Quantifying Risk in Investment Decision-Making

by

Jaheera Thasleema Abdul Lathief

1,

Sunitha Chelliah Kumaravel

1,

Regina Velnadar

1,

Ravi Varma Vijayan

2 and

Satyanarayana Parayitam

3,* 1

Department of Commerce Holy Cross College, Manonmaniam Sundaranar University, Tirunelveli 629002, Tamil Nadu, India

2

Government Arts and Science College, Bharathiar University, Coimbatore 641109, Tamil Nadu, India

3

Department of Management and Marketing, Charlton College of Business, University of Massachusetts Dartmouth, Dartmouth, MA 02745, USA

*

Author to whom correspondence should be addressed.

J. Risk Financial Manag. 2024, 17(2), 82; https://doi.org/10.3390/jrfm17020082

Submission received: 15 January 2024

/

Revised: 10 February 2024

/

Accepted: 14 February 2024

/

Published: 18 February 2024

(This article belongs to the Special Issue Inflation Hedging Instruments)

Abstract

:In the wake of inflation, investors engage in identifying inflation hedging instruments. Most importantly, investors attempt to minimize risk and maximize returns to safeguard against inflation. Risk plays an important role in this process. The objective of this research is to examine the relationship between risk factors and investor behavior, particularly in the Indian context. Based on the theory of planned behavior (TPB), we built a conceptual model investigating the intricate relationship between risk factors, investment priority, investment strategy and investment decision-making. We collected data from 537 respondents in the southern region of India and analyzed the data using Partial Least Squares Structural Equation Modeling (PLS-SEM). The result indicate: (i) risk factors (risk capacity, risk tolerance, and risk propensity) are positively related to investment priority and investment strategy, (ii) investment priority is positively related to investment decision-making, (iii) conscientiousness moderates the relationship between investment priority and investment decision-making, (iv) investment strategy is positively related to investment decision-making. Finally, the practical and theoretical implications for research are discussed.

1. Introduction

A significant body of research over the last three decades in behavioral finance investigated the effects of risks on the investment decisions of individuals (Bucciol and Miniaci 2018; Gakhar 2019; Rothman 2017; Streich 2023; Zheng and Prislin 2012). Several studies established that an individual’s investment decision-making process is influenced by their unique characteristics and traits (Chitra and Sreedevi 2011; Galil et al. 2023; Mishra et al. 2010; Young et al. 2012) and how they perceive that investment provides a cushion against inflation (Aimone and Pan 2022; Sanfelici and Magnani 2022).

Making investment decisions is a significant aspect of managing one’s finances, as it balances current requirements and future aspirations. Financial planning can be an extensive and resource-intensive process for individuals and families, requiring careful consideration and analysis of various investment options (Baker et al. 2021; Nadeem et al. 2020). It is also necessary to safeguard against inflation and risky situations (Galil et al. 2023). Researchers in finance have not considered personal and environmental factors that affect investor choices (Sivaramakrishnan et al. 2017; Xiao and Porto 2017). Researchers in psychology, economics, and finance increasingly agreed that investors behave irrationally and do not adhere to rational decision-making processes, which causes them to make tremendous mistakes in their decisions (Dam and Mate 2017). The researchers have shifted their focus from traditional finance, where investors make rational decisions, to claiming that decisions are usually irrational. The basic presumption of behavioral finance researchers is that a sophisticated interplay of psychological elements influences investing decisions. Traditional financial theories hold that investors make rational decisions, whereas behavioral scientists contend that investor behavior is irrational (Tekce and Yılmaz 2015). In order to achieve optimal results in financial development, it is imperative to exercise prudence in allocating resources (Lusardi and Mitchell 2014). Behavioral finance and economics scholars have identified numerous obstacles individuals face when making sound financial decisions (Abreu and Mendes 2012; Li and Yu 2012). The literature on behavioral finance examines various elements that influence an individual’s financial decisions (Aydemir and Aren 2017; Davis and Runyan 2016). Information has dramatically aided the investor’s ability to make informed investment decisions; yet, it has been discovered that perceived risk is more critical than actual risk (Ricciardi 2008). According to several studies, investors exhibit varying behaviors in different situations (Riitsalu and Murakas 2019; Wood and Zaichkowsky 2004). Investors heavily depend on the information at their disposal to make decisions impacting their investments (Kubilay and Bayrakdaroglu 2016). This research aims to find the answers to the following questions.

RQ1: How do various risk factors (risk capacity, risk tolerance, and propensity) influence investment priority and strategy?

RQ2: How does investment priority influence the investment decision-making of individuals?

RQ3: How does investment strategy influence the investment decision-making of individuals?

RQ4: How does conscientiousness moderate the relationship between investment priority and decision-making?

This research makes three significant contributions to the literature on behavioral finance. First, three components of risk, risk propensity, risk tolerance, and risk capacity, are investigated in the context of investors in a developing country, India. This study bridges a gap by connecting three dimensions of risk to investor priority and investor decisions. Second, this research underscores the importance of investment priority and strategy in driving investment decisions. Most importantly, the investor’s preference may involve protecting the investment in light of inflation and securing adequate returns. Though previous researchers have exhaustively studied risk perception, it is intriguing that a substantial amount of work has not been conducted concerning risk and investment decisions, especially in developing countries. Third, this study highlights the importance of conscientiousness, a personality trait, in strengthening the relationship between investment priority and investment decision. This study is the first to consider various risk factors (risk capacity, risk tolerance, and risk propensity) that may influence investment priority and investment strategy. Further, this study emphasizes the significance of conscientious investors in influencing investment decisions.

The Study Context—India

India is the number one populated country in the world, and investors’ behavior is radically different from other countries (Pandit and Yeoh 2014). Indian investors tend to invest in their children’s education, healthcare, and celebrations like marriage. Most of the investors in India plan their investments in favor of real estate and stock market. Some individuals and families tend to invest in gold ornaments (Rajasekar et al. 2022). The risk propensity of investors plays a vital role in the diversification of investments in India (Saivasan and Lokhande 2022). Further, limited financial knowledge and financial inclusion prompt most of the investors to seek financial consultants to make financial decisions (Adil et al. 2023); Recent research reported that Indian stock markets are highly volatile (Rath 2023), thus making investment decisions very difficult for Indian investors.

This paper is organized in a specific manner to ensure clarity and cohesiveness. Firstly, we provide a concise summary of the research that substantiates our hypotheses. Next, we specify variables, hypotheses development, and analysis methods to ensure transparency and accurate interpretation of our results. Finally, we delve into the theoretical and practical implications of our findings, while also acknowledging any limitations in our research and proposing potential avenues for future research.

2. Variables in the Study

2.1. Risk Capacity

Investors evaluate the potential gains and the risks involved in their investments. However, some individuals may be risk-averse, regardless of their ability to withstand potential losses. In contrast, others may actively seek risk, even though they may not have the financial resources to absorb potential losses (Sindhu and Kumar 2014). Risk capacity can be objectively determined based on various factors such as income, age, financial stability, dependents, and other related elements (Roszkowski et al. 2005). Risk capacity measures how much risk a person can tolerate while investing (Rajasekar et al. 2022).

2.2. Risk Tolerance

Investors and financial service providers increasingly need to grasp financial risk tolerance. From the retail investor’s perspective, it facilitates better financial decision-making and prevents frustration. Analysis of a client’s investment risk tolerance increases confidence in one’s decision-making (Hallahan et al. 2003). An investor’s wealth increases his absolute risk tolerance since he can use his money to acquire any knowledge. In contrast, less affluent people remain doubtful because they cannot afford to buy that much information (Makarov and Schornick 2010). Successful prior investments suggest a high-risk tolerance that undoubtedly produces high returns (Chou et al. 2010). Risk tolerance is a subjective measure based on attitudes and beliefs, which can vary among individuals, even within a group sharing similar characteristics, such as age and income. Therefore, individuals with comparable incomes, age, and other factors may exhibit similar risk-taking tendencies (Roszkowski et al. 2005).

2.3. Risk Propensity

An individual’s portfolio allocation of their financial resources is determined by their attitude towards risk-taking (Hallahan et al. 2003). Risk propensity assesses risk-taking in the current situation (Combrink and Lew 2019). Investors willing to buy the stock demonstrate that they are willing to accept risks, which may ultimately impact their ability to make money from investments. To obtain a more significant return from the stock market, people perceive a higher level of risk (ul Abdin et al. 2022). An individual’s inclination towards risk is not a static trait but a dynamic characteristic that various experiences and events can influence. This propensity for risk can ultimately impact the decisions made regarding risk-taking behavior (Hung and Tangpong 2010).

2.4. Investment Priority

In developing nations like India, where there is a high population density and a lack of available land, real estate prices rise with time; many investors prefer real estate over other forms of sustainable investment (Shanmugam et al. 2022a). The subject of investment priority is the prioritized elements of investments. For example, some people invest to pay for their children’s education, weddings, healthcare, or other essentials. They then plan their tactics and select their investment portfolio (Rajasekar et al. 2022).

2.5. Conscientiousness

Conscientiousness is one of the Big Five personality traits (McCrae and Costa 1997) that explains how individuals act with a sense of purpose. Individuals high in conscientiousness tend to be organized, systematic, and responsible in making decisions. They acquire knowledge through various sources before making rational decisions as far as possible. Conscientiousness entails two distinct traits—a strong work ethic and a focus on achieving goals (Caliendo et al. 2014). Conscientious people tend to be competent and obedient (Shanmugam et al. 2022b), with a level of appreciation individuals have for preparation, resilience, and commitment towards achieving goals (Rossberger 2014), reliable, punctual, highly capable, determined, cautious, analytical, methodical, self-disciplined, and generally have specific financial objectives (Pak and Mahmood 2015). Extant research reported that individuals high in conscientiousness effectively manage their finances and avoid financial distress (Fenton-O’Creevy and Furnham 2020; McCrae and Costa 1997; McCrae and Terracciano 2005; Weele 2013).

2.6. Investment Strategy

Individuals must engage in investment strategy to maintain control of their finances, invest surplus funds with discipline, and have the confidence to profit from investments. (Asandimitra et al. 2019). Like a company’s investment strategy, which outlines its long-term investment goals, primary activity paths, risk tolerance, and evaluation procedures, individuals chalk out investment strategies to meet their goals (Kartasova 2013). A study on financial constraints revealed that businesses with more significant financial uncertainty and financial disadvantage are more likely to use a peer investment strategy and rely on other businesses’ decisions (Park et al. 2017). The investor’s short-term and long-term investments comprise their strategy (Rajasekar et al. 2022).

2.7. Investment Decision

An investment decision is an investor’s action to allocate cash among many investment possibilities, including financial and tangible assets (Cheng 2014). While making investment decisions, individuals gather information from various sources: friends, relatives, social media, stock prices, and fluctuations and changes in real estate prices (Sahi et al. 2013). The other factors influencing investment decisions include financial position, ease of borrowing, and average rate of return on investment (Adhikari 2020). Investment decisions play a significant role in the financial function and are the only factor that affects a company’s worth (Hidayat 2010). Individual investors’ previous investments are a strong basis for future decisions (Mak and Ip 2017). Investors may also choose instruments that are readily accessible and convenient, i.e., reasonable returns and retaining value, especially in the wake of inflation.

3. Theoretical Underpinnings and Hypothesis Development

Modern portfolio theory (MPT) (Markowitz 1952) provides a theoretical framework for the present study. According to MPT, investors attempt to maximize return while minimizing risk and select portfolios accordingly. The basic tenet of MPT is that investors are risk-averse and are prepared to take risks only when a higher rate of return compensates them. However, the perception of risk differs between individuals, as some are more risk-averse than others. Though in the perfect market with rational investors, specific risks associated with assets can be reduced by diversification, in real life, investors rely on decisions based on the expected values of assets. Hence, MPT is applicable to this study. Systematic risks (market risks) cannot be diversified, whereas unsystematic risks can be diversified. Thus, investors considering an increasing inflation rate are more likely to select portfolios and choose priorities that will help them compensate for inflation and simultaneously ensure a higher rate of return. Despite criticism, some scholars believe that MPT helps investment strategy by diversifying assets to produce a profitable investment portfolio (Elton and Gruber 1997).

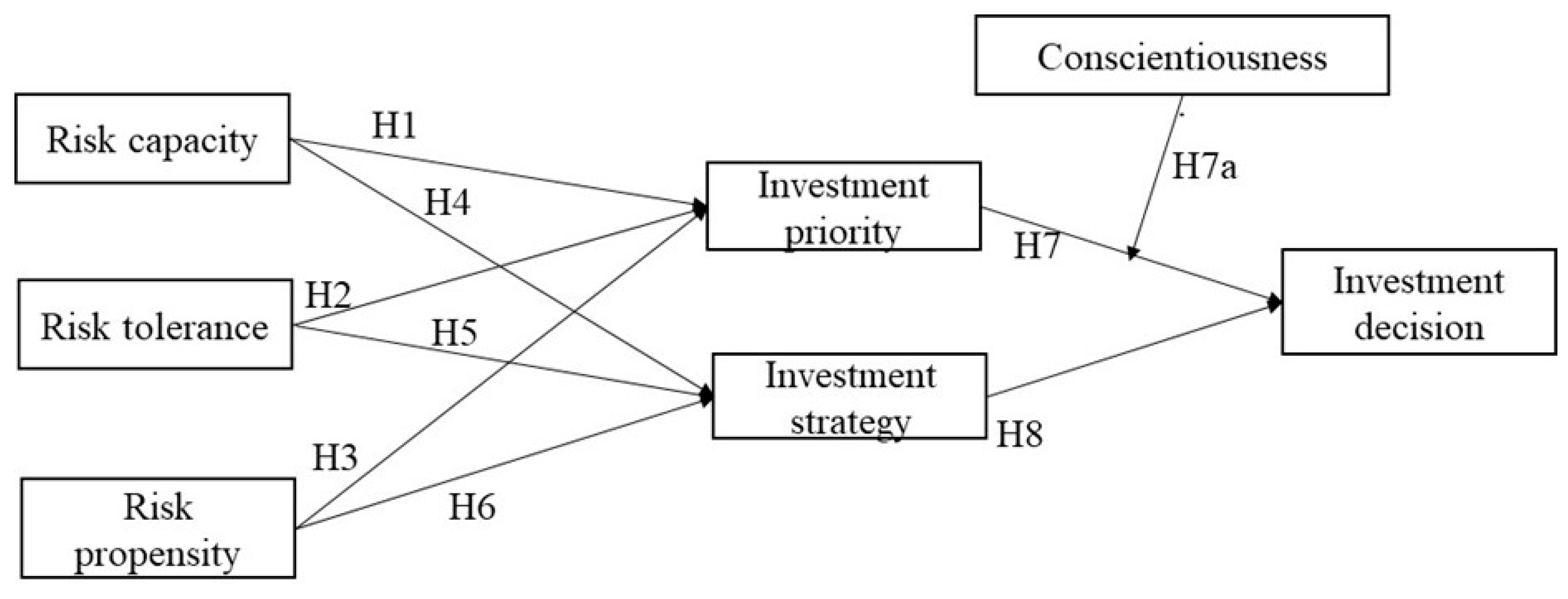

Using MPT, this study examines the impact of three risk factors (risk capacity, risk tolerance, and risk propensity) on investment priority and investment strategy. Second, we explain how investment priority and investment strategy influence the investment decision-making of individuals. The conceptual model is presented in Figure 1.

3.1. Risk Capacity and Investment Priority

The investment behavior of individuals in uncertain conditions is determined by their risk capacity, while their investment priorities shape their approach to investing (De Bortoli et al. 2019). Several studies worldwide have documented the positive association between risk capacity and investment priority, which is one of the critical financial decisions (Alquraan et al. 2016; Baker and Nofsinger 2002; Charness et al. 2013; ul Abdin et al. 2022). Individuals evaluate the risk involved in investment decisions and choose their priorities depending on their risk capacity. In a recently conducted study on Indian investors, the researchers found that personality characteristics influenced both risk capacity and investment priority (Rajasekar et al. 2022). Individuals with high-risk capacity may prioritize their investments in favor of real estate and stock that may provide against inflation. Based on scant and sporadic empirical evidence, we offer the following hypothesis.

H1.

Risk capacity is positively related to investment priority.

3.2. Risk Tolerance and Investment Priority

Risk tolerance is different from risk capacity. Risk capacity is concerned with the ability of individuals to take risks, whereas risk tolerance is their ability to withstand losses when they take risks (Streich 2023). People with high-risk capacity may not have risk tolerance when they lose money in their investments (Corter and Chen 2006; Grable and Roszkowski 2008). Before making investment decisions, people often gather information about the options available to them so that they can choose their priority depending on their risk tolerance. Behavioral finance research indicates that informed investors choose profitable investments and maintain diversified portfolios, leading to higher returns in proportion to their risk tolerance (Sivaramakrishnan et al. 2017). Risk tolerance is the opposite of risk aversion. The uncertainty a person is willing to take while investing is often referred to as financial risk tolerance within the context of financial choices (Bayar et al. 2020; Joo and Grable 2004). Thus, based on the above arguments, we offer the following hypothesis:

H2.

Risk tolerance is positively related to investment priority.

3.3. Risk Propensity and Investment Priority

Risk propensity is a personality attribute of individuals and is related to the extent to which individuals take or avoid risks in making investment decisions (Hung and Tangpong 2010; Sitkin and Pablo 1992). Most of the research in behavioral finance is aimed at explaining the relationship between the risk propensity of individuals and how it affects their choices of making decisions (King and Slovic 2014). Understanding investors’ risk propensity is essential for making effective investment decisions (Combrink and Lew 2019). In a recent study conducted on 315 respondents from India, researchers found that risk propensity significantly influenced diversification and investment priority (Saivasan and Lokhande 2022). Earlier scholars reported similar results when they surveyed 256 respondents from the Tunisian stock market (Mouna and Jarboui 2015). Thus, we offer the following hypothesis based on available empirical evidence and logical explanations.

H3.

Risk propensity is positively related to investment priority.

3.4. Risk Capacity and Investment Strategy

Individuals with a greater capacity for risk are more inclined to opt for investment strategies that involve higher levels of risk compared to those with lower risk capacities (Rajasekar et al. 2022), and make investments based on their level of risk capacity (Millroth et al. 2020). Most of the financial decisions are related to risk perception, which includes risk capacity and risk tolerance. The risk capacity determines the extent to which an individual can take risks without adversely affecting the outcomes of taking risks. Investment strategy is primarily determined by the risk capacity of individuals, which depends on their income, assets, and financial position about their assets and liabilities. If the risk capacity is low and investors engage in risky investment decisions, it may exacerbate their financial situation. On the contrary, individuals with a high capacity to take risks devise investment strategies by considering alternatives (Noussair et al. 2014). Based on the above arguments, we propose the following hypothesis:

H4.

Risk capacity is positively related to investment strategy.

3.5. Risk Tolerance and Investment Strategy

Risk tolerance positively correlates with past investment behavior, influencing investment decisions (Chou et al. 2010). Investment experience is a key predictor, with more seasoned investors displaying risk-tolerant attitudes and riskier investment strategies (Corter and Chen 2006). In investing, it is crucial to have a comprehensive comprehension of an investor’s risk tolerance. This knowledge can help prevent impulsive and ill-informed decisions from harming an individual’s investment decisions (Combrink and Lew 2019). In a recently conducted study on respondents from China, researchers found a positive association between risk tolerance and investment strategy depending on various levels: aggressive, moderate, and conservative (Liu et al. 2022). Studies conducted among investors in India revealed that risk tolerance depends on a variety of factors: materialism, age, and ratio of earnings to total family earnings (Mishra and Mishra 2016; Purkayastha 2008). We offer the following exploratory hypothesis based on scant research investigating the relationship between risk tolerance and specific investment strategies.

H5.

Risk tolerance is positively related to investment strategy.

3.6. Risk Propensity and Investment Strategy

An individual’s inclination towards risk-taking is not constant but somewhat varies depending on their experiences (Bayar et al. 2020). The decisions they make when faced with risky situations are influenced by their past experiences, which shape their risk propensity (Hung and Tangpong 2010). Individuals use various investment strategies, such as relying on brokers or peers and information from the media (Rajasekar et al. 2022). In a recent study conducted on 450 respondents from Pakistan, researchers found that risk propensity and perception are significant determining factors of their investment strategies (Ahmed et al. 2022). Several studies found that individuals may be willing to invest in stock because of the risk propensity, which may result in losses sometimes (Alquraan et al. 2016; Aduda et al. 2012; Chou et al. 2021). Based on the above arguments, we offer the following hypothesis.

H6.

Risk propensity is positively related to investment strategy.

3.7. Investment Priority, Investment Strategy, and Investment Decision

Investment priority may differ from one individual to the other depending on their short-term and long-term goals. Some individuals may prefer to invest in real estate to offset inflation and secure the safety of their investment and high return, especially in developing countries like India. On the other hand, some individuals may exhibit their priorities in investing in their children’s education (Shanmugam et al. 2022b). Obtaining information from publicly available sources can alter their perception of risk, potentially influencing their investment priorities and attitudes during the decision-making process (De Bortoli et al. 2019). Their prior experiences can influence investment priority. For instance, an experienced investor is more likely to opt for a riskier portfolio, since they have learned how to handle it effectively through their past experiences (Chou et al. 2010).

How individuals seek information from various sources plays a vital role in investment decisions. They may obtain information through television, financial advisers, and investment analysis software, and then weigh the pros and cons of investments before making final decisions (ul Abdin et al. 2022; Bayar et al. 2020; Mouna and Jarboui 2015; Saivasan and Lokhande 2022). Thus, we offer the following exploratory hypotheses based on scattered research on the relationship between investment priority, strategy, and investment decisions.

H7.

Investment priority is positively and significantly related to investment decision.

H8.

Investment strategy is positively and significantly related to investment decision.

3.8. Conscientiousness as a Moderator

Conscientiousness traits are positively correlated with short-term investment (Mayfield et al. 2008). Some researchers suggest that individuals with high levels of conscientiousness often exhibit overconfidence in their investment decisions compared to others (Jamshidinavid and Amiri 2012). Past studies have shown that investor’s characteristics primarily influence their investment decisions (Corter and Chen 2006; Crysel et al. 2013; Grable 2000; Hunter and Kemp 2004; Young et al. 2012). However, researchers have yet to explore the moderating impact of conscientiousness in influencing the relationship between investment priority and investment decisions. We argue that conscientiousness, an important Big-Five personality characteristic (McCrae and Costa 2008), may influence individuals’ investment decision-making. It will be interesting to delve into how conscientiousness changes the strength of the relationship between investment priority and investment decision-making, especially given countering inflation. Based on the above arguments, we offer the following exploratory moderation hypothesis.

H7a.

Conscientiousness moderates the relationship between investment priority and investment decision-making such that the relationship between investment priority and investment decision-making becomes stronger (weaker) when the risk tolerance is higher (lower).

4. Method

4.1. Sample

In this study, a convenience nonrandom sampling approach was employed, and 550 questionnaires were distributed to various investors in Kanniyakumari district. Since there is no fixed list of investors, we used non-probability-based convenience sampling to collect data. The high response rate, with 543 questionnaires returned, reflects the engagement of the target population. Following a meticulous data cleaning process that involved the exclusion of six unfilled questionnaires, the final dataset for empirical analysis comprised 537 questionnaire responses. Comrey and Lee (1992) classified a sample size of over 500 as “very good” (100 is poor, 200 is acceptable, 300 is good, and 1000 or more is excellent). We tested the non-response bias by comparing the first fifty respondents with the last fifty respondents and found no statistical difference between these two groups.

4.2. Demographics

The demographic profiles of the respondents were displayed in Table 1.

4.3. Measures

The study utilized previously developed scales to measure all the variables. To measure the constructs, we used a Likert-type 5-point scale ranging from 1 (strongly disagree) to 5 (strongly agree).

Risk capacity was measured using ten items adopted from (Rajasekar et al. 2022), and Cronbach’s alpha reliability value was 0.93. Risk tolerance was measured using five items adopted from (Joo and Grable 2004), and Cronbach’s alpha reliability value was 0.84. Risk propensity was measured using six items adopted from (Bucciol and Miniaci 2018), and Cronbach’s alpha reliability value was 0.86. Investment priority was measured using eight items, the investment strategy using ten items adopted from (Rajasekar et al. 2022), and Cronbach’s alpha reliability values were 0.92. Conscientiousness was measured using five items adopted from (Rajasekar et al. 2022), and Cronbach’s alpha reliability value was 0.93. Investment decision was measured using four items adapted from (Sahi et al. 2013), and Cronbach’s alpha reliability value was 0.85.

5. Analysis and Results

5.1. Measurement Model

We followed a two-step process recommended by Anderson and Gerbing (1988) by checking the measurement model first before testing the structural model. We evaluated the measurement model using Confirmatory Factor Analysis (CFA) to assess its construct’s properties. The factor loadings of the indicators were over 0.7 and the Cronbach’s alpha values for all the variables were above 0.7, indicating that they are reliable (Hair et al. 2019). The results of CFA are presented in Table 2.

5.2. Descriptive Statistics, Discriminant Validity, and Reliability

The average variance extracted (AVE) estimations in this study were higher than the recommended limit of 0.50, which means that their square roots were higher than 0.70. The requirement for discriminant validity was thus met (Fornell and Larcker 1981). The square root of AVE estimation for the variables was higher than the correlations, as shown in Table 3.

For instance, the square root of AVE estimates for risk tolerance and risk propensity were 0.78 and 0.76, respectively, and the correlation between these variables was 0.66. Furthermore, the square root of the AVE estimates for investment priority and investment strategy were 0.81 and 0.78, respectively. The correlation between investment priority and investment strategy was 0.77.

Using the Heterotrait-Monotrait (HTMT) method, we carried out another check to evaluate the discriminant validity, which is mentioned in Table 4. The correlation values for all the constructs were less than 0.9, thus providing additional evidence for the discriminant validity.

5.3. Multicollinearity and Common Method Bias

We checked the inner and outer VIF values, which are mentioned in Table 5 and Table 6. We found that they were both less than 5, and multicollinearity is not an issue with the data (Hair et al. 2019).

Since survey-based data are prone to having common method bias (CMB), it is necessary to test for CMB. We checked CMB in two ways. First, we conducted traditional Harman’s single-factor analysis and found that a single factor accounted for 28.75% of variance, and hence, CMB was not a problem with the data. Second, we followed the latent variable method by subjecting all the indicators to one construct at a time and found that the inner VIF values were than 3.3, suggesting that the data was not infected with CMB (Kock 2015).

5.4. Hypotheses Testing

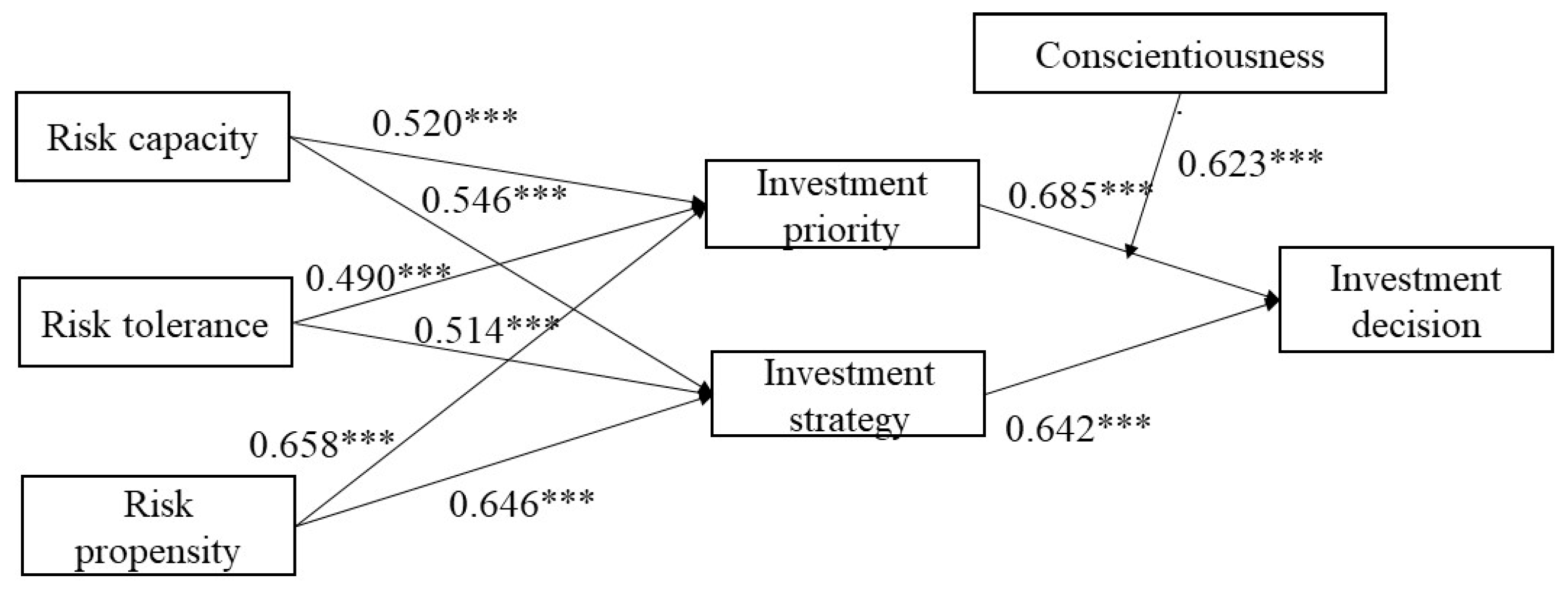

After checking the discriminant validity and reliability and multicollinearity, we tested the hypotheses. The results of testing the hypotheses are mentioned in Table 7.

The results reveal that the regression coefficients of risk capacity (β = 0.520; p < 0.001), risk tolerance (β = 0.490; p < 0.001), and risk propensity (β = 0.658; p < 0.001) on investment priority were positive and significant, thus supporting H1–H3.

The regression coefficients of risk capacity (β = 0.546; p < 0.001), risk tolerance (β = 0.514; p < 0.001), and risk propensity (β = 0.646; p < 0.001) on investment strategy were positive and significant, thus supporting H4–H6.

The regression coefficients of investment priority (β = 0.623; p < 0.001) and investment strategy (β = 0.642; p < 0.001) on investment decision were positive and significant, thus supporting H7 and H8.

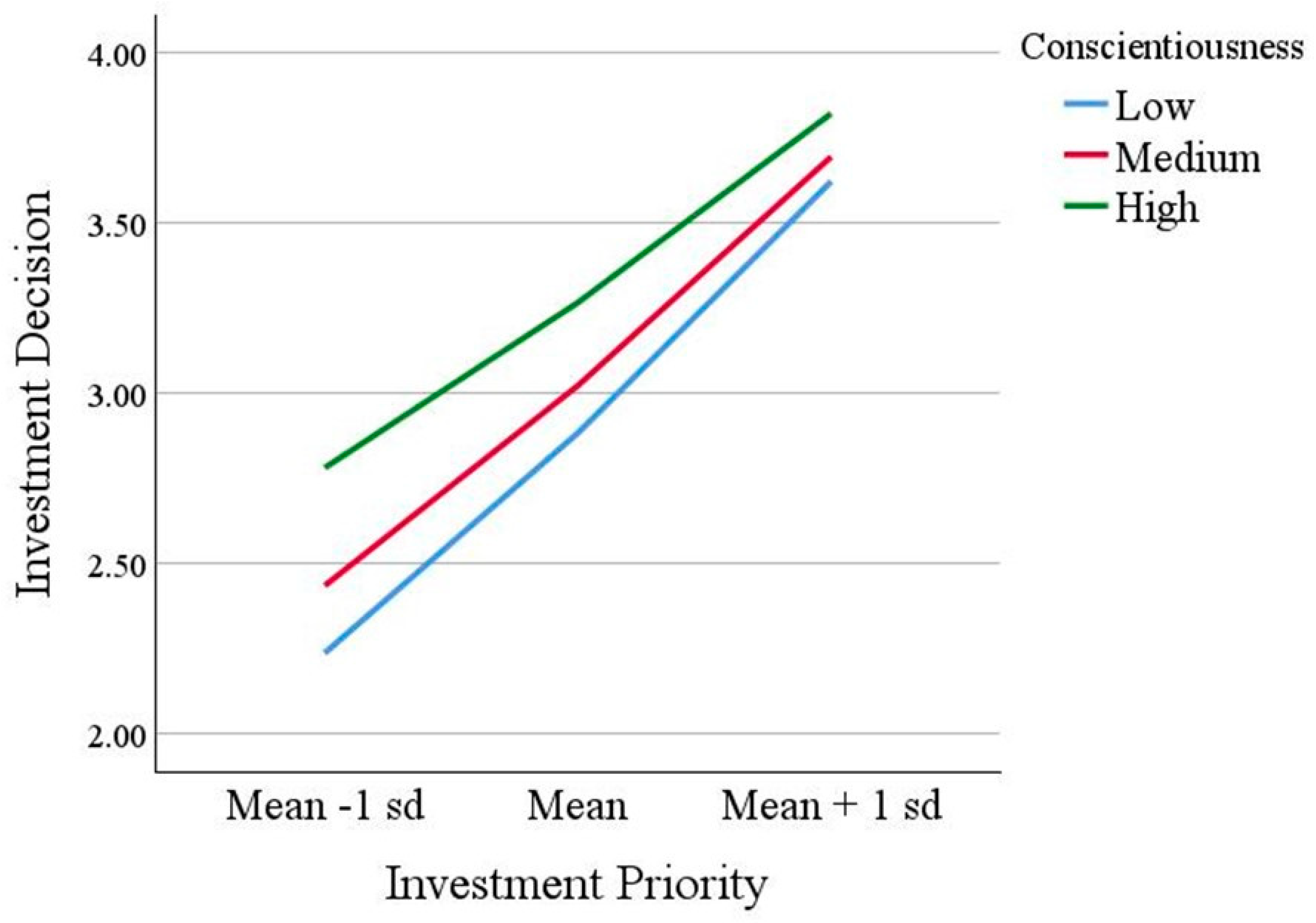

5.5. Testing Moderation Hypothesis (H7a)

The moderating effect of conscientiousness between investment priority and investment strategy reveal a significant interaction term (β investment priority × conscientiousness = 0.623; p < 0.001), thus supporting H7a. The conditional effect of the focal predictor (Conscientiousness) at values of the moderator are presented in Table 8.

The visual representation of the moderator interaction is presented in Figure 2.

Figure 2 shows that at higher levels of conscientiousness, investment priority results in higher levels of investment decision-making than at lower levels of conscientiousness. Furthermore, when investment priority increases from low to high, lower level of conscientiousness were associated with a steep reduction in investment decision-making, whereas at higher levels of conscientiousness, the decrease in investment decision-making was not high. The slopes of the curves indicating “high”, “medium”, and “low” levels of conscientiousness render support to the moderating hypothesis (H7a).

The empirical model is presented in Figure 3.

6. Discussion

This study is to examine how risk factors influence investments among various individuals. We created a conceptual model and investigated the connections between risk factors (risk capacity, risk tolerance, and risk propensity), investment priority, investment strategy, and investment decision-making. To our knowledge, this is the first model in the Indian context. After assessing the instrument’s reliability, we tested the hypotheses, and the moderator relationship was evaluated using Hayes’ (2018) process macros. We found support for each of the eight hypotheses and compared our results with the existing literature to validate our findings.

First, the findings indicate that risk capacity was positively and significantly related to investment priority (Hypothesis 1), which corroborates findings from the literature (Alquraan et al. 2016; Baker and Nofsinger 2002; Charness et al. 2013; ul Abdin et al. 2022). It is expected that the greater the risk capacity, the greater the investment priority. Second, the results support the positive relationship between risk tolerance and investment priority (Hypothesis 2), concurring with findings from the literature (Bayar et al. 2020; Sivaramakrishnan et al. 2017). Third, the positive impact of risk propensity on investment priority (Hypothesis 3) is found to support this research; the finding is consistent with results from the earlier researchers (Combrink and Lew 2019; Sitkin and Pablo 1992; Saivasan and Lokhande 2022).

A fourth key finding is the support for a positive association of risk capacity with investment strategy (Hypothesis 4), corroborating some studies conducted by previous scholars (Noussair et al. 2014; Rajasekar et al. 2022). Fifth, risk tolerance is a significant predictor of investment strategy (Hypothesis 5), which is supported in this research. Though the research investigating this relationship is sparse, available evidence aligns with the findings (Chou et al. 2010; Combrink and Lew 2019; Liu et al. 2022). Sixth, the positive relationship between risk propensity and investment strategy (Hypothesis 6) has been validated in this study. The survey conducted on investors from the Nairobi stock market (Aduda et al. 2012) and the Saudi stock market (Alquraan et al. 2016) provided support in addition to other studies (Chou et al. 2021). Seventh, this study also found that investment priority and investment strategy were positively and significantly related to investment decision-making (Hypotheses 7 and 8); these findings align with the results of previous researchers (Bayar et al. 2020; Hidayat 2010; Mouna and Jarboui 2015; Park et al. 2017; Shanmugam et al. 2022b; ul Abdin et al. 2022; Saivasan and Lokhande 2022).

The eighth key finding is conscientiousness as a moderator in the relationship between investment priority and investment decision-making (Hypothesis 7a). Though previous scholars did not investigate the moderating effect, some empirical evidence supports direct relationships (Corter and Chen 2006; Crysel et al. 2013; Hunter and Kemp 2004; Young et al. 2012). Thus, this study provided overall support for all of the hypotheses consistent with results from previous studies (De Bortoli et al. 2019; Corter and Chen 2006; Sindhu and Kumar 2014).

6.1. Theoretical Implications

A conceptual model was developed for exploring the relationship between risk factors (risk capacity, risk tolerance, and risk propensity) and investment decision-making of individuals, especially in the context of a developing country, India. Investors consider that, in addition to securing reasonable returns on their investments, they are likely to consider how the investment secures them against inflation. As a measure to hedge against inflation, investors engage in strategies to diversify their portfolios. This research makes significant contributions to the investment literature. First, this research advances the MPT theoretical framework to explain the relationship between various risk factors: risk capacity, risk tolerance, risk propensity, and investment decision. Second, it adds to the body of knowledge on investor behavior by defining investment priority and investment strategy as antecedents to investment decision-making; it advances the earlier literature on investor behavior and provides new opportunities for increasing investment returns to safeguard against inflation. Though previous studies dwell on the risk–return relationship, the relationship between investment priority and investment strategy resulting in investment decisions needs to be studied more, making a significant contribution.

The third pivotal contribution of this research is the moderating role of conscientiousness in influencing the individual’s investment priority towards investment decision-making. The study found that conscientiousness directly influences investment priority and has a multiplicative effect when combined with investment priority. This finding is fascinating and sheds light on the importance of conscientiousness in investment decision-making. Several studies have been conducted in India but have not explored the relationship between risk variables, investment priority, investment strategy, and investment decision-making. Therefore, this study contributes a unique perspective to the expanding field of behavioral finance.

6.2. Practical Implications

The findings of this study have implications for individual investors. First, an individual has to conduct a comprehensive financial assessment to determine their investments. Second, our study suggests having an adequate emergency fund to cover unforeseen expenses, which can increase risk capacity by reducing the need to liquidate investments in emergencies. Third, this study underscores the importance of seeking advice from financial professionals, especially for complex investment decisions. Their expertise can help individuals to navigate the investment landscape effectively. Fourth, our study suggests implementing risk management techniques, such as setting stop-loss orders, diversifying holdings, and using appropriate hedging strategies. Fifth, the study vouches for the importance of gathering continuous information about investment strategies, risk management, and financial markets. This knowledge can empower individuals to make more informed investment decisions. Thus, the present study recommends that individual investors choose investment portfolios depending on future investment goals.

6.3. Limitations and Future Research

It is important to note limitations when interpreting the study’s conclusions. First, the small sample size may make it difficult to generalize the findings. However, if the sample is representative of the entire population, then it can be assumed that the results apply to everyone. Second, this study used convenience sampling, which could be better than a probability-based sampling technique. However, the researchers implemented a risk-taking behavior sampling technique that aligns with the study’s criteria (Rajasekar et al. 2022). Therefore, the study sample can still be considered capable of representing the target population. Third, we gathered information from individual investors. We were unable to choose our sample from among stock market investors. This research could yield more beneficial outcomes for stock market investors, if possible.

This study suggests several avenues for further investigation. Firstly, individuals may exhibit five distinct personality traits; each trait could affect their investment choices. This study used only one personality trait (conscientiousness), and future studies may involve other traits to see if they influence investment decisions. In other words, it would be valuable to explore the relationship between each trait and investment decisions in greater depth in order to gain a deeper understanding of their nature. Second, future researchers could conduct longitudinal studies to examine how risk capacity, risk tolerance, and risk propensity change over time in response to life events, market experiences, and individual development. This can help understand the evolution of an individual’s risk profile and its impact on investment decisions. Third, future studies may investigate how cultural factors influence risk perception and risk-taking behavior. Comparative studies can shed light on cultural variations in risk capacity, tolerance, and propensity, and their influence on investment decision-making. Fourth, a more significant sample across different parts of the country will make the conceptual model more generalizable. Fifth, it will be interesting to conduct studies on investor behavior in different developing countries and see if there are cultural differences in individuals’ investment priorities and decisions.

6.4. Conclusions

This study aimed to enhance our understanding of how various risk factors affect investment decisions, explicitly focusing on India as a developing country. The findings of this study suggest that having a sound investment strategy and identifying one’s investment priorities are critical to making informed financial decisions. This study highlighted the importance of considering an individual’s investment priorities and level of conscientiousness when making investment decisions. Risk in investment decision-making is a complex but necessary process that empowers individuals and organizations to navigate financial markets with prudence and confidence. By understanding and integrating risk capacity, tolerance, propensity, and the behavioral aspects of risk perception, investors can create tailored strategies that maximize the potential for financial success while managing and mitigating risk effectively. Such strategies help investors engage in inflation-hedging investment decisions to mitigate the ill effects of inflation and protect them from incurring losses.

Author Contributions

Conceptualization, J.T.A.L., S.C.K. and R.V.; methodology, S.C.K. and S.P.; software, S.C.K., R.V.V. and S.P.; validation, J.T.A.L., S.C.K. and R.V.; formal analysis, J.T.A.L. and S.P.; investigation, S.C.K. and R.V.; resources, J.T.A.L. and S.C.K.; data curation, J.T.A.L., R.V.V. and S.P.; writing—original draft preparation, J.T.A.L., S.C.K. and S.P.; writing—review and editing, S.C.K., R.V.V. and S.P.; visualization, J.T.A.L.; supervision, S.C.K.; project administration, J.T.A.L. and S.C.K. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Data Availability Statement

We make the data available on request.

Conflicts of Interest

The authors declare no conflicts of interest.

References

- Abreu, Margarida, and Victor Mendes. 2012. Information, overconfidence and trading: Do the sources of information matter? Journal of Economic Psychology 33: 868–81. [Google Scholar] [CrossRef]

- Adhikari, Prem Lal. 2020. Factors influencing investment decisions of individual investors at Nepal stock exchange. Management Dynamics 23: 183–98. [Google Scholar] [CrossRef]

- Adil, Mohd, Yogita Singh, Mohammad Subhan, Mamdouh Abdulaziz Saleh Al-Faryan, and Mohd Shamim Ansari. 2023. Do trust in financial institution and financial literacy enhances intention to participate in stock market among Indian investors during COVID-19 pandemic? Cogent Economics & Finance 11: 2169998. [Google Scholar] [CrossRef]

- Aduda, Josiah, Eric Oduor Odera, and Mactosh Onwonga. 2012. The behaviour and financial performance of individual investors in the trading shares of companies listed at the Nairobi stock exchange, Kenya. Journal of Finance and Investment Analysis 1: 33–60. [Google Scholar]

- Ahmed, Zeeshan, Shahid Rasool, Qasim Saleem, Mubashir Ali Khan, and Shamsa Kanwal. 2022. Mediating role of risk perception between behavioral biases and investor’s investment decisions. Sage Open 12: 21582440221097394. [Google Scholar] [CrossRef]

- Aimone, Jason A., and Xiaofei Pan. 2022. My Risk, Your Risk, and Our Risk: Costly Deviation in Delegated Risk-Taking Environments. Journal of Behavioral Finance 23: 371–87. [Google Scholar] [CrossRef]

- Alquraan, Talal, Ahmad Alqisie, and Amjad Al Shorafa. 2016. Do behavioral finance factors influence stock investment decisions of individual investors? (Evidences from Saudi Stock Market). American International Journal of Contemporary Research 6: 159–69. [Google Scholar]

- Anderson, James C., and David W. Gerbing. 1988. Structural equation modeling in practice: A review and recommended two-step approach. Psychological Bulletin 103: 411–23. [Google Scholar] [CrossRef]

- Asandimitra, Nadia, Tony Seno Aji, and Achmad Kautsar. 2019. Financial behavior of working women in investment decision-making. Information Management and Business Review 11: 10–20. [Google Scholar] [CrossRef]

- Aydemir, Sibel Dinç, and Selim Aren. 2017. Do the effects of individual factors on financial risk-taking behavior diversify with financial literacy? Kybernetes 46: 1706–34. [Google Scholar] [CrossRef]

- Baker, H. Kent, and John R. Nofsinger. 2002. Psychological biases of investors. Financial Services Review 11: 97–116. [Google Scholar]

- Baker, H. Kent, Satish Kumar, and Nisha Goyal. 2021. Personality traits and investor sentiment. Review of Behavioral Finance 13: 354–69. [Google Scholar] [CrossRef]

- Bayar, Yılmaz, H. Funda Sezgin, Omer Faruk Ozturk, and Mahmut Unsal Şaşmaz. 2020. Financial literacy and financial risk tolerance of individual investors: Multinomial logistic regression approach. Sage Open 10: 2158244020945717. [Google Scholar] [CrossRef]

- Bucciol, Alessandro, and Raffaele Miniaci. 2018. Financial risk propensity, business cycles and perceived risk exposure. Oxford Bulletin of Economics and Statistics 80: 160–83. [Google Scholar] [CrossRef]

- Caliendo, Marco, Frank Fossen, and Alexander S. Kritikos. 2014. Personality characteristics and the decisions to become and stay self-employed. Small Business Economics 42: 787–814. [Google Scholar] [CrossRef]

- Charness, Gary, Uri Gneezy, and Alex Imas. 2013. Experimental methods: Eliciting risk preferences. Journal of Economic Behavior & Organization 87: 43–51. [Google Scholar]

- Cheng, Philip Y. K. 2014. Decision utility and anticipated discrete emotions: An investment decision model. Journal of Behavioral Finance 15: 99–108. [Google Scholar] [CrossRef]

- Chitra, K., and V. Ramya Sreedevi. 2011. Does personality traits influence the choice of investment? IUP Journal of Behavioral Finance 8: 47. [Google Scholar]

- Chou, Hsin-I., Mingyi Li, Xiangkang Yin, and Jing Zhao. 2021. Overconfident institutions and their self-attribution bias: Evidence from earnings announcements. Journal of Financial and Quantitative Analysis 56: 1738–70. [Google Scholar] [CrossRef]

- Chou, Shyan-Rong, Gow-Liang Huang, and Hui-Lin Hsu. 2010. Investor attitudes and behavior towards inherent risk and potential returns in financial products. International Research Journal of Finance and Economics 44: 16–30. [Google Scholar]

- Combrink, Sean, and Charlene Lew. 2019. Potential underdog bias, overconfidence and risk propensity in investor decision-making behavior. Journal of Behavioral Finance 21: 337–51. [Google Scholar] [CrossRef]

- Comrey, Andrew L., and Howard B. Lee. 1992. A First Course in Factor Analysis, 2nd ed. Hillsdale: Lawrence Erlbaum. [Google Scholar] [CrossRef]

- Corter, James E., and Yuh-Jia Chen. 2006. Do investment risk tolerance attitudes predict portfolio risk? Journal of Business and Psychology 20: 369–81. [Google Scholar] [CrossRef]

- Crysel, Laura C., Benjamin S. Crosier, and Gregory D. Webster. 2013. The Dark Triad and risk behavior. Personality and Individual Differences 54: 35–40. [Google Scholar] [CrossRef]

- Dam, Leena, and Rashmi Makrand Mate. 2017. Role of an attitude and financial literacy in stock market participation. International Journal of Management, IT and Engineering 7: 137–49. [Google Scholar]

- Davis, Kimberlee, and Rodney C. Runyan. 2016. Personality traits and financial satisfaction: Investigation of a hierarchical approach. Journal of Financial Counseling and Planning 27: 47–60. [Google Scholar] [CrossRef]

- De Bortoli, Daiane, Newton da Costa Jr., Marco Goulart, and Jessica Campara. 2019. Personality traits and investor profile analysis: A behavioral finance study. PLoS ONE 14: e0214062. [Google Scholar] [CrossRef]

- Elton, Edwin J., and Martin J. Gruber. 1997. Modern portfolio theory, 1950 to date. Journal of Banking & Finance 21: 1743–59. [Google Scholar]

- Fenton-O’Creevy, Mark, and Adrian Furnham. 2020. Personality, ideology, and money attitudes as correlates of financial literacy and competence. Financial Planning Review 3: e1070. [Google Scholar] [CrossRef]

- Fornell, Claes, and David F. Larcker. 1981. Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research 18: 39–50. [Google Scholar] [CrossRef]

- Gakhar, Divya. 2019. Role of Optimism Bias and Risk Attitude on Investment Behaviour. Theoretical Economics Letters 9: 91776. [Google Scholar] [CrossRef]

- Galil, Koresh, Avia Spivak, and Aviad Tur-Sinai. 2023. Socioeconomic status and individual investors’ behavior during a financial crisis. Journal of Behavioral and Experimental Finance 40: 100855. [Google Scholar] [CrossRef]

- Grable, John E. 2000. Financial risk tolerance and additional factors that affect risk taking in everyday money matters. Journal of Business and Psychology 14: 625–30. [Google Scholar] [CrossRef]

- Grable, John E., and Michael J. Roszkowski. 2008. The influence of mood on the willingness to take financial risks. Journal of Risk Research 11: 905–23. [Google Scholar] [CrossRef]

- Hair, Joseph F., William C. Black, Barry J. Babin, and Rolph E. Anderson. 2019. Multivariate Data Analysis, 8th ed. London: Cengage Learning. [Google Scholar]

- Hallahan, Terrence, Robert Faff, and Michael McKenzie. 2003. An exploratory investigation of the relation between risk tolerance scores and demographic characteristics. Journal of Multinational Financial Management 13: 483–502. [Google Scholar] [CrossRef]

- Hayes, Andrew F. 2018. Introduction to Mediation, Moderation, and Conditional Process Analysis: A Regression-Based Approach. New York: The Guilford Press. [Google Scholar]

- Hidayat, Riskin. 2010. Keputusan investasi dan financial constraints: Studi empiris pada bursa efek Indonesia. Buletin Ekonomi Moneter dan Perbankan 12: 457–79. [Google Scholar] [CrossRef]

- Hung, Kuo-Ting, and Chanchai Tangpong. 2010. General risk propensity in multifaceted business decisions: Scale development. Journal of Managerial Issues 22: 88–106. [Google Scholar]

- Hunter, Katrina, and Simon Kemp. 2004. The personality of e-commerce investors. Journal of Economic Psychology 25: 529–37. [Google Scholar] [CrossRef]

- Jamshidinavid, Babak, and Shahla Amiri. 2012. The Impact of Demographic and Psychological Characteristics on the Investment Prejudices in Tehran Stock. European Journal of Business and Social Sciences 1: 41–53. [Google Scholar]

- Joo, So-Hyun, and John E. Grable. 2004. An exploratory framework of the determinants of financial satisfaction. Journal of Family and Economic Issues 25: 25–50. [Google Scholar] [CrossRef]

- Kartasova, Jekaterina. 2013. Factors forming irrational Lithuanian individual investors’ behaviour. Journal of Business Economics and Management 3: 69–78. [Google Scholar]

- King, Jesse, and Paul Slovic. 2014. The affect heuristic in early judgments of product innovations. Journal of Consumer Behaviour 13: 411–28. [Google Scholar] [CrossRef]

- Kock, Ned. 2015. Common method bias in PLS-SEM: A full collinearity assessment approach. International Journal of e-Collaboration 11: 1–10. [Google Scholar] [CrossRef]

- Kubilay, Bilgehan, and Ali Bayrakdaroglu. 2016. An empirical research on investor biases in financial decision-making, financial risk tolerance and financial personality. International Journal of Financial Research 7: 171–82. [Google Scholar] [CrossRef]

- Li, Jun, and Jianfeng Yu. 2012. Investor attention, psychological anchors, and stock return predictability. Journal of Financial Economics 104: 401–19. [Google Scholar] [CrossRef]

- Liu, Jianxu, Yangnan Cheng, Xiaoqing Li, and Songsak Sriboonchitta. 2022. The role of risk forecast and risk tolerance in portfolio management: A case study of the Chinese financial sector. Axioms 11: 134. [Google Scholar] [CrossRef]

- Lusardi, Annamaria, and Olivia S. Mitchell. 2014. The economic importance of financial literacy: Theory and evidence. American Economic Journal: Journal of Economic Literature 52: 5–44. [Google Scholar] [CrossRef]

- Mak, Mark K. Y., and Wao-Han Ip. 2017. An exploratory study of investment behaviour of investors. International Journal of Engineering Business Management 9: 1–12. [Google Scholar] [CrossRef]

- Makarov, Dmitry, and Astrid V. Schornick. 2010. Explaining Households’ Investment Behavior. INSEAD Working Papers Collection 44: 1–23. [Google Scholar] [CrossRef]

- Markowitz, Harry. 1952. Portfolio Selection. The Journal of Finance 7: 77–91. [Google Scholar] [CrossRef]

- Mayfield, Cliff, Grady Perdue, and Kevin Wooten. 2008. Investment management and personality type. Financial Services Review 17: 219–36. [Google Scholar]

- McCrae, Robert R., and Antonio Terracciano. 2005. Universal features of personality traits from the observer’s perspective: Data from 50 cultures. Journal of Personality and Social Psychology 88: 547. [Google Scholar] [CrossRef] [PubMed]

- McCrae, Robert R., and Paul T. Costa Jr. 1997. Personality trait structure as a human universal. American Psychology 52: 509–16. [Google Scholar] [CrossRef] [PubMed]

- McCrae, Robert R., and Paul T. Costa Jr. 2008. The five-factor theory of personality. In Handbook of Personality: Theory and Research. Edited by Oliver P. John, Richard W. Robins and Lawrence A. Pervin. New York: The Guilford Press, pp. 159–81. [Google Scholar]

- Millroth, Philip, Peter Juslin, Anders Winman, Hakan Nilsson, and Marcus Lindskog. 2020. Preference or ability: Exploring the relations between risk preference, personality, and cognitive abilities. Journal of Behavioral Decision Making 33: 477–91. [Google Scholar] [CrossRef]

- Mishra, Manit, and Sasmita Mishra. 2016. Financial Risk Tolerance among Indian Investors: A Multiple Discriminant Modeling of Determinants. Strategic Change 25: 485–500. [Google Scholar] [CrossRef]

- Mishra, Sandeep, Martin L. Lalumière, and Robert J. Williams. 2010. Gambling as a form of risk-taking: Individual differences in personality, risk-accepting attitudes, and behavioral preferences for risk. Personality and Individual Differences 49: 616–21. [Google Scholar] [CrossRef]

- Mouna, Amari, and Anis Jarboui. 2015. Financial literacy and portfolio diversification: An observation from the Tunisian stock market. International Journal of Bank Marketing 33: 808–22. [Google Scholar] [CrossRef]

- Nadeem, Muhammad Asif, Muhammad Ali Jibran Qamar, Mian Sajid Nazir, Israr Ahmad, Anton Timoshin, and Khurram Shehzad. 2020. How investors attitudes shape stock market participation in the presence of financial self-efficacy. Frontiers in Psychology 11: 553351. [Google Scholar] [CrossRef]

- Noussair, Charles N., Stefan T. Trautmann, and Gijs van de Kuilen. 2014. Higher Order Risk Attitudes, Demographics, and Financial Decisions. The Review of Economic Studies 81: 325–55. [Google Scholar] [CrossRef]

- Pak, Olga, and Monowar Mahmood. 2015. Impact of personality on risk tolerance and investment decisions: A study on potential investors of Kazakhstan. International Journal of Commerce and Management 25: 370–84. [Google Scholar] [CrossRef]

- Pandit, Ameet, and Ken Yeoh. 2014. Psychological Tendencies in an Emerging Capital Market: A Study of Individual Investors in India. The Journal of Developing Areas 48: 129–48. Available online: http://www.jstor.org/stable/24241232 (accessed on 14 February 2024). [CrossRef]

- Park, Kwangho, Insun Yang, and Taeyong Yang. 2017. The peer-firm effect on firm’s investment decisions. The North American Journal of Economics and Finance 40: 178–99. [Google Scholar] [CrossRef]

- Purkayastha, Saptarshi. 2008. Investor profiling and investment planning: An empirical study. The IUP Journal of Management Research 7: 17–40. [Google Scholar]

- Rajasekar, Arvindh, Arul Ramanatha Pillai, Rajesh Elangovan, and Satyanarayana Parayitam. 2022. Risk capacity and investment priority as moderators in the relationship between big-five personality factors and investment behavior: A conditional moderated moderated-mediation model. Quality & Quantity 57: 2091–123. [Google Scholar]

- Rath, Prabath Kumar. 2023. Nexus between Indian Financial Markets and Macro-economic Shocks: A VAR Approach. Asia-Pacific Financial Markets 30: 131–64. [Google Scholar] [CrossRef]

- Ricciardi, Victor. 2008. The psychology of risk: The behavioral finance perspective. Handbook of Finance: Investment Management and Financial Management 2: 85–111. [Google Scholar]

- Riitsalu, Leonore, and Rein Murakas. 2019. Subjective financial knowledge, prudent behaviour and income: The predictors of financial well-being in Estonia. International Journal of Bank Marketing 37: 934–50. [Google Scholar] [CrossRef]

- Rossberger, Robert J. 2014. National personality profiles and innovation: The role of cultural practices. Creativity and Innovation Management 23: 331–48. [Google Scholar] [CrossRef]

- Roszkowski, Michael J., Geoff Davey, and John E. Grable. 2005. Insights from psychology and psychometrics on measuring risk tolerance. Journal of Financial Planning 18: 66–76. [Google Scholar]

- Rothman, Tiran. 2017. How Behavioral Finance Patterns affect Investors’ Activity in Capital Markets? Journal of Business & Financial Affairs 6: 277. [Google Scholar] [CrossRef]

- Sahi, Shalini Kalra, Ashok Pratap Arora, and Nand Dhameja. 2013. An exploratory inquiry into the psychological biases in financial investment behavior. Journal of Behavioral Finance 14: 94–103. [Google Scholar] [CrossRef]

- Saivasan, Rangapriya, and Madhavi Lokhande. 2022. Influence of risk propensity, behavioural biases and demographic factors on equity investors’ risk perception. Asian Journal of Economics and Banking 6: 373–403. [Google Scholar] [CrossRef]

- Sanfelici, Daniel, and Maira Magnani. 2022. Pension fund investment in commercial real estate: A qualitative analysis of decision-making and investment practices in Brazil. Area Development and Policy 7: 62–81. [Google Scholar] [CrossRef]

- Shanmugam, Karthikeyan, Vijayabanu Chidambaram, and Satyanarayana Parayitam. 2022a. Effect of financial knowledge and information behavior on sustainable investments: Evidence from India. Journal of Sustainable Finance & Investment, 1–24. [Google Scholar] [CrossRef]

- Shanmugam, Karthikeyan, Vijayabanu Chidambaram, and Satyanarayana Parayitam. 2022b. Relationship Between Big-Five Personality Traits, Financial Literacy and Risk Propensity: Evidence from India. IIM Kozhikode Society & Management Review 12: 85–101. [Google Scholar]

- Sindhu, K. P., and S. Rajitha Kumar. 2014. Influence of risk perception of investors on investment decisions: An empirical analysis. Journal of Finance and Bank Management 2: 15–25. [Google Scholar]

- Sitkin, Sim B., and Amy L. Pablo. 1992. Reconceptualizing the determinants of risk behavior. Academy of Management Review 17: 9–38. [Google Scholar] [CrossRef]

- Sivaramakrishnan, Sreeram, Mala Srivastava, and Anupam Rastogi. 2017. Attitudinal factors, financial literacy, and stock market participation. International Journal of Bank Marketing 35: 818–41. [Google Scholar] [CrossRef]

- Streich, David J. 2023. Risk preference elicitation and financial advice taking. Journal of Behavioral Finance 24: 259–75. [Google Scholar] [CrossRef]

- Tekce, Bulent, and Neslihan Yılmaz. 2015. Are individual stock investors overconfident? Evidence from an emerging market. Journal of Behavioral and Experimental Finance 5: 35–45. [Google Scholar] [CrossRef]

- ul Abdin, Syed Zain, Fiza Qureshi, Jawad Iqbal, and Sayema Sultana. 2022. Overconfidence bias and investment performance: A mediating effect of risk propensity. Borsa Istanbul Review 22: 780–93. [Google Scholar] [CrossRef]

- Weele, Inger. 2013. The Effects of CEO’s Personality Traits (Big 5) and a CEO’s External Network on Innovation Performance in SMEs. Bachelor’s thesis, University of Twente, Enschede, The Netherlands. [Google Scholar]

- Wood, Ryan, and Judith Lynne Zaichkowsky. 2004. Attitudes and trading behavior of stock market investors: A segmentation approach. The Journal of Behavioral Finance 5: 170–79. [Google Scholar] [CrossRef]

- Xiao, Jing Jian, and Nilton Porto. 2017. Financial education and financial satisfaction: Financial literacy, behavior, and capability as mediators. International Journal of Bank Marketing 35: 805–17. [Google Scholar] [CrossRef]

- Young, Susan, Gisli H. Gudjonsson, Philippa Carter, Rachel Terry, and Robin Morris. 2012. Simulation of risk-taking and it relationship with personality. Personality and Individual Differences 53: 294–29. [Google Scholar] [CrossRef]

- Zheng, Congcong, and Radmila Prislin. 2012. Beyond Risk Propensity-The Influence of Evaluation Period and Information Relevance on Risk Taking Behavior. Academy of Entrepreneurship Journal 18: 1–10. [Google Scholar]

Figure 1.

Conceptual model.

Figure 2.

Conscientiousness as a moderator in the relationship between investment priority and investment decision.

Figure 2.

Conscientiousness as a moderator in the relationship between investment priority and investment decision.

Figure 3.

Empirical model, *** p < 0.001.

{kind=link}

{kind=link}

{kind=link}

Table 1.

Demographic profile of respondents.

| Category | Profile | Total Number | Percentage |

|---|---|---|---|

| Gender | Male | 191 | 35.6 |

| Female | 346 | 64.4 | |

| Age | 21–25 | 233 | 43.4 |

| 26–30 | 97 | 18.1 | |

| 31–35 | 77 | 14.3 | |

| 36–40 | 53 | 9.9 | |

| 40 and above | 77 | 14.3 | |

| Educational qualification | 10th or +2 | 26 | 4.8 |

| Vocational education | 30 | 5.6 | |

| Undergraduate degree | 163 | 30.4 | |

| Masters’ degree | 252 | 46.9 | |

| Others (Professional) | 66 | 12.3 | |

| Marital | Married | 284 | 52.9 |

| Unmarried | 232 | 43.2 | |

| Widowed | 12 | 2.2 | |

| Divorced | 9 | 1.7 | |

| Occupation | Employee | 157 | 29.2 |

| Businessmen | 20 | 3.7 | |

| Professionals | 72 | 13.4 | |

| Others | 288 | 53.6 | |

| Annual Income (INR = Indian Rupees $ = US Dollar) | Below INR 120,000 ($1500) | 241 | 44.9 |

| Rs. 120,000–Rs. 240,000 ($1500–$3000) | 82 | 15.3 | |

| INR240,000–Rs. 360,000 ($3000–$4500) | 62 | 11.5 | |

| INR 360,000- Rs. 480,000 ($4500–$6000) | 47 | 8.8 | |

| INR 480,000–Rs. 600,000 ($6000–$7500) | 36 | 6.7 | |

| Above INR 600,000 ($7500) | 69 | 12.8 | |

| Residential status | Urban | 194 | 36.1 |

| Semi Urban | 142 | 26.4 | |

| Rural | 201 | 37.4 |

Source: The authors.

Table 2.

Results of Confirmatory Factor Analysis (CFA) and measurement properties.

| Constructs and Source of These Constructs | Alpha | Standardized Loadings (λyi) | Reliability (λ2yi) | Variance (Var(Ɛi)) | Average Variance Extracted Estimate Ʃ (λ2yi)/[(λ2yi) + (Var(Ɛi))] |

|---|---|---|---|---|---|

| Risk Capacity (Rajasekar et al. 2022) | 0.93 | 0.61 | |||

| I pull back my investment funds in money market stores for emergencies | 0.72 | 0.52 | 0.48 | ||

| I take a loan for promising long-term investing opportunity | 0.77 | 0.60 | 0.40 | ||

| I take a loan for promising short-term investing opportunity | 0.80 | 0.63 | 0.37 | ||

| I make necessary changes to improve my investment performance, using my judgment | 0.83 | 0.69 | 0.31 | ||

| I wait it out, anticipating future improvements over the long run | 0.81 | 0.65 | 0.35 | ||

| I consult with a financial advisor before taking any action | 0.78 | 0.61 | 0.39 | ||

| I indulge in panic selling | 0.78 | 0.61 | 0.39 | ||

| I assess the tax implications of the investment | 0.80 | 0.65 | 0.35 | ||

| I determine my return objective for the investment | 0.78 | 0.61 | 0.39 | ||

| I am real gambler willing to task risk after completing adequate research | 0.72 | 0.52 | 0.48 | ||

| Risk Tolerance (Joo and Grable 2004) | 0.84 | 0.61 | |||

| Investing is too difficult to understand | 0.70 | 0.49 | 0.51 | ||

| I am more comfortable putting my money in a bank account than in the stock market | 0.80 | 0.63 | 0.37 | ||

| When I think of the word “risk” the term “loss” comes to mind immediately | 0.82 | 0.67 | 0.33 | ||

| Making money in stocks and bonds is based on luck | 0.80 | 0.63 | 0.37 | ||

| In terms of investing, safety is more important than returns | 0.80 | 0.64 | 0.36 | ||

| Risk Propensity (Bucciol and Miniaci 2018) | 0.86 | 0.58 | |||

| I think it is more important to have safe investments and guaranteed returns, than to take a risk to have a chance to get the highest possible returns | 0.73 | 0.53 | 0.47 | ||

| I would never consider investments in shares because I find this too risky | 0.76 | 0.57 | 0.43 | ||

| If I think an investment will be profitable, I am prepared to borrow money to make this investment | 0.72 | 0.52 | 0.48 | ||

| I want to be certain that my investments are safe | 0.82 | 0.68 | 0.32 | ||

| I get more and more convinced that I should take greater financial risks to improve my financial position | 0.82 | 0.67 | 0.33 | ||

| I am prepared to take the risk to lose money, when there is also a chance to gain money | 0.73 | 0.54 | 0.46 | ||

| Investment Priority (Rajasekar et al. 2022) | 0.92 | 0.65 | |||

| I invest my pension amount to satisfy my retirement objectives | 0.77 | 0.59 | 0.41 | ||

| To ensure a comfortable retirement | 0.81 | 0.66 | 0.34 | ||

| I invest the money as a principle instalment of my house | 0.74 | 0.55 | 0.45 | ||

| To achieve high growth in investments | 0.84 | 0.71 | 0.29 | ||

| To protect income in case of death or disability | 0.82 | 0.67 | 0.33 | ||

| To ensure transfer of assets to dependents smoothly | 0.84 | 0.71 | 0.29 | ||

| To invest in an endowment plan (Assured returns + Risk cover) | 0.84 | 0.70 | 0.30 | ||

| To invest in unit linked insurance plan (Market linked returns + Risk cover) | 0.80 | 0.64 | 0.36 | ||

| Investment Strategy (Rajasekar et al. 2022) | 0.93 | 0.61 | |||

| I review my overall investment goals | 0.73 | 0.54 | 0.46 | ||

| I consider the variety of investment options | 0.83 | 0.69 | 0.31 | ||

| I get investment information from financial advisor (Individual or Institutional) | 0.78 | 0.61 | 0.39 | ||

| I get investment information from television | 0.73 | 0.54 | 0.46 | ||

| I buy or sell investments over online trading | 0.71 | 0.50 | 0.50 | ||

| I use investment analysis or management software | 0.72 | 0.52 | 0.48 | ||

| I discuss with my family or friends who are knowledgeable in trading | 0.81 | 0.65 | 0.35 | ||

| I assess the convenience with which the investment can be made, looked after and disposed | 0.83 | 0.68 | 0.32 | ||

| I weigh all the pros and cons and analyze all the facts before taking financial decisions | 0.84 | 0.71 | 0.29 | ||

| Safety of investment is the most important factor I look at when choosing a investment strategy | 0.79 | 0.63 | 0.37 | ||

| Conscientiousness (Rajasekar et al. 2022) | 0.93 | 0.77 | |||

| Does a thorough job of financial planning | 0.83 | 0.69 | 0.31 | ||

| Is a reliable in every task performing | 0.89 | 0.80 | 0.21 | ||

| Perseveres until the task is finished | 0.90 | 0.82 | 0.18 | ||

| Does things efficiently | 0.89 | 0.80 | 0.20 | ||

| Makes plans and follows through with them | 0.88 | 0.77 | 0.24 | ||

| Investment Decision (Sahi et al. 2013) | 0.85 | 0.69 | |||

| I will choose investments based on the information easily available to me | 0.85 | 0.72 | 0.28 | ||

| I know that this investment did very well before, so I invested here again | 0.88 | 0.77 | 0.23 | ||

| Last week I read that the gold prices will go up so, I invested more in gold | 0.78 | 0.61 | 0.39 | ||

| I invest in instruments that are readily accessible and convenient | 0.82 | 0.67 | 0.33 |

Table 3.

Descriptive Statistics: Means, Standard deviations, and zero-order correlations. ** Correlation is significant at the 0.01 level (2-tailed); Square root of average variance extracted in diagonals (in bold).

Table 3.

Descriptive Statistics: Means, Standard deviations, and zero-order correlations. ** Correlation is significant at the 0.01 level (2-tailed); Square root of average variance extracted in diagonals (in bold).

| Variables | Mean | SD | 1 | 2 | 3 | 4 | 5 | 6 | 7 | Cronbach Alpha | Composite Reliability | Average Variance Extracted Estimates |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1. Risk capacity | 2.99 | 0.85 | 0.78 | 0.93 | 0.94 | 0.61 | ||||||

| 2. Risk tolerance | 2.99 | 0.85 | 1.00 ** | 0.78 | 0.84 | 0.89 | 0.61 | |||||

| 3. Risk propensity | 3.05 | 0.85 | 0.66 ** | 0.66 ** | 0.76 | 0.86 | 0.90 | 0.58 | ||||

| 4. Investment priority | 3.12 | 0.89 | 0.54 ** | 0.54 ** | 0.70 ** | 0.81 | 0.92 | 0.94 | 0.65 | |||

| 5. Investment strategy | 3.06 | 0.88 | 0.53 ** | 0.53 ** | 0.66 ** | 0.77 ** | 0.78 | 0.93 | 0.94 | 0.61 | ||

| 6. Conscientiousness | 3.26 | 0.99 | 0.53 ** | 0.53 ** | 0.49 ** | 0.47 ** | 0.50 ** | 0.88 | 0.93 | 0.94 | 0.77 | |

| 7. Investment decision | 3.11 | 0.94 | 0.52 ** | 0.52 ** | 0.62 ** | 0.72 ** | 0.68 ** | 0.48 ** | 0.83 | 0.85 | 0.90 | 0.69 |

Source: The authors. Notes: ** Correlation is significant at the 0.01 level (2-tailed). Square root of Average Variance Extracted in diagonals (in bold).

Table 4.

Discriminant validity using HTMT (Heterotrait-Monotrait).

| Constructs | 1 | 2 | 3 | 4 | 5 | 6 | 7 |

|---|---|---|---|---|---|---|---|

| 1. Conscientiousness | |||||||

| 2. Investment decision making | 0.54 | ||||||

| 3. Investment priority | 0.50 | 0.81 | |||||

| 4. Investment strategy | 0.53 | 0.77 | 0.83 | ||||

| 5. Risk capacity | 0.48 | 0.71 | 0.72 | 0.74 | |||

| 6. Risk propensity | 0.55 | 0.72 | 0.78 | 0.75 | 0.77 | ||

| 7. Risk tolerance | 0.60 | 0.61 | 0.62 | 0.60 | 0.67 | 0.79 |

Source: The authors.

Table 5.

Outer VIF Values.

| Indicator | VIF | Indicator | VIF |

|---|---|---|---|

| Risk capacity 1 | 1.807 | Investment priority 5 | 2.429 |

| Risk capacity 2 | 2.41 | Investment priority 6 | 2.609 |

| Risk capacity 3 | 2.587 | Investment priority 7 | 2.629 |

| Risk capacity 4 | 2.707 | Investment priority 8 | 2.427 |

| Risk capacity 5 | 2.448 | Investment strategy 1 | 2.28 |

| Risk capacity 6 | 2.199 | Investment strategy 2 | 3.114 |

| Risk capacity 7 | 2.309 | Investment strategy 3 | 2.326 |

| Risk capacity 8 | 2.512 | Investment strategy 4 | 2.319 |

| Risk capacity 9 | 2.272 | Investment strategy 5 | 2.477 |

| Risk capacity 10 | 1.814 | Investment strategy 6 | 2.446 |

| Risk tolerance 1 | 1.427 | Investment strategy 7 | 2.444 |

| Risk tolerance 2 | 1.905 | Investment strategy 8 | 2.87 |

| Risk tolerance 3 | 2.071 | Investment strategy 9 | 3.368 |

| Risk tolerance 4 | 1.825 | Investment strategy 10 | 2.864 |

| Risk tolerance 5 | 1.765 | Conscientiousness 1 | 2.668 |

| Risk propensity 1 | 1.799 | Conscientiousness 2 | 3.655 |

| Risk propensity 2 | 1.845 | Conscientiousness 3 | 3.436 |

| Risk propensity 3 | 1.838 | Conscientiousness 4 | 3.228 |

| Risk propensity 4 | 2.192 | Conscientiousness 5 | 3.846 |

| Risk propensity 5 | 2.249 | Investment decision 1 | 2.46 |

| Risk propensity 6 | 1.834 | Investment decision 2 | 2.722 |

| Investment priority 1 | 2.161 | Investment decision 3 | 1.642 |

| Investment priority 2 | 2.586 | Investment decision 4 | 1.783 |

| Investment priority 3 | 1.782 | ||

| Investment priority 4 | 2.64 |

Source: The authors.

Table 6.

Inner VIF Values.

| Constructs | 1 | 2 | 3 | 4 | 5 | 6 | 7 |

|---|---|---|---|---|---|---|---|

| 1.Risk capacity | 2.03 | 2.03 | |||||

| 2. Risk tolerance | 2.34 | 2.34 | |||||

| 3. Risk propensity | 1.92 | 1.92 | |||||

| 4. Investment priority | 2.46 | ||||||

| 5. Investment strategy | 2.46 | ||||||

| 6. Conscientiousness | 1.40 | ||||||

| 7. Investment decision |

Source: The authors.

Table 7.

Results of hypotheses testing.

| Hypotheses | Relationships | β | t | p | Result |

|---|---|---|---|---|---|

| H1 | Risk capacity → investment priority | 0.520 | 15.111 | 0.000 | Supported |

| H2 | Risk tolerance → investment priority | 0.490 | 12.231 | 0.000 | Supported |

| H3 | Risk propensity → investment priority | 0.658 | 21.387 | 0.000 | Supported |

| H4 | Risk capacity → investment strategy | 0.546 | 15.768 | 0.000 | Supported |

| H5 | Risk tolerance → investment strategy | 0.514 | 14.368 | 0.000 | Supported |

| H6 | Risk propensity → investment strategy | 0.646 | 19.807 | 0.000 | Supported |

| H7 | Investment priority → investment decision | 0.685 | 21.447 | 0.000 | Supported |

| H8 | Investment strategy → investment decision making | 0.642 | 19.666 | 0.000 | Supported |

| H7a | Investment priority × Conscientiousness → investment decision | 0.623 | 19.042 | 0.000 | Supported |

Source: The authors.

Table 8.

Conditional effect of focal predictor (Conscientiousness) at values of the moderator.

| Conscientiousness | Effect | se | t | p | LLCI | ULCI |

|---|---|---|---|---|---|---|

| 1.0000 | 0.8389 | 0.0656 | 12.7868 | 0.0000 | 0.7100 | 0.9678 |

| 1.1905 | 0.8230 | 0.0614 | 13.4106 | 0.0000 | 0.7024 | 0.9435 |

| 1.3810 | 0.8071 | 0.0573 | 14.0937 | 0.0000 | 0.6946 | 0.9195 |

| 1.5714 | 0.7911 | 0.0533 | 14.8362 | 0.0000 | 0.6864 | 0.8959 |

| 1.7619 | 0.7752 | 0.0496 | 15.6321 | 0.0000 | 0.6778 | 0.8726 |

| 1.9524 | 0.7593 | 0.0461 | 16.4661 | 0.0000 | 0.6687 | 0.8499 |

| 2.1429 | 0.7434 | 0.0429 | 17.3074 | 0.0000 | 0.6590 | 0.8277 |

| 2.3333 | 0.7274 | 0.0402 | 18.1042 | 0.0000 | 0.6485 | 0.8064 |

| 2.5238 | 0.7115 | 0.0379 | 18.7790 | 0.0000 | 0.6371 | 0.7859 |

| 2.7143 | 0.6956 | 0.0362 | 19.2333 | 0.0000 | 0.6245 | 0.7666 |

| 2.9048 | 0.6797 | 0.0351 | 19.3659 | 0.0000 | 0.6107 | 0.7486 |

| 3.0952 | 0.6637 | 0.0347 | 19.1064 | 0.0000 | 0.5955 | 0.7320 |

| 3.2857 | 0.6478 | 0.0351 | 18.4472 | 0.0000 | 0.5788 | 0.7168 |

| 3.4762 | 0.6319 | 0.0362 | 17.4520 | 0.0000 | 0.5608 | 0.7030 |

| 3.6667 | 0.6160 | 0.0379 | 16.2317 | 0.0000 | 0.5414 | 0.6905 |

| 3.8571 | 0.6000 | 0.0403 | 14.9059 | 0.0000 | 0.5210 | 0.6791 |

| 4.0476 | 0.5841 | 0.0430 | 13.5722 | 0.0000 | 0.4996 | 0.6687 |

| 4.2381 | 0.5682 | 0.0462 | 12.2959 | 0.0000 | 0.4774 | 0.6590 |

| 4.4286 | 0.5523 | 0.0497 | 11.1127 | 0.0000 | 0.4546 | 0.6499 |

| 4.6190 | 0.5363 | 0.0534 | 10.0368 | 0.0000 | 0.4314 | 0.6413 |

| 4.8095 | 0.5204 | 0.0574 | 9.0694 | 0.0000 | 0.4077 | 0.6331 |

| 4.8095 | 0.5045 | 0.0615 | 8.2044 | 0.0000 | 0.3837 | 0.6253 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Lathief, J.T.A.; Kumaravel, S.C.; Velnadar, R.; Vijayan, R.V.; Parayitam, S. Quantifying Risk in Investment Decision-Making. J. Risk Financial Manag. 2024, 17, 82. https://doi.org/10.3390/jrfm17020082

AMA Style

Lathief JTA, Kumaravel SC, Velnadar R, Vijayan RV, Parayitam S. Quantifying Risk in Investment Decision-Making. Journal of Risk and Financial Management. 2024; 17(2):82. https://doi.org/10.3390/jrfm17020082

Chicago/Turabian StyleLathief, Jaheera Thasleema Abdul, Sunitha Chelliah Kumaravel, Regina Velnadar, Ravi Varma Vijayan, and Satyanarayana Parayitam. 2024. "Quantifying Risk in Investment Decision-Making" Journal of Risk and Financial Management 17, no. 2: 82. https://doi.org/10.3390/jrfm17020082