, focusing on how liability options and social norms are reshaping industry structures. We anticipate lasting transformations due to the emergence of new safety standards that bridge the gap between corporate interests and societal welfare. To foster these changes, effective post-lockdown economic policies could encompass not only rigorous social standards but also specific financial incentives. Examples of such incentives include tax relief for businesses implementing comprehensive health protocols and subsidies for those transitioning to remote work or modifying production layouts to minimize infection risks. Our analysis delineates two predominant operational frameworks for firms in this new environment: the liability and property regimes. These are determined by each firm’s financial outcomes and the extent of damages incurred, all measured against societal expectations. Firms within the liability regime may exhibit only partial compliance, often attributed to ambiguous standards and prevailing uncertainties, potentially leading to a dip in profits. In contrast, entities operating under the property regime are likely to engage in more extensive organizational restructuring. A key insight from our study is the paradigm shift in investment behavior, increasingly influenced by risk management, particularly in the strategic choice between liability and property rules. This shift is evident in how firms now prioritize managing potential external liabilities, such as environmental hazards or evolving regulatory landscapes, in their investment decisions. Consequently, the traditional growth-centric investment paradigm is being supplemented by strategies that emphasize safeguarding against various external risks, marking a significant realignment in corporate investment philosophies post-pandemic. This transition underscores the intricate interplay between economic policies, corporate strategies, and societal dynamics in the contemporary business milieu.

1. Introduction

In this paper, we examine the multifaceted stages of response that authorities face during a pandemic, with a focus on the concept of expiring options. During the initial outbreak, the government possesses the option to react aggressively to halt virus spread, weighed against the risk of overreacting to what might be a mild virus due to uncertainties in infection rates, mortality, and immunity. The alternative—deferring action to gather more information—risks delayed responses that could harm economic growth and political credibility.

As the pandemic progresses and the early response option expires, the government confronts choices in the next phase: expanding medical capacity to handle infection surges or imposing economic shutdowns to flatten the curve. These decisions are complemented by the option to initiate virus research, which can inform and support either strategy.

In the ensuing ‘new normalcy’ stage, with the economy operational but restricted, businesses face three types of potential third-party liabilities: government-imposed fines or shutdowns for standard violations, public backlash for inadequate safety measures, and legal actions from sickened workers or customers. These liabilities influence business decisions, ranging from remaining closed and operating at reduced capacity for safety to investing in protective measures or new technologies. Firms must thus weigh two strategies: the liability rule approach—accepting potential non-compliance risks for greater returns and the property rule approach—prioritizing full regulatory compliance to avoid risks but possibly incurring upfront costs or operational limitations. This decision reflects a firm’s strategic balance between risk management and business objectives.

This paper explores this new normalcy stage, highlighting the complex decisions businesses face amidst ongoing pandemic threats. We investigate how these decisions affect a company’s valuation and risk management strategy, particularly in choosing between liability and property rule approaches. The study underscores the economic challenges in high-risk environments, including the costs of implementing safety measures and their impact on profits and financial liabilities.

In the context of firms responding to COVID-19 regulations, the liability and the property rule respectively correspond to “adaptive strategies” and “transformative actions”, which can be defined as follows:

- Adaptive Strategies: These are the responsive measures that firms take to adjust and cope with the immediate challenges posed by COVID-19 regulations. Adaptive strategies typically involve short-term, tactical changes that allow a business to continue operating under new constraints. Examples include modifying workspaces to comply with social distancing guidelines, implementing remote working policies, or altering business hours to align with curfews and lockdowns. The focus of adaptive strategies is on resilience and maintaining continuity in the face of sudden and often temporary changes.

- Transformative Actions: Transformative actions, on the other hand, are more profound changes that firms undertake in response to COVID-19 regulations. These actions signify a fundamental shift in the way a business operates or engages with its market. They are strategic and long-term in nature and often result from a realization that the business landscape has changed irreversibly due to the pandemic. Examples of transformative actions include pivoting to new business models (like moving from in-store retail to e-commerce), innovating new products or services to meet emerging needs, or rethinking supply chain management to enhance resilience against future disruptions. Transformative actions are characterized by their forward-thinking approach and their aim to not just survive the current crisis, but to emerge from it stronger and more adaptable to future changes.

Both adaptive strategies and transformative actions are critical for businesses navigating the evolving landscape shaped by the pandemic, each playing a distinct role in ensuring short-term survival and long-term sustainability and growth.

Our analysis reveals that in situations where conflicting options from different parties exist, the typical ‘bad news principle’ in real option theory may not always apply. This principle states that if there is a possibility of unfavorable developments that could impact the decision or investment negatively (the prospect of “bad news”), it becomes more valuable to wait and gather more information before committing. In the presence of conflicting options, however, delaying action can be both a growing threat and a cost for the opposing party, underscoring the nuanced and dynamic nature of strategic decision-making in pandemic conditions.

The remainder of this paper is organized as follows. Section 2 delves into “The Liability Options of a Firm under Dynamic Uncertainty”, by examining the strategic choices firms face amidst evolving uncertain conditions. This is followed by Section 3 on the “Review of the Literature”, providing a comprehensive overview of existing research relevant to our topic. In Section 4, “A Model of Real Options of a Pandemic with Government Intervention”, we introduce a theoretical framework that integrates real option theory in the context of government and/or third-party actions during a pandemic. Section 5—“The Social Standard and the Liability Option”—delves into how societal norms influence and become part of a firm’s decision-making regarding liability. Finally, Section 6—“Endogenizing the Social Standard”—discusses the absorption of these societal norms into corporate strategies and interacting decision-making, leading to the “Conclusions” section that encapsulates our key findings and their broader implications, along with suggestions for further research avenues.

2. The Liability Options of a Firm under Dynamic Uncertainty

During periods of dynamic uncertainty, such as a pandemic, decision-making is fraught with complexity, particularly when it comes to irreversible commitments like investments or policy rollouts. The real option framework is instrumental in such contexts as it allows one to account for potential adverse outcomes by preserving the flexibility to postpone decisions. Nonetheless, interpreting investment solely as a real option owned by a single entity might not capture the intricate nature of decision-making during a pandemic. This is where the notion of a liability option comes into play, representing the potential costs that one party’s exercise of an option may impose on another, highlighting the interplay between these costs and inaction. In these circumstances, holders of liability options, like legal or regulatory bodies, can suffer significant repercussions if they do not take timely protective actions. Such repercussions might encompass a range of penalties or legal consequences in response to non-compliance or inaction. For instance, a pharmaceutical company deliberating over the release of a new vaccine must weigh the benefits of additional testing against the risk of liability claims. Hesitation or delay, while beneficial for product refinement, may incur liabilities from stakeholders or prompt governments to pursue other avenues, underscoring the delicate balance firms must maintain during a pandemic.

The real option approach highlights how decision-making, particularly in environments of dynamic uncertainty, is heavily influenced by the potential for downside risks. This approach is especially relevant in situations involving irreversible decisions, such as significant investments or the implementation of public policies. The key insight from the real option perspective is that, when faced with irreversibility, uncertainty, and the possibility of delaying decisions, the cost of taking an irreversible action must be outweighed by future benefits. In other words, the potential future benefits must substantially exceed the irreversible costs for it to be rational to proceed with immediate action. This approach emphasizes a cautious and measured response to decision-making, where the option to delay or defer action is valued due to the inherent uncertainty and the high cost of reversing a decision once made. It reflects a risk-averse stance, advocating for inaction or delayed action until more information becomes available or until the benefits more definitively outweigh the costs.

Conversely, the concept of a liability option presents a different paradigm that is related to the cost in addition to the benefit of inaction. In this context, failing to invest in an irreversible project can prompt those holding the option (such as regulatory bodies, legal entities, or other stakeholders) to take actions that might be detrimental to the decision-maker. This could include imposing regulations, sanctions, or pursuing legal action. The failure to act or invest timely, therefore, carries its own risks and potential costs as the inaction might trigger negative reactions from stakeholders who are affected by or interested in the decision.

In essence, while the real option approach advises caution in the face of uncertainty and irreversible costs, advocating for a delay until benefits are clear and significant, the liability option framework suggests that inaction or delay can itself be risky and potentially costly as it might provoke adverse actions from other parties. This highlights a more complex decision-making landscape, where the costs of both action and inaction, and the reactions they may provoke from stakeholders, must be carefully weighed.

In general terms, a liability option can be conceptualized as a potential risk or threat to one entity (Party A), stemming from the capability of another entity (Party B) to exercise a call option. This scenario is particularly relevant when both party A and party B must engage in costly actions but party A’s actions essentially depend on the power of party B to inflict damages as in the case of regulatory and legislative bodies, or natural forces or phenomena, such as “Mother Nature”, as Party B.

