Exploring Competence-Based Synergism in Strategic Collaborations: Evidence from the Global Healthcare Industry

Business Department, RISEBA University of Applied Sciences, Meza Street 3, LV-1048 Riga, Latvia

J. Risk Financial Manag. 2024, 17(3), 93; https://doi.org/10.3390/jrfm17030093

Submission received: 14 January 2024

/

Revised: 18 February 2024

/

Accepted: 20 February 2024

/

Published: 21 February 2024

(This article belongs to the Special Issue Financial Econometrics and Quantitative Economic Analysis)

Abstract

:One of the most essential issues in business partners’ collaboration is whether the integration of their businesses creates a collaborative synergy and adds market value to merging companies. This paper aims to develop a methodological framework that will be convenient for managerial praxis and helpful for scholars’ research in forecasting explicit synergy and valuing tacit synergy in strategic collaborations. The paper theoretically and empirically contributes twofold to strategic foresight. It employs the ARCTIC framework as an extension of the VRIO model to predict an explicit synergy and real options methodology to measure tacit competence-based synergies in M&A deals. The paper makes several theoretical contributions and managerial implications to corporate finance and strategic management disciplines. Finally, the paper discusses research limitations and future work.

1. Introduction

“Synergy makes great business sense, but it may make lousy consumer sense for health care.” Arthur Caplan, the New York University Grossman School of Medicine

A methodical and distinct focus on the future of corporations characterizes foresight (Fergnani 2022, p. 825). Corporate foresight gives a company the flexibility to reorganize its resource base by adding resources from partnerships and acquisitions. However, it can be very difficult to realize the value-creating potential of collaborative solutions (Bower 2001; Schweizer et al. 2022; King et al. 2004). According to the resource-based perspective (RBV), the foundation for adding more value than competitors is the acquisition of rare, valuable, unique, and organized (VRIO) resources (Barney and Hesterly 2015). For instance, it is now standard practice in academic and managerial strategic thinking to build up VRIO resources to increase economic rent (added value) (Lin and Wu 2014). Furthermore, there is still a lack of consensus in the literature addressing the relationship between value-added economic rent and the components of a mechanism that generates synergy through integrating collaborative partners’ VRIO resources and predicting their synergistic implications.

According to Haleblian et al. (2006), King et al. (2004), and Schweizer et al. (2022), most collaborative strategic transactions do not seem to meet expectations, so scholars and practitioners alike have been calling for a deeper understanding of M&A performance. To assess collaborative synergies, Rabier (2017) suggests measuring financial synergies (such as enhancing free cash flows and optimizing the weighted average cost of capital (WACC) and operating synergies (such as revenue growth through new product offerings or cost savings through economies of scale) that are more likely to result in higher operating profit margins (EBIT/net sales). Thus, scholars and practitioners mostly examine explicit synergies between revenue growth and cost savings. But, to achieve tacit synergy, new core competencies must be developed to leverage the VRIO resources of merging partners and generate “value in development” (Hao et al. 2020).

The adoption of this kind of tacit synergy or “value in development” calls for thought from academics and professionals. The purpose of this study is to create a conceptual framework that academics and professionals may utilize to value explicit and tacit synergies in strategic merger and acquisition endeavors. As a result, this study seeks to address two research questions: (1) How does one analyze the prerequisites of explicit competence-based synergism in M&A deals employing the ARCTIC framework? (2) How does one measure a tacit competence-based synergism of M&A deals with the application of real options?

By examining the prerequisites for explicit competence-based synergies using the ARCTIC framework, measuring tacit synergy by exploring the acquisition of One Medical by Amazom.com in 2022 and valuing their collaborative tacit synergies with real options, three real options methodologies, namely, BOPM, BSOPM, and Monte Carlo simulations, were used to empirically addresses the research questions. To answer the first research question, the paper examines explicit competence-based synergies in mergers and acquisitions within the global healthcare industry through the RBV theoretical lens in general and the ARCTIC framework in particular. To answer the second research question, the paper employs methodological quantitative triangulation (Patton 1999; Arias Valencia 2022) that refers to the application and combination of three real options valuation methods in the study of the same phenomenon, namely, “value in development” or tacit synergies.

