Tax Compliance in Slovenia: An Empirical Assessment of Tax Knowledge and Fairness Perception

1

Faculty of Economics and Business, University of Maribor, 2000 Maribor, Slovenia

2

Faculty of Economics and Business, University of Zagreb, 10000 Zagreb, Croatia

*

Author to whom correspondence should be addressed.

J. Risk Financial Manag. 2024, 17(3), 89; https://doi.org/10.3390/jrfm17030089

Submission received: 11 January 2024

/

Revised: 12 February 2024

/

Accepted: 15 February 2024

/

Published: 20 February 2024

(This article belongs to the Special Issue Sustainable Tax and Accounting Reporting in Building a New Tax Culture)

Abstract

:Complex tax systems can result in tax evasion, which further impacts the revenues necessary to achieve sustainable development goals. Enhancing taxpayer education, tax knowledge, and tax fairness perception is essential for boosting revenues to support societal sustainability. The aim of this study was to assess the levels of tax knowledge and tax fairness perception within the Slovene taxpayer population, with a specific focus on the differences related to gender and settlement size. Further, the connections between tax knowledge and various aspects of tax fairness were explored. The Kruskal–Wallis test was used to assess the statistical significance of gender and settlement size differences and the Kendall’s coefficient of rank to determine the association between the tax knowledge and fairness perception dimensions. The results provide evidence that highlights disparities in tax knowledge between male and female taxpayers (p-value = 0.0116). Additionally, this study demonstrates that settlement size does not significantly impact tax knowledge perception among Slovene taxpayers (p-value = 0.2067). However, tax fairness encompasses various dimensions, and our research reveals no disparities based on gender (p-value = 0.7263) or settlement size (p-value = 0.2786). When assessing the correlation between tax knowledge and tax fairness perception, the results indicate statistically significant but weak correlations in both directions, depending on the specific fairness dimension.

Keywords:

tax compliance; tax evasion; tax fairness; tax knowledge; gender; settlement size; Slovenia1. Introduction

Tax systems are complex and complicated, and taxpayers with limited or no prior tax knowledge may struggle to grasp their tax obligations. This can result in unintentional or intentional non-compliance (Carley et al. 2010), leading to the loss of entitled benefits and reduced state revenues, particularly affecting the most vulnerable in society. A valuable tool for helping raise the tax revenues necessary to achieve sustainable development goals is improving taxpayer education, their tax knowledge (OECD 2015, 2021), and the equality of the tax systems (OECD 2022). This approach aims to achieve higher tax compliance, involving the concept of “reciprocity”, which encompasses both the “public goods provided by the state” and the perception of fairness within the tax system (Saad 2010, 2014).

Tax education has been a key component of the OECD’s priorities (as indicated in the 2015 and 2021 surveys). To build a new tax culture centered on a “culture of tax compliance” means educating taxpayers to perceive tax payments as an integral part of their relationship with the government, built upon rights and responsibilities (OECD 2021). Tax education plays a critical role in promoting voluntary tax compliance, enhancing taxpayer understanding of the tax system, improving their perceptions of the tax system’s fairness, and building trust in tax authorities, leading to more effective compliance and enforcement (Mukhlis et al. 2015; Gunaasih 2022; Kumi and Kwasi 2023). Merely informing taxpayers about their tax obligations falls short (Moore 2019; Craig and Slemrod 2022). Therefore, new communication strategies via social networks and social media are becoming important (Juliobenedrick et al. 2023; Puklavec et al. 2023), even in raising tax compliance awareness.

The potential for a gap in public tax knowledge exists alongside the financial tax gap, which represents the disparity between budgeted and actual government tax revenues and is a substantial concern from a social justice standpoint and in the public interest (Edgley and Holland 2021). Increasing levels of financial and tax literacy could yield a dual benefit: not only would enhanced financial and tax literacy positively affect tax morale, but this impact might be amplified through the influence of fairness (Phyllis and Balavac-Orlic 2022). Higher education levels lead to increased tax knowledge (Kumi and Kwasi 2023; Gunaasih 2022; Fauziati et al. 2016; Saad 2014; Eriksen and Fallan 1996). Conversely, low levels of tax knowledge have been linked to negative attitudes toward tax payment (Inasius 2019a, 2019b; Ali and Ahmad 2014; Lewis 1982). Tax knowledge exhibits a positive correlation with tax compliance (Mukhlis et al. 2015). The level of knowledge is important in the way people comprehend the reality underlying taxation and the associated attitude toward taxation that is expressed (Eriksen and Fallan 1996). A solid understanding of taxation is essential for boosting tax awareness (Palil 2010) as higher tax knowledge leads to higher tax compliance and poor tax knowledge leads to higher tax non-compliance (Kirchler et al. 2008). Tax knowledge is important as it can significantly change attitudes toward the fairness of the tax system (Fallan 1999). Prior studies tend to focus on the effect of tax knowledge on the overall fairness of the tax system, even though there is evidence that fairness is a multi-dimensional construct of general, exchange, horizontal, vertical, retributive, personal, and administrative fairness (Saad 2010; Gilligan and Richardson 2005). The prevailing theory in the tax compliance literature suggests that taxpayers’ perceived fairness in the tax system enhances their trust in the government, exerting a positive influence on compliance (Jimenez and Iyer 2016). If taxpayers perceive fairness and equity in taxation, they tend to be more compliant; conversely, when they believe they do not receive any benefits, they are more inclined to engage in tax evasion (Amin et al. 2022). Perceptions of the tax fairness dimensions might vary between countries (Saad 2012). Tax education positively impacts tax knowledge, which, in turn, influences tax fairness positively, and this significantly contributes to tax compliance (Mukhlis et al. 2013, 2015). Insufficient tax knowledge (Inasius 2019a, 2019b) stands as a significant challenge for numerous tax authorities, knowing that taxpayer education is linked to local economic, social, and cultural realities. There are many factors linked to tax knowledge and the perception of tax fairness. Although authors highlight economic, psychological, and socio-demographic factors in tax compliance, research on the gender and settlement size impact on taxpayers’ tax knowledge and tax fairness perception is limited (Saad 2010, 2012; Mohamad et al. 2013). Gender differences are driven by various mechanisms, including income disparities, occupational disparities, family responsibilities, tax knowledge and financial literacy, legal and regulatory factors, risk aversion, enforcement and penalties, social and cultural norms, and access to resources (Coelho et al. 2022). Fallan (1999) identified a higher level of tax literacy among males, while Formanova et al. (2021) could not find a gender effect on the level of tax literacy. The results are mixed and country-specific. Besides gender differences, Williams (2020) argues that on the European level, taxpayers in villages and rural areas are more likely to be non-compliant. Altering the tolerance for tax non-compliance can be achieved through educational efforts and awareness-raising campaigns.

Each country possesses distinctive cultural, social, economic, and legal characteristics (Singh et al. 2023); it is expected that these contexts shape taxpayers’ perceptions, behaviors, and tax compliance differently by geographic area. Citizens in the EU and OECD countries possess some of the highest education levels globally (Dayioğlu Erul 2020). Therefore, they may use their advanced education and knowledge to exploit legal loopholes for non-compliance. Alternatively, they might choose to relocate their investments to countries with lower tax rates or less stringent audits, using their knowledge as a strategic advantage instead of emphasizing greater compliance (Dayioğlu Erul 2020). On the other hand, Vincent’s (2023) findings indicate that a lack of tax knowledge tends to worsen the negative impacts of sub-national taxing authority and discretionary control over tax authorities on tax compliance. A comparative analysis conducted by the European Commission (2019) on non-compliance among EU Member States (period 2001–2016) reveals that Slovenia is among the 14 Member States with the lowest estimated lost revenue regarding tax non-compliance (accounting for less than 5% of the EU-28 total). An additional integrative analysis on tax compliance by Surugiu et al. (2021) utilized unbalanced panel data for the European Union (EU28), including Slovenian data, covering the period from 2007 to 2017. This analysis demonstrated a positive and significant influence of the quality of the education system on tax compliance, similar to findings in studies by Dayioğlu Erul (2020) and Tilahun (2019). The design of tax policies in all Member States should always consider the gender gaps prevailing (Nerudova et al. 2019), and European institutions and Member States are required to analyze and assess tax policies concerning socioeconomic gender gaps (Gunnarsson et al. 2017). Slovenia belongs to the economy, being a member of the EU and OECD, a country with a high influence on international tax regulations and guidelines. According to the data from the Statistical Office of the Republic of Slovenia (SURS 2023), females have recently attained higher levels of education than males. Only 40 percent of individuals live in settlements larger than 5000, as Slovenia has many small settlements, with the majority residing in rural areas. Financial literacy is considered to be low according to internationally established criteria (UMAR 2023). Therefore, improving financial and other types of literacy, especially among adults, is among the priorities of the country (UMAR 2023).

Thus, recognizing the importance of tax knowledge and tax fairness on compliance, based on the presented literature and strategic documents of the EU and OECD, the first question that arises is whether tax knowledge perception depends on gender and settlement size. Secondly, do the dimensions of tax fairness perception differ based on gender and settlement size? And thirdly, what is the relationship between tax knowledge perception and tax fairness perception?

The aim of this study is to assess the level of tax knowledge perception and tax fairness perception among Slovene taxpayers, examining differences based on gender and settlement size. By examining Slovenian taxpayers, new insights into factors, such as tax knowledge and fairness perception within a specific region can be gained. The findings may offer valuable information for Slovenian policymakers to tailor tax educational policies as well as for other countries with similar social, political, and economic situations. As the empirical evidence in this study is limited to tax knowledge perceptions and tax fairness perceptions, it is expected that the results of this study will contribute to the literature on tax compliance behavior (tax compliance factors). This study generates additional evidence for the limited literature available on these aspects in Slovenia, especially by analyzing differences based on gender and settlement size. Further, the study proposes some educational initiatives based on the results to enhance existing taxpayer knowledge and awareness.

The findings of this study indicate disparities in perceived tax knowledge between male and female taxpayers. Furthermore, this research demonstrates that the size of one’s settlement does not notably affect the level of tax knowledge among Slovene taxpayers. The statistically significant relationship between tax knowledge and tax fairness perception was relatively weak in both directions, contingent on the particular dimension of fairness being considered. However, in order to better understand the relationship between gender and tax knowledge and settlement size and tax knowledge while controlling for relevant factors such as education, income, and marital status, a more comprehensive multivariate analysis based on data from an improved questionnaire and a stratified random sample should be conducted in future studies.

2. Literature Review and Theoretical Background

Becker (1968) and Allingham and Sandmo (1972) represent the first attempts to develop a framework for tax compliance behaviour. Their Economic Approach (Rational Choice Theory) involves taxpayers engaging in both tax evasion and tax avoidance. Taxpayers commonly undertake a cost-benefit analysis, assessing potential penalties and the tax loss they might face if their evasion is detected (Güzel et al. 2019). The Moral Sentiments The Planned Behaviour Theory, a concept within social psychology, explains individuals behavior through the examination of behavioral intentions influenced by attitudes toward three key components: the behavior itself, subjective norms, and perceived behavioral control (Sundari et al. 2022; Taing and Chang 2020). The Behavioural Approach, emphasizes that the behavior of taxpayers in complying with taxes is shaped by non-economic factors and not just by economic ones. The non-economic factors of tax compliance include trust, tax morality, perception of justice/fairness, beliefs, norms (personal and social), deterrence, and educational awareness.

This study investigated two non-economic factors of tax compliance, tax knowledge perception, and tax fairness perception. The educational level of taxpayers significantly influences their understanding of taxes, particularly with respect to tax laws and regulations. Tax knowledge helps taxpayers navigate declaration procedures effectively, accurately determine tax liabilities (Nguyen 2022). A prevailing agreement in tax compliance research highlights the important role of a fair tax system in shaping taxpayers’ compliance behavior (Taing and Chang 2020; Nguyen 2022; Inasius 2019a). Therefore, education on taxation has a positive impact on tax knowledge (Kumi and Kwasi 2023; Gunaasih 2022), leading to a positive influence on the perceptions of tax fairness, which in turn significantly contributes to enhanced tax compliance, Mukhlis et al. (2015).

2.1. Tax Knowledge

In the tax compliance literature, the term “tax knowledge” lacks a singular, universally accepted definition and is used in various contexts. Tax knowledge encompasses a broad spectrum of fiscal awareness, including general financial knowledge, awareness of tax evasion possibilities, overall educational background, and familiarity with tax laws (Devos 2016). According to Wong and Lo (2015), tax knowledge pertains to an individual’s assessment of their capability to adhere to tax regulations, including both technical expertise in taxation and a broader understanding of the tax system and compliance requirements. Tax knowledge is a fundamental component of a voluntary tax compliance system (Kasippilai 2000). Non-compliance with tax regulations may arise due to the taxpayer’s insufficient knowledge and skills to adhere to them (OECD 2019b). Udin (2015) considered tax knowledge as one of the crucial factors in determining taxpayers’ tax obligation correctly. Loo (2006) emphasized that in a self-assessment system, taxation knowledge stands out as the most influential factor in shaping taxpayer compliance behavior.

There are several types of knowledge, including implicit knowledge, explicit knowledge, empirical knowledge, and rationalism knowledge (Damajanti 2015). Saad (2014) determined two dimensions of tax knowledge: knowledge acquired through formal education and knowledge focused on potential tax evasion opportunities, while Bornman and Ramutumbu (2019) identify three categories of tax knowledge: general knowledge, procedural knowledge, and legal knowledge. There is limited research (Saad 2010; Mohamad et al. 2013) measuring next to general knowledge and also specific tax knowledge (legal and technical knowledge).

General tax knowledge for the individual means to understand the overall fiscal strategies of the government, i.e., to understand why taxes should be paid, to understand one’s personal financial situation, and to understand the influence of taxation on personal financial situation (Bornman and Ramutumbu 2019). Saad (2010) and Mohamad et al.’s (2013) idea is that general tax knowledge relates to a perceived idea of the tax system and its purpose.

Legal knowledge highlights individuals’ knowledge of regulatory aspects, including their obligations and responsibilities, rights, and consequences in the form of penalties for non-compliance (Saad 2010; Mohamad et al. 2013). Bornman and Ramutumbu (2019) suggested that legal knowledge can be divided into a conceptual understanding of tax legislation, which includes a high-level awareness of legislative terminology and the capacity to differentiate between various taxation concepts. Additionally, they proposed a technical understanding of tax legislation, which involves the capability to apply legal tax knowledge to one’s specific situation and ensure precise compliance with tax obligations (Bornman and Ramutumbu 2019). Taxpayers are feeling tax incompetent because of the complexity of the tax laws and because of that, they lose interest in the tax system (McKerchar 2001). The situation becomes notably demanding because tax laws are usually subject to frequent changes and are often too complex for the average person to understand, which is particularly true for many small business owners (Bornman and Ramutumbu 2019).

Technical knowledge pertains to individuals’ capability to fill out and submit their tax return form (Saad 2010; Mohamad et al. 2013). In some research, it is also defined as procedural knowledge, which refers to understanding the process and timing for submitting a tax return. According to Oladipupo and Obazee (2016), procedural knowledge encompasses several key elements. These include understanding the rationale behind the current structure and administration of the tax system, familiarity with tax requirements, particularly in relation to registration and filing obligations, and awareness of diverse compliance measures (Oladipupo and Obazee 2016). Additionally, procedural knowledge involves a certain degree of consciousness and attentiveness regarding procedures and protocols associated with tax return filing, comprehension of the processes and obligations involved in maintaining tax compliance, and the practice of timely, accurate, and comprehensive record-keeping for the completion and submission of tax returns and relevant documents (Oladipupo and Obazee 2016). Bornman and Ramutumbu (2019) proposed that procedural tax knowledge can be delineated into two key components: interacting with tax authorities and maintaining essential records for tax-related purposes.

In the existing literature, most studies examined the relationship between tax knowledge and tax compliance. The results of these studies are mixed, from the confirmation of existing correlation between tax knowledge and tax compliance, where taxpayers’ decisions regarding tax compliance are largely influenced by their tax knowledge (Hofmann et al. 2008; Azmi et al. 2016; Maqsudi et al. 2021; Remali and Jalil 2021; Remali et al. 2018), to non-existing correlation (Nicoleta 2011; Ghani et al. 2020). According to Hofmann et al. (2008), tax knowledge is a fundamental factor that affects tax compliance. In the context of individual taxpayers’ attitudes, having a solid understanding of tax laws is crucial, and there is a notable positive correlation between tax knowledge and the level of tax compliance (Azmi et al. 2016). Maqsudi et al. (2021) also found that taxpayer knowledge directly and positively influences taxpayer compliance. Contrary to that, Nicoleta (2011) found that tax knowledge is negatively linked to tax compliance behavior and revealed that taxpayers with a higher level of tax knowledge were more capable of identifying discrepancies in the tax system and regulations, which, in turn, led to increased instances of tax non-compliance. Ghani et al. (2020) indicated that tax knowledge does not significantly impact tax compliance among self-employed individuals. According to Palil et al. (2013), individuals with sufficient tax knowledge can mitigate unintentional noncompliance. In other words, this implies that tax knowledge can enhance the degree of tax compliance. Remali and Jalil (2021) claimed that tax education can help undergraduate students enhance their tax compliance by positively influencing their perceptions of the tax system and ethical attitudes. Additionally, some authors have suggested that education is linked to knowledge and, in this way, search for connections with tax compliance (Putri and Venusita 2019; Natasha and Yustina 2020). However, they mostly did not find any significant partial influence, as general education is not always associated with an understanding of the tax system and specific tax knowledge. One of the goals of this study was to test the relationship between tax knowledge and two socio-demographic factors (gender and settlement size). As the first main hypothesis, which was further tested with two subhypotheses, we defined the following:

H1:

The level of tax knowledge differs significantly by gender and settlement size among taxpayers in Slovenia.

Stotsky (1996) and Gunnarsson et al. (2017) demonstrated that gender differences exist even in taxation (OECD 2022). Tax policies significantly influence the economic participation and overall well-being of both females and males. These policies play a crucial role in shaping gender outcomes by impacting disposable consumption, incomes, and wealth. Therefore, tax policies are instrumental in influencing the overall well-being of individuals across genders OECD (2022). Socioeconomic inequality between males and females derives from legal cultures and economic structures (Torgler and Schneider 2004). The division of labor plays a central role in shaping fundamental objectives and norms in society, introducing a gendered dimension to the distributive and allocative effects of tax laws and policies. Males traditionally earn more and are wealthier than females; they accumulate more wealth in capital income, property rights, and financial investments and are therefore more oriented toward entrepreneurship (OECD 2022). Females are clustered in lower-income groups and have higher poverty rates than males. Paid work favors males rather than females. While males’ labor is more valued publicly in the market, females tend to be more reproductive inside the private domain of the home (Gunnarsson et al. 2017).

Implicit and explicit gender bias exists in most tax systems around the world, and eliminating bias may increase equality within tax systems (Grown et al. 2022). Females and males can be deliberately treated differently due to favorable tax law provisions, regulations, and procedures (explicit gender bias) or because the tax system and taxes affect their well-being differently (implicit bias). The inefficiencies of any tax system must be continually tested. Even if females and males are taxed under the same tax law, the structure of the tax system can have different impacts on females versus males (Grown et al. 2022). Gender differences drive various mechanisms, shaping the gender perception of the tax system differently between males and females. Coelho et al. (2022) identified differences in labor supply, progressivity on pay gaps, and lower effective capital income taxation on the personal income tax burden gap as gender bias in taxation. It is evident that gender differences exist (OECD 2022; Stotsky 1996; Gunnarsson et al. 2017) due to interaction with economic or societal differences between males and females.

Several researchers have examined gender as a demographic variable (Lohse and Qari 2014; Amponsah and Adu 2017; D’Attoma et al. 2017), demonstrating that males are less compliant than females. Kastlunger et al. (2010) pointed out that gender needs to be examined with caution as it affects socialization and education. Natasha and Yustina (2020) and Formanova et al. (2021) could not find a gender effect on the level of tax knowledge or literacy, which does not align with Fallan’s (1999) conclusion that reportedly identified a higher level of tax literacy among males. A sizable gender gap in financial knowledge was identified by Yao et al. (2023). Although gender-sensitive tax laws are essential, they cannot attain gender equality. However, Fallan’s (1999) study unveiled a non-significant result that gender does not possess predictive power in this context.

When explaining the reasons for the gender gap in tax knowledge, we can follow the findings of Yao et al. (2023), who identified some key factors for explaining a possible gender gap in financial knowledge. These mechanisms can be assumed to also apply to the gap in tax knowledge.

Gender differences depend on the complex interactions between specific family contexts and the socialization of gender roles, i.e., the family financial socialization process. In this process, norms, values, standards, attitudes, knowledge, and behaviors are acquired, contributing to the well-being of the individual and financial viability (Yao et al. 2023; Danes 1994). The socialization processes positively correlate with individuals’ subjective self-evaluated knowledge and objective knowledge (Zhu 2018; Deenanath et al. 2019). Previous research (LeBaron and Kelley 2020) on traditional gender roles depicts males as the breadwinners, financially responsible, and females as the caregivers, highlighting differences in parenting. Male children tend to receive more experiences in information about financial matters compared to female children (Yao et al. 2023).

Another particularly important source identified for acquiring financial knowledge is formal (informal) financial education. Prior research has found positive causal effects (Kaiser et al. 2021) of education programs on knowledge and financial behaviors, favoring females. Even after taking formal courses (Danes and Haberman 2007; Danes and Brewton 2014), females gained more knowledge. Yao et al.’s (2023) investigation confirmed that, in comparison to family socialization, financial experiences beyond the family, such as education, play significantly more substantial roles in influencing the gender gap in financial knowledge among males and females. Eriksen and Fallan (1996) found that females and males learn tax knowledge differently; there are unique learning patterns, as reported by Fallan (1999). Coelho et al. (2022) observed that gender differences are driven by various mechanisms, including income disparities, occupational disparities, family responsibilities, tax knowledge and financial literacy, legal and regulatory factors, risk aversion, enforcement and penalties, social and cultural norms, and access to resources. As Formanova et al. (2021) could not find a gender effect on the level of tax literacy, which does not align with Fallan’s (1999) conclusion that reportedly identified a higher level of tax literacy among males, the mix result needs additional testing country-specific.

We believe that (tax) cultural, social norms, and (tax) values, as well as society expectation regarding responsibility, may influence the level of type and engagement in acquiring tax knowledge by gender differently. Other potential reasons for variations in tax knowledge by gender could derive from historical gender roles, due to unequal access to education—educational disparities, unequal access to financial resources and opportunities for financial decision-making, and occupational segregation. The scope of this research is limited to the subjective perception of tax knowledge based on self-evaluated knowledge, focusing on general knowledge, legal knowledge, and technical knowledge. If our study confirms gender differences in tax knowledge, further detailed research should be conducted, testing, for example, effective knowledge and the possible mechanisms driving gender differences. Building on the previous literature, the current study seeks to examine the following subhypothesis:

H1a:

The level of tax knowledge differs significantly between male and female taxpayers in Slovenia.

When examining the differences by settlement type between rural and urban areas, there seems to have been a shift over time, with a smaller percentage of tax non-compliance observed in rural areas and an increase in non-compliance rates in small or medium-sized towns (Williams 2020). Although there were no significant differences between urban and rural residents in their likelihood of engaging in tax non-compliance in 2007 and 2013, by 2019, those living in large urban areas were significantly less likely to be non-compliant compared to those in rural areas or villages (Williams 2020). Therefore, Williams (2020) argues that at the European level, taxpayers in villages and rural areas are more likely to be non-compliant. Altering the tolerance for tax non-compliance can be achieved through educational efforts and awareness-raising campaigns, e.g., higher tax knowledge. There are few other studies measuring the impact of a taxpayer’s settlement size (rural or urban area) on their compliance, with some empirical evidence supporting the influence of the area variable for businesses on tax compliance (Dissanayake and Premaratna 2020; Williams 2020).

There could be several reasons why differences might be expected based on settlement size. Significant disparities in rural areas, both in OECD and non-OECD countries, exist primarily in terms of mobility, the accessibility of public transport, the adoption of new information, and communication technologies, as well as the availability of sufficient and high-quality resources for education and training (OECD 2006, 2019a). Wood (2023) identifies the following reasons for differences in knowledge between urban and rural areas. First, the availability of resources, such as well-equipped educational institutions, favors urban areas, making it challenging for rural areas, which often lack these resources. Consequently, access to specific and high-quality education in taxation, as well as highly qualified educators, is difficult (Wood 2023). Due to the distance and limited access to formal educational institutions in rural areas, access to specific knowledge is restricted, and local knowledge needs to be disseminated through others, such as online communication channels, for which the infrastructure is not always adapted (Wood 2023). Among the most significant factors in knowledge dissemination are communication networks, which are more crucial for spreading specific tax knowledge in rural areas as well as transport and access to services (Pateman 2011). Due to the distance and limited access to formal educational institutions in rural areas, access to specific knowledge is restricted, and local knowledge needs to be disseminated through others, such as online communication channels, for which the infrastructure is not always adapted. Access to technology, facilitating online resources and tools for learning about tax matters, is not equal. There are more economic activities in urban areas than in rural areas. Urban areas have more robust government services, including tax-related education and assistance, compared to urban areas. Second, socio-economic factors, especially income levels, are higher in urban areas, and this significantly influences educational, that is, knowledge differences (Wood 2023). Rural individuals are found to have lower financial (i.e., tax) literacy levels than their urban individuals, and a possible explanation could be found in several socio-economic and demographic variables, such as age, income level, marital status, and employment status (Mckenzie 2022).

This study examines the existence of the differences between rural and urban taxpayers in tax knowledge perception but does not investigate the mechanisms and reasons behind them, which could be the subject of future research. The subhypothesis states the following:

H1b:

The level of tax knowledge differs significantly between rural taxpayers and urban taxpayers in Slovenia.

2.2. Tax Fairness

Social psychologists discovered that tax compliance is affected by the taxpayers’ perceptions of fairness and unfairness (Tyler 1997). Psychological elements, including attitudes, norms, and the perceived fairness of the tax system, hold equal significance as economic factors in enhancing taxpayer compliance (Kirchler 2007). In general, research examining the impact of fairness consistently reveals that “taxpayers are less inclined to adhere to a tax system they perceive as unjust, inequitable, and therefore lacking legitimacy” (Wenzel 2002). Kirchler et al. (2008) proposed in a slippery-slope framework that taxpayer compliance relies on a combination of economic and non-economic factors. Taxpayers adhere to tax compliance either out of fear of the tax authorities or due to a sense of obligation. The dimension of fear pertains to the perceived authority’s power and the enforced compliance, including economic factors like audit rates and penalties. The sense of obligation, on the other hand, is associated with trust in the tax authorities and voluntary compliance, including non-economic factors such as norms, attitudes, and the perceived fairness of the tax system. The literature on tax morale has revealed that, in addition to deterrence mechanisms (Kirchler 2007; Alm 2019), the social and institutional context in which individuals engage with one another can have a substantial impact on their tax morale (Bergolo et al. 2020).

According to Kassa (2021), tax fairness is defined as the equity in tax collection procedures, principles, and execution, and when the tax collection process lacks fairness, it can lead to unethical practices. Tax fairness is a topic of debate, contention, and controversy since all taxpayers do not pay taxes using the same tax rates (Abate 2019). Fairness is linked to the perception of a harmonious balance between taxes paid and the benefits of public goods received. Despite the extensive discussion about individual motivations for tax compliance, the political economy literature still provides limited consideration to the impact of individual attitudes regarding fairness and wealth redistribution on tax morale (Castañeda 2023).

Previous research indicates the importance of fairness in taxation (Gobena and Van Dijke 2017; Niesiobędzka and Kołodziej 2020). Fairness could be observed from many different aspects, and therefore, there are many understandings of this concept (Sikayu et al. 2022). When taxpayers believe that the existing tax processes and procedures are unjust toward them, they might be hesitant to collaborate with tax audit officials (Kirchler et al. 2008). Individuals who are more sensitive to fairness are less inclined to view tax payment as a civic duty and more inclined to rationalize tax evasion (Castañeda 2023). Tax evasion is more likely to happen among taxpayers who perceive the tax system as unfair, leading them to exhibit non-compliance with their tax obligations (Sing and Bidin 2020). Tax fairness is a non-economic determinant of tax evasion and represents a significant factor influencing taxpayer behavior (Alm et al. 2017).

Ullah et al. (2018) find that most of the survey participants (individual taxpayers in Pakistan) believe that transparency and fairness within the system would directly contribute to an increase in tax revenue. Chan et al. (2000) discovered that when taxpayers believe that the government does not allocate tax revenue fairly, it leads to a perception of tax unfairness. Saad (2010) found that taxpayers considered the current income tax system fair, but there was no proof that this perception significantly affected their compliance behavior. Additionally, Saad (2010) found that fairness perceptions were influenced by tax knowledge and tax complexity, while Mohamad et al. (2013) indicated a significant difference in tax knowledge and fairness perception between accounting and non-accounting students.

There are various classifications of the dimensions and sub-dimensions of fairness in the literature and ways defined by the authors (Gerbing 1988; Azmi and Perumal 2008; Farrar et al. 2020). Based on previous research (Hartner et al. 2008; Van Dijke and Verboon 2010; Wenzel 2002; Farrar et al. 2020, 2022), Saad (2010) suggested ten dimensions of fairness, but in her study, seven dimensions were identified to be important in assessing the fairness of the income tax system: general fairness, exchange fairness, vertical fairness, horizontal fairness, personal fairness, retributive fairness, and administrative fairness. General fairness assesses individuals’ opinions regarding the overall fairness of the (income) tax system (Saad 2010). Exchange fairness focuses on the fairness in the relationship between the benefits received from public goods and services provided by the government and the tax burden placed on taxpayers (Bayram et al. 2017). Personal fairness pertains to an individual’s self-interest, whereas administrative fairness encompasses both the content of tax law (policy fairness) and the procedures followed by the tax authority (procedural fairness) (Saad 2010). Vertical equity is a judgment regarding the appropriate tax burden for taxpayers with varying abilities to pay while horizontal equity is a judgment that taxpayers with equal ability to pay should be subjected to the same taxation (Susilawati 2022). In other words, horizontal fairness pertains to the equitable distribution of benefits and costs among individuals within the same group, while vertical fairness concerns the allocation of benefits and costs among individuals who are not of equal standing (Bayram et al. 2017). In the context of tax behavior, some have authors categorized fairness as distributive, procedural, and retributive justice (Comunale et al. 2019). Among the principles of justice, distributive justice and procedural justice are given the most attention (Druckman 2020). Distributive justice concerns the fairness of the decision’s outcome, while procedural justice pertains to the fairness of the decision-making process (Druckman and Wagner 2016). Distributive justice refers to the equity of outcomes in resource allocation or distribution and boasts the longest history of research in social psychology (Wenzel 2003). The primary four principles of distributive justice include equality, proportionality, compensation, and need (Druckman and Wagner 2016). Another categorization of distributive fairness can be horizontal fairness, vertical fairness, or fairness in exchanges with the government (Bayram et al. 2017).

Wenzel (2003) observed distributive, procedural, and redistributive justice in tax research on the societal, group, and individual levels. The individual level of analysis of distributive justice in tax research includes analysis of personal tax burdens, personal benefits, and personal options related to tax evasion compared to others, other times, or relative income. Procedural justice encompasses the consideration of the process (Druckman 2020) and includes analysis of holding regard for everyone’s dignity and maintaining consistency compared to others, expression, authority, process and decision control, information and explanation, effectiveness, and balancing service quality against expenses incurred by the individual (Wenzel 2003). It offers a way to assess individuals’ perceptions regarding the legitimacy of an authority and their compliance with the rules and decisions established by that authority (Hoong Voon et al. 2023). Redistributive justice includes an analysis of the appropriateness of a penalty for individuals (penalties) and inflexibility or lack of consideration in the audit process for individual cases (audits) (Wenzel 2003).

Incorporating gender considerations is important across all tiers of research, policy development, and advocacy in the realm of tax fairness/justice; overlooking this dimension implies forfeiting the chance to achieve an equitable tax system (Christain Aid 2014). Even if explicit and implicit gender biases do not exist in a tax system, implementing a gender-based tax system may face challenges in achieving high compliance, as it can still be perceived as unfair by taxpayers. Therefore, when designing tax systems and tax policies and considering the gender gaps (Nerudova et al. 2019), these should not be overlooked. The reason why tax fairness perception differs might be also found in the non-uniform distribution of tax preferences in society, which varies depending on the urbanization rate (Andersson 2017). This study limited the research to all dimensions of fairness defined by Saad (2010, 2012), who confirmed positive perceptions of personal, vertical, and administrative fairness. However, for exchange, horizontal, and retributive fairness perceptions, the results were mixed. Fairness perception by dimensions can differ among different groups, as Mohamad et al. (2013) revealed in their research on accounting and non-accounting students. Measuring perceptions on all dimensions of fairness by gender and settlement size was identified as a literature gap. Therefore, as the second main hypothesis, which was further tested with two subhypotheses, we defined the following:

H2:

The level of tax fairness differs significantly by gender and settlement size among taxpayers in Slovenia.

In addition to the gender arguments already stated under subhypothesis one, why expect gender differences in tax knowledge, we believe that the same mechanisms apply to tax fairness. Gender differences in the perception of tax fairness are anticipated because females often earn lower incomes, enter and exit the labor market at different life stages, and contribute significantly to unpaid labor and caregiving responsibilities at home, in family businesses, and within the community (Nerudova et al. 2019; Hundsdoerfer and Eva 2020). These variations also arise from the prevailing gender roles in society (Christain Aid 2014). Altering female and male awareness with improved tax knowledge raises perceptions of the fairness of the tax system (Fallan 1999). Research has confirmed gender disparities in perceptions of fairness concerning distributive and procedural justice (Hundsdoerfer and Eva 2020) and in redistributive fairness (Nerudova et al. 2019). Male participants are particularly responsive to procedural justice violations in their fairness perceptions, while female participants tend to adjust their fairness perceptions based on the outcomes of the tax allocation procedure (Hundsdoerfer and Eva 2020). To test whether gender differences exist in different dimensions of tax fairness, the subhypothesis was as follows:

H2a:

The level of tax fairness differs significantly between male and female taxpayers in Slovenia.

Disparities between urban and rural areas can impact individuals’ perspectives on taxes (Mohammed and Tangl 2024). The literature explains that these disparities may arise from actual differences in taxation between urban and rural areas in terms of paying different types of taxes and receiving tax exemptions and allowances that some are entitled to while others are not (Beck et al. 2016), affecting both vertical and horizontal fairness. We expect that the tax fairness perception between urban and rural areas will be different due to differences in economic, social, and cultural conditions, as well as the varying needs and expectations of individuals in both types of areas. Access to services and infrastructure, as well as access to tax education and specific tax knowledge, can influence the perception of tax fairness in these different environments. Therefore, to examine the dimensions of tax fairness perception based on settlement size, the following subhypothesis was formulated:

H2b:

The level of tax fairness differs significantly between rural and urban taxpayers in Slovenia.

The perception of the fairness of the tax system can be improved by raising tax knowledge (Fallan 1999). These findings are inconsistent with Chucks and Azaka’s (2023) conclusion, which states that the level of tax knowledge does not influence individuals’ perception of tax fairness. Contrary to this, Saad (2010) confirmed a positively oriented relationship between tax knowledge and fairness dimensions and concluded that, in general, tax knowledge had varying effects on fairness perceptions, except for horizontal fairness (Saad 2010, 2014). Specifically, technical knowledge was found to significantly influence vertical fairness, retributive fairness, and personal fairness, while legal knowledge was only significant in shaping taxpayers’ perceptions of retributive fairness (Saad 2010). The results in the literature are mixed. Based on these findings, we further tested the third hypothesis:

H3:

Tax knowledge positively influences the dimensions of fairness perception of Slovene taxpayers.

3. Materials and Methods

In the conducted survey, the respondents were Slovene taxpayers who provided answers to a long range of questions related to the tax topic. For most respondents, the tax topic tends to be a sensitive topic. Therefore, in order to select respondents and further recruit them, the snowball sampling approach was used (a non-probability sampling technique).

Snowball sampling is a non-probability sampling technique used in social sciences to select respondents from populations that may be marginalized, hidden, or hard to identify with traditional sampling methods. The snowball sampling starts with a small group of respondents who provide information about other possible respondents. These respondents are then asked to participate in the survey and to recommend other potential respondents with specific characteristics. The process continues until there are no more recommendations or the planned sample size is reached.

Snowball sampling can be employed when studying attitudes toward sensitive topics like tax payments or opinions about the tax system. However, it is crucial to emphasize that snowball sampling could introduce bias into the survey results. Specifically, respondents may recommend others who share similar characteristics and opinions with the existing respondents, leading to a non-representative sample. Therefore, the results obtained through snowball sampling should be interpreted and observed carefully, with the main focus on the characteristics of the observed respondents.

In the survey, which was carried out from March to May 2023, 390 respondents who completed the questionnaire participated. The survey included in-depth and detailed questions related to the taxpayers’ attitude toward the tax system in Slovenia.

Table 1 shows a list of the selected variables from the questionnaire, the key variables for conducting the analysis. Overall, 30 items were adopted from previous studies. Items measuring tax knowledge (GK1, LK1, LK2, LK3, TK1, TK2, and TK3) from Mohamad et al. (2013) and Saad (2010), items measuring tax fairness (GF1, GF2, GF3, GF4, GF5, HF1, EF1, VF2, and RF1) from Mohamad et al. (2013), and items measuring personal (PF1–PF9) and administrative fairness (AF1, AF2) from Braithwaite et al. (2001) were included, while 12 items (marked as “overall”) are introduced by calculating the averages of subdimension variables for the purpose of further analyzing the results.

While the survey questions were based on previous research studies, additional steps were taken to validate the survey questionnaire. Initially, the content of the survey questionnaire was validated, ensuring that all relevant aspects of the observed topic were appropriately measured and covered. Furthermore, some questions were slightly modified to enhance their clarity. Pilot testing was carried out with a small sample of respondents, and suggestions for improving the questionnaire were duly considered. Additionally, the data collection process was closely monitored to promptly address any unexpected issues that may have arisen.

Those 30 observed variables, listed in Table 1, belong to the 5-point Likert scale type of question, with the answer range from 1 (strong disagreement) to 5 (strong agreement). The variables were grouped according to their main dimensions, tax knowledge, and fairness perceptions. Inside those dimensions, variables were grouped further according to their following subdimensions. There are three tax knowledge subdimensions introduced: general knowledge, legal knowledge, and technical knowledge. The definitions and understanding of those items are provided by Saad (2010), and Mohamad et al. (2013). In the dimension of fairness perception, seven subdimensions were defined as follows: general fairness, exchange fairness, horizontal fairness, vertical fairness, retributive fairness, personal fairness, and administrative fairness. The definitions and understanding of those items are provided by Saad (2010) and Braithwaite et al. (2001) are presented in Appendix A. An additional 12 variables were introduced by calculating the averages of subdimension variables. Values from the variable legal knowledge (LK) were calculated as averages of variables LK1, LK2, and LK3 for each respondent separately. The tax knowledge (TAXK) variable was calculated as an average of variables GK, LK, and TK, which present the three subdimensions under the tax knowledge dimension. Similarly, the variable fairness perceptions (FAIRP) was estimated by considering seven fairness perceptions subdimensions: GF, EF, HF, VF, RF, PF, and AF. The analysis of the data was conducted using Microsoft Excel, R 4.3.0, and RStudio 2023.06.1+524. The data editing was conducted using Microsoft Excel, whereas the statistical analyses were performed in RStudio.

The analysis was conducted as follows: In the first step, the structure of the respondents according to their main demographic characteristics was observed. That was first performed on the overall level, and after that, it was according to the respondents’ gender and the respondents’ settlement type in which they live. The separate view of respondents according to their gender (H1a) and settlement type (H1b) is important. Research hypothesis H1a states that the level of tax knowledge differs significantly between females and males and H1b between rural taxpayers and urban taxpayers, respectively. To inspect whether those differences are statistically significant or not, the Kruskal–Wallis test was applied. The Kruskall–Wallis test (Kruskal–Wallis rank sum test) is a rank-based nonparametric test in which at the null hypothesis it is assumed that there are no statistically significant differences between two or more groups, whereas at the alternative hypothesis it is assumed that there is at least one group statistically different from the others. The test statistic is equal to the following:

where is the total number of observations in all groups, is the number of groups, is the observations’ number in the -th group, is the rank of the -th observation from the -th group, is the average rank of all observations in the -th group, and is the average rank of all observations (Kruskal and Allen 1952; Dunn 1964). The Kruskal–Wallis test is appropriate since the observed data are assumed not to follow a normal distribution, a consequence of using the Likert scale with only five answer options. Additionally, two independent groups were observed (males vs. females and respondents from rural vs. urban settlements). The preliminary analysis indicates similar distributions in each group in terms of the shape and spread. However, a significant Kruskal–Wallis test will not indicate a difference in medians but the presence of a statistically significant difference between the groups, ensuring comparability for different variables. Finally, the large total sample size ensures that each group sample has more than 20 observations (Zar 2010). The Kruskal–Wallis test will be applied to inspect research hypothesis H2 (the level of tax fairness differs significantly between females and males (H2a), and between rural taxpayers and urban taxpayers respectively (H2b) as well. Finally, to investigate research hypothesis H3, tax knowledge positively influences the dimensions of fairness perception of Slovene taxpayers, the Kendall’s coefficient of rank is used to determine the association between the tax knowledge with seven fairness perception dimensions. The Kendall’s coefficient of rank is suitable for use when observing the association between ordinal variables measured on the Likert scale. To make appropriate adjustments for ties, Kendall’s Tau-b statistic is used in the analysis (Agresti 2010):

where is the number of concordant pairs, is the number of discordant pairs, , , is the number of tied values in the -th group of ties for the first variable, , and is the number of tied values in the -th group of ties for the second variable. Kendall’s Tau-b statistic ranges from −1 to 1, where −1 indicates a perfect negative association, while a value of 1 indicates a perfect positive association. If Kendall’s Tau-b statistic equals 1, this would imply that there is no association between the two observed variables. It has been demonstrated that Kendall’s Tau-b statistic is robust against outliers. Additionally, Kendall’s Tau-b statistic is often employed in cases where the observed variables are not normally distributed.

4. Results

4.1. Demographic Structure of Respondents

In Table 2, the structure of all 390 respondents, according to their main demographic characteristics, is given. The share of respondents was calculated by taking the ratio of the number of respondents in a certain category to the total number of respondents (n = 390) and multiplying the result by 100.

In the survey, 52% females and 48% males participated. Most respondents have a vocational secondary education (42%), and most respondents have a gross income in the range from EUR 1001 to 2000 (50%). The vast majority of respondents have stated that they are Christians (73%). Where a marital status is observed, 41% of respondents are married, whereas 37% of the respondents are in domestic partnership or cohabiting. According to the settlement type in which they live, 60% of respondents are from a rural settlement, whereas 40% of respondents are from an urban settlement. In this research, rural settlements are considered to have 3000 or fewer inhabitants. On the other hand, rural settlements are those with more than 3000 inhabitants. The structure of the respondents’ demographic characteristics according to gender is provided in Table 3.

The share of female respondents was calculated by taking the ratio of the number of female respondents in a certain category to the total number of female respondents (n = 203) and multiplying the result by 100. Similarly, the share of male respondents was calculated by taking the ratio of the number of male respondents in a certain category to the total number of male respondents (n = 187) and multiplying the result by 100. This approach allows for the comparison of distributions across different variables (education, gross income, religion, marital status, and type of settlement) between female and male respondents. The demographic characteristics of female and of male respondents are quite similar. However, it can be concluded that considerable differences are present if the education and the marital status of respondents are observed. There are more females with tertiary education or university degree than males (37% vs. 20%). On the other side, there are fewer females with vocational, secondary education than males (35% vs. 49%). There are also more married females than males (47% vs. 34%), but there are fewer single females than males (11% vs. 26%).

The structure of the respondents’ demographic characteristics according to the settlement type in which they live is given in Table 4.

The share of rural respondents was calculated by taking the ratio of the number of respondents living in rural settlements in a certain category to the total number of respondents living in rural settlements (n = 233) and multiplying the result by 100. Similarly, the share of urban respondents was calculated by taking the ratio of the number of respondents living in urban settlements in a certain category to the total number of respondents living in urban settlements (n = 157) and multiplying the result by 100. This approach allows for the comparison of distributions across different variables (gender, education, gross income, religion, and marital status) between respondents living in rural settlements and respondents living in urban settlements. The main differences between respondents who live in a rural or in urban settlement appear in variables such as education and religion. There are more respondents with vocational, secondary education from rural settlements than from urban settlements (47% vs. 34%), but there are fewer respondents from rural settlements with a tertiary education or university degree than from urban settlements (25% vs. 35%). There are more Christians in rural settlements than in urban settlements (78% vs. 66%). Respondents from urban settlements tend to be less religious than respondents from rural settlements (15% vs. 7%).

It has to be emphasized that the focus of the paper is to observe the differences between respondents based on gender (female vs. male) and type of settlement (rural vs. urban) in the areas of tax knowledge and fairness perception. Therefore, to better understand the structure of respondents according to these two main variables of interest, the distributions of respondents for different demographic variables are shown in Table 3 and Table 4. However, other demographic variables (education, gross income, religion, and marital status) will not be further analyzed as they are not the main focus of the paper’s research.

4.2. Tax Knowledge Differences by Gender and Settlement Size

In this chapter, tax knowledge level differences between females and males and between respondents from rural and urban settlements are investigated. Table 5 shows the average levels of tax knowledge variables for females, males, respondents from a rural settlement, and respondents from an urban settlement. The average levels were calculated as the means of all respondents belonging to specific groups (females, males, respondents from rural settlements, and respondents from urban settlements) for each tax knowledge variable separately. All tax knowledge variables are rated on a scale from one to five, where one indicates strong disagreement with the statement related to the tax knowledge variables, and five indicates strong agreement with the statement. The midpoint, value 3, in this context, signifies that a respondent neither disagrees nor agrees with the statement in the tax knowledge variable. Therefore, all calculated averages presented in Table 5 should be interpreted in the context of specific groups of respondents tending to agree or disagree with certain tax knowledge variables.

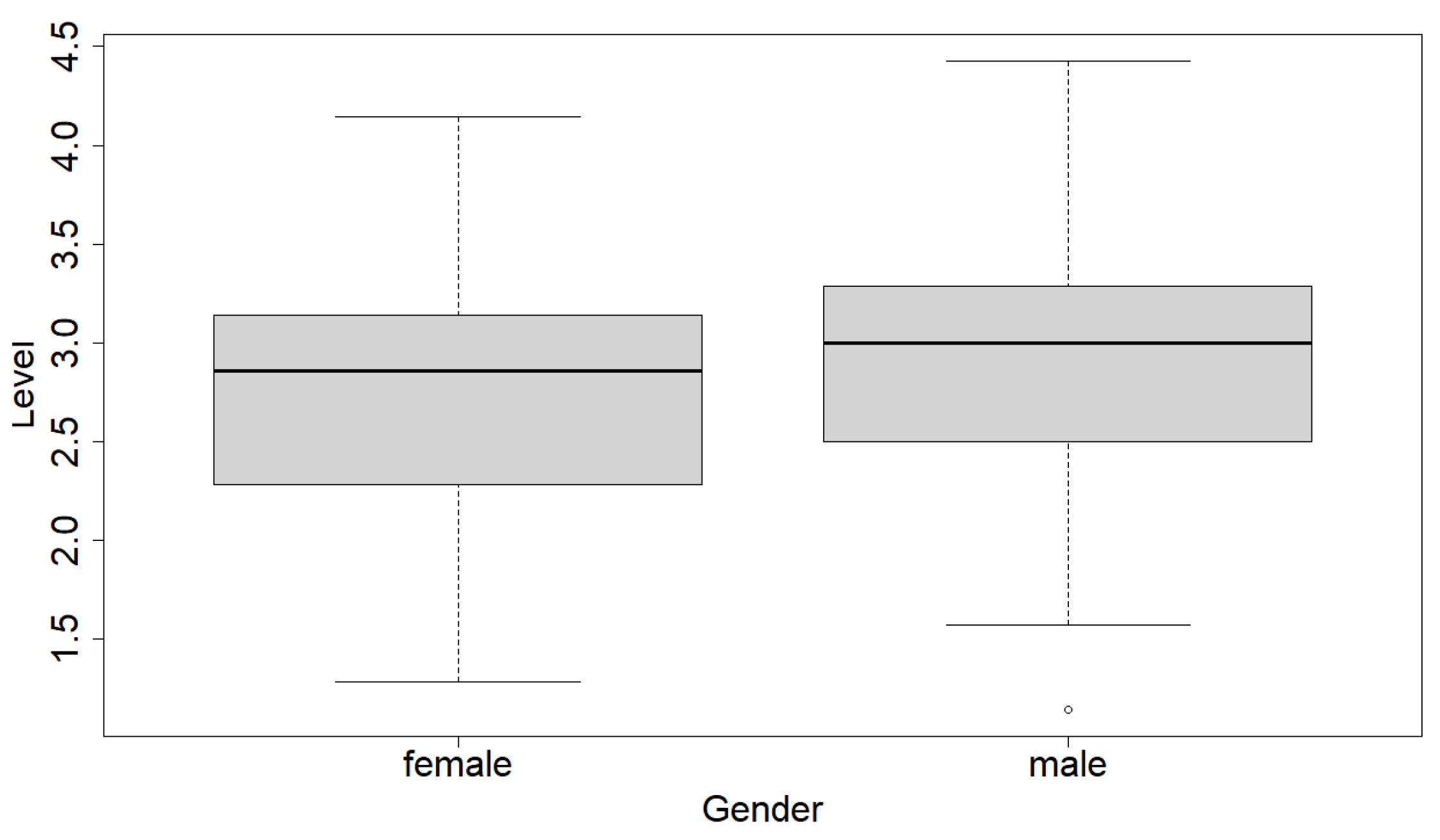

The highest average tax knowledge level for females is achieved at variable GK1 (3.33), whereas males have the highest average at variable TK1 (3.42). On the other hand, the lowest average tax knowledge level for both females (2.31) and males (2.58) was achieved at variable TK3. Respondents from a rural settlement have the highest average at variable GK1 (3.37) and the lowest average at variable TK3 (2.27). Respondents from an urban settlement have the highest average at variable TK1 (3.42) and the lowest average at variable LK3 (2.52). In Figure 1, box plots of variable tax knowledge (TAXK) according to gender are shown (Figure 1).

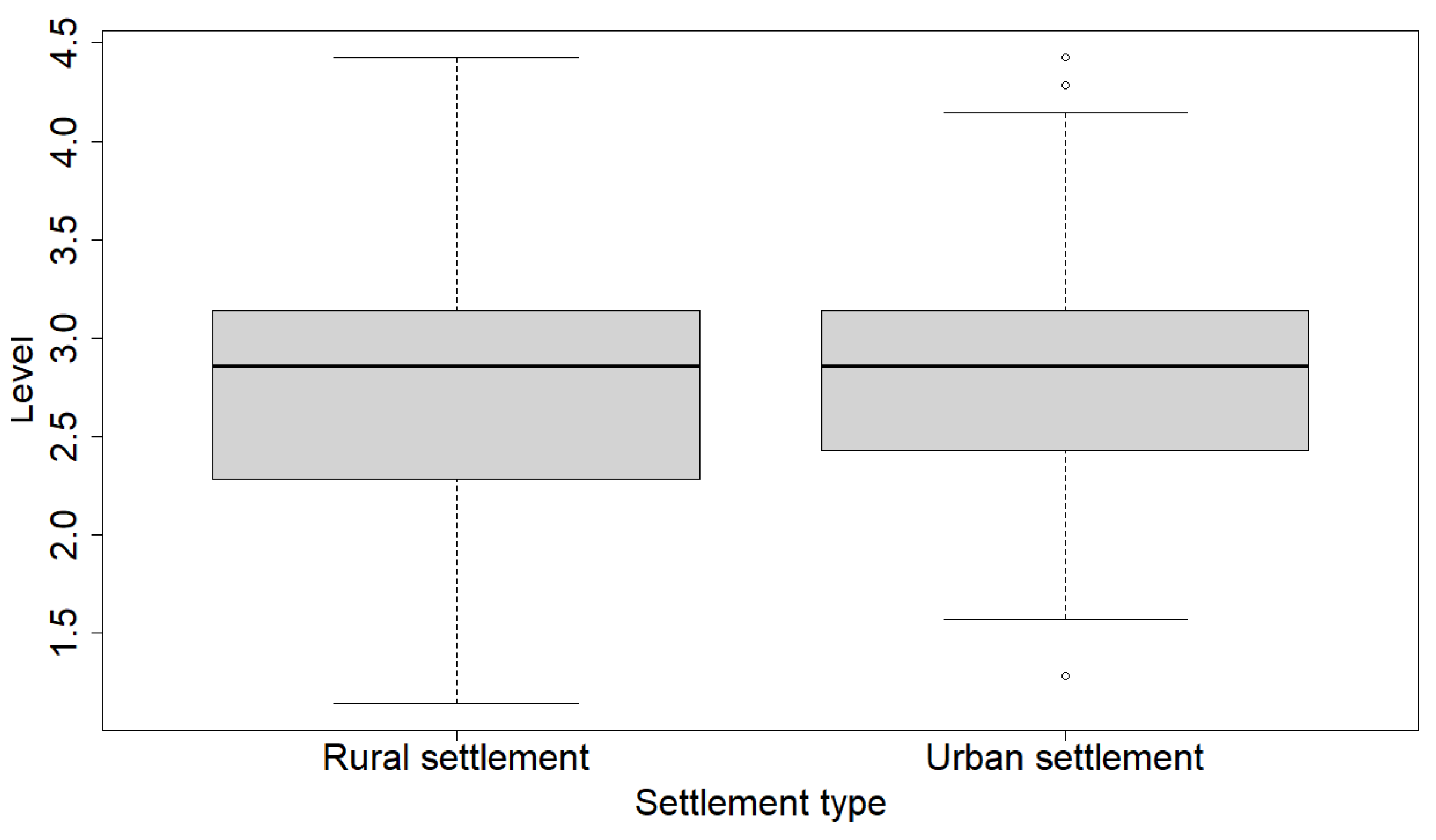

A box plot consists of a “box” that is delimited by the values of the first and third quartiles. Inside this box or between the first and third quartiles, the median value can be found. In addition to the quartiles, a box plot provides information about the minimum and maximum values. However, the presented box plots will also provide information about potential outliers. Data values that may be considered potential outliers are shown as circles in the box plots.

If those box plots are compared, it could be concluded that females have lower values of TAXK levels than males. Namely, all five key elements of a box plot—minimum, first quartile, median, third quartile, and maximum—are lower for females than for males for the observed variable. Similarly, in Figure 2 box plots of variable tax knowledge (TAXK) according to settlement type are provided.

It seems that the variability level of variable TAXK is larger at respondents from a rural settlement than at respondents from an urban settlement. This conclusion can be drawn by observing the data range (the difference between the maximum and the minimum) and the interquartile range (the difference between the third and the first quartile). On the other hand, the median values are at the same level for respondents who live in rural settlements and respondents who live in urban settlements (median = 2.86). It should be emphasized that the box plot analysis was presented only for the main variable under study, which is the variable TAXK, whereas the box plots for other tax knowledge dimensions are not shown.

Kruskal–Wallis rank sum test results, in which tax knowledge variables according to gender and settlement type are compared, are given in Table 6.

In Table 6, the test statistics of the conducted Kruskal–Wallis rank sum tests and their corresponding p-values are provided separately. If the p-value is lower than 0.05, it can be concluded that there is a statistically significant difference in the tax knowledge level for a certain tax knowledge variable between females and males when observed according to gender, or between respondents living in urban and rural settlements when observed according to settlement type variables.

According to the results, statistically significant differences, at the significance level of 0.05, between females and males regarding tax knowledge level appeared to be at variables TAXK (p-value = 0.0116), LK (p-value = 0.0316), LK2 (p-value = 0.0195), TK (p-value = 0.0227), and TK3 (p-value = 0.0369). So, the research subhypothesis H1a, that the level of tax knowledge differs significantly between females and males, can be accepted. However, the research subhypothesis H1b, that the level of tax knowledge differs significantly between rural taxpayers and urban taxpayers, cannot be accepted. Namely, there are statistically significant differences, at the significance level of 0.05, between respondents from a rural settlement and from an urban settlement at LK1 (p-value = 0.0425), TK (p-value = 0.0167), and TK3 (p-value = 0.0006) but not at variable TAXK (p-value = 0.2067).

4.3. Fairness Perception Differences by Gender and Settlement Size

Fairness perception levels have been separately observed for gender and settlement type. The average values throughout fairness perception variables are given in Table 7. The average levels were calculated as the means of all respondents belonging to specific groups (females, males, respondents from rural settlements, and respondents from urban settlements) for each fairness perception variable separately. Similar to the tax knowledge variables, the fairness perception variables are also rated on a scale from one to five with the same meaning of the values. Therefore, one indicates strong disagreement with the statement related to the fairness perception variables, the midpoint (value three) signifies that a respondent neither disagrees nor agrees with the statement, and five indicates strong agreement with the fairness perception statement. Therefore, all calculated averages provided in Table 7 should be interpreted as the levels of disagreement or agreement of specific groups of respondents with the fairness perception variables.

Both females and males have achieved the highest average value at variable VF1 with the same value of 3.95. The lowest average values for females and males have also been achieved at the same variables GF4 (female = 2.42; male = 2.64) and PF6 (female = 2.69; male = 2.63). If respondents are compared by the type of settlement in which they live it can be noticed that there are a lot of similarities present here as well. So, respondents from a rural settlement and respondents from an urban settlement have achieved the highest average value at variable VF1 (rural settlement = 4.01; urban settlement = 3.85). The lowest average values from both categories, respondents from a rural settlement and respondents from an urban settlement, were recorded at variable GF4 (rural settlement = 2.47; urban settlement = 2.60).

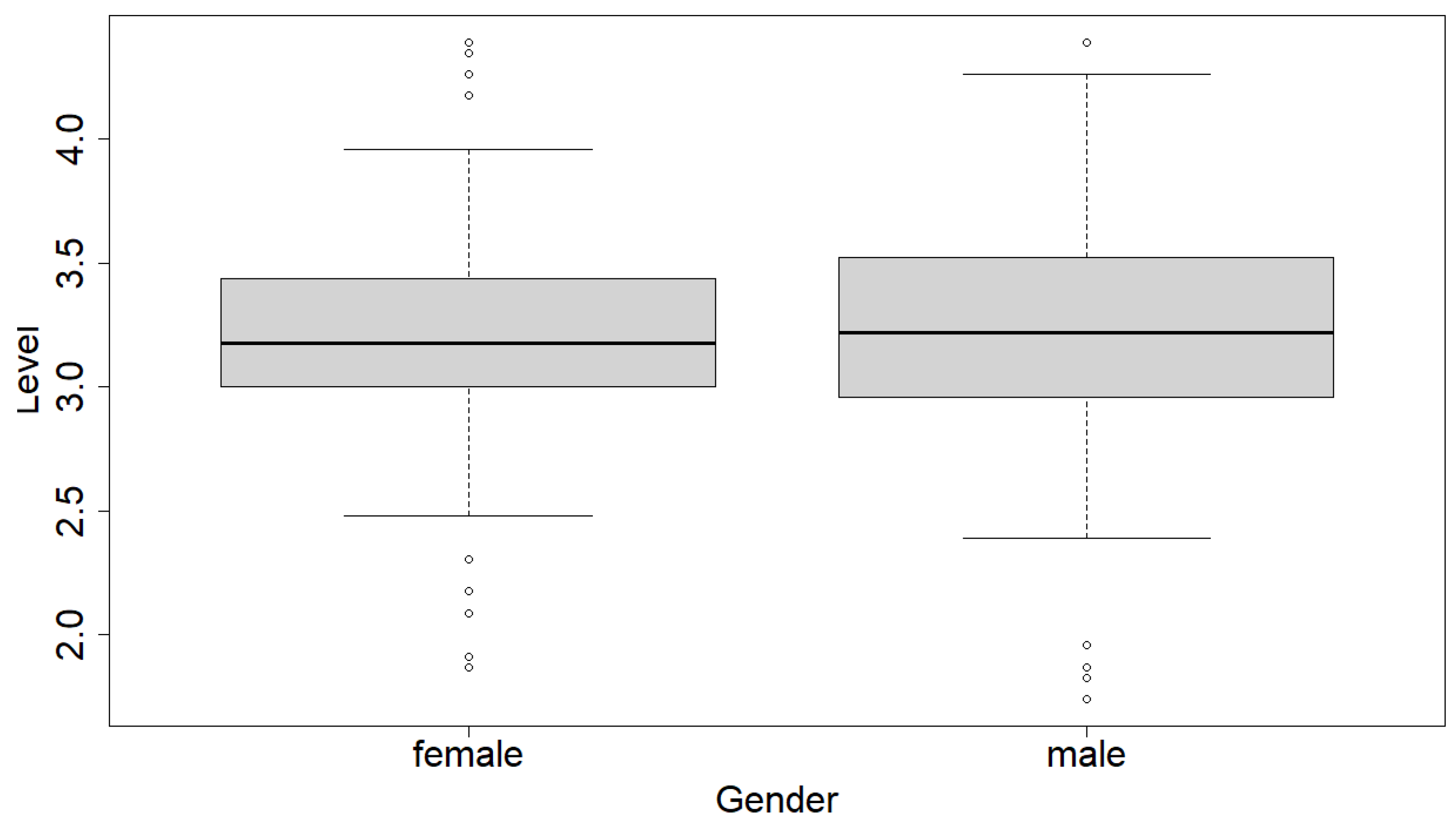

The data distributions of variable FAIRP according to respondents’ gender are shown in Figure 3.

According to the box plots given in Figure 3, it can be concluded that males could have a slightly higher variability level of the fairness perceptions (FAIRP) variable distribution than females. This conclusion can be drawn from the fact that males have a lower minimum (without outliers) and a higher maximum (without outliers) in variable FAIRP than females. Additionally, males have a lower first quartile but a higher third quartile in variable FAIRP compared to female respondents. However, the average levels seem to be quite the same between males and females at the variable FAIRP.

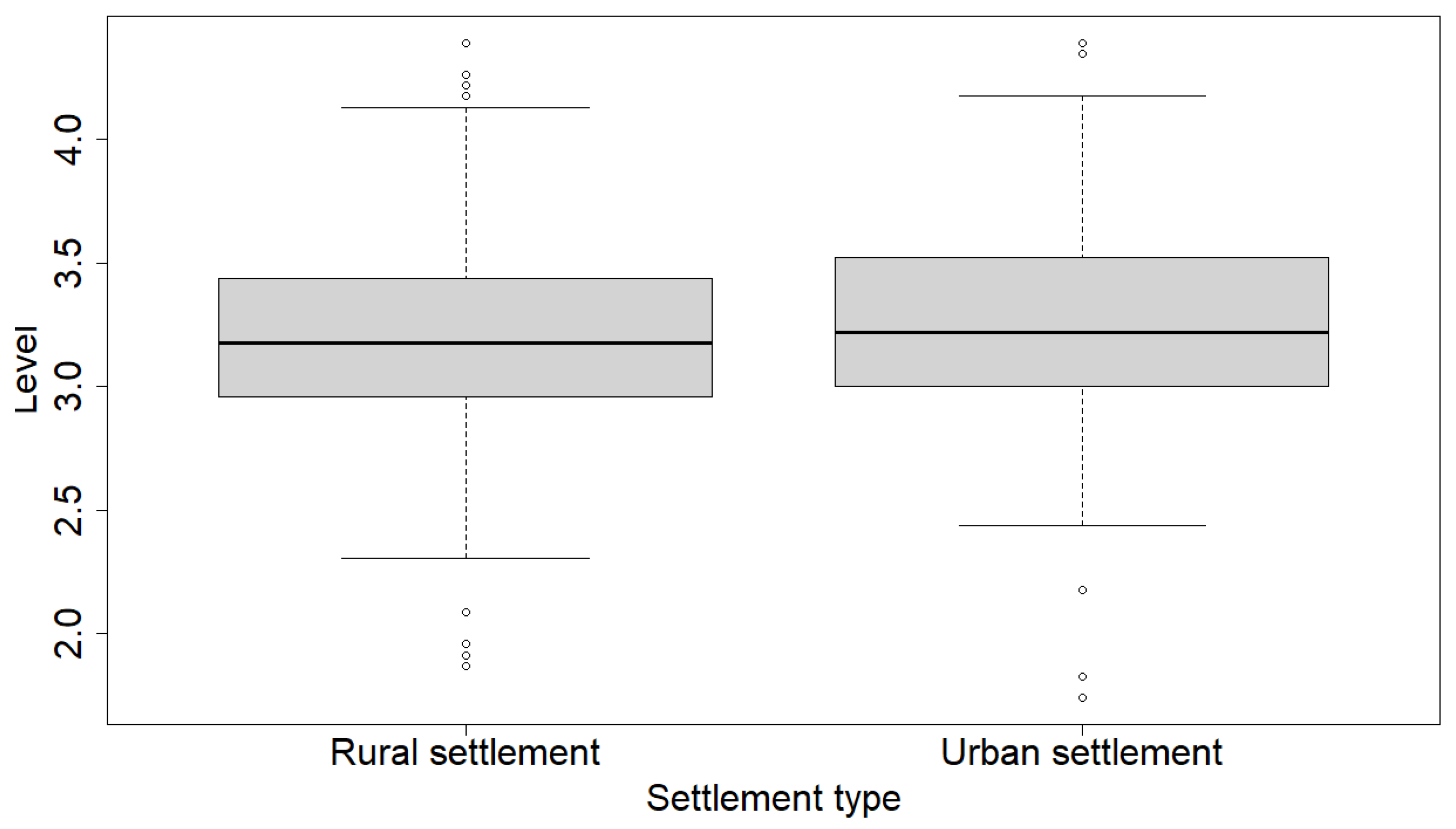

The data distributions of variable FAIRP according to the settlement type in which respondents live are presented by box plots in Figure 4.

The box plots suggest that respondents from a rural settlement and respondents from an urban settlement have quite similar distributions of variable FAIRP. For example, the first quartile for respondents who live in rural settlements is 2.96, whereas for respondents who live in urban settlements, it is 3.00. Similarly, the median for respondents who live in rural settlements is 3.17, whereas for respondents who live in urban settlements, it is 3.22. Again, the box plots are presented only for the main variable under study, FAIRP, whereas the box plots for other fairness perception dimensions are not shown.

In Table 8 Kruskal–Wallis rank sum test results are provided, in which fairness perception variables according to gender and settlement type are compared.

In Table 8, the test statistics of the conducted Kruskal–Wallis rank sum tests and their corresponding p-values are provided separately. If the p-value is lower than 0.05, it can be concluded that there is a statistically significant difference in fairness perception levels for a certain fairness perception variable between females and males when observed according to gender or between respondents living in urban and rural settlements when observed according to settlement type variables. The results from Table 7, Figure 3, and Figure 4 already indicated what could be the Kruskal–Wallis rank sum test results. According to results from Table 8, at the significance level of 0.05, there is a statistically significant difference between females and males only at variable AF1 (p-value = 0.0263). Similarly, statistically significant differences, at the significance level of 0.05, between respondents from a rural settlement and from an urban settlement are present only at variables RF1 (p-value = 0.0004) (consequently at variable RF as well) and PF6 (p-value = 0.0500). Therefore, the research subhypothesis (H2a, H2b) that the level of tax fairness differs significantly between females and males and between rural taxpayers and urban taxpayers, respectively, can be rejected.

4.4. Tax Knowledge Correlation with Fairness Perception Dimensions

The correlation between overall tax knowledge (variable TAXK) and fairness perception dimensions (variables GF, EF, HF, VF, RF, PF, and AF) was measured by applying the Kendall’s coefficient of rank. The correlation results are given in Table 9. Along with Kendall’s Tau-b statistic, the related p-value is provided as well. If the p-value is lower than 0.05, it can be concluded that there is a statistically significant association between the variable TAXK and the observed fairness perception dimension. If the association is statistically significant, the strength of the association can be commented upon.

According to the results from Table 9, all observed correlations are statistically significant at significance level 0.05. However, tax knowledge is mostly weakly associated with fairness perception dimensions. The highest association levels are present at the GF and RF fairness perception dimensions. In those two cases, it could be concluded that tax knowledge is medium and positively associated with GF (Kendall’s = 0.2936) and RF (Kendall’s = 0.2922), respectively. The results have shown that tax knowledge is negatively associated with HF (Kendall’s = −0.1262) and with VF (Kendall’s = −0.1805). Therefore, the third research hypothesis, H3, that tax knowledge positively influences the dimensions of fairness perception of Slovene taxpayers, can be partially accepted.

5. Discussion

For the purpose of selecting respondents, the snowball sampling approach was used. This method is appropriate when investigating sensitive topics, such as personal finances and tax behaviors, due to privacy concerns and a reluctance to disclose certain sensitive information. However, snowball sampling could lead to bias in the results due to a non-representative sample. Therefore, the drawn conclusions should be limited only to the observed sample.

The findings regarding taxpayers’ tax knowledge indicate that taxpayers perceive themselves as having an average level of general tax knowledge. When comparing the results of tax knowledge perception levels between male and female taxpayers in Slovenia, it was revealed that females have a lower overall tax knowledge level than males (TAXK). Among the dimensions of tax knowledge perceptions, females tend to believe more than males that the taxation obligation in the existing income tax system is fair and equitable. The highest score in male perception was achieved for the statement about their lack of technical knowledge regarding deductions from their tax liability. On the other hand, both females and males had the lowest average tax knowledge level when it came to the technical knowledge of whether it is acceptable to overstate tax deductions on one’s tax returns. It should be emphasized that our research measured the perception of tax knowledge, not the reasons influencing perception, and not differences in actual tax knowledge between females and males. Statistically, females in Slovenia achieve higher levels of formal education than males (SURS 2023). Nevertheless, their perception is that their tax knowledge is lower than that of males. The explanation for such results could be attributed to various underlying mechanisms, including historical, sociological, psychological, economic, institutional, or others. According to Yao et al. (2023) and their family financial socialization process theory, as well as the conclusions of Zhu (2018) and Deenanath et al. (2019), individuals’ subjective self-evaluated knowledge correlates with socialization processes. These factors undoubtedly influence the educational self-image of females in Slovenia. Further research is needed to examine this more precisely. If we compare our results to those from Saad’s (2010) study, our taxpayers exhibit notably much lower levels of perceived general, legal, and technical tax knowledge, irrespective of gender. Still, as the differences in overall tax knowledge in our research were significant, the research subhypothesis H1a, that the level of tax knowledge differs significantly between females and males, was accepted. These results are similar to Fallan’s (1999) conclusion that males and females may possess varying levels of tax knowledge, but these differences were not substantial in his research; therefore, he sees that gender lacks predictive influence. This result does not align with the findings of Natasha and Yustina’s (2020) study, in which no gender differences in tax knowledge and tax compliance were identified. They concluded that socialization could be conducted uniformly regardless of gender, as males and females absorb tax knowledge from the same media in the same amount (Natasha and Yustina 2020).

The results of the research subhypothesis H1b indicate that the variability in the level of overall tax knowledge perception is higher among taxpayers from rural settlements compared to taxpayers from urban areas. Taxpayers in rural areas perceive the existing income tax system as sufficient for most citizens, even though it may not be perfect. However, urban taxpayers scored the highest on the statement about having low knowledge of tax deductions (technical knowledge). On the other hand, rural taxpayers tend to disapprove of the acceptability of overstating tax deductions on their tax returns (technical knowledge), while urban taxpayers have slightly better legal knowledge concerning appeals against tax authority assessments compared to those in rural areas. However, the research subhypothesis H1b, which suggests that the level of tax knowledge significantly differs between rural and urban taxpayers, was not accepted. There are no statistically significant differences in overall tax knowledge (TAXK), although there are statistically significant differences in LK1, TK, and TK3. Our finding shows that taxpayers’ tax knowledge perception is independent of their living area (urban and rural). Potential reasons behind these results might stem from the fact that the Slovenian tax system (tax administration) is well-organized, has good information support, and taxpayers are informed about crucial tax matters, such as meeting tax obligations (tax return deadlines), primarily through public media (TV, radio), and online.

Further, our results also show that both females and males have achieved the highest average value in the variable of vertical fairness, indicating that higher-income earners should pay more taxes than lower-income earners. Both females and males mostly disagree with the idea that tax evasion is justified as ethical, even if the tax system is not fair. When measuring their perceived attitude toward personal fairness, they both perceive a specific group of taxpayers, namely board members, as not paying their fair share of taxes under the current income tax system. According to the results, males may have a slightly higher level of variability in the distribution of the fairness perceptions (FAIRP) variable compared to females. However, the average levels of the FAIRP variable appear to be quite similar between males and females. When comparing taxpayers based on the type of settlement they live in, it becomes evident that there are numerous similarities. Both taxpayers from rural settlements and those from urban settlements have achieved the highest average value in the variable of vertical fairness, which suggests that higher-income earners should pay more taxes than lower-income earners. However, both categories recorded the lowest average values in the variable of general fairness. This implies that tax evasion is considered ethical if the tax system is perceived as unfair. Taxpayers from rural and urban settlements exhibit quite similar distributions in the FAIRP variable. The subhypotheses H2a and H2b, which hypothesized significant differences in tax fairness levels between females and males, as well as between rural and urban taxpayers, were rejected. Statistically significant differences were found only between respondents from rural and urban settlements in variables RF1 (and consequently RF) and PF6, but not in the overall variable of fair perception (FAIRP). Our results are not in line with Hundsdoerfer and Eva’s (2020) findings, where gender disparities in perceptions of fairness concerning distributive and procedural justice were confirmed. Male participants are particularly responsive to procedural justice violations in their fairness perceptions, while female participants tend to adjust their fairness perceptions based on the outcomes of the tax allocation procedure (Hundsdoerfer and Eva 2020).

The third hypothesis (H3) predicts a positive influence of tax knowledge on the perception of tax fairness dimensions. The results show that all observed correlations between tax knowledge (TAXK) and fairness dimensions were statistically significant, but weak. General fairness and redistributive fairness exhibited the most moderate associations among all dimensions with tax knowledge. Still, further analysis, using Kendall’s test, confirmed statistically significant correlations between tax knowledge and various tax fairness dimensions, including general, exchange, redistributive, personal, and administrative fairness. However, the correlations were negative for horizontal and vertical fairness, also known as distributive fairness. Horizontal fairness pertains to providing equitable tax treatment to taxpayers in similar economic circumstances, while vertical fairness evaluates taxpayers’ ability to pay and their preference for the tax rate structure (progressive or not). The negative relationship suggests that higher tax knowledge does not necessarily lead to a higher perception of distributive fairness within the existing income tax system. Therefore, the third research hypothesis, H3, was partially accepted. One explanation for this finding is mostly like that of Saad (2010), who suggests that taxpayers may believe that they should not be taxed equally solely based on income without considering their financial responsibilities or social welfare. Our findings align with previous studies (Saad 2010; Fallan 1999; White 1990) that assert tax knowledge increases taxpayers’ perceptions of tax fairness. However, the findings do not fully align with Eriksen and Fallan (1996), whose conclusions suggest that the perception of fairness increases with tax knowledge, and with the more knowledgeable taxpayers viewing the tax system more favorably. We defined tax knowledge and tax fairness as multidimensional, but the Eriksen and Fallan (1996) study did not distinguish between these dimensions. According to our study, higher tax knowledge does not appear to support taxpayers in perceiving greater distributive fairness.