In this context, the value of the liability option for Party B is influenced by several key factors:

- Positive Correlation with Uncertainty and Payoff: The more uncertain the situation, the higher the potential value of the option held by Party B as uncertainty can increase the range of possible outcomes, some of which might be highly favorable to Party B. Additionally, the greater the potential payoff that Party B can extract from Party A, the more valuable the option becomes. For instance, in an environmental context, if a regulatory body (Party B) has the option to penalize a polluting company (Party A), the value of this option increases with the severity of the pollution and the potential fines that could be imposed.

- Negative Correlation with the Cost of Exercising the Call: The value of the option for Party B is inversely related to the cost of exercising the call. These costs can be influenced by the protective or preventive actions taken by Party A. For example, if Party A takes significant steps to mitigate the risk or potential damage (such as a company implementing rigorous environmental safeguards), it increases the cost for Party B to exercise its option (e.g., tougher enforcement or legal action), thereby reducing its value.

- Likelihood of Exercise: The probability that Party B will exercise the option is higher when there is lower uncertainty, greater potential payoff, and lower costs associated with exercising the option. This likelihood is a dynamic interplay of these factors, influenced by both parties’ actions. In the case of natural phenomena, if the risk to Party A (such as a community or business) from a natural disaster is high (greater payoff for nature in terms of impact) and the costs for nature to exert its force are low (e.g., due to lack of preventive measures by humans), the likelihood of this “natural liability option” being exercised is higher.

In summary, a liability option represents a complex interaction between two parties, where the value and potential exercise of the option are dictated by the interplay of uncertainty, payoff potential, and the cost of exercising the option, all of which are dynamically influenced by the actions of both Party A and Party B.

The case of a pandemic allows our analysis to be more concrete in applying the concept of liability options to a firm under stress and can be quite intricate. In this case, a liability option arises when external parties, such as customers, employees, the general public, or financial institutions like banks, hold the capability to exercise their choices or “options” in response to the pandemic. These choices can significantly impact the rights or obligations of the firm. A breakdown of how they can manifest is provided below:

- Customers: Customers might decide to minimize their interactions with the firm to reduce infection risk. This shift in consumer behavior can lead to decreased sales and revenue for the firm. If the firm operates in a sector where physical presence is crucial (like retail or hospitality), this shift can be particularly impactful.

- Employees: Employees might exercise their option to demand safer working conditions or to work remotely. This can lead to additional operational costs for the firm as they might need to invest in safety equipment or adapt their operations to remote work. In extreme cases, employees might refuse to work under conditions they consider unsafe, leading to labor shortages.

- General Public: The broader community’s response to the pandemic can also affect the firm. If there is a public outcry for stricter safety measures or if the public perception of the firm’s handling of the pandemic is negative, it could lead to reputational damage or increased regulatory scrutiny.

- Banks and Financial Institutions: Financial entities might alter their lending or investment policies in response to the pandemic. For instance, banks might become more risk-averse and reduce their lending to sectors heavily impacted by the pandemic, or they might increase interest rates to mitigate their risk exposure. This can affect the firm’s financial flexibility and access to capital.

- Government and Regulators: Government and regulatory bodies might exercise their option to introduce new policies, regulations, or sanctions in response to the pandemic. These could range from enforcing health and safety guidelines to imposing lockdowns or restrictions on business operations. Such measures can directly affect the firm’s ability to operate, its compliance costs, and overall business strategy.

- Regulatory Compliance: The cost and complexity of complying with new regulations or guidelines can be significant. Firms might need to invest in new infrastructure, technology, or personnel to meet these requirements.

In essence, each of these scenarios represents a form of liability option. The firm does not control these options; they are exercised by external parties. However, the firm must be prepared to respond to these exercises of options, which adds a layer of uncertainty and complexity to its strategic and operational planning during a pandemic. This dynamic uncertainty requires the firm to be agile and adaptable, constantly reassessing its strategies in light of evolving external conditions. Liability options, within the context of a firm’s operations, particularly during a pandemic, are a form of real options. However, unlike traditional real options, which often present opportunities for a firm to enhance its value, liability options typically have negative financial implications. They are real options because they represent choices or actions that external parties (like customers, employees, governments, and regulators) can exercise in response to the pandemic. These actions directly or indirectly affect the firm’s operations and financial standing and may reduce its real worth. They require that the firm constantly assess and respond to the external environment, often demanding rapid adaptation and flexibility. This can divert resources from growth-oriented initiatives, further impacting the firm’s long-term value.

The decision of the firm can also be seen in a context of interdependence of decisions among different players in the business ecosystem. In this respect, the liability option may partially be the result of other firms’ actions and not only of the regulator or an impersonal agent. Here, the application of game theory, as suggested by the works of Smit and Trigeorgis (2006), may become relevant. Although we do not explicitly develop the model by using a game theoretical approach, an interesting extension of our study could incorporate strategic interactions, where the action chosen by each participant would depend on the actions of others.

In this context, applying game theory could further help in understanding how businesses’ decisions to adopt certain liability or property rules are influenced not only by their own circumstances but also by the actions and reactions of other firms, regulatory bodies, and possibly consumers. For example, a firm’s decision to invest more heavily in organizational changes to adhere to social standards might depend on the expected responses of its competitors, the likelihood of stricter regulations being enforced, or the shifting preferences of consumers towards more responsible businesses. This perspective can also underscore the importance of anticipating and understanding the strategic moves of others in the industry, which is crucial for firms as they navigate the challenges and opportunities presented in a post-pandemic world.

While our study does not intend to develop a comprehensive game-theoretic approach to the issue at hand, the model does incorporate a unique aspect of interdependence. This form is elliptically expressed through the concept of a liability option for the firm and a corresponding option to sanction held by a regulator or an impersonal agency. In line with the game theoretical approach, this agency can be interpreted as a proxy for the collective behavior of other firms and consumers. This reflects an evolving social standard of regulation and sanction shaped by the interplay of business behavior and broader societal dynamics. Some examples of these connections are given below.

- Investment in Health and Safety Technologies: In this scenario, a firm’s decision to invest in health and safety improvements can be seen as a response to the liability option. This liability option represents the potential sanctions that a regulatory body might impose, reflecting societal expectations for safety. The firm’s decision-making process, influenced by the actions of other businesses and consumer expectations, demonstrates the interconnectedness of industry standards and societal norms.

- Flexible Work Policies and Regulatory Compliance: When firms consider implementing flexible work arrangements, they weigh the liability option of non-compliance with emerging work safety regulations. These regulations, enforced by a regulatory body, encapsulate the collective behavior and expectations of other firms and the workforce. A firm’s decision thus reflects a response to this broader social standard, where non-compliance carries the risk of sanctions, and compliance aligns with evolving industry practices.

- Strategic Alliances and Collaborative Ventures: In forming strategic alliances for risk mitigation, the liability option manifests in the potential regulatory repercussions of not adhering to industry standards, which are, in turn, influenced by the collective actions of firms and consumer expectations. The decision to enter into a collaborative venture is therefore not only a strategic response to direct competition but also to the overarching regulatory environment shaped by the broader business community and societal norms.

- Market Adaptation to Consumer Preferences: As consumer preferences shift post-pandemic, firms face the liability option related to market expectations. The regulatory or sanctioning body in this context could be interpreted as representing consumer behavior and social standards. Firms, therefore, adapt not just to direct market demands but also to the implied regulatory environment shaped by consumer-driven social standards.

- Response to Environmental and Social Governance (ESG) Expectations: In addressing ESG concerns, firms are responding to the liability option associated with the failure to meet these standards. This option reflects the sanctions or repercussions from regulatory bodies, which themselves embody the evolving social and ethical standards driven by other firms’ behaviors and societal pressure.

In each of these examples, the concept of a liability option held by the firm is intrinsically linked to the option to sanction by a regulator or an impersonal agency. This agency, reflecting the collective behavior of other firms and the expectations of society at large, emphasizes the interconnectedness of individual firm decisions within the broader context of evolving social and regulatory standards. This interdependence highlights the dynamic and complex nature of strategic decision-making in the post-pandemic business landscape, where actions are influenced by and in turn influence the collective ecosystem of businesses, regulators, and consumers.

3. Review of the Literature

Our investigation is centered on the emergence of liability options that materialize as contingent liabilities when one entity’s operations inadvertently inflict damage on others. These liabilities can arise from either individual actions or the implementation of specific contracts. In the realm of economics, these situations often relate to “externalities”, a concept rooted in Coase’s theory (Coase 1960). In the intersection of law and economics, these are observed when the exercise of rights goes beyond their initially intended scope.

This can be illustrated by the following two examples:

- A Manufacturing Plant’s Pollution: A manufacturing plant engages in production activities that, while lawful, result in the unintended discharge of pollutants into a nearby river. This scenario represents a classic externality. The plant, by exercising its right to produce, oversteps legal boundaries by polluting, assuming it lacks the legal authorization to release pollutants. Such an action can lead to liabilities under various legal categories, including criminal or administrative law (safeguarding societal rights) and civil law (particularly under property or tort laws). These liabilities in turn may materialize if the parties affected (including the courts or the regulators) decide to take action by exercising their option to do so.