According to Brandão et al. (2005), investments with option-like characteristics—that is, where the investment’s value is dependent on events occurring over time—can be classified as real options in the widest sense. But, for a real option to be worth something, the management of the firm has to be able and willing to exercise (or actualize) the option when the circumstances are appropriate. This ability is also known as dynamic management capabilities (Helfat and Martin 2014) or (managerial) flexibility or “contingency” (Mun 2003, p. 285; Li et al. 2007). While the term “uncertainty” is used rather generically in the context of real options, it means that it is unclear what a given variable will be worth in the future (Copeland and Keenan 1998a; Triantis and Borison 2001). Uncertainty typically has been associated with potential volatility in the value of an underlying asset or the investment’s cash flow stream (Mun 2002, p. 147; Damodaran 2005).

Flexibility only has a meaningful value when management can respond to uncertainty surrounding an investment (Copeland and Keenan 1998b; Mun 2002, p. 82). Thus, the overall goal of real options theory is to assess management flexibility as a monetary value. Real options have important features that make them more suitable for valuing M&A synergism in a changing environment than common static techniques like discounted free cash flows. Expansion or growth option (invest), abandon option (reject), and deferred option (postpone) are the three various types of options related to M&A deals. While the abandon option is valued as a put option, the growth and deferred options are valued as call options. Consequently, it is possible to value the tacit managerial synergies that result from a merger as a real call option (Čirjevskis 2021c).

The structure of the paper is as follows: It begins by looking at the sources of synergies as well as the importance of the core competencies for M&As’ success. The ARCTIC framework is established based on a profound examination of previously published scholars’ papers on M&A successes and failures. The ARCTIC model that was developed to predict explicit competence-based synergies and generalized in the previous author’s publications is then empirically tested by using a deviant case study as the most intriguing Amazon acquisition in the global healthcare industry, namely, the acquisition of One Medical by Amazon.com in 2022. Next, three real options valuation models, Black–Scholes option pricing model (BSOPM), the binominal option pricing model (BOPM), and Monte-Carlo simulations (MCS), for the assessment of strategic tacit competence-based synergism in M&A are employed and explained in detail. The author addresses theoretical contributions, empirical findings, limitations, and future work at the end of the paper.

2. Key Literature Review

2.1. Foreseeing Explicit and Valuing Tacit Strategic Collaborative Synergism

The strategic compatibility, complementarities, and transferability of core competencies across collaborative partners are factors that contribute to strategic synergism in collaborative endeavors. According to recent research by Hao et al. (2020), two sorts of synergistic effects are related to a business partnership’s strategic collaboration: explicit and implicit. Financial and operational synergies are straightforward to comprehend and measure. They are explicit types of synergies. Explicit synergy arises when business partners reciprocally share complementing core competencies (Zaheer et al. 2013).

Relying on multiple case studies, the ARCTIC framework expanded generalizability (Chirjevskis and Joffe 2007; Čirjevskis 2020, 2021a, 2021b, 2023a). The usefulness of the ARCTIC framework application was measured for a broader set of case studies on strategic collaborative deals, particularly for M&A deals (among them Facebook’s acquisitions of Instagram in 2012 and WhatsApp in 2014, Microsoft’s acquisition of LinkedIn in 2016, and others) and alliances (among them the alliance of Renault–Nissan–Mitsubishi within 1999–2016, and the alliance of Ford and Mazda in 1995). There are several case studies where the ARCTIC framework had predicted competence-based synergies (e.g., the Samsung Electronics acquisition of Harman Industry International in 2017) and where the ARCTIC model had NOT predicted one (e.g., the L’Oreal acquisition of the Body Shop in 2006 and the alliance of Tesco–Carrefour within 2018–2021). That research allowed readers to contrast case studies and grasp how the ARCTIC framework works in greater detail. Because the ARCTIC framework was broadly applicable to many different types of collaborative strategies, the current case study, therefore, is said to have good generalizability.

