Analysing the Impact of Crises on Financial Performance: Empirical Insights from Tourism and Transport Companies Listed on the Bucharest Stock Exchange (during 2005–2022)

Abstract

:1. Introduction

2. Literature

2.1. Current State of Research on Financial Performance Analysis and Organisational Resilience

2.2. Hypotheses

3. Methodology

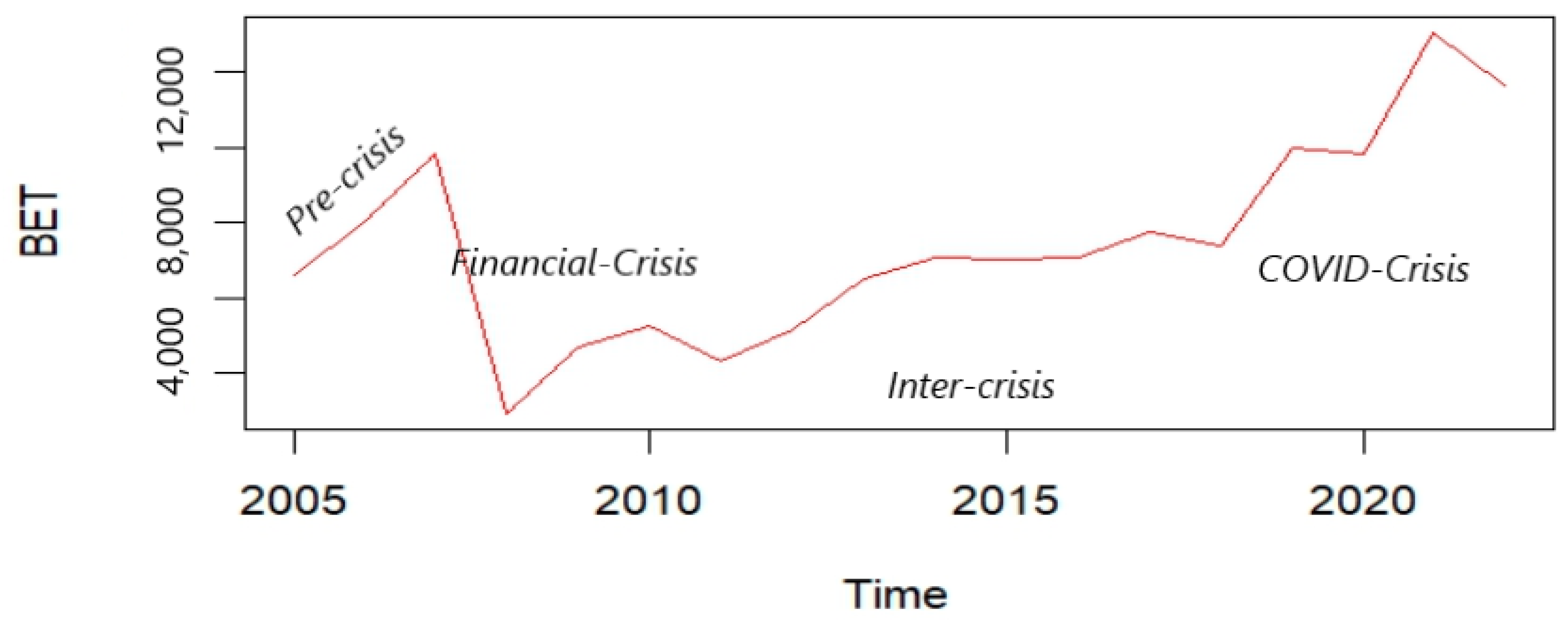

3.1. Data and Variables

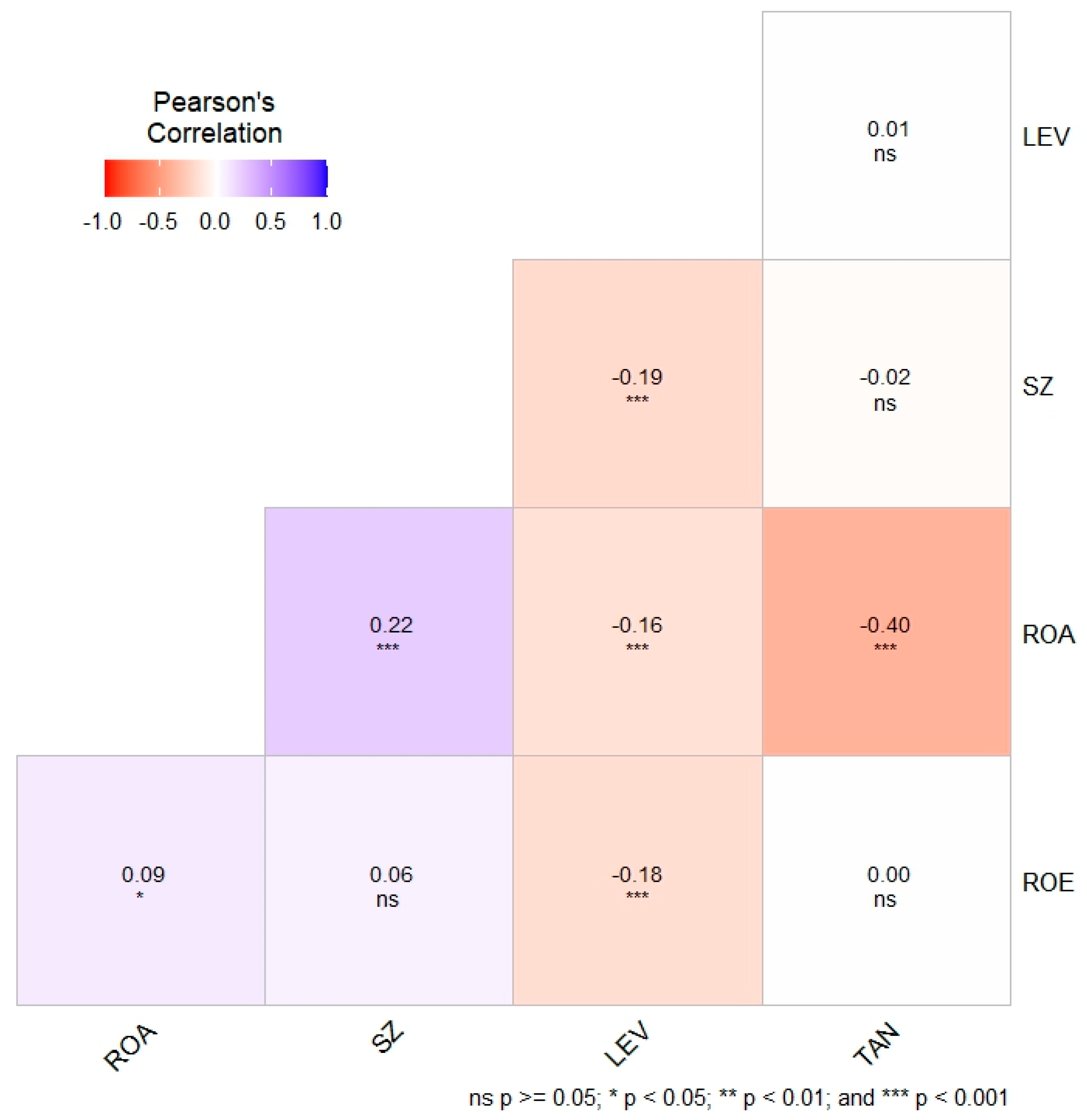

3.2. Descriptive Statistics and Correlations

3.3. Method

4. Results and Discussion

4.1. Leverage and Financial Performance

4.2. Leverage, Crisis, and Financial Performance

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Ahmad, Muhammad Ishfaq, Wang Guohui, Mudassar Hasan, Muhammad Yasir Rafiq, and Ramiz-Ur Rehman. 2017. Financial Leverage Hits Corporate Performance. In Advances in Applied Economic Research. Edited by Nicholas Tsounis and Aspasia Vlachvei. Springer Proceedings in Business and Economics. Cham: Springer, pp. 125–38. [Google Scholar]

- Al-Rdaydeh, Mahmoud, Ammar Yaser Almansour, and Mohammad Ahmad Al-Omari. 2018. Moderating effect of competitive strategies on the relation between financial leverage and firm performance: Evidence from Jordan. Business and Economic Horizons 14: 626–41. [Google Scholar] [CrossRef]

- Amankwah-Amoah, Joseph, Zaheer Khan, and Geoffrey Wood. 2021. COVID-19 and business failures: The paradoxes of experience, scale, and scope for theory and practice. European Management Journal 39: 179–84. [Google Scholar] [CrossRef]

- Brick, Ivan E., Oded Palmon, and John K. Wald. 2006. CEO compensation, director compensation, and firm performance: Evidence of cronyism? Journal of Corporate Finance 12: 403–23. [Google Scholar] [CrossRef]

- Brown, Lawrence D., and Marcus L. Caylor. 2006. Corporate governance and firm valuation. Journal of Accounting and Public Policy 25: 409–34. [Google Scholar] [CrossRef]

- BSE. 2023. Bursa de Valori București. Available online: https://www.bvb.ro/ (accessed on 22 May 2023).

- Bui, Tung Duy, Huan Huu Nguyen, and Vu Minh Ngo. 2021. Financial leverage and performance of smes in Vietnam: Evidence from the post-crisis period. Economics and Business Letters 10: 229–39. [Google Scholar] [CrossRef]

- Carvalho, Antonio Oliveira de, Ivano Ribeiro, Claudia Brito Silva Cirani, and Renato Fabiano Cintra. 2016. Organizational resilience: A comparative study between innovative and non-innovative companies based on the financial performance analysis. International Journal of Innovation 4: 58–69. [Google Scholar] [CrossRef]

- Chen, Yasheng, and Zhuojun Wu. 2022. Taking Risks to Make Profit during COVID-19. Sustainability 14: 15750. [Google Scholar] [CrossRef]

- Collins, Simon. 2015. Strategising for Resilience. Ph.D. thesis, Victoria University of Wellington, Wellington, New Zealand. [Google Scholar]

- Dang, Thuy T., Nguyen Tran Xuan Linh, Hau Trung Nguyen, and Dinh Cong Hoang. 2024. Impacts of Capital Structure on Microfinance Institutions’ Risk: Evidence from Low- and Middle-Income Countries. In Studies in Systems, Decision and Control. Cham: Springer, vol. 483, pp. 654–66. [Google Scholar]

- Danso, Albert, Theophilus A. Lartey, Daniel Gyimah, and Emmanuel Adu-Ameyaw. 2021. Leverage and performance: Do size and crisis matter? Managerial Finance 47: 635–55. [Google Scholar] [CrossRef]

- Deliaune, Hervé. 2015. Pour une approche proxémique de l’ingénierie de la résilience: Conditions managériales de la réduction de l’incertitude. Le cas d’une PME confrontée au désarroi organisationnel. Doctoral dissertation. Available online: http://www.theses.fr/2015PAUU2002 (accessed on 22 May 2023).

- DesJardine, Mark, Pratima Bansal, and Yang Yang. 2017. Bouncing Back: Building Resilience Through Social and Environmental Practices in the Context of the 2008 Global Financial Crisis. Journal of Management 45: 1434–60. [Google Scholar] [CrossRef]

- Donthu, Naveen, and Anders Gustafsson. 2020. Effects of COVID-19 on business and research. Journal of Business Research 117: 284–89. [Google Scholar] [CrossRef]

- Duchek, Stephanie. 2019. Organizational resilience: A capability-based conceptualization. Business Research 13: 215–46. [Google Scholar] [CrossRef]

- Epps, Ruth W., and Sandra J. Cereola. 2008. Do institutional shareholder services (ISS) corporate governance ratings reflect a company’s operating performance? Critical Perspectives on Accounting 19: 1135–48. [Google Scholar] [CrossRef]

- Gisladottir, Viktoria, Alexander A. Ganin, Jeffrey M. Keisler, Jeremy Kepner, and Igor Linkov. 2017. Resilience of Cyber Systems with Over- and Underregulation. Risk Analysis 37: 1644–51. [Google Scholar] [CrossRef]

- Gittell, Jody Hoffer, Kim Cameron, Sandy Lim, and Victor Rivas. 2006. Relationships, Layoffs, and Organizational Resilience: Airline Industry Responses to September 11. The Journal of Applied Behavioral Science 42: 300–29. [Google Scholar] [CrossRef]

- Hall, C. Michael. 2010. Crisis events in tourism: Subjects of crisis in tourism. Current Issues in Tourism 13: 401–17. [Google Scholar] [CrossRef]

- Jackling, Beverley, and Shireenjit Johl. 2009. Board Structure and Firm Performance: Evidence from India’s Top Companies. Corporate Governance: An International Review 17: 492–509. [Google Scholar] [CrossRef]

- Karanovic, Goran, Ana Štambuk, and Davor Jagodić. 2020. Profitability Performance under Capital Structure and other Company Characteristics: An Empirical Study of Croatian Hotel Industry. Journal of The Polytechnics of Rijeka 8: 227–42. [Google Scholar]

- Khin Khin Oo, Nay Chi, and Sirisuhk Rakthin. 2022. Integrative Review of Absorptive Capacity&rsquo’s Role in Fostering Organizational Resilience and Research Agenda. Sustainability 14: 12570. [Google Scholar]

- Lo, Kin. 2003. Economic consequences of regulated changes in disclosure: The case of executive compensation. Journal of Accounting and Economics 35: 285–314. [Google Scholar] [CrossRef]

- Mal, Suraj, R. B. Singh, Christian Huggel, and Aakriti Grover. 2018. Introducing Linkages between Climate Change, Extreme Events, and Disaster Risk Reduction. In Climate Change, Extreme Events and Disaster Risk Reduction: Towards Sustainable Development Goals. Edited by Suraj Mal, R. B. Singh and Christian Huggel. Cham: Springer International Publishing. [Google Scholar]

- Mareque, Mercedes, Francisco López-Corrales, and Aurea Pedrosa. 2017. Audit reporting for going concern in Spain during the global financial crisis. Economic Research-Ekonomska Istraživanja 30: 154–83. [Google Scholar] [CrossRef]

- Maxwell, James Clerk. 1997. VIII. A dynamical theory of the electromagnetic field. Philosophical Transactions of the Royal Society of London 155: 459–512. [Google Scholar]

- Morck, Randall, Masao Nakamura, and Anil Shivdasani. 2000. Banks, Ownership Structure, and Firm Value in Japan. The Journal of Business 73: 539–67. [Google Scholar] [CrossRef]

- Ortiz-De-Mandojana, Natalia, and Pratima Bansal. 2016. The long-term benefits of organizational resilience through sustainable business practices. Strategic Management Journal 37: 1615–31. [Google Scholar] [CrossRef]

- Pal, Rudrajeet, Håkan Torstensson, and Heikki Mattila. 2014. Antecedents of organizational resilience in economic crises—An empirical study of Swedish textile and clothing SMEs. International Journal of Production Economics 147: 410–28. [Google Scholar] [CrossRef]

- Palazzo, Maria, Iza Gigauri, Mirela Clementina Panait, Simona Andreea Apostu, and Alfonso Siano. 2022. Sustainable Tourism Issues in European Countries during the Global Pandemic Crisis. Sustainability 14: 3844. [Google Scholar] [CrossRef]

- Palmi, Pamela, Domenico Morrone, Pier Paolo Miglietta, and Giulio Fusco. 2018. How Did Organizational Resilience Work Before and after the Financial Crisis? An Empirical Study. International Journal of Business and Management 13: 54–62. [Google Scholar] [CrossRef]

- Palttala, Pauliina, and Maria Vos. 2012. Quality Indicators for Crisis Communication to Support Emergency Management by Public Authorities. Journal of Contingencies and Crisis Management 20: 39–51. [Google Scholar] [CrossRef]

- Pinel, William. 2009. La résilience organisationnelle: Concepts et activités de formation. Master’s thesis, École Polytechnique de Montréal, Montréal, QC, Canada. [Google Scholar]

- Pinnuck, Matt. 2012. A Review of the Role of Financial Reporting in the Global Financial Crisis. Australian Accounting Review 22: 1–14. [Google Scholar] [CrossRef]

- Prayag, Girish, Mesbahuddin Chowdhury, Samuel Spector, and Caroline Orchiston. 2018. Organizational resilience and financial performance. Annals of Tourism Research 73: 193–96. [Google Scholar] [CrossRef]

- Qian, Meijun, and Bernard Y. Yeung. 2015. Bank financing and corporate governance. Journal of Corporate Finance 32: 258–70. [Google Scholar] [CrossRef]

- Richtnér, Anders, and Hans Löfsten. 2014. Managing in turbulence: How the capacity for resilience influences creativity. R&D Management 44: 137–51. [Google Scholar]

- Robu, Ioan-Bogdan, and Costel Istrate. 2014. Empirical study on the analysis of the global financial crisis influence on the accounting information reported by Romanian listed companies. Procedia Economics and Finance 15: 280–87. [Google Scholar] [CrossRef]

- Tingbani, Ishmael, Godwin Okafor, Venancio Tauringana, and Alaa Mansour Zalata. 2019. Terrorism and country-level global business failure. Journal of Business Research 98: 430–40. [Google Scholar] [CrossRef]

- Tooze, Adam. 2018. Crashed: How a Decade of Financial Crises Changed the World. London: Penguin. [Google Scholar]

- Yu, Wantao, Mark A. Jacobs, Roberto Chavez, and Jiehui Yang. 2019. Dynamism, disruption orientation, and resilience in the supply chain and the impacts on financial performance: A dynamic capabilities perspective. International Journal of Production Economics 218: 352–62. [Google Scholar] [CrossRef]

- Zabri, Shafie Mohamed, Kamilah Ahmad, and Khaw Khai Wah. 2016. Corporate Governance Practices and Firm Performance: Evidence from Top 100 Public Listed Companies in Malaysia. Procedia Economics and Finance 35: 287–96. [Google Scholar] [CrossRef]

- Zeitun, Rami, and Gary G. Tian. 2007. Capital structure and corporate performance: Evidence from Jordan. Australasian Accounting, Business and Finance Journal 1: 40–61. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Authors and Year of Study | Purpose of the Study | Study Findings |

|---|---|---|

| Gittell et al. (2006) | Investigating the conduct of ten airlines after the 11 September 2001 terrorist attack | The airline industry suffered a severe decline after the crisis, and rapid recovery requires a viable business model to increase financial reserves. |

| Pal et al. (2014) | Analysis of the resilience potential of organisations in crises | The study reviews the following resilience strategies: investment financing and cash flow, physical asset ownership, strategic and operational flexibility, and prudent management. |

| Robu and Istrate (2014) | Analysis of the influence of the global financial crisis on the financial performance of Romanian companies listed on the Bucharest Stock Exchange (BVB) | On average, Romanian companies listed on the BSE maintain a high level of financial autonomy and also a high level of the set provisions. |

| Ortiz-De-Mandojana and Bansal (2016) | Social and environmental practices associated with organisational sustainability contribute to organisational resilience | Organisations that adopt social and environmental practices show lower financial volatility, increased sales, and higher chances of survival. |

| Carvalho et al. (2016) | Analysis of the relationship between innovation and resilience from the perspective of the evolution of financial performance | Innovative companies can achieve higher financial results than non-innovative ones. |

| DesJardine et al. (2017) | The impact of social and environmental practices on organisational resilience after the 2008 global financial crisis | Strategic environmental and social practices create interdependencies between investors, leading to stability. |

| Prayag et al. (2018) | Investigating the relationship between the organisational resilience and financial performance of tourism companies in New Zealand | Planned resilience has no significant influence on financial performance, whereas adaptive resilience does influence financial performance. |

| Palmi et al. (2018) | Analysing the relationship between corporate, environmental, and social governance practices and the economic performance of organisations, assessing their organisational resilience | The study highlights the importance of organisational resilience. Organisations become able to withstand shocks. |

| Yu et al. (2019) | Investigating the impact of supply chain dynamism on risk management, resilience, and financial performance | Supply chain dynamism has a positive effect on risk management and supply chain resilience, and resilience influences financial performance. |

| Danso et al. (2021) | Analysis of the impact of financial leverage on company performance, as well as the extent to which the size of the company and the crisis affect this relationship | Financial leverage significantly and negatively affects firm performance, larger firms have greater resilience, and the global financial crisis did not influence the relationship between financial leverage and firm performance. 1 |

| Field of Activity | Total Companies Listed on BSE | Companies Included in the Study | Weight of Comments |

|---|---|---|---|

| Hotels and restaurants | 21 | 21 | 61.76% |

| Transport and storage | 15 | 13 | 38.24% |

| Total | 36 | 34 | 100% 1 |

| Variable | Period | Indicator | Formula |

|---|---|---|---|

| Dependent Variable | |||

| Return on assets | 2005–2022 | ROA | Net Income/Total Assets |

| Return on equity | 2005–2022 | ROE | Net income/Equity |

| Independent variable | |||

| Overall leverage | 2005–2022 | LEV | Total debt/Total assets |

| Control variables | |||

| Firm size | 2005–2022 | SZ | Log of total assets |

| Assets tangibility | 2005–2022 | TAN | Fixed assets/Total assets 1 |

| Var | Mean | Median | Std. Dev. | Min | Max | 1st Qu. | 3rd Qu. | Obs |

|---|---|---|---|---|---|---|---|---|

| ROA | 0.01973 | 0.01052 | 0.09651 | −0.40451 | 0.86148 | −0.01398 | 0.04574 | 612 |

| ROE | −0.18405 | 0.01685 | 5.05483 | −124.90297 | 3.35046 | −0.01685 | 0.05605 | 612 |

| LEV | 0.185247 | 0.13031 | 0.18306 | 0.0003687 | 1.2834866 | 0.050351 | 0.269766 | 612 |

| SZ | 7.583 | 7.508 | 0.7599189 | 5.631 | 9.903 | 7.113 | 8.089 | 612 |

| TAN | 0.8029 | 0.8741 | 0.2000671 | 0.00 | 1.2562 | 0.7183 | 0.9387 | 612 1 |

| Equation | Method of Panel Data Regression | |

|---|---|---|

| ROA ~ LEV * (SZ + TAN) | (1) | Fixed Effect Method |

| F = 3.2066, df1 = 33, df2 = 573, p-value = 0.00001284 | ||

| ROE ~ LEV * (SZ + TAN) | (2) | Pooled OLS Method |

| F = 0.75795, df1 = 33, df2 = 573, p-value = 0.8348 | ||

| plm(formula = ROA ~ LEV * (SZ + TAN), data = mydata, model = “within”) | ||||

| Balanced Panel: n = 34, T = 18, N = 612 | ||||

| Residuals: | ||||

| Min. | 1st Qu. | Median | 3rd Qu. | Max. |

| −0.3965729 | −0.0304096 | −0.0025022 | 0.0261361 | 0.6638999 |

| Coefficients: | ||||

| Estimate | Std. Error | t-value | Pr(>|t|) | |

| LEV | −1.04 | 0.21 | −5.03 | 0.0000006431 *** |

| SZ | −0.02 | 0.02 | −1.12 | 0.26 |

| TAN | −0.21 | 0.02 | −8.71 | <0.0000 *** |

| LEV:SZ | 0.12 | 0.03 | 4.39 | 0.00001353 *** |

| LEV:TAN | 0.06 | 0.11 | 0.59 | 0.56 |

| Total Sum of Squares: 4.718 | ||||

| Residual Sum of Squares: 3.5657 | ||||

| R-Squared: 0.24422 | ||||

| Adj. R-Squared: 0.1941 | ||||

| F-statistic: 37.0324 on 5 and 573 DF. p-value: < 0.05 | ||||

| Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1 1 | ||||

| plm(formula = ROE ~ LEV * (SZ + TAN), data = mydata, model = “pooling”) | ||||

| Balanced Panel: n = 34, T = 18, N = 612 | ||||

| Residuals: | ||||

| Min. | 1st Qu. | Median | 3rd Qu. | Max. |

| −119.0308 | −0.38707 | 0.022113 | 0.392037 | 12.10678 |

| Coefficients: | ||||

| Estimate | Std. Error | t-value | Pr(>|t|) | |

| (Intercept) | 6.98441 | 3.36482 | 2.0757 | 0.038341 * |

| LEV | −38.0582 | 10.91093 | −3.4881 | 0.000522 *** |

| SZ | −0.81661 | 0.43431 | −1.8803 | 0.06055. |

| TAN | −0.32396 | 1.28859 | −0.2514 | 0.801583 |

| LEV:SZ | 4.18081 | 1.43074 | 2.9221 | 0.003606 ** |

| LEV:TAN | 3.85319 | 5.60728 | 0.6872 | 0.492235 |

| Total Sum of Squares: 15,612 | ||||

| Residual Sum of Squares: 14,872 | ||||

| R-Squared: 0.047409 | ||||

| Adj. R-Squared: 0.03955 | ||||

| F-statistic: 6.03199 on 5 and 606 DF, p-value: 0.000018447 | ||||

| Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1 1 | ||||

| Pre-Crisis | Financial Crisis | Inter-Crisis | COVID-19 Crisis | |

|---|---|---|---|---|

| LEV | 0.5170429 (0.4622434) | −1.604134 (0.380124) *** | −0.3549116 (0.3894683) | −0.370718 (0.719317) |

| SZ | −0.0064898 (0.0291470) | −0.035091 (0.017064) * | 0.0144361 (0.0104217) | 0.025956 (0.031881) |

| TAN | 0.0804022 (0.1022111) | −0.204880 (0.055972) *** | −0.1100167 (0.0367794) ** | −0.294951 (0.057288) *** |

| LEV:SZ | 0.1291974 (0.0694073). | 0.219251 (0.057210) *** | 0.0619663 (0.0431669) | 0.026387 (0.095225) |

| LEV:TAN | −0.5626256 (0.2697109) * | −0.041087 (0.219177) | −0.1694818 (0.1705043) | 0.081556 (0.265487) |

| Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1 1 | ||||

| Pre-Crisis | Financial Crisis | Inter-Crisis | COVID Crisis | |

|---|---|---|---|---|

| LEV | −4.50479 (2.23941) * | −2.81588 (0.507203) *** | −1.44152 (0.5405435) ** | −216.05 (46.2918) *** |

| SZ | 0.12583 (0.13031) | −0.05697 (0.023203) * | −0.00489 (0.0147959) | −6.0935 (2.0366) ** |

| TAN | −1.35785 (0.50944) ** | −0.15207 (0.073233) * | −0.116 (0.0510204) * | 5.273 (3.6442) |

| LEV:SZ | −0.30961 (0.32521) | 0.421482 (0.076866) *** | 0.228456 (0.0602397) *** | 29.4817 (6.2732) *** |

| LEV:TAN | 8.44029 (1.36051) *** | −0.36962 (0.291469) | −0.44838 (0.2343129). | −26.1381 (19.0741) |

| Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1 1 | ||||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Neacșu, M.; Georgescu, I.E. Analysing the Impact of Crises on Financial Performance: Empirical Insights from Tourism and Transport Companies Listed on the Bucharest Stock Exchange (during 2005–2022). J. Risk Financial Manag. 2024, 17, 80. https://doi.org/10.3390/jrfm17020080

Neacșu M, Georgescu IE. Analysing the Impact of Crises on Financial Performance: Empirical Insights from Tourism and Transport Companies Listed on the Bucharest Stock Exchange (during 2005–2022). Journal of Risk and Financial Management. 2024; 17(2):80. https://doi.org/10.3390/jrfm17020080

Chicago/Turabian StyleNeacșu, Mihaela, and Iuliana Eugenia Georgescu. 2024. "Analysing the Impact of Crises on Financial Performance: Empirical Insights from Tourism and Transport Companies Listed on the Bucharest Stock Exchange (during 2005–2022)" Journal of Risk and Financial Management 17, no. 2: 80. https://doi.org/10.3390/jrfm17020080