- Construction Noise in a Residential Area: A construction company operates in a densely populated residential area. The company has the right to build, but its activities cause excessive noise, disrupting the lives of local residents, especially during early mornings and late nights. Here, the company’s right to construct collides with the residents’ rights to a peaceful living environment. If the construction noise exceeds legal limits or occurs during restricted hours without proper authorization, the company could face liability challenges from the residents affected. These could manifest as civil lawsuits (tort law) for noise pollution or administrative actions for violating local ordinances.

Both examples underscore the complex relationship between operational rights and contingent liabilities, particularly when these rights infringe upon the well-being of others or exceed legal limits.

The idea of a liability option is intimately connected to the concept of a social contract, both explicit and implicit, which is a fundamental element in various social and business interactions. This contract is established on the basis of shared norms, expectations, and often legal obligations that dictate the conduct of the involved parties. It is predicated on the assumption that all parties will comply with these mutually agreed conditions, deemed equitable and reasonable from the beginning (ex-ante). When a party perceives a deviation from these initial conditions, or that the original terms are not being honored, it may lead to the activation of a liability option (an option that is a liability for the party against which the action is directed). This typically happens if the party feels that persisting under these changed or unmet conditions would cause disproportionate harm or damage to their interests. In such cases, the party may view this as a breach of the social contract, thereby legitimizing their recourse to a liability option.

For instance, during a pandemic, if a company’s actions pose a significant risk to its employees, customers, or even the general public, this might be interpreted as a breach of the implicit social contract with the community and regulatory authorities. Such actions might lead the community or regulators to view this as a violation of the initial fair and reasonable conditions. As a consequence, they might exercise their rights to pursue actions that create liabilities for the company in question (the exercise of liability options), such as pursuing legal action or calling for more stringent regulations, to seek remedy for the breach and its resulting harm.

In essence, a liability option serves as a tool within both implicit and explicit social contracts, utilized when the perception arises that the initially established and equitable terms of the contract have been breached, thereby potentially or definitively causing harm. The value of this option, seen as contingent assets from the perspective of the affected party and as contingent liabilities from the viewpoint of the party responsible for the harm, hinges on the extent of deviation from legally sanctioned rights and the severity of potential sanctions for this deviation.

While not explicitly related to Coase’s theory or the theory of real options, the concept of the liability option is widely present in the legal literature and can be traced back to a seminal 1972 article by Calabresi and Melamed in tort law, which opened new avenues of research. In their landmark paper, these authors discussed the distribution of entitlements by law, allocating them either to the victim (under a property rule) or to the injurer (under a liability rule). They identified two primary remedies for rights violations: injunctions and monetary damages, classifying the former under property rules and the latter under liability rules. Their argument that legislators should allocate rights to those who value them most highlights the challenges faced due to information asymmetry, which can lead to rights being assigned to those who least value them. This underscores the complexities involved in evaluating subjective valuations of these rights and the subsequent impact on legal and social contracts.

Subsequent scholarly work has focused on finding the most effective mechanism to extract information from those holding entitlements and to price subjective preferences efficiently. Three main themes have emerged. First, Coasian bargaining mechanisms suggest that irrespective of how rights are initially allocated, parties will negotiate to transfer these rights, ideally leading to their possession by those who value them most. However, the same information asymmetries faced by legislators can also affect private parties, potentially leading to inefficient pricing. Second, litigation and judicial intervention are based on laws permitting rights to be traded non-consensually, achieved by assigning absolute rights protection mechanisms. For example, a polluter may compel a party to sell their right to clean air at a certain price, which is set based on the type of protection scheme assigned. Scholars have delved deeper to discuss which protection schemes enable the most efficient non-consensual transfers, essentially determining which rule best extracts value information and fully compensates the party deprived of their right. Finally, other mechanisms have been suggested such as Solomonic rules and alternative mechanisms to extract information.

In recent legal scholarship, significant contributions have been made by authors like Morris (1992), Krier and Schwab (1995), Avraham (2006), and Ayres and Goldbart (2001), particularly concerning the management of harmful activities like pollution. These studies resonate with the challenges faced by firms during the COVID-19 pandemic in adapting to new regulatory landscapes and potential liabilities. For example, research by Atella and Scandizzo (2023) suggests regulations requiring companies to suspend certain operations during the pandemic and provide compensation for prevented damages or losses.

The foundational work of Calabresi and Melamed (1972), further Id by scholars, such as Cooter and Ulen (1986) and Ayres and Goldbart (2001, 2003), emphasizes the efficiency of property rules in contexts where transaction costs are minimal. However, they have acknowledged that in scenarios marked by significant disruptions like environmental crises or pandemics, the legal system often seeks a balance between assigning damages and enforcing injunctions. This balancing act is evident in the COVID-19 pandemic response, where businesses were often required to adjust their operations and offer compensation, as opposed to facing outright shutdowns. This strategy reflects a more adaptable approach to pandemic management, focusing on operational modifications and reparations rather than total cessation.

Emphasizing the vital connection between Ronald Coase’s economic theories and the legal frameworks developed from the fundamental analysis of Calabresi and Melamed is crucial for a deeper understanding of decision-making in economics and law. Coase’s groundbreaking work on externalities in economic transactions underpins the importance of information in managing these externalities, a concept that Calabresi and Melamed extended into the legal domain by exploring the legal allocation and infringement of rights. Joseph Farrell’s (1987) analysis of the Coase Theorem, particularly regarding information dynamics, highlights the challenges businesses face in making decisions amidst information asymmetries, especially during the pandemic. This relates to Coase’s insights on the critical role of information in the negotiation and management of externalities, which is a cornerstone in the legal perspectives developed by Calabresi and Melamed. The evolution from an ex-post to an ex-ante approach in legal literature, as pointed out by Bar-Gill (2014), mirrors this relationship. The ex-ante approach emphasizes the initial allocation of rights and the influence of legal rules before events like a pandemic occur, aligning with Coase’s principles and their practical application in business strategy during the COVID-19 crisis.

For example, consider a scenario where a manufacturing company faces new environmental regulations to reduce emissions. This situation echoes Coase’s theories on negotiating externalities, where the company must balance its economic activities with the environmental impact. Calabresi and Melamed’s legal frameworks come into play as the company navigates these regulations, deciding whether to invest in cleaner technologies (property rule approach) or risk potential penalties (liability rule approach). Knudsen and Scandizzo’s (2005) exploration of how social standards influence investment decisions underlines the complexity of these choices in uncertain environments, demonstrating the ongoing relevance of understanding the interplay between Coase’s economic theories and the legal principles established by Calabresi and Melamed.

In the business accounting and management literature, liability options are evoked by Luckner et al. (2003) in exploring the rise of the concept of Enterprise Risk Management (ERM) compared to the traditional Asset Liability Management (ALM). ERM involves a broad and integrated approach to managing the various risks an organization faces, which directly relates to how a firm might handle liability options. As stated by the authors, these options, which are decisions or actions by external parties that affect the firm, represent a form of risk that needs to be identified, assessed, monitored, and managed, all of which are key components of ERM. For example, recent studies include an analysis by Subramanian and Vrande (2019) concerning the intensity of human capital in innovative projects as a potential liability for pharmaceutical companies due to its role in delaying the discontinuation of unsuccessful projects.

The duality between property and liability rules in our study parallels the entrepreneur/manager duality in option chain and management theory (Burger-Helmchen 2009), emphasizing their contrasting roles in innovation-driven industries. According to this approach, entrepreneurs generate new real options through innovation and risk-taking, while managers evaluate and execute these options in line with strategic objectives. This dynamic, which is crucial in industries requiring constant innovation may determine why, in a resource-based framework, some firms chose to stick with adaptive strategies (following liability rules), while others identify and value new real options, fostering option creation (developing property rule). This difference may explain some of the heterogeneity in firms’ resource accumulation and capability development as different entrepreneurial and managerial approaches lead to diverse strategies.

Similar to the theme of our paper, Naboush and Alnimer (2020) explored whether the transmission of COVID-19 falls under the definition of an ‘accident’ as per aviation conventions and examined the extent of air carrier liability in cases where passengers contract COVID-19. Against the background of the increased liabilities from the COVID-19 pandemic, Gerard et al. (2020) presented a summary of potential policies that could constitute a thorough social protection strategy in countries with low and moderate incomes, including examples of specific policies that have been implemented in such contexts. Several studies have applied real option models to analyze business and government reactions to the pandemic, but they typically do not consider the difference between property and liability rules. For example, Chakhovich and Marttila (2020) discussed how the COVID-19 pandemic has significantly impacted individuals, businesses, and governments globally, creating a climate of uncertainty in the business realm. Their study applied the concept of real options to examine the uncertainty surrounding COVID-19, with a particular focus on government responses. It explored how governments have strived to maintain flexibility in their decision-making by keeping various options open by also delving into specific real options, trying to assess how uncertainty and cognitive biases might shape decision-making through real options. In a similar vein, but concentrating on post-pandemic opportunities, Wang et al. (2023) applied a real option approach to investment behavior, finding a link between circuit breakers and lockdowns, with a counterintuitive effect on global business and trade growth. In this context, an important role appears to be played by ‘time-to-build’ real options, enhancing adaptive and transformative growth in government and corporate sectors. The authors found that, while some sectors grow faster, managing investment remains a complex endeavor, with a notable interplay between government actions and corporate sector values, where governmental decisions directly influence corporate strategies and valuations.

The notion of liability options has direct implications for the decision of whether to adopt property rules or liability rules during a pandemic since it hinges on the nature of the investment required. Property rules necessitate upfront investments to ensure compliance with regulations, such as a hospital investing in advanced air purification systems. Conversely, liability rules do not require immediate investments but expose firms to potential costs or penalties if they fail to comply, like a restaurant opting to continue regular operations instead of redesigning its dining area for social distancing. The choice between these two approaches intuitively depends on the firm’s risk appetite and financial standing, as property rules provide upfront certainty but may be costly, while liability rules defer costs but expose firms to potential liabilities.

4. A Model of Real Options of a Pandemic with Government Intervention

4.1. The Main Lines of the Model and Its Interpretation

In order to explore the implications of social and corporate options of liability and property rule strategies, we developed a simple real option model based on stylized characters of a firm and social agent (the government or a regulator) under the stressful condition of an advanced (possibly final state) of a pandemic. The model explores the interplay between firms and governments during pandemics, focusing on the strategic adjustments that both parties make to balance economic recovery and public health. A key assumption is the existence of a social tolerance threshold (R), representing the level of damages that society deems acceptable without government intervention. When the accumulation of damages exceeds this threshold, governments are expected to intervene with regulatory measures like lockdowns or social distancing guidelines, aiming to curb the pandemic’s spread. Firms, on the other hand, face revenue losses due to government-imposed restrictions. Additionally, if their safety measures fail to meet the socially acceptable Ik level (R), they may be held liable for excess damages, further impacting their financial well-being.

To illustrate this dynamic, an example of a restaurant operating during a pandemic can be considered. As customer density increases, so does the risk of contagion, and the resulting damage given by the product of customer density by the expected damage, potentially triggering government intervention in the form of restrictions. If the restaurant’s safety measures fall short of public expectations, exceeding the acceptable risk level, it faces not only revenue losses from restrictions, but also potential legal liabilities related to contagion outbreaks. Another example is a manufacturing firm whose increased production might lead to higher social density due to increased employment and transportation needs. Under an ongoing pandemic, this increase in social density, combined with the firm’s production activities, could accelerate the spread of contagion (X) and lead to more damage (QX).

The model’s results, while hypothetical, offer the possibility of multifaceted across various domains. They may provide valuable insights for policymakers in crafting and adjusting public health measures while aiding businesses in strategizing to mitigate operational disruptions caused by the pandemic. They may also suggest strategies for risk management, allowing for the identification of critical points where intervention becomes necessary. Above all, the model findings may enhance our understanding of the delicate balance between health and economic considerations during a pandemic and highlight key features of the complex reasoning behind necessary health measures.

As mentioned above, the model depicts a pandemic as a continuous random diffusion process (X), where the rate of contagion correlates with social density, like the concentration of workers or customers in a given area. This rate of contagion is linked to the level of economic activity (Q), resulting in damage level QX. Should this level exceed a critical social tolerance threshold (R), it triggers government intervention with measures like lockdowns or social distancing to control further spread. The process X is modeled following Dixit and Pindyck (1994) as a Wiener process with drift, according to Equation (1):

where is a stochastic variable equal to the increment of a Wiener process, is its drift parameter, and is its standard deviation. The term is a normally distributed random variable such that and .

Equation (1) posits that a pandemic can be modeled as a continuous random diffusion process, where the variable represents the spread of the disease. The spread is assumed to follow a Wiener process with drift, meaning that it includes both a consistent trend and random fluctuations. The increment in this process is by a stochastic variable that follows a normal distribution, with an expected value of zero, indicating that there is no predictable change on average. This mathematical formulation is a simple but effective way to capture the unpredictable nature of a pandemic’s spread and its complex interaction with societal and economic factors. It acknowledges that, while we can identify general trends (like an overall increase or decrease in cases), the exact trajectory at any given moment is subject to random variations. This is crucial for understanding the complex interaction of the pandemic with societal and economic factors, as these interactions can significantly influence the disease’s spread in ways that are not always predictable.

In sum, the model uses mathematical principles to represent how a pandemic spreads and how it interacts with social and economic factors. Its key components can be summarized as follows:

- Continuous Random Diffusion Process (X): The pandemic’s spread is modeled as a continuous random diffusion process, represented by the variable ‘X’. This approach is used to describe the way the disease spreads over time, incorporating both predictable patterns and random fluctuations, which is characteristic of how infectious diseases propagate in a population.

- Correlation with Social Density: The model posits that the rate of contagion is closely linked to social density. Social density refers to how closely packed individuals are in a given area, like in workplaces, shopping centers, or public transport. High social density typically leads to a higher rate of contagion because the virus can spread more easily when people are in close proximity to each other.

- Linkage of Damage (Q) to Economic Activity: The damage to economic activity, denoted as ‘Q’, is another crucial factor in this model. Economic activities bring people together, either as workers or consumers, increasing social density. The model suggests that the level of economic activity is directly linked to the rate of contagion; more economic activity usually means higher social density, which can lead to a higher rate of contagion.

- Damage Proportionate to QX: The model implies that the damage caused by the pandemic (in terms of health, economic impact, etc.) is proportionate to the product of ‘Q’ (damage to economic activity) and ‘X’ (rate of contagion). This means that, as either the economic activity or the rate of contagion increases, the overall damage or impact of the pandemic also increases.

- Critical Threshold (R): The model introduces the concept of a critical threshold ‘R’. This threshold represents a point at which the combined effect of economic activity and contagion becomes of such concern for society that public action is enabled. It could be measured in terms of healthcare system capacity, economic strain, or social disruption.

- Triggering Government Intervention: When the rate of damage (QX) surpasses this critical threshold ‘R’, it prompts government intervention. These interventions could include measures like lockdowns, social distancing mandates, or restrictions on economic activities. The purpose of these interventions is to reduce the rate of contagion (and hence the product QX) to bring it back below the critical threshold, thereby controlling the further spread of the disease and its impact.

In essence, the model aims to provide a framework to understand the dynamic interplay between a pandemic’s spread, social density, economic activity, and government interventions. It highlights how these factors are interdependent and how balancing them is crucial in managing the impact of a pandemic. While the work reported in this paper does not include specific validation tests, it lays a foundational groundwork for planning future validation efforts. This involves comparing the model’s predictions against real-world pandemic data and outcomes from established models. Scenario analyses, expert evaluations, and iterative updates using new data are integral to this process. Collaborative research initiatives will further enhance the model’s robustness. Although not yet validated, the model does provide indications and methodologies for future research to test and refine its predictive efficacy and accuracy.

4.2. The Decision-Making Process

With respect to the process considered, we assume that two decision makers are involved: (i) a private business and (ii) a government agent holding a contingent right to restrict the economic activity of the private firms if the risk of damages from the diffusion of the infection following its normal operations exceeds a threshold of social tolerance (i.e., a “social standard”). The private firm concerned is assumed to be penalized by restrictive measures prescribed by the government on social distancing and other security and medical controls in proportion to revenue foregone from applying the social distancing and security regulations. In turn, these restrictions are assumed to reduce the firm’s expected output or to increase its costs. In addition to this proportional loss, the firm is also faced with the threat of having to pay excess damages if its measures to comply with regulations fall short of the “danger level” corresponding to an established social standard, defined as the maximum level of damages tolerable by society. This level and the right to extract compensations for excess damages are assumed to be established by law, regulations, or jurisprudence. This condition can also be interpreted in the spirit of the “precautionary principle” as a combination of the potential victim’s right and injurer liability, contingent on the attainment of a “threshold of danger”, which makes a proportional fine insufficient to account for the risks involved in raising the overall level of damages.

As a decision maker, the firm faces the choice between two alternatives. The first alternative, which consists of the liability rule, is for the faculty to try to abide by the restrictive rules (e.g., maintaining a minimum distance between workers and between customers, sanitizing with the required frequency, etc.) by taking limited measures, such as reducing the firm’s scale of operations (for example, by reducing labor intensity in manufacturing or by servicing a lower number of customers per unit of space in entertainment and restauration establishments) and/or by investing in measures that reduce the probability of violating the norms and incurring into the sanctioning domain of the public agency. However, compliance would be plagued by the liability option, e.g., the threat of being fined, restricted, or locked down because compliance is judged unsatisfactory, the social standard has become more restrictive, and/or the measures taken are, voluntarily or involuntarily, insufficient to prevent the spread of the virus. The second alternative is the property rule, that is, the faculty to use the firms’ property rights to remove the threat. This can entail, for example, investing in a radical reorganization of the production processes, through the construction of a new workplace, the introduction of new technologies and modes of work (e.g., distance working), and other changes that drastically reduce the threat of contagion and essentially eliminate the possibility (and the need) of control on the part of the public regulator. We assume that adopting this strategy, according to a protocol established by the government, would also remove the threat of any fine or restrictive measure from the public regulator. Choosing the property rule thus may imply an investment cost in reengineering the production process that can be considered equivalent to a once-and-for-all commitment of resources which could immediately reduce the expected value of the threat that the firm may contribute to the spread of the same or a similar infection in the present or future. The private adopter’s incentive to voluntarily pay these excess damage costs to comply with the social standard derives from a “liability option”, i.e., an option to proceed against the firm by other parties (a regulator or the parties damaged) based on the government’s coercion power or the right to sue for damages through the court system.

More specifically, we assume that the firm faces the problem of selecting between two strategies: (1) adopting a liability rule approach, which entails pursuing maximum expected profit by continuing business as usual, despite incurring costs and being exposed to potential liabilities, or (2) opting for a property rule strategy, requiring a complete overhaul of operational modes to eliminate or significantly reduce any risk of causing contagion and violating social standards. This choice can be formally expressed as follows:

In expression (2), is the present value of the firm’s profit at the appropriate rate of discount , is the cost to comply and/or to avoid the regulator’s fine, and the liability option, i.e., the option of the regulator to sanction the firm in case of insufficient compliance. In expression (3), is the rate of damage per unit of output, , is the expected value of the damages over the time horizon of production, is a social standard defining a maximum tolerable level of potential damages from the point of view of society, and is the option of the firm to switch from compliance to technology at the investment cost , which we assume is approved by the regulator, thus eliminating the possibility of being sanctioned and drastically reducing the probability of giving rise to a significant level of contagion.

The parameter will generally be greater than one and can be interpreted as the average investment cost that the firm would have to bear to close the gap between the damage generated and the social standard. Aligned with the real option theory and the foundational model by McDonald and Siegel (1986), we view the firm’s investment opportunity as akin to a perpetual call option. This means the firm has the right, but not the obligation, to purchase an asset at a predetermined price. In our study, we propose that the investment opportunity arises due to an option held by an external entity, like a regulatory body. This option is seen by the firm as a contingent liability, presenting a risk that could prompt the firm to engage in costly compliance activities. These actions could manifest as heightened operational costs to ensure adherence, yet still leaving the firm vulnerable to potential sanctions under a liability rule framework. Alternatively, the firm might opt for a one-time investment that eliminates the risk of non-compliance, aligning with a property rule approach.

The social standard, which serves as a benchmark for acceptable levels of a firm’s operations that could cause harm, is not a static measure and may evolve in response to changing circumstances. This standard could manifest in various forms, such as mandatory social distancing protocols for customers and employees, required use of special protective equipment, or specific sanitation practices. For instance, a restaurant might have to adhere to a social standard of maintaining a certain distance between tables or ensuring all staff wear masks. It is important to note that this social standard can shift, particularly in response to the evolving severity of situations like a pandemic. If the pandemic intensifies, firms might anticipate a tightening of these standards. A business, such as a retail store, might initially be required to limit customer capacity to 50%, but with worsening conditions, this limit could be further reduced. Similarly, a manufacturing plant might face more stringent safety inspections or be required to implement additional protective measures for its workers. Moreover, the social standard is an endogenous benchmark, reflecting the balance between the operational needs of firms and broader societal health and safety concerns. As the situation, such as a pandemic, escalates or de-escalates, firms must be prepared to adjust to potentially stricter or relaxed standards accordingly.

Expressions (2) and (3) encapsulate the dilemma faced by private firms regarding the potential spread of contagion through their operations, characterized by crowding effects and contamination risks. The government, or any other agent empowered by the circumstances, represents the potential action in response to the threat posed by the infection’s spread. Essentially, this situation posits contagion as an external cost of economic activities, which could be mitigated by imposing penalties on those responsible for exacerbating it. Thus, the expression highlights how a contagion linked to the intensity of a firm’s activities can be addressed through external penalties, internalizing the externality. Expression (3) outlines the scenario where a private firm opts to invest in technology that definitively meets the social standard, thereby eliminating any significant risk of contagion. In this case, the firm aligns with a property rule, proactively addressing the issue. Conversely, if the firm chooses not to make such an investment (thereby following a liability rule), it remains vulnerable to potential fines proportionate to the excess damage it causes, such as the number of deaths beyond a socially accepted limit. The function in expression (3) symbolizes the value of a liability option that may be exercised against the firm if its business-as-usual activities create a level of negative externality that surpasses a pre-determined social threshold. The firm has two choices: it can either disregard this risk and continue facing potential fines or other abatement costs (a proportion of the expected excess damage), or it can eliminate this threat through costly innovation under a property rule. This decision involves weighing the immediate cost of eliminating the threat against the ongoing risk of facing uncertain, potentially substantial liabilities. The function thus represents the option value of a liability, which can be exercised against the firm if the negative externality generated by the health crisis reaches the critical value of an enforceable social standard. The firm can ignore this threat, or it can decide to remove it by engaging in costly innovations under a property rule. In doing so, it would compare the disadvantage of removing the threat by engaging in costly investment against the advantage of not continuing to face a threat of uncertain magnitude. For simplicity and to clarify the relationship with the size of the threat, we assume that investment costs would be equal to a given proportion of expected excess damage.

4.3. The Dynamics of the Liability Option

Considering the liability option , its present value can be determined using dynamic programming. Starting at an initial , the condition for the optimum (the Bellman equation) prescribes that, in the continuation region (i.e., where the option is not exercised), the option value be equal to the present value of its expected capital gains:

where r is the appropriate rate of discount.

Equation (4) states that, to maximize the present value of the option, the holder (e.g., the government or the regulator) is to equate, in continuing time (that is, at the margin between holding and exercising the option), the value obtained by exercising the option to the expected present value of the future capital gains obtained by holding it. The expression can be expanded using Ito’s Lemma (see Dixit and Pindyck (1994)). Using primes to denote derivative yields the following expression:

Substituting for using (3), with , gives the following expression:

The solution to (6) is:

where , are the roots of the characteristic equation:

The first term on the right-hand side of (7), , increases with the level of output, which is consistent with the expected value of the sanction increasing with output under noncompliance. Thus, this term is greater than zero. The second term, on the other hand, goes to infinity as the level of output grows without limits. The constant B, therefore must be zero.

A similar analysis can be applied to the option held by the firm to apply a property strategy by investing in the new contagion-free technology, yielding:

where the term with the negative root has been dropped because, as in the case of the liability option, the value of the option would go to zero as output grows without limits.

5. The Social Standard and the Liability Option

5.1. The Value of the Liability Option

During a pandemic, through a lack of hygienic measures and excessive crowding of customers or workers, a business operation can create negative externalities that contribute to exacerbating the severity and reach of the infection. When the anticipated damage caused by its activities crosses a certain limit, which is deemed the maximum acceptable level by an external body (like the government, a public organization the parties affected, or even “mother nature”), this entity may gain the authority to act. Such intervention, possibly via executive measures or legal channels, will generally be intended to curb the spread of the pandemic and limit the damage to the parties involved. This might involve enforcing actions such as lockdowns or specific social distancing measures, and the intervention can be characterized as a “liability option” for the party affected, which can be prevented or compensated for by the right to recoup a portion of the damage undergone. Concurrently, the business affected will incur avoidance costs, which could include measures to comply with the imposed restrictions or to minimize further damages; these measures are subject to the discretion of the firms. Firms can strategically adjust these costs in a manner that is most conducive to their interests, balancing compliance with profit maximization.

The value of the liability option1 can thus be established by using the following “value matching” and “smooth pasting” conditions (Dixit and Pindyck 1994, pp. 108–9), which result in the following expressions:

Equations (10) and (11) delineate the threshold conditions for the option’s exercise by its holders, such as the regulator. Equation (10) mathematically represents the option’s value from the holder’s perspective on the left-hand side, contrasting with the potential returns from exercising the option on the right-hand side, as detailed by Dixit and Pindyck (1994, p. 108). This equation implies that the option’s value, acting as an asset for the holder (e.g., the regulator) and a liability for the party subject to it (e.g., the regulated firm), is tied to the expected excess damage over the social norm R, minus the cost C. This cost is a consequence of the expenses incurred by the liable party to shield itself from the regulator’s actions. It reflects the firm’s efforts to reduce production, limit contagion effects, or avoid detection of noncompliance, all while operating within the Business as Usual (BAU) regime and thus facing potential regulatory sanctions. Equation (11) frames this scenario in marginal terms, indicating that exercising the option is justified for the regulator only if the benefits offset these protective costs, and any slight increase in costs must be balanced by a corresponding increase in benefits. The parameter plays a key role by determining the level of the sanction as proportional to the damage in excess of the acceptable social threshold . It is worth noting that the expression for the social standard is equivalent to a cost in (10), in the sense that it reduces the amount of damage that may be tolerated before considering an action. Equation (11), on the other hand, states the condition that, at the optimum, the marginal benefits for the regulator, and implicitly for society, from exercising the option should equal the marginal costs.

By solving the system of Equations (10) and (11), we obtain the value of the threshold (corresponding to the value of expected social cost from the increased risks of the spread of the infection) at which the option of imposing the penalty may be expected to be optimally exercised by the regulator:

Equation (12) embodies the main result of real option theory, which consists in a rule of action depending on a threshold of costs (in this case, the present value of the sum of the social standard plus the effective cost of protection) multiplied by a factor greater than unity that incorporates a sort of objective risk aversion. In this equation, the social standard is equivalent to a cost, indicating the point where the pandemic’s effects are sufficiently large to require possible action. This equivalent cost is adjusted to include the additional costs the regulator will face due to the protective actions implemented by the regulated entity. Because of uncertainty, the value of the damage at which the penalty should be levied on non-compliant firms would not coincide with this summation but would exceed since is negatively related to volatility.

From (11) and (12), we can also obtain the value of the constant :

Thus, the explicit expression for the liability option is as follows:

5.2. The Reaction of the Firm under the Liability Rule

If the firm chooses to follow the liability rule, in order to maximize profits, it sets the cost to maximize the present value of profits defined in expression (2). This implies differentiating Equation (2) with respect to , taking account of (14) and equating to zero:

From (15), solving for , we find that:

This value indicates the profit-maximizing level of the cost of protection for the firm affected by the liability option. However, it must be noted that this cost is not fixed but must be adjusted continuously to reflect the current value of the damage. By substituting into Equation (12), we obtain the expression for the threshold of the sanction with the firm pursuing optimal cost adjustment under a liability rule. By substituting the result given by (16) into (12), we obtain the expression for the sanctioning threshold conditioned by the profit maximizing firm:

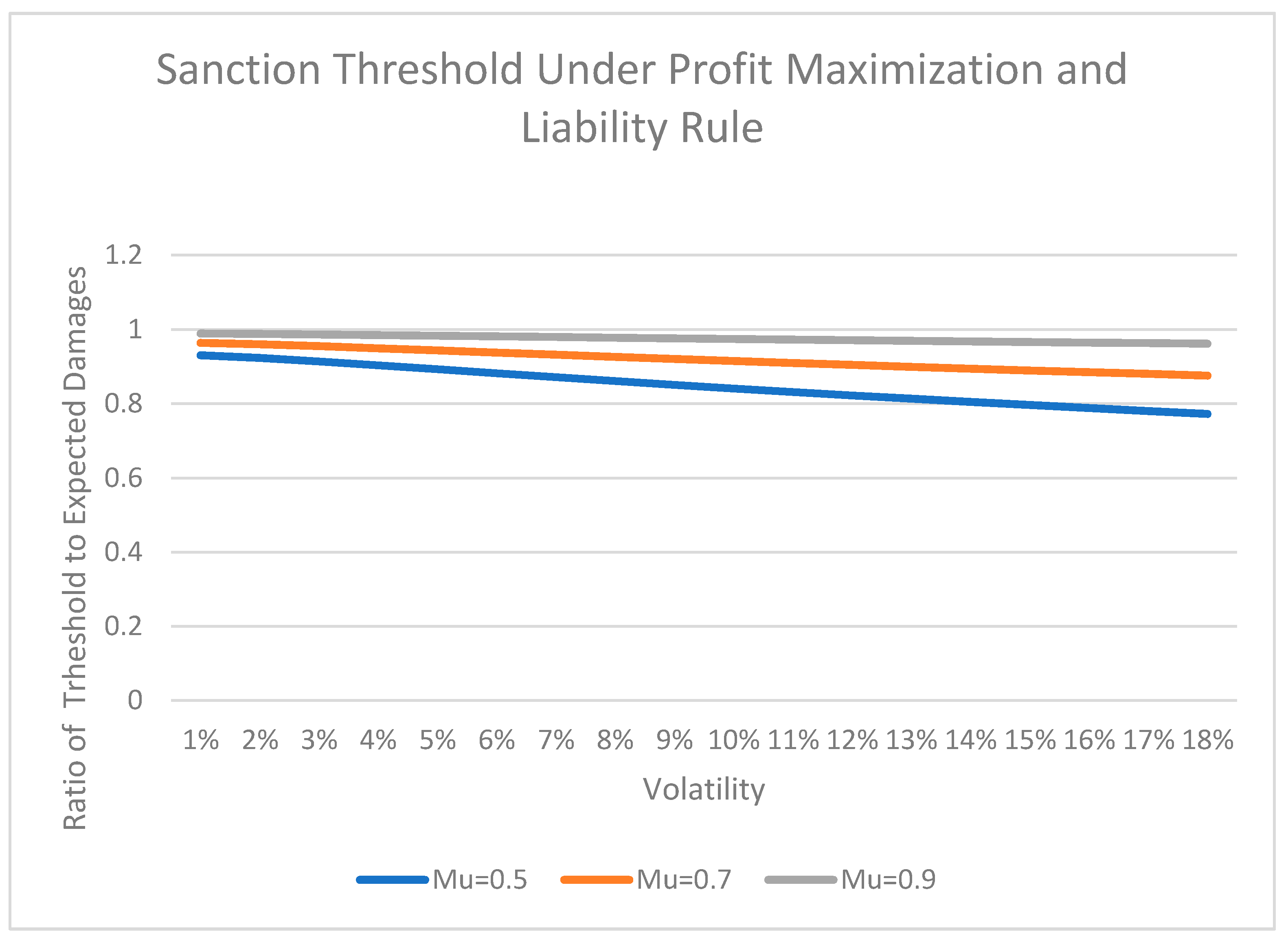

Expression (17) and Figure 1 show that by setting the costs at the profit-maximizing level indicated by (16), the firm may succeed in keeping the regulator in an area of permanent inaction, with the intervention threshold above the current value of the damages of a factor depending positively on both private cost-effectiveness and uncertainty. However while this result appears to validate the efficacy of a liability rule, it requires that the firm continually adjusts its current costs to the stochastic trajectory of the damage function, with even a temporary failure to do so exposing it to the risk of being sanctioned. Moreover, if a sufficiently large number of firms adopt this strategy, the result may be greater infection levels and, as a consequence, a more restrictive standard and greater penalties. Thus, the adjustment may require growing costs without completely eliminating the threat of the liability option.

By substituting into (14), we also obtain:

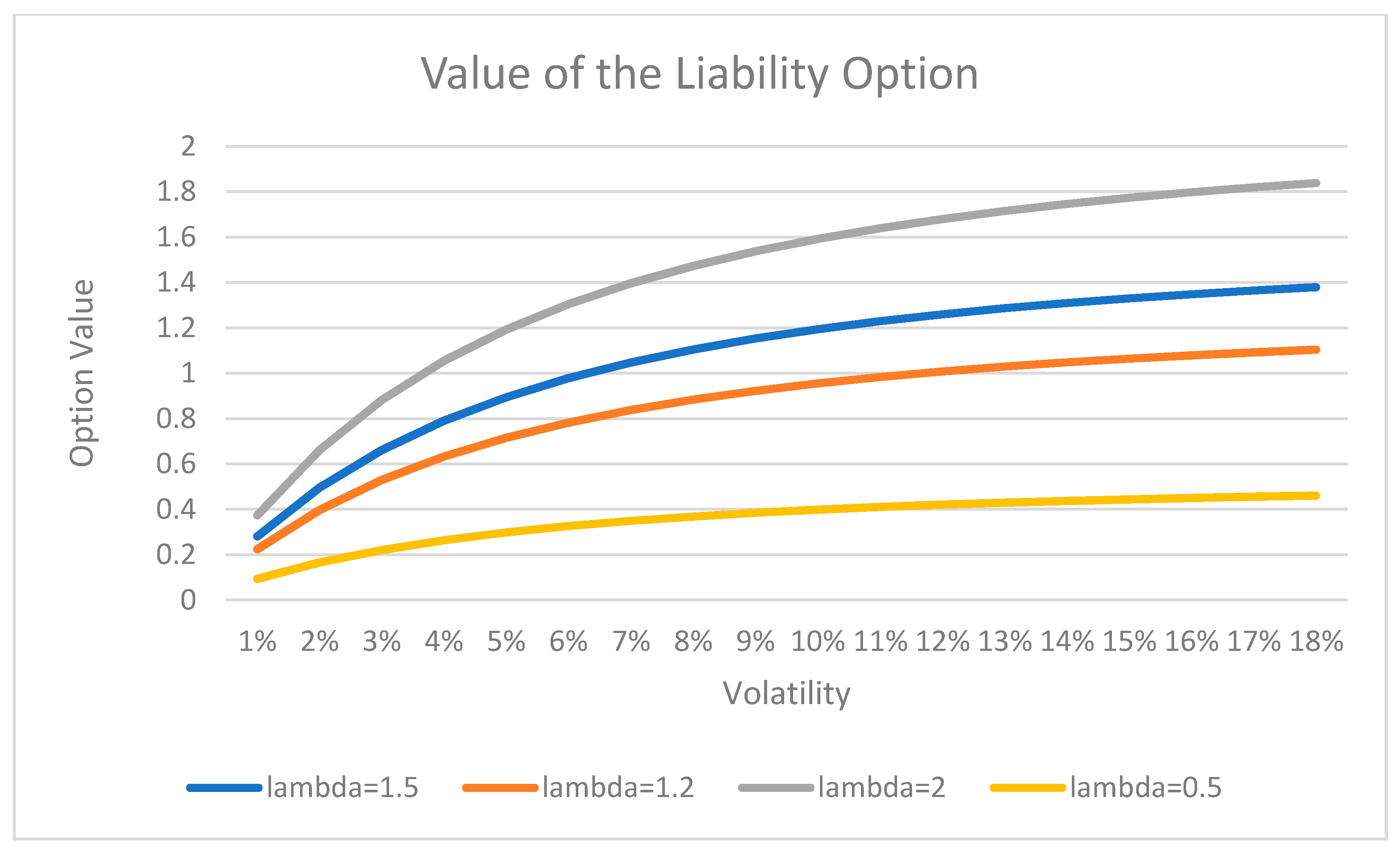

It must be noted that expression (18) identifies the value of the option to wait (the amount of reparatory payments foregone) rather than to sanction the firm from the point of view of society (represented by the figure of the regulator) and that this value depends only on the current value of the damage and not on the social standard. As in the case of the threshold, at the optimum protection cost, the value of the option will thus equal to a proportion of the expected damage and will be larger, with greater uncertainty (the lower ), the lower, coeteris paribus, private efficiency in compliance and/or protection costs. As Figure 2 shows, the value of the option increases less than proportionally with increases in volatility and is higher, the higher the sanction rate ( that can be applied to noncompliance.

By substituting (16) and (17) into (3), we obtain the value of the maximum profit under the liability rule:

Expression (19) implies that the expected profits of a firm will decrease as the social standard becomes more stringent (indicated by a lower R), meaning that a lower level of tolerable contagion is set before the firm is deemed non-compliant with mandated restrictions.

Expressions (16) and (19) show the levels of profits and operational costs that meet the social standard while minimizing the value of the liability option. However, these cost values must be periodically adjusted to remain compliant with a consistent standard in the face of infection rate volatility. This need for periodic adjustment introduces additional uncertainties and risks as the firm must continuously adapt to changing conditions to maintain compliance. It must also be noted that expression (19) can be interpreted as a statement of the Coase theorem. It implies that under the hypothesis of profit maximization, the introduction of the liability fully internalizes the externality if there are no transaction costs or other inefficiencies ( and the social standard (the degree of tolerance for the damage inflicted) is zero. In this case, in fact, expression (19) simply becomes the profit level net of the value of the damage, i.e., private benefits minus social costs:

In summary, these expressions provide a nuanced understanding of how firms can strategically manage their finances while adhering to social standards and minimizing liability in an unpredictable environment like a pandemic. The model’s alignment with the Coase theorem under specific conditions further enriches its theoretical relevance, offering a comprehensive framework for analyzing the economic and social implications of business decisions during health crises.

5.3. Adopting the Property Rule

By substituting (18) and (19) into Equation (3), we can now impose the value matching (benefits = costs) and the smooth pasting condition (marginal benefits equal marginal costs) to the option to act on the part of the firm. This allows us to find at which level of expected damages the firm may conclude that it is more convenient to switch to the new mode of production (i.e., to adopt the “property rule”), accounting for the uncertainty that this level will be higher or lower in the future:

In (21), as indicated in expression (3), is the investment level that assures compliance to a technology, which we assume is approved by the regulator, thus eliminating the possibility of being sanctioned and drastically reducing the probability of giving rise to a significant level of contagion.

Through the development of these conditions, the model allows one to pinpoint the ideal time for a firm to change its operational strategy. For simplicity, it is assumed that the firm has already maximized its profits under a liability rule before this point. This assumption serves as a basis for determining an upper bound in the model’s calculations. Essentially, if the firm had not previously implemented a temporary strategy based on a liability rule, it would require a smaller incentive to transition to a property rule.

Simply put, the model assumes that the firm is already following a certain strategy (liability rule) that optimizes its profits without undertaking a major investment. The conditions developed in the model then help to ascertain the threshold or the specific point at which it becomes more beneficial for the firm to switch to a different strategy (property rule) where such an investment would be needed. If the firm had not already been using a liability-based strategy, the threshold for switching to the property rule would be lower, meaning it would be easier or more advantageous for the firm to make this switch. This perspective is crucial for understanding the firm’s decision-making process regarding operational changes in response to external factors or regulatory environments.

In even simpler terms, Equations (21) and (22) show how a firm would have to decide when to significantly modify how it operates. Before reaching this point, the firm has already taken steps to reduce any negative impact from liabilities by tweaking its costs. However, these adjustments are not enough to ensure that the firm fully meets all regulatory or legal requirements without the threat of sanction and continuous adjustments. The model guides the firm in understanding when further, more substantial changes are necessary—these changes refer to those that go beyond cost adjustments and involve a complete overhaul of operational scale and processes to ensure total compliance with existing rules and standards.

In expressions (21) and (22), we assume, for simplicity, that the same appropriate rate of discount can be applied to the firm and the regulator so that the option parameter is the same for both agents. By solving for , we obtain the critical value at which the firm will exercise the option to switch to the new risk-free technology:

This threshold marks a discontinuity between the attempt to comply (and/or to avoid sanctions) by adopting a liability rule and the decision to switch to a property rule, by undertaking a once-and-for-all investment. It must be noted that, for = 1, i.e., perfect effectiveness of private costs to comply under the liability rule, expression (20) simply becomes the following:

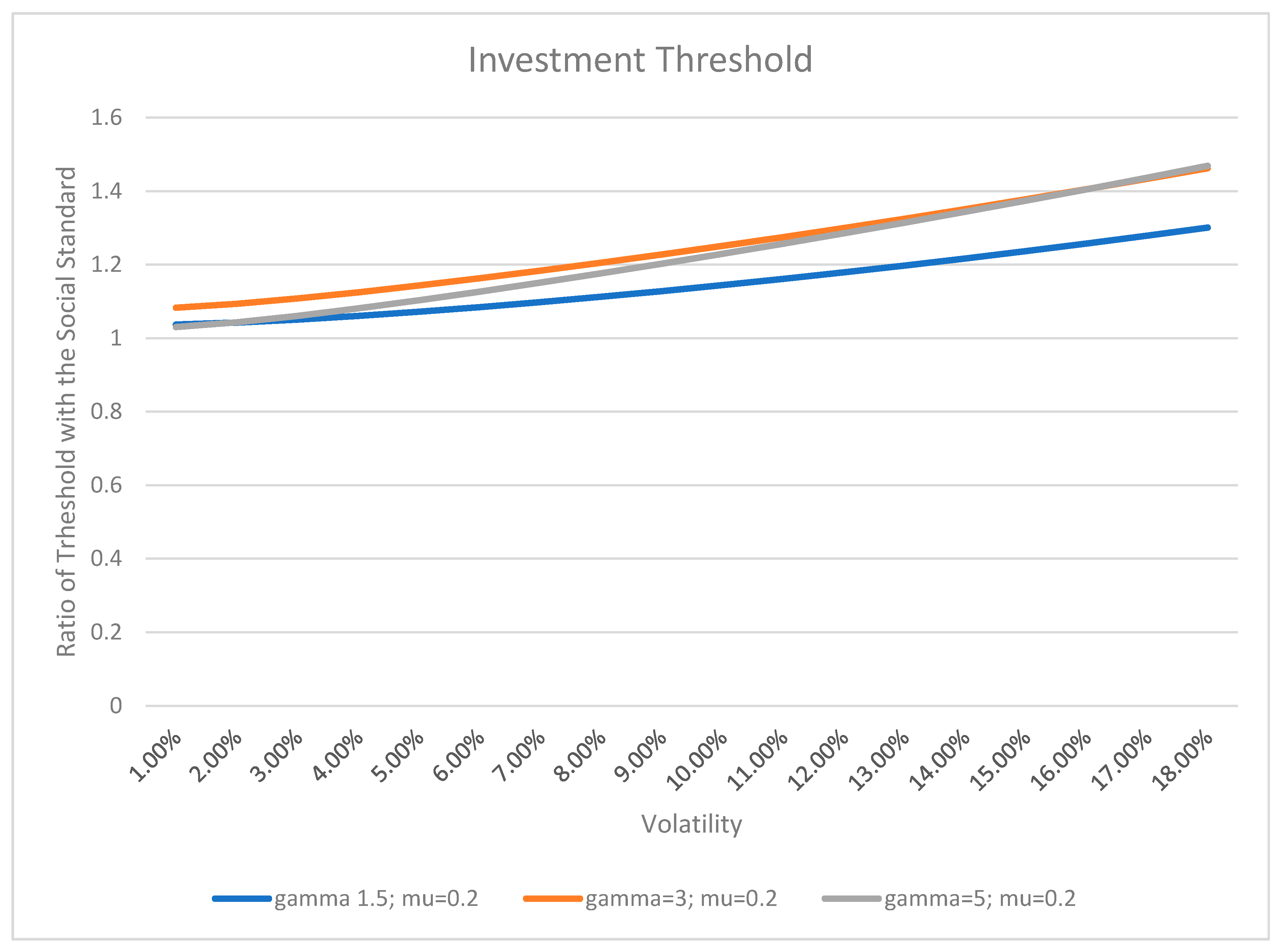

In this case, the sanction threshold (expression (12)) with no private costs and the investment threshold will coincide and will simply be the level of the standard multiplied by the uncertainty factor. In other words, the firm will decide to switch to the property rule regime precisely when the regulator can be expected to apply the sanction. Thus, the threshold at which the representative firm will switch to the minimum risk technology will be higher, where the higher the uncertainty (the lower ), the higher the effectiveness of avoidance costs, and the higher the social standard. A stricter social standard will thus act as an incentive to switch to structural security measures for the private firms, and the lower the uncertainty, the lower the effectiveness of firms’ costs in avoiding the fines ( and the lower the cost of investment to perform the switching.

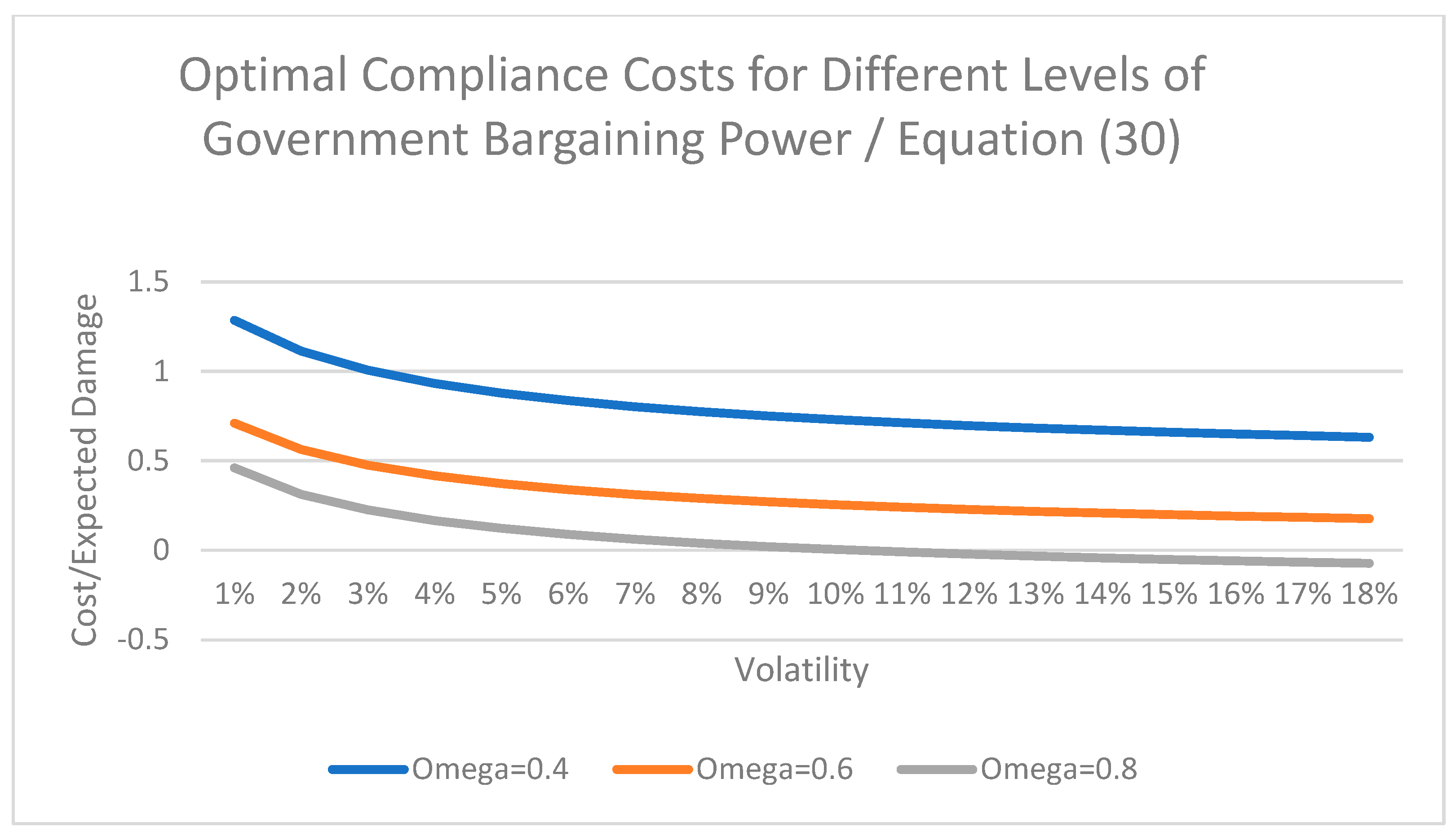

As shown by Figure 3, the threshold at which the firm will be willing to invest tends to increase with uncertainty and with investment costs (as measured by the parameter in expression (19)). At a given level of uncertainty, the firm may be indifferent to the liability and the property rule, but a small reduction of uncertainty may be sufficient to make the investment option more attractive. In other words, the firm will switch from a liability to a property rule if uncertainty is sufficiently low and will do so more willingly when the uncertainty and investment costs are lower.

Importantly, as demonstrated in Figure 1 and Figure 3, the model’s results are characterized by their robustness, particularly in relation to key parameters such as volatility. This robustness implies that the outcomes of the model remain consistent and reliable, even when there are fluctuations or changes in critical factors like market volatility. In other words, the decision point identified by the model for switching operational strategies is not excessively sensitive to changes in these parameters. To explain further, the robustness of the model means that it provides stable and dependable guidance for operational decisions, regardless of the dynamic and often unpredictable nature of factors like market volatility. This stability is crucial for firms operating in environments where such factors can change rapidly and unpredictably. It ensures that the strategic guidance offered by the model remains valid and applicable even as external conditions fluctuate, thereby offering a reliable tool for decision-making in various scenarios.

For the case of the pandemic, these findings imply that measures like social distancing or other methods to curtail virus spread by enforcing norms affecting business earnings will typically lead to two separate scenarios. These scenarios hinge on the proportion of expected damage relative to the social standards. They correspond to either opting for a liability approach or a property strategy in managing risk. In both regimes, business profits will be reduced, with respect to the BAU situation, by a proportion of the expected damage over and above the social standard. In the liability rule regime, however, uncertainty and a lax social standard will conspire to induce imperfect compliance on the part of the firms in the form of pro tempore costs that will include compliance as well as avoidance (elusion or evasion) actions. In this regime, the firm will be passive or engage in actions aimed to neutralize a contingent loss (the liability option), i.e., the risk that infection exceeds the social standard, if the measures imposed are not very costly (the standard is low). This will occur if the level of infection generated does not cross a threshold, which depends on the strictness of the social standard as well as on the costs of a technology that removes the risk of infection from productive activities. Once this barrier is crossed, a complete reorganization of the productive process is in order and the second, more persistent property rule regime may prevail. More generally, the results indicate that a liability rule can be interpreted as a form of exercising the option to wait by the firm, whose willingness to switch to a property rule by undertaking a costly investment will tend to decrease over time as more information is gained and uncertainty is reduced.

6. Endogenizing the Social Standard

Both the government agency and the private firm utilize different methods to exert their influence: the regulator through fines and the firm through costs incurred to avoid these fines. However, the social standard emerges as a common factor, subject to negotiation between these entities. From the society viewpoint, this standard serves as a benchmark to assess damage. It allows for the evaluation of public well-being by measuring the positive discrepancy between the damage inflicted on society (such as loss of life and other social costs due to infection) and the standard itself.

The stringency of this social standard, however, comes with its own trade-offs. Increasing its strictness can lead to higher societal costs, which include lost income opportunities and expenses related to enforcement. The formulation of this concept suggests that the establishment of a social standard can be represented as a decomposition of expected damage:

In (25), the present value of the standard is a maximum tolerance level over which the damage caused by the pandemic becomes of social concern. The introduction of this standard in the measurement of social well-being thus reduces the value of the damage by the same amount. However, by neglecting the damages below its level, it also causes social costs.

This idea is captured in a linearized form in Equation (23):