However, the previously published papers on the ARCTIC framework did not provide an answer to the important question: does the ARCTIC framework predict explicit or tacit types of synergies or both? Understanding the differences between explicit and tacit collaborative synergism was a critical point for the further application and development of the ARCTIC framework. In this vein, the current research argues the ARCTIC framework provides an analytical tool to explore the potential of explicit competence-based synergies. As a result, the current research addresses the question of how to analyze the prerequisites of explicit competence-based synergism in M&A deals employing the ARCTIC framework. Hao et al. (2020) argued that the exchange of core competencies between partners generate “value-in-exchange” or an explicit synergy that can be easily predicted in advance. Therefore, the ARCTIC framework explores the prerequisites and predicts explicit synergies (value-in-exchange) in the process of the exchange of collaborative partners’ core competencies. For example, partnering with IBM brings traceability and transparency to Walmart’s entire food supply network through blockchain (Aitken 2017). Blockchain reduces waste, spoilage, and contamination incidents (Lawrence 2018), thereby facilitating an explicit type of synergy.

However, new core competencies may emerge spontaneously through strategic collaboration and, thus, represent a tacit synergy in real business practice. Hao et al. (2020) referred to this alternating concept of tacit synergy as “value-in-development” (Hao et al. 2020, p. 434). According to Hao et al. (2020), collaborative tacit synergies known as “value in development” occur when partners’ core competencies complement one another and encourage the generation of novel core competencies or ways to create value (Lasker et al. 2001; Hao et al. 2020, p. 433). For instance, Alphabet’s core competencies in high tech and Carrefour’s core competencies in retail grocery have been integrated into new customer value proposition development, thus updating the retailer’s business model, reframing their modes of thinking, and adding tacit synergetic value (Čirjevskis 2022).

To anticipate and recognize a tacit synergy in the process of synthesizing existing core competencies to develop new competencies and, therefore, new competence-based synergies is far more difficult. Partner firms might come from unrelated industries or market areas but entail the potential to inspire each other to develop new core competencies. Tacit synergies cannot be predicted until collaboration has proceeded but can be approximated with the application of the real options. In this vein, the acquisition of One Medical by Amazon.com is a spectacular illustration of tacit synergy. Accordingly, partner businesses’ knowledge bases and their mutual learning, creativity, and managerial flexibility to integrate and build new core competencies constitute the foundation of tacit synergy and “value in development” (Baum et al. 2010; Hao et al. 2020, p. 434). Hence, it is a call for real option application because real options can be used to value managerial flexibility and, thus, tacit synergies.

A real options methodology views collaborative strategy as a set of options that are continuously exercised to produce both short- and long-term returns on co-operation. Furthermore, the author argues that the potential of a tacit competence-based synergy can be approximated by using the real options theory (ROT). The logic behind real options recognizes the importance of strategic managerial flexibility, as well as the possibility of obtaining better returns on investment or, in the case of co-operative strategies, competence-based synergies (Yeo and Qiu 2003). In this vein, real options valuation techniques can be adopted to quantify tacit competence-based synergies in collaborative strategies (Čirjevskis 2021c). Tacit synergy can be pursued when business partners’ knowledge bases spur learning and inspire new core competencies that could not be predicted upfront (Baum et al. 2010) but can be valued as a real option.

Moreover, numerous researchers have recognized foresight methods—in particular, strategic (real) options techniques—as approaches that offer a competitive advantage through the real value of foresight (Fergnani 2022, p. 828). In this line, the following section is devoted to real options reasoning and application because this study is interested in employing real choices theory to quantify collaborative tacit synergies.

2.2. Application of Real Options to Measure Competence-Based Synergies

The management flexibility resulting from M&A transactions is measured by the synergy evaluation inclusion of real options (Loukianova et al. 2017). Consequently, the synergies generated by a merger or acquisition can be viewed as the market value added by the merging business or as a real option value. Additionally, Bruner (2004) emphasized that M&A professionals require real options. The present work incorporates the commonly accepted recommendations of Dunis and Klein (2005, p. 8) on the correspondence of financial options’ parameters to real options as follows:

The cumulative market value of the target and acquirer, or their capitalizations before the announcement, excluding the week of an announcement (four-week average) is the share price (So) equivalent of the option. Market capitalization data are typically accessible through the following websites: https://ycharts.com/ (accessed on 20 February 2024); https://companiesmarketcap.com/ (accessed on 20 February 2024); and other websites. The hypothetical future market value of the separated entities forecast by EV-based (EV/EBITDA and EV/Revenues) multiples is the strike price (E). The volatility (σ) of a share price can be obtained through direct observation or by using the V-Lab APARCH Volatility Analysis. The synergy life cycle or duration of real options (T) is usually one year according to Dunis and Klein (2005). A long-term government bond yield is known as the risk-free rate (Rf).

Following the Black–Scholes option pricing model, the European call option on the market value added of the combined firm represents the competence-based synergies at the moment of real options expiration. Cox et al. (1979) proposed a different method for valuing real options and suggested using the binomial options pricing model (BOPM) to evaluate American options. A competence-based synergy can be valued by time steps within the projected time frame. According to Gilbert (2005), the binomial lattice approach and the American option are the most practical, adaptable, and natural methods for valuing real options. The parameters of the binomial tree can be derived once all input parameters described above have been established. As such, it permits an analyst to evaluate a synergy based on competencies as an American call option in the following manner.

First, the underlying (event tree) lattice needs to be built. The calculation starts at the initial node and moves from left to right until the real options expire. The movement of the underlying asset (S) throughout the real option is depicted by a lattice of the underlying asset. In this work, the author employs EV/EBITDA (Enterprise Value/Earnings before Interest, Taxes, Depreciation, and Amortization) for Amazon.com and EV/Revenue multiples for One Medical to determine the value of the underlying asset at time zero, also known as the PV of the underlying asset (So). Stepping time (δt, ΔT, or Δt) is the interval of time between each time step in the lattice that needs to be calculated (Brealey and Myers 2003; Nembhard and Aktan 2009, p. 24). Second, the real option valuation lattice is constructed and computed from the terminal nodes backward.

The value of the underlying asset will bifurcate at each time step in the lattice, increasing by the up factor (u) and decreasing by the down factor (d). These parameters depend on both the duration of the real option and the implied volatility of the underlying assets (Mun 2003, p. 74). Following the development of the underlying lattice, the real option valuation lattice or decision tree lattice (Copeland et al. 2000, p. 410) has to be built. Real options attain maturity at the terminal nodes, according to Kodukula and Papudesu (2006, p. 79). Therefore, terminal nodes’ real options value needs to be identified by deducting the exercise price—“E” from the share price—“So”.

The value of the embedded real options is then found by back-calculating (also known as “rolling back”) the lattice to the initial node, using a risk-neutral probability formula for the up and down nodes of the real options lattice, as Borison (2005) notes. Hence, the real option valuation lattice is computed back to the first node (where So was initially input) via the backward induction procedure. Real options proponents view the value of the real option in the initial node as the “fair value” of any options (Mun 2003, p. 98). Nevertheless, the primary drawback of BOPM is its computational complexity, as it takes numerous time steps to yield a result that is accurate enough.

Mun (2002, p. 145) states that, when employing binomial lattices, the more time steps, the higher the level of accuracy and, thus, the higher the level of precision. Hull (2005, p. 355) argues that approximately thirty steps produce satisfactory results for financial options. However, Kodukula and Papudesu (2006, p. 96) suggest that, in real option valuation, four to six steps are typically sufficient for good approximations. The stepping time is the duration of each time step or the amount of time that elapses between consecutive nodes (Mun 2002, p. 144). Mun (2002) argued that, to obtain an extended net present value (eNPV), the option value should be added to the NPV of the project that is determined by the discounted cash flow (DCF) approach or, in the case of the current research, the EV/EBITDA and EV/Revenues multiples.

To conclude the literature review part, the net present value (NPV) of the collaborative strategies measures the “value-in-exchange” whereas the real options value approximates the “value-in-development” (Hao et al. (2020). Therefore, the analysts can employ both the NPV without real options application and the eNPV with the application of those by measuring competence-based synergies of collaborative strategies. Lastly, real option valuation is essentially a dynamic form of net present value (NPV) where the discount rate is modified in response to evolving uncertainty and the perceived risk of the deal (Lambrecht 2017, p. 168).

3. Research Design and Methodology

Using a qualitative case study methodology, researchers can investigate complex phenomena in depth within a particular setting (Rashid et al. 2019, p. 1). The research phenomena of the paper are explicit and tacit competence-based collaborative synergies in the context of M&A deals. Seawright and Gerring (2008) argued that case selection in case study research desires (a) a representative sample and (b) useful variation on the dimensions of theoretical interest. When it comes to sampling, according to Eisenhardt and Graebner (2007), it is appropriate to use a single case if a phenomenon-driven research question “how” is subject to investigation. Ultimately, each case can be viewed as a discrete experiment that could be repeated (Yin 2009). Regarding research investigating a single case, Siggelkow (2007) notes that it can be a very powerful example.

Because the main theoretical interest of the current paper is the valuation of collaborative competence-based synergies and its valuation, Amazon.com as a high-tech giant with its ecosystem throughout the world is an appropriate object of current research. When it comes to a unit of research, namely, Amazon’s acquisition of One Medical, this concrete case study is instrumental to answering research questions and reaching the research aim for the following reasons: According to cross-case methods of case selection and analysis (Seawright and Gerring 2008), the case study of the One Medical acquisition can be characterized as a deviant case study that deviates from some cross-case relationships on recent acquisitions of Amazon.com, like the acquisition of Souq.com in Dubai in 2017 and Whole Foods in the US in 2017.

The rationales behind acquiring Dubai-based start-up Souq.com were to enter a new geographic market and to acquire Souq.com’s core competencies, capabilities, and logistic system to navigate a complicated region (MAGNiTT 2017, p. 1). Thus, consumers in the Middle East can buy Amazon.com products using the Souq.com platform (Banerjee 2021). Regarding the highly strategic and not-standard acquisition of Whole Foods by Amazon in 2017, having had limited knowledge and experience in the offline retail environment, Amazon needed to acquire more expertise in perishable grocery procurement and more knowledge of the retail market, improve the management of its supply chain for the offline retail store, and continue investing in R&D for the grocery retail business (Čirjevskis 2023b).

However, having announced in July 2022 Amazon’s decision to acquire One Medical, Amazon has pursued a strengthening of its physical presence in the US healthcare market and an expansion of its online pharmacy business as well as diagnostic business. These acquisitions strongly deviate from previous Amazon strategic acquisitions that pursued new geographic online grocery market development with Souq.com and penetrated the offline grocery market with Whole Foods. The nature of the deviant case study of Amazon’s acquisition of One Medical is exploratory, and the usage of this case study is confirmatory to justify the provided theoretical proposition. Moreover, Seawright and Gerring (2008) argued that one deviant case study can be used as a high-residual case or an outlier.

There are two phases to this study: A deviant case study constitutes the first phase. According to Sekaran and Bougie (2018), the validity of qualitative case study research is determined by how well the findings of the study reflect the data that were gathered (internal validity) and how well they can be applied to different contexts (external validity). One of the main benefits of case study research is that it allows for the investigation of a small number of selected samples, or even one case study, that can be investigated in depth (Yin 1984). The fact that the secondary researcher was not there throughout the data-gathering process and is, therefore, unaware of the precise methods used is a significant drawback of employing secondary data.

However, the clear advantages of adopting secondary data might outweigh its drawbacks (Johnston 2014). According to Smith (2008), the primary benefits of secondary analysis are its cost-effectiveness and ease. Not all the data gathered were used in the original survey study; however, the data that are not used can offer new insights or answers to unanswered questions (Smith 2008). According to Andrews et al. (2012) and Smith (2008), there is increasing evidence that using pre-existing secondary data for study is possible in an era where academics worldwide are gathering and archiving large amounts of data.

Regarding evidence presentation, Eisenhardt and Graebner (2007) assert that there is no rigid standard for findings presentation, unlike in large-scale investigations, because of the abundance of data that accumulate throughout the case study. As a result, the first phase of the current study uses the findings from deviant case studies as well as scholars’ publications to demonstrate how the ARCTIC framework to assess the prerequisites of explicit synergies is applied. One tool that can be used to prepare existing data is contextual positioning.

In grounded theory research, the author used pertinent secondary documents to develop the ARCTIC framework, employing the contextual positioning approach (Ralph et al. 2014). To gain a micro-level understanding that enhances the operationalization of the ARCTIC framework, the current study relies on a thorough literature review and archival search that includes financial statements, annual reports, internal papers, industry publications, and CEO statements.

This has been accomplished by using contextual positioning to position the extant data of the inductive case study. This has allowed the author to identify the critical success factors (prerequisites) of competence-based synergy and codify them in the ARCTIC framework. As a result, contextual positioning makes the process of gathering data more interactive. In practice, the process is broken down into the following two stages. Using the VRIO framework, the target and acquirer companies’ core competencies are determined in the first stage.

As a result, the VRIO framework makes it possible to pinpoint merging organizations’ core competencies as the foundation of their long-term competitive advantages. Next, an analysis of the core competencies complementarity, compatibility, and transferability with the ARCTIC framework is the second stage. The purpose of the ARCTIC framework application is to assess whether the core competencies of partners can be sources of strategic explicit synergism in the M&A deal.

Furthermore, the second phase of the case study involves utilizing a real options valuation technique to value the strategic tacit synergism of the M&A deal. The tacit competence-based synergies in the M&A deal are measured as an added market value using real options application involving the Black–Scholes option pricing model (BSOPM); the binominal option pricing model (BOPM), and the Monte Carlo methodology, thereby achieving methodological triangulation (Patton 1999) to test the validity of the measurement of strategic tacit synergism in M&A deals and obtaining the convergence of valuation results from different quantitative methods (Arias Valencia 2022).

The first valuation model used for this step was based on the Black–Scholes option pricing model (Black and Scholes 1973), namely, C (S, t) = S0 × N(d1) − K × e−rT × N(d2), where N(d1), N(d2) are the cumulative distribution functions of the standard normal distribution; C (S, t) is call option price at time t; S0 is the price of the underlying asset at time 0; K is the exercise price at time t; T is time in years; r is a risk-free rate; e is a mathematical constant approximately equal to 2.71828, the base of the natural logarithm; and σ is expected volatility of an underlying asset’s value.

The Black–Scholes option-pricing model’s variables, binomial option pricing model, and Monte Carlo’s parameters to measure the strategic tacit synergism of Amazon and One Medical deal are further discussed in the case study research. The BOPM is used to quantify the value of strategic synergism and, hence, the market value added to the M&A deal.

To answer the first research question of how to analyze the prerequisites of explicit competence-based synergism in M&A deals employing the ARCTIC framework, the methodology is discussed in the next sub-chapter.

Competency-Based Explicit Synergy Testing Using the ARCTIC Research Framework in Mergers and Acquisitions: A Methodology

Employing the six criteria (questions) of the ARCTIC research framework is comparable to employing the VRIO framework. The ARCTIC framework’s first three criteria address the possible complementarity and compatibility of core competencies in a recently merged firm, and they closely resemble the VRIO framework’s first three criteria. Put another way, the first three criteria evaluate the extent to which consumers value core competencies (external relatedness), rare and difficult to imitate by rivals (internal advantages), and can be integrated by a target’s or acquirer’s businesses (absorption capacity).

According to Penrose (1959) and Rugman and Verbeke (2002), “competencies lead to sustained superior returns”; thereby, the first three criteria (“A”, “R”, and “C”) also line up with their statement. According to Larsson and Finkelstein (1999), employee support for the joining firms’ integration and the level of organizational integration following the deal’s completion were key factors in determining how much a merger or acquisition produced synergistic benefits. Consequently, the following three criteria (“T,” “I”, and last “C”) center on the integration process of two sets of core competencies.

Furthermore, Penrose (1959) noted that businesses profit from the “services of resources”—that is, from how they use resources—rather than from having resources in and of themselves. Thus, an assessment of the processes of the transfer and integration of core competencies throughout the M&A deal can be carried out by employing the following three criteria. Therefore, the last three criteria also align with Penrose’s (1959) arguments, namely, the time (duration) of integration of core competencies, the integration plan, and cultural fit. The core competencies of both collaborative partners must meet all six requirements, or the six critical success factors, to generate competence-based synergy during the M&A process. All criteria, which are presented as questions, should, of course, be thoroughly explained.

“A” stands for Internal Advantage. Is it necessary to enhance the core competencies of one company (the target company) to foster complementarity with the acquiring company and support competence-based synergies? The answer is “Yes”, if competence is uncommon and challenging for many rivals to copy, and taking advantage of it would produce competence-based synergy during the merger and acquisition process (Hitt et al. 2009; Bauer and Matzler 2014).

“R” stands for External Relatedness. The answer is “No” if the core competencies do not offer a novel value proposition to the consumer, and the core competencies of the other partner are not connected to the market demand externally. If the core competencies enable the businesses to adapt to environmental challenges or threats, offer value to customers, and facilitate the creation of new customer value propositions, then the answer is “Yes” (Bauer and Matzler 2014). This is the second aspect of synergy potential in a transaction.

“C” stands for the ability to merge business and absorb core competencies. Each competency has a certain level of complexity that makes it difficult for partners and competitors to transmit, as well as each partner possessing different absorption capabilities. Although having core competencies that are relevant, beneficial, and valuable for the other business is important, it might not be enough. The answer to the complexity issue is “No”, as this would hinder competence-based synergy if fundamental competencies are too complex for the other organization to readily absorb (Hitt et al. 2009; Bauer and Matzler 2014). The answer is “Yes” if the other company’s appropriation of core competencies is not as costly and time-consuming and is quite fast to absorb and take advantage of. This is the third component of the M&A process’s potential for synergy.

“T” stands for Integration Time. Perhaps the most important factor in determining how well acquisitions create synergy is how quickly the process of exchanging knowledge and integrating core competencies takes. Research has demonstrated that an acquisition’s chances of success decrease with the length of time it takes for integration to take place and for operations to begin operating consistently (Netz et al. 2019; Spanner et al. 1993). The answer is “No” if rare and valuable core competencies transfer so slowly as to be rendered useless. Thus, the answer is “Yes” if the transfer of fundamental abilities happens quickly. This is the M&A process’s fourth possible synergy component.

“I” is also known as the post-merger Integration Plan of core competencies. When senior management assesses a possible acquisition, at least a few realistic implementation stages must have been planned. Post-merger integration is a very complicated topic that requires careful planning, successful execution, and efficