Determinants of Behavioral Intention to Use Digital Payment among Indian Youngsters

Abstract

:1. Introduction

1.1. Objectives of this Study

- To determine shoppers’ behavioral intention to use M-wallet services;

- To assess the elements that influence shoppers’ use of digital payments;

- To investigate the impact of identified variables on shoppers’ satisfaction and trust, which are mediators of M-wallet intention;

- To provide recommendations to M-wallet institutions for ways to increase the use of M-wallets among shoppers.

1.2. Statement of the Problem

2. Theoretical Background

2.1. Technology Acceptance Theories

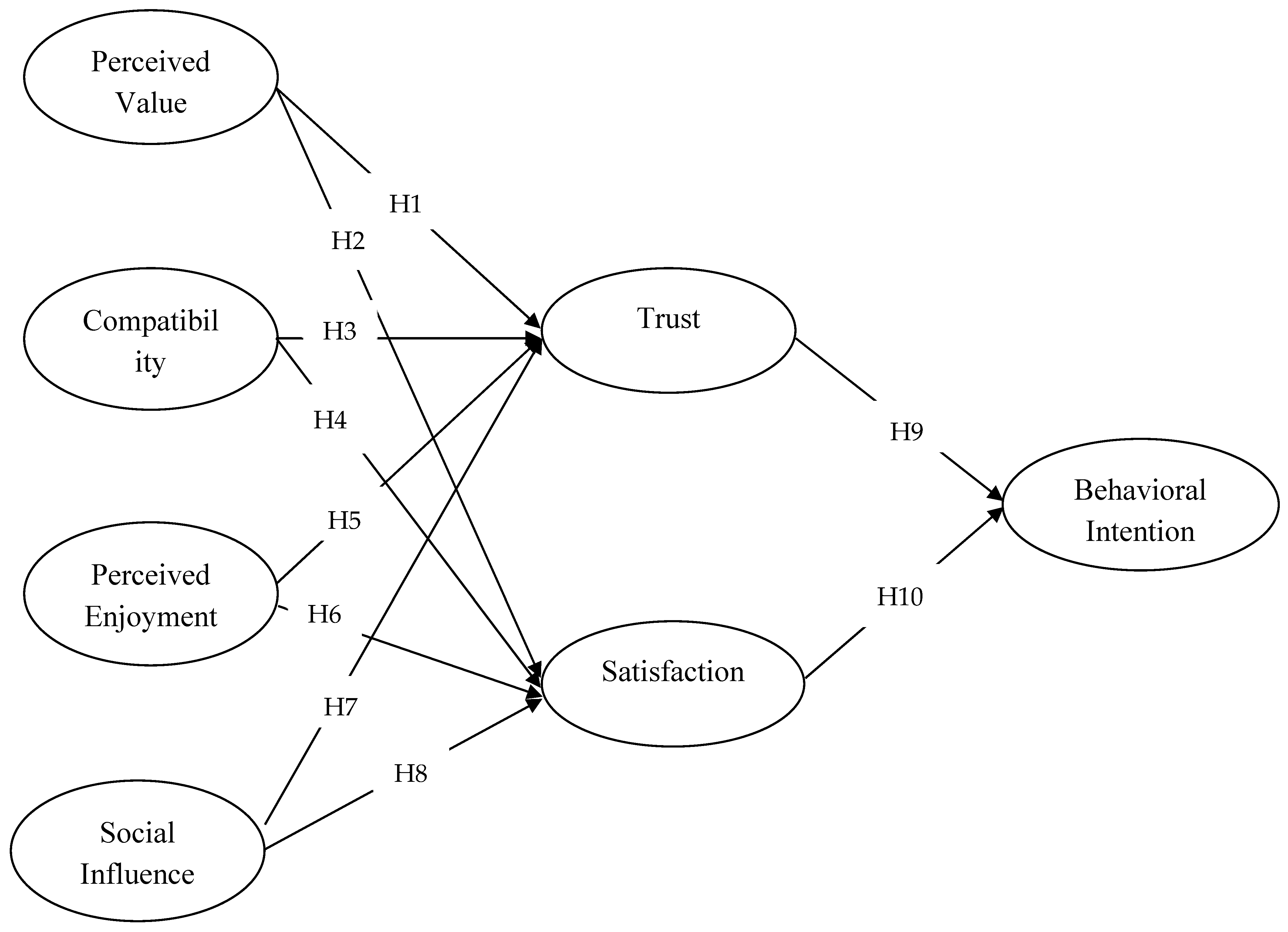

2.2. Research Hypothesis Development

- Perceived Value and Trust

- Perceived Value and Shopper Satisfaction

- Compatibility and Trust

- Compatibility and Shopper Satisfaction

- Perceived Enjoyment and Trust

- Perceived Enjoyment and Shopper Satisfaction

- Social Influence and Trust

- Social Influence and Shopper Satisfaction

- Trust and Behavioral Intention

- Shoppers Satisfaction and Behavioral Intention

2.3. Research Gap

3. Research Methodology

3.1. Research Design

3.2. Sampling

3.3. Instrument Used

3.4. Data Collection

4. Results

4.1. Demographic Analysis

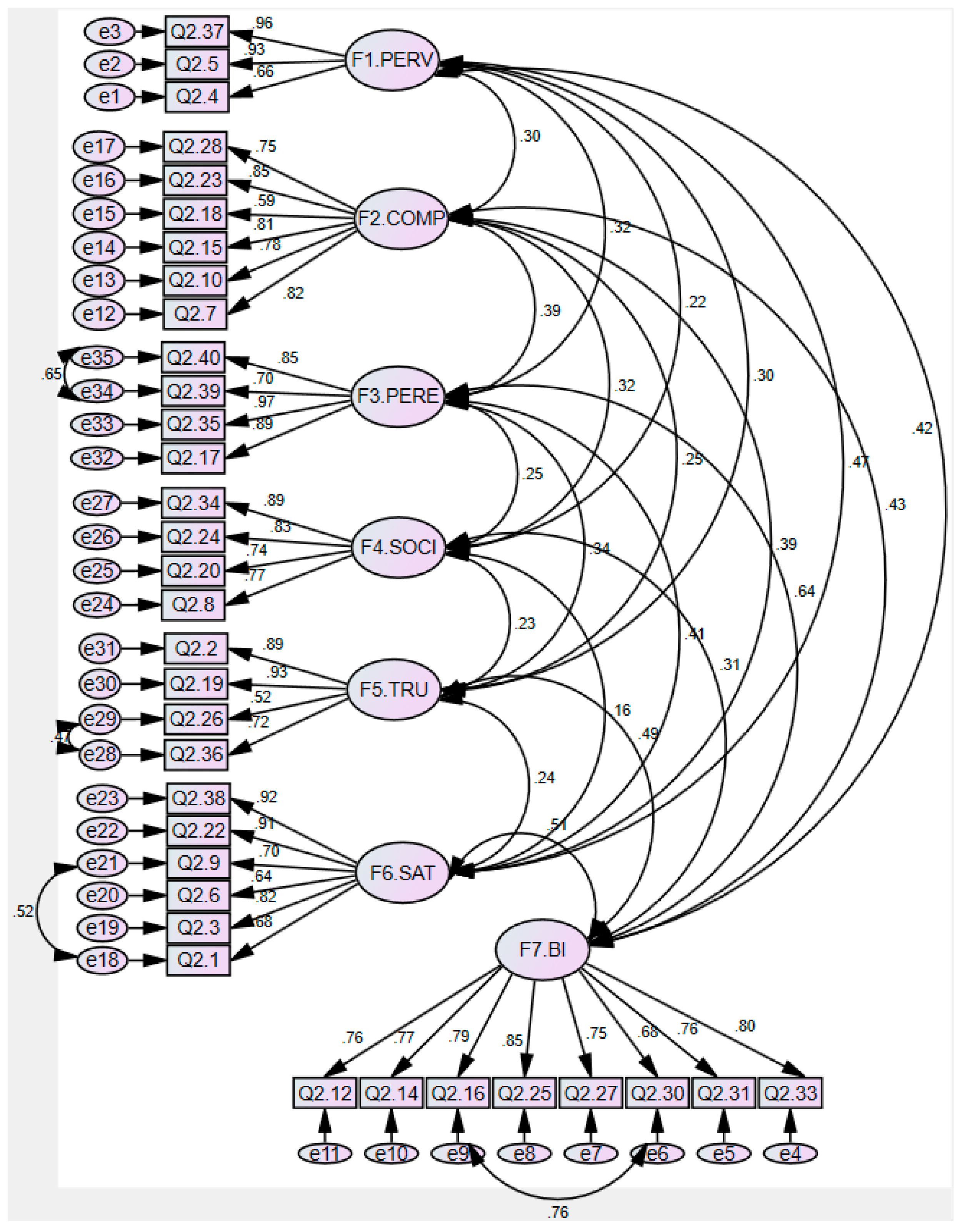

4.2. Reliability and Validity Analysis

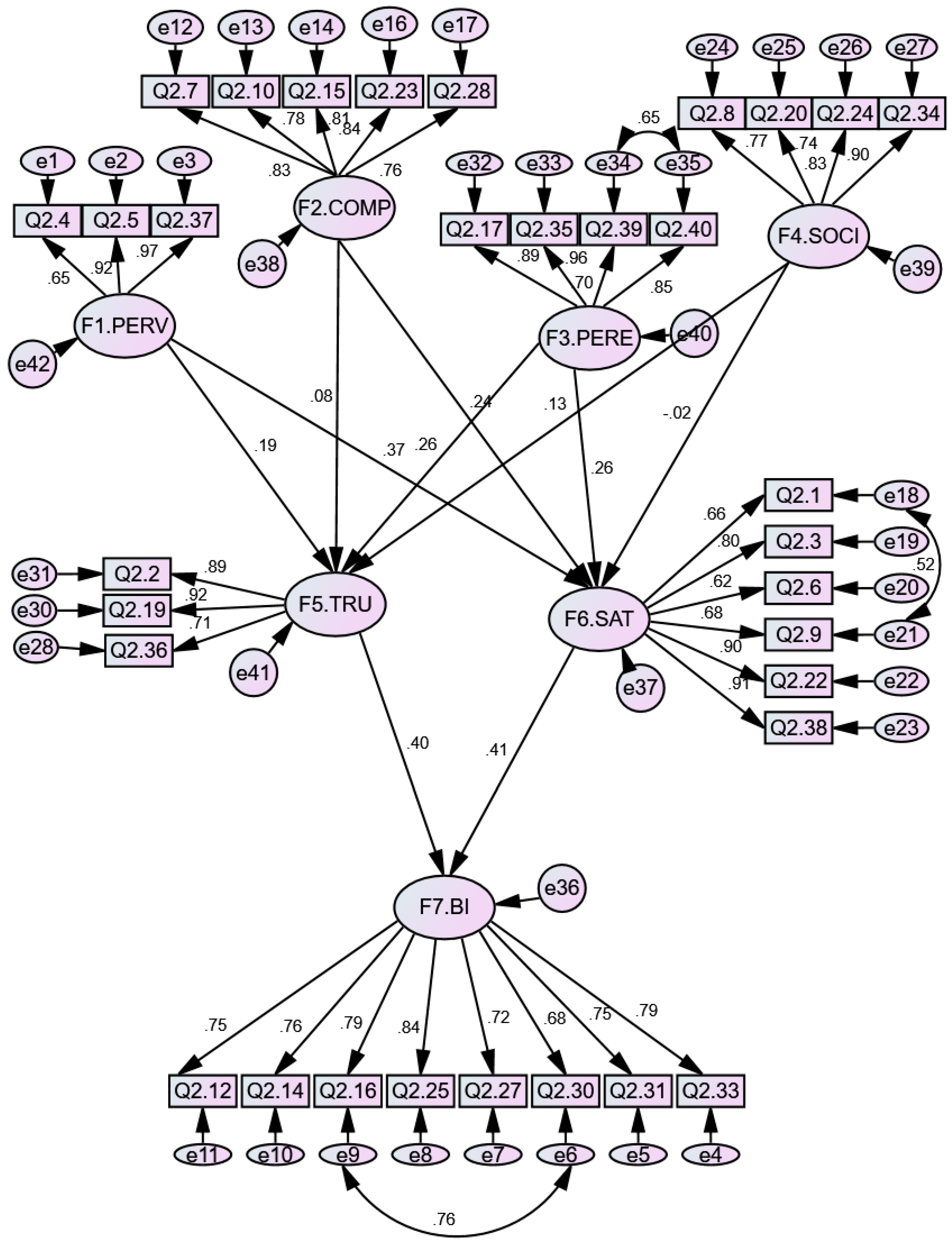

4.3. Structural Model and Hypothesis Testing

5. Results and Findings

6. Suggestions and Implications

7. Limitations and Future Research Agenda

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Adeoti, O. O., and K. O. Oshotimehin. 2011. Factors influencing consumers adoption of point of sale terminals in Nigeria. Journal of Emerging Trends in Economics and Management Sciences 2: 388–92. [Google Scholar]

- Aithal, Rajesh K., Vikram Choudhary, Harshit Maurya, Debasis Pradhan, and Dev Narayan Sarkar. 2023. Factors influencing technology adoption amongst small retailers: Insights from thematic analysis. International Journal of Retail & Distribution Management 51: 81–102. [Google Scholar]

- Ajzen, Icek. 1991. The theory of planned behavior. Organizational Behavior and Human Decision Processes 50: 179–211. [Google Scholar] [CrossRef]

- Ajzen, Icek, and Martin Fishbein. 1975. A Bayesian analysis of attribution processes. Psychological Bulletin 82: 261. [Google Scholar] [CrossRef]

- Alalwan, A. A., Y. K. Dwivedi, and N. P. Rana. 2017. Factors influencing adoption of mobile banking by Jordanian bank customers: Extending UTAUT2 with trust. International Journal of Information Management 37: 99–110. [Google Scholar] [CrossRef]

- Apanasevic, Tatjana, Jan Markendahl, and Niklas Arvidsson. 2012. Mobile Payments Guide 2012: Insights in the Worldwide Mobile Financial Service Market. Released by The Paypers BV, March, 2012. Available online: http://ibfsinc.com/uploads/Mobile_Payments_Market_Guide_2012.pdf (accessed on 29 March 2015).

- Aslam, W., M. Ham, and I. Arif. 2017. Consumer behavioral intentions towards mobile payment services: An empirical analysis in Pakistan. Trziste Market 29: 161–76. [Google Scholar] [CrossRef]

- Auh, Seigyoung, and Michael D. Johnson. 2005. Compatibility effects in evaluations of satisfaction and loyalty. Journal of Economic Psychology 26: 35–57. [Google Scholar] [CrossRef]

- Balan, Rajesh Krishna, and Narayanasamy Ramasubbu. 2009. The digital wallet: Opportunities and prototypes. IEEE Computer 42: 100. [Google Scholar] [CrossRef]

- Bashir, Irfan, and Chendragiri Madhavaiah. 2015. Consumer attitude and behavioural intention towards Internet banking adoption in India. Journal of Indian Business Research 7: 67–102. [Google Scholar] [CrossRef]

- Benitez, Jose, Yang Chen, Thompson S. H. Teo, and Aseel Ajamieh. 2018. Evolution of the impact of e-business technology on operational competence and firm profitability: A panel data investigation. Information & Management 55: 120–30. [Google Scholar]

- Brand, Benedikt Martin, and Daniel Baier. 2020. Adaptive CBC Adaptive CBC: Are the benefits justifying its additional efforts compared to CBC? Archives of Data Science, Series A 6: 6, 22S. [Google Scholar]

- Cazier, Joseph. 2003. The Role of Value Compatibility in Trust Production and E-Commerce. AMCIS 2003 Proceedings. 430. Available online: http://aisel.aisnet.org/amcis2003/430 (accessed on 3 January 2024).

- Chang, Shuchih Ernest, Wei-Cheng Shen, and Anne Yenching Liu. 2016. Why mobile users trust smartphone social networking services? A PLS-SEM approach. Journal of Business Research 69: 4890–95. [Google Scholar] [CrossRef]

- Chawla, Deepak, and Himanshu Joshi. 2019. Consumer attitude and intention to adopt mobile wallet in India–An empirical study. International Journal of Bank Marketing 37: 1590–618. [Google Scholar] [CrossRef]

- Chen, Shih Chih. 2012. To use or not to use: Understanding the factors affecting continuance intention of mobile banking. International Journal of Mobile Communications 10: 490–507. [Google Scholar] [CrossRef]

- Chiu, Jason Lim, Nelson C. Bool, and Candy Lim Chiu. 2017. Challenges and factors influencing initial trust and behavioral intention to use mobile banking services in the Philippines. Asia Pacific Journal of Innovation and Entrepreneurship 11: 246–78. [Google Scholar] [CrossRef]

- Chong, Alain Yee-Loong. 2013. Predicting m-commerce adoption determinants: A neural network approach. Expert Systems with Applications 40: 523–30. [Google Scholar] [CrossRef]

- Cole, Alan, Scott McFaddin, Chandra Narazanaswami, and Alpana Tiwari. 2009. Toward a Mobile Digital Wallet. New York: IBM Research Division. [Google Scholar]

- Constantiou, Ioanna D., Jan Damsgaard, and Lars Knutsen. 2006. Exploring perceptions and use of mobile services: User differences in an advancing market. International Journal of Mobile Communications 4: 231–47. [Google Scholar] [CrossRef]

- Curran, James M., and Matthew L. Meuter. 2005. Self-service technology adoption: Comparing three technologies. Journal of Services Marketing 19: 103–13. [Google Scholar] [CrossRef]

- Dahlberg, Tomi, Niina Mallat, Jan Ondrus, and Agnieszka Zmijewska. 2008. Past, present and future of mobile payments research: A literature review. Electronic Commerce Research and Applications 7: 165–81. [Google Scholar] [CrossRef]

- Davis, Fred D. 1989. Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Quarterly 13: 319–40. [Google Scholar] [CrossRef]

- Davis, Fred D., Richard P. Bagozzi, and Paul R. Warshaw. 1992. Extrinsic and intrinsic motivation to use computers in the workplace 1. Journal of Applied Social Psychology 22: 1111–32. [Google Scholar] [CrossRef]

- Doney, Patricia M., and Joseph P. Cannon. 1997. An examination of the nature of trust in buyer–seller relationships. Journal of Marketing 61: 35–51. [Google Scholar]

- Eggert, Andreas, and Wolfgang Ulaga. 2002. Customer perceived value: A substitute for satisfaction in business markets? Journal of Business & Industrial Marketing 17: 107–18. [Google Scholar]

- Ehrenhard, Michel, Fons Wijnhoven, Tijs van den Broek, and Marc Zinck Stagno. 2017. Unlocking how start-ups create business value with mobile applications: Development of an App-enabled Business Innovation Cycle. Technological Forecasting and Social Change 115: 26–36. [Google Scholar] [CrossRef]

- Esmaili, Ebrahim, Mohammad Ishak Desa, Hadi Moradi, and Amin Hemmati. 2011. The role of trust and other behavioral intention determinants on intention toward using internet banking. International Journal of Innovation, Management and Technology 2: 95. [Google Scholar]

- Eze, Uchenna Cyril, Gerald Goh Guan Gan, John Ademu, and Samson A. Tella. 2008. Modelling user trust and mobile payment adoption: A conceptual Framework. Communications of the IBIMA 3: 224–31. [Google Scholar]

- Gbongli, Komlan. 2022. Understanding Mobile Financial Services Adoption through a Systematic Review of the Technology Acceptance Model. Open Journal of Business and Management 10: 2389–404. [Google Scholar] [CrossRef]

- Gefen, David, and Detmar W. Straub. 2004. Consumer trust in B2C e-Commerce and the importance of social presence: Experiments in e-Products and e-Services. Omega 32: 407–24. [Google Scholar] [CrossRef]

- Gefen, David, Elena Karahanna, and Detmar W. Straub. 2003. Trust and TAM in online shopping: An integrated model. MIS Quarterly 27: 51–90. [Google Scholar] [CrossRef]

- George, Ajimon, and Prajod Sunny. 2021. Developing a research model for mobile wallet adoption and usage. IIM Kozhikode Society & Management Review 10: 82–98. [Google Scholar]

- Govender, Irene, and Walter Sihlali. 2014. A study of mobile banking adoption among university students using an extended TAM. Mediterranean Journal of Social Sciences 5: 451. [Google Scholar] [CrossRef]

- Gupta, Anil, Nikita Dogra, and Babu George. 2018. What determines tourist adoption of smartphone apps? An analysis based on the UTAUT-2 framework. Journal of Hospitality and Tourism Technology 9: 50–64. [Google Scholar] [CrossRef]

- Gupta, Dinesh, Abhishek Singhal, Sudarshana Sharma, Arif Hasan, and Sandeep Raghuwanshi. 2023. Humans’ Emotional and Mental Well-Being under the Influence of Artificial Intelligence. Journal for ReAttach Therapy and Developmental Diversities 6: 184–97. [Google Scholar]

- Hair, Joe F., Christian M. Ringle, and Marko Sarstedt. 2011. PLS-SEM: Indeed a silver bullet. Journal of Marketing Theory and Practice 19: 139–52. [Google Scholar] [CrossRef]

- Hair, Joseph F., William C. Black, Barry J. Babin, Rolph E. Anderson, and R. Tatham. 2010. Multivariate Data Analysis. Edited by Multivariate Data Analysis. Hoboken: Pearson Prentice Hall. [Google Scholar]

- Hamza, Aminu, and Asadullah Shah. 2014. Gender and mobile payment system adoption among students of tertiary institutions in Nigeria. International Journal of Computer and Information Technology 3: 13–20. [Google Scholar]

- Hasan, Arif, Abhishek Singhal, Priyanka Sikarwar, Kul Prakash, Sandeep Raghuwanshi, Prashant Raj Singh, Arun Mishra, and Dinesh Gupta. 2023a. Impact of Destination Image Antecedents on Tourists Revisit Intention in India. Journal of Law and Sustainable Development 11: e843. [Google Scholar] [CrossRef]

- Hasan, Arif, and S. K. Gupta. 2020. Exploring tourists’ behavioural intentions towards use of select mobile wallets for digital payments. Paradigm 24: 177–94. [Google Scholar] [CrossRef]

- Hasan, Arif, Archana Yadav, Sudarshana Sharma, Abhishek Singhal, Dinesh Gupta, Sandeep Raghuwanshi, Vikas Kumar Khare, and Priyanka Verma. 2023b. Factors Influencing Behavioural Intention to Embrace Sustainable Mobile Payment Based on Indian User Perspective. Journal of Law and Sustainable Development 11: e627. [Google Scholar] [CrossRef]

- Hasan, Arif. 2018a. Evaluation of Factors Influencing Exclusive Brand Store Choice: An Investigation in the Indian Retail Sector. Vision 22: 416–24. [Google Scholar] [CrossRef]

- Hasan, Arif. 2018b. Impact of store and product attributes on purchase intentions: An analytical study of apparel shoppers in Indian organized retail stores. Vision 22: 32–49. [Google Scholar] [CrossRef]

- Hayashi, Fumiko, and Terri Bradford. 2014. Mobile payments: Merchants’ perspectives. Economic Review 99: 5–30. [Google Scholar]

- Hemchand, Shravan. 2016. Adoption of sensor based communication for mobile marketing in India. Journal of Indian Business Research 8: 65–76. [Google Scholar]

- Holbrook, Morris B., ed. 1999. Consumer Value: A Framework for Analysis and Research. London: Psychology Press. [Google Scholar]

- Hossain, Md Shamim, Xiaoyan Zhou, and Mst Farjana Rahman. 2018. Examining the impact of QR codes on purchase intention and customer satisfaction on the basis of perceived flow. International Journal of Engineering Business Management 10: 1847979018812323. [Google Scholar] [CrossRef]

- Hung, Do Nam, Jacquline Tham, S. F. Azam, and Abdol Ali Khatibi. 2019. An Empirical Analysis of Perceived Transaction Convenience, Performance Expectancy, Effort Expectancy and Behavior Intention to Mobile Payment of Cambodian Users. International Journal of Marketing Studies 11: 77. [Google Scholar] [CrossRef]

- Hwang, Yujong, and Dan J. Kim. 2007. Customer self-service systems: The effects of perceived Web quality with service contents on enjoyment, anxiety, and e-trust. Decision Support Systems 43: 746–60. [Google Scholar] [CrossRef]

- Indrati, Aviarini, Edi Minaji, Sugiharti Binastuti, and Philipus Dwi Raharjo. 2014. Comparation of Model Unified Theory of Acceptance and Use Technology (UTAUT) And Technology Acceptance Model (TAM) for Internet Adoption of Credit Union Staff. In The First International Credit Union Conference on Social Micro. Depok: Gunadarma University. [Google Scholar]

- Kalyani, Pawan. 2016. An Empirical Study about the Awareness of Paperless E-Currency Transaction like E-Wallet Using ICT in the Youth of India. Journal of Management Engineering and Information Technology 3: 18–41. [Google Scholar]

- Khare, Vikas Kumar, Sandeep Raghuwanshi, Anil Vashisht, Priyanka Verma, and Rashmi Chauhan. 2023. The importance of green management and its implication in creating sustainability performance on the small-scale industries in India. Journal of Law and Sustainable Development 11: e699. [Google Scholar] [CrossRef]

- Khatoon, Sadia, Xu Zhengliang, and Hamid Hussain. 2020. The Mediating Effect of customer satisfaction on the relationship between Electronic banking service quality and customer Purchase intention: Evidence from the Qatar banking sector. Sage Open 10: 2158244020935887. [Google Scholar] [CrossRef]

- Kim, Changsu, Wang Tao, Namchul Shin, and Ki-Soo Kim. 2010. An empirical study of customers’ perceptions of security and trust in e-payment systems. Electronic Commerce Research and Applications 9: 84–95. [Google Scholar] [CrossRef]

- Kline, Rex B. 2015. Principles and practice of structural equation modeling. Guilford Publications 40: 381. [Google Scholar]

- Kline, Stephen J., and Nathan Rosenberg. 2010. An overview of innovation. In Studies on Science and the Innovation Process: Selected Works of Nathan Rosenberg. Singapore: World Scientific, pp. 173–203. [Google Scholar]

- Kotecha, Priyanka S. 2018. An Empirical Study of Mobile Wallets in India. Research Guru: Online Journal of Multidisciplinary Subjects 11: 605–11. [Google Scholar]

- Krejcie, Robert V., and Daryle W. Morgan. 1970. Determining sample size for research activities. Educational and Psychological Measurement 30: 607–10. [Google Scholar] [CrossRef]

- Lai, T. L. 2004. Service quality and perceived value’s impact on satisfaction, intention and usage of short message service (SMS). Information Systems Frontiers 6: 353–68. [Google Scholar] [CrossRef]

- Lewicki, Roy J., Edward C. Tomlinson, and Nicole Gillespie. 2006. Models of interpersonal trust development: Theoretical approaches, empirical evidence, and future directions. Journal of Management 32: 991–1022. [Google Scholar] [CrossRef]

- Lewis, Beth A., David M. Williams, Amanda Frayeh, and Bess H. Marcus. 2016. Self-efficacy versus perceived enjoyment as predictors of physical activity behaviour. Psychology & Health 31: 456–69. [Google Scholar]

- Lin, Hsin-Hui, and Yi-Shun Wang. 2006. An examination of the determinants of customer loyalty in mobile commerce contexts. Information & Management 43: 271–82. [Google Scholar]

- Liu, S., Yue Zhuo, Dilip Soman, and Min Zhao. 2012. The Consumer Implications of the Use of Electronic and Mobile Payment Systems. Toronto: Rotman School of Management, University of Toronto. [Google Scholar]

- Lwoga, Edda Tandi, and Noel Biseko Lwoga. 2017. User acceptance of mobile payment: The effects of user-centric security, system characteristics and gender. The Electronic Journal of Information Systems in Developing Countries 81: 1–24. [Google Scholar] [CrossRef]

- Mallat, N., M. Rossi, and V. K. Tuunainen. 2004. Mobile banking services. Communications of the ACM 47: 42–46. [Google Scholar] [CrossRef]

- Markendahl, J., M. Smith, and P. Andersson. 2010. Analysis of Roles and Position of Mobile Network Operators in Mobile Payment Infrastructure. Calgary: International Telecommunications Society (ITS). [Google Scholar]

- Mattila, Anna S., and Jochen Wirtz. 2001. Congruency of scent and music as a driver of in-store evaluations and behavior. Journal of Retailing 77: 273–89. [Google Scholar] [CrossRef]

- Mayer, Roger C., James H. Davis, and F. David Schoorman. 1995. An integrative model of organizational trust. Academy of Management Review 20: 709–34. [Google Scholar] [CrossRef]

- McDonald, Roderick P., and Moon-Ho Ringo Ho. 2002. Principles and practice in reporting structural equation analyses. Psychological Methods 7: 64. [Google Scholar] [CrossRef] [PubMed]

- McDougall, Gordon H. G., and Terrence Levesque. 2000. Customer satisfaction with services: Putting perceived value into the equation. Journal of Services Marketing 14: 392–410. [Google Scholar] [CrossRef]

- Mew, Jamie, and Elena Millan. 2021. Mobile wallets: Key drivers and deterrents of consumers’ intention to adopt. The International Review of Retail, Distribution and Consumer Research 31: 182–210. [Google Scholar] [CrossRef]

- Mittal, Saurabh, and Vikas Kumar. 2018. Adoption of Mobile Wallets in India: An Analysis. IUP Journal of Information Technology 14: 42–57. [Google Scholar]

- Murendo, C., M. Wollni, A. De Brauw, and N. Mugabi. 2018. Social network effects on mobile money adoption in Uganda. The Journal of Development Studies 54: 327–42. [Google Scholar] [CrossRef]

- Musa, Grace Akinyi, Pamela Atieno Moro, and Sandra Beldine Otieno. 2020. An Assessment of Customers’ Adaptability to Technological Innovations in Kenya’s Banking Industry: Effects of Customers Perceptions. Research Journal of Finance and Accounting 11: 14–21. [Google Scholar]

- Nowlis, Stephen M., and Itamar Simonson. 1997. Attribute–task compatibility as a determinant of consumer preference reversals. Journal of Marketing Research 34: 205–18. [Google Scholar]

- Nunnally, Jum C., and I. H. Bernstein. 1994. Psychometric Theory, 3rd ed. New York: McGraw Hill. [Google Scholar]

- Nysveen, Herbjørn, Per E. Pedersen, and Helge Thorbjørnsen. 2005. Explaining intention to use mobile chat services: Moderating effects of gender. Journal of Consumer Marketing 22: 247–56. [Google Scholar] [CrossRef]

- Oliveira, Tiago, Manoj Thomas, Goncalo Baptista, and Filipe Campos. 2016. Mobile payment: Understanding the determinants of customer adoption and intention to recommend the technology. Computers in Human Behavior 61: 404–14. [Google Scholar] [CrossRef]

- Oliveira, Tiago, Matilde Alhinho, Paulo Rita, and Gurpreet Dhillon. 2017. Modelling and testing consumer trust dimensions in e-commerce. Computers in Human Behavior 71: 153–64. [Google Scholar] [CrossRef]

- Ondrus, Jan, and Yves Pigneur. 2006. Towards a holistic analysis of mobile payments: A multiple perspectives approach. Electronic Commerce Research and Applications 5: 246–57. [Google Scholar] [CrossRef]

- Pavlou, Paul A. 2003. Consumer acceptance of electronic commerce: Integrating trust and risk with the technology acceptance model. International Journal of Electronic Commerce 7: 101–34. [Google Scholar]

- Plouffe, Christopher R., Mark Vandenbosch, and John Hulland. 2001. Intermediating technologies and multi-group adoption: A comparison of consumer and merchant adoption intentions toward a new electronic payment system. Journal of Product Innovation Management: An International Publication of The Product Development & Management Association 18: 65–81. [Google Scholar]

- Podsakoff, Philip M., Scott B. MacKenzie, Jeong-Yeon Lee, and Nathan P. Podsakoff. 2003. Common method biases in behavioral research: A critical review of the literature and recommended remedies. Journal of Applied Psychology 88: 879. [Google Scholar] [CrossRef] [PubMed]

- Prabhakaran, Sarika, S. Vasantha, and P. Sarika. 2020. Effect of social influence on intention to use mobile wallet with the mediating effect of promotional benefits. Journal of Xi’an University of Architecture & Technology 12: 3003–19. [Google Scholar]

- Pura, M. 2005. Linking perceived value and loyalty in location-based mobile services. Managing Service Quality: An International Journal 15: 509–38. [Google Scholar] [CrossRef]

- Purohit, Sonal, J. Kaur, and S. Chaturvedi. 2022. Mobile payment adoption among youth: Generation z and developing country perspective. Journal of Content, Community and Communication 15: 194–209. [Google Scholar] [CrossRef]

- Ramanathan, Usha, Nachiappan Subramanian, and Guy Parrott G. 2017. Role of social media in retail network operations and marketing to enhance customer satisfaction. International Journal of Operations and Production Management 37: 105–23. [Google Scholar] [CrossRef]

- Rathore, Hem Shweta. 2016. Adoption of digital wallet by consumers. BVIMSR’s Journal of Management Research 8: 69. [Google Scholar]

- Rees, Sharon, Helen Farley, and Clint Moloney. 2020. Economising learning: How nurses maintain competence with limited resources. A grounded theory study exploring Registered Nurses’ use of mobile devices in postgraduate education. BMC Nursing. preprint. [Google Scholar] [CrossRef]

- Rogers, Everett M., and David G. Cartano. 1962. Methods of measuring opinion leadership. Public Opinion Quarterly 26: 435–41. [Google Scholar] [CrossRef]

- Rogers, Everett M., Una E. Medina, Mario A. Rivera, and Cody J. Wiley. 2005. Complex adaptive systems and the diffusion of innovations. The Innovation Journal: The Public Sector Innovation Journal 10: 1–26. [Google Scholar]

- Roy, Sanjit Kumar, M. S. Balaji, Saalem Sadeque, Bang Nguyen, and T. C. Melewar. 2017. Constituents and consequences of smart customer experience in retailing. Technological Forecasting and Social Change 124: 257–70. [Google Scholar] [CrossRef]

- Schneider, Fred B., Steven M. Bellovin, and Alan S. 1998. Critical Infrastructures You Can Trust: Where Telecommunications Fits. Ithaca: Cornell University. [Google Scholar]

- Sharma, Deepti, Deepshikha Aggarwal, and Amisha Gupta. 2019. A study of consumer perception towards mwallets. International Journal of Scientific & Technlogy Research 8: 3892–95. [Google Scholar]

- Shaw, Norman. 2014. The mediating influence of trust in the adoption of the mobile wallet. Journal of Retailing and Consumer Services 21: 449–59. [Google Scholar] [CrossRef]

- Shin, Dong-Hee. 2009. Towards an understanding of the consumer acceptance of mobile wallet. Computers in Human Behavior 25: 1343–54. [Google Scholar] [CrossRef]

- Singh, Ajit Kumar, Sandeep Raghuwanshi, Sudarshana Sharma, Vikas Khare, Abhishek Singhal, Meenakshi Tripathi, and Subhojit Banerjee. 2023a. Modeling the Nexus Between Perceived Value, Risk, Negative Marketing, and Consumer Trust with Consumers’ Social Cross-Platform Buying Behaviour in India Using Smart-PLS. Journal of Law and Sustainable Development 11: e488. [Google Scholar] [CrossRef]

- Singh, Arjun, Somanchi Hari Krishna, Sandeep Raghuwanshi, Jitendra Sharma, and Varsha Bapat. 2023b. Measuring Psychological Wellbeing of Entrepreneurial Success–An Analytical Study. Journal for ReAttach Therapy and Developmental Diversities 6: 338–48. [Google Scholar]

- Srivastava, Shirish C., and Shalini Chandra. 2010. trusting the avatar: Antecedents and moderators of trust for using the virtual world. In Academy of Management Proceedings. Briarcliff Manor: Academy of Management, vol. 2010, pp. 1–6. [Google Scholar]

- Taylor, Shirley, and Peter Todd. 1995. Decomposition and crossover effects in the theory of planned behavior: A study of consumer adoption intentions. International Journal of Research in Marketing 12: 137–55. [Google Scholar] [CrossRef]

- To, Anh Tho, and Thi Hong Minh Trinh. 2021. Understanding behavioral intention to use mobile wallets in vietnam: Extending the tam model with trust and enjoyment. Cogent Business & Management 8: 1891661. [Google Scholar]

- Van der Heijden, Hans. 2002. Factors affecting the successful introduction of mobile payment systems. Paper presented at BLED 2002 Proceedings, Bled, Slovenia, June 17–19; vol. 20. [Google Scholar]

- Varki, Sajeev, and Mark Colgate. 2001. The role of price perceptions in an integrated model of behavioral intentions. Journal of Service Research 3: 232–40. [Google Scholar] [CrossRef]

- Vasantha, S., and P. Sarika. 2019. Empirical analysis of demographic factors affecting intention to use mobile wallet. International Journal of Engineering and Advanced Technology 8: 768–76. [Google Scholar]

- Venkatesh, Viswanath, and Fred D. Davis. 2000. A theoretical extension of the technology acceptance model: Four longitudinal field studies. Management Science 46: 186–204. [Google Scholar] [CrossRef]

- Venkatesh, Viswanath, James Y. L. Thong, and Xin Xu. 2012. Consumer acceptance and use of information technology: Extending the unified theory of acceptance and use of technology. MIS Quarterly 36: 157–78. [Google Scholar] [CrossRef]

- Venkatesh, Viswanath, Michael G. Morris, Gordon B. Davis, and Fred D. Davis. 2003. User acceptance of information technology: Toward a unified view. MIS Quarterly 27: 425–78. [Google Scholar] [CrossRef]

- Wang, Yonggui, Hing-Po Lo, and Yongheng Yang. 2004. An Integrated Framework for Service Quality, Customer Value, Satisfaction: Evidence from China’s Telecommunication Industry. Information Systems Frontiers 6: 325–40. [Google Scholar] [CrossRef]

- Wenzel, Stefanie, and Martin Benkenstein. 2019. The influence of relationship closeness on central motives for joint shopping and satisfaction with the shopping experience among adolescents. SMR-Journal of Service Management Research 3: 126–36. [Google Scholar] [CrossRef]

- Worthington, Steve. 2003. The Chinese payment card market: An exploratory study. International Journal of Bank Marketing 21: 324–34. [Google Scholar] [CrossRef]

- Wu, Jen-Her, and Shu-Ching Wang. 2005. What drives mobile commerce?: An empirical evaluation of the revised technology acceptance model. Information & Management 42: 719–29. [Google Scholar]

- Xu, Fang, and Jia Tina Du. 2018. Factors influencing users’ satisfaction and loyalty to digital libraries in Chinese universities. Computers in Human Behavior 83: 64–72. [Google Scholar] [CrossRef]

- Yaghoubi, Nour-Mohammad, and Ebrahim Bahmani. 2010. Factors affecting the adoption of online banking: An integration of technology acceptance model and theory of planned behavior. International Journal of Business and Management 5: 159–65. [Google Scholar] [CrossRef]

- Yang, Zhilin, and Robin T. Peterson. 2004. Customer perceived value, satisfaction, and loyalty: The role of switching costs. Psychology & Marketing 21: 799–822. [Google Scholar]

- Zeithaml, Valarie A. 1988. Consumer perceptions of price, quality, and value: A means-end model and synthesis of evidence. Journal of Marketing 52: 2–22. [Google Scholar] [CrossRef]

- Zhang, Tingting, Can Lu, and Murat Kizildag. 2018. Banking “on-the-go”: Examining consumers’ adoption of mobile banking services. International Journal of Quality and Service Sciences 10: 279–95. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Constructs | Items | Sources | SRWs | AVE | CR |

|---|---|---|---|---|---|

| PERV | Q2.4. Using M-wallet is convenient | Venkatesh and Davis (2000) Davis (1989) | 0.654 | 0.85 | 0.874 |

| Q2.5. Accomplish financial tasks & payments | 0.921 | ||||

| Q2.37. Spend more time on M-wallet | 0.972 | ||||

| COMP | Q2.7. Using mobile payment services are easy M-wallet | Hayashi and Bradford (2014) Lwoga and Lwoga (2017) | 0.827 | 0.77 | 0.896 |

| Q2.28. Satisfied with the security of M-wallet | 0.781 | ||||

| Q2.10. Familiar with all the transactions | 0.81 | ||||

| Q2.15. Attractive and explanatory. | 0.590 | ||||

| Q2.18. Referred by my family and friends. | 0.849 | ||||

| Q2.23. Trust in mobile wallet apps | 0.763 | ||||

| PERE | Q2.17. M-payment services are beneficial. | Lewis et al. (2016) Zhang et al. (2018) Wenzel and Benkenstein (2019) | 0.891 | 0.85 | 0.928 |

| Q2.35. Using M-wallet when the opportunity arises. | 0.963 | ||||

| Q2.39. Using a mobile payment procedure | 0.704 | ||||

| Q2.40. Always tries to use Mobile wallet. | 0.853 | ||||

| SOCI | Q2.8. Using mobile payment services fits well | Taylor and Todd (1995) Venkatesh and Davis (2000), Venkatesh et al. (2003) | 0.768 | 0.81 | 0.882 |

| Q2.20. using mobile payment services is a good idea | 0.738 | ||||

| Q2.24. My money is not secured in mobile wallet. | 0.832 | ||||

| Q2.34. Frequently use Mobile wallet in the future | 0.897 | ||||

| TRU | Q2.2. Mobile services users have a high profile. | Kim et al. (2010) Schneider et al. (1998) Venkatesh et al. (2003) | 0.886 | 0.78 | 0.863 |

| Q2.36. Availability of access in m payment | 0.927 | ||||

| Q2.19. Will use it because my society people use it. | 0.518 | ||||

| Q2.26. Using M-wallet service gives me satisfaction. | 0.717 | ||||

| SAT | Q2.1. Using m-payment services are prestigious | S. C. Chen (2012), Hossain et al. (2018) | 0.676 | 0.78 | 0.916 |

| Q2.3. Using mobile payment is a status symbol. | 0.819 | ||||

| Q2.6. Mobile wallet is integrated with banking | 0.639 | ||||

| Q2.9. Appreciate using mobile payment services | 0.699 | ||||

| Q2.22. Mobile wallet is safe and has reliable features. | 0.908 | ||||

| Q2.38. Strongly recommends others to use M-wallet. | 0.918 | ||||

| BIs | Q2.12. Using mobile payment system is pleasant. | Davis (1989), Gefen et al. (2003) Venkatesh and Davis (2000) Venkatesh et al. (2012) | 0.759 | 0.77 | 0.902 |

| Q2.14. Banking is fun in mobile wallet. | 0.768 | ||||

| Q2.16. People influence to me for m-payment. | 0.785 | ||||

| Q2.25. Trust this app due to my closed ones. | 0.847 | ||||

| Q2.27. Satisfied with the fees charged in M-wallet. | 0.749 | ||||

| Q2.30. Transfer money to anyone anytime | 0.677 | ||||

| Q2.31. Have a positive attitude toward m-payments. | 0.758 | ||||

| Q2.33. intend to adopt mobile wallet. | 0.792 |

| Factors | PERV | COMP | PERE | SOCI | SAT | TRU | BI |

|---|---|---|---|---|---|---|---|

| PERV | 0.85 | ||||||

| COMP | 0.29 | 0.77 | |||||

| PERE | 0.32 | 0.38 | 0.85 | ||||

| SOCI | 0.22 | 0.32 | 0.24 | 0.81 | |||

| SAT | 0.34 | 0.25 | 0.34 | 0.23 | 0.78 | ||

| TRU | 0.47 | 0.39 | 0.40 | 0.16 | 0.24 | 0.78 | |

| BI | 0.42 | 0.43 | 0.63 | 0.31 | 0.49 | 0.50 | 0.77 |

| Hypothesis | Estimates (β) | p-Value | Supported |

|---|---|---|---|

| H1 Perceived Value—Trust | 0.147 | 0.000 | Yes |

| H2 Perceived Value—Satisfaction | 0.250 | 0.000 | Yes |

| H3 Compatibility—Trust | 0.072 | 0.095 | No |

| H4 Compatibility—Satisfaction | 0.186 | 0.000 | Yes |

| H5 Perceived Enjoyment—Trust | 0.208 | 0.000 | Yes |

| H6 Perceived enjoyment—Satisfaction | 0.177 | 0.000 | Yes |

| H7 Social Influence—Trust | 0.141 | 0.000 | Yes |

| H8 Social Influence—Satisfaction | 0.022 | 0.599 | No |

| H9 Trust—Behavioral Intentions | 0.0429 | 0.000 | Yes |

| H10 Satisfaction—Behavioral Intentions | 0.508 | 0.000 | Yes |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hasan, A.; Sikarwar, P.; Mishra, A.; Raghuwanshi, S.; Singhal, A.; Joshi, A.; Singh, P.R.; Dixit, A. Determinants of Behavioral Intention to Use Digital Payment among Indian Youngsters. J. Risk Financial Manag. 2024, 17, 87. https://doi.org/10.3390/jrfm17020087

Hasan A, Sikarwar P, Mishra A, Raghuwanshi S, Singhal A, Joshi A, Singh PR, Dixit A. Determinants of Behavioral Intention to Use Digital Payment among Indian Youngsters. Journal of Risk and Financial Management. 2024; 17(2):87. https://doi.org/10.3390/jrfm17020087

Chicago/Turabian StyleHasan, Arif, Priyanka Sikarwar, Arun Mishra, Sandeep Raghuwanshi, Abhishek Singhal, Astha Joshi, Prashant Raj Singh, and Abhilasha Dixit. 2024. "Determinants of Behavioral Intention to Use Digital Payment among Indian Youngsters" Journal of Risk and Financial Management 17, no. 2: 87. https://doi.org/10.3390/jrfm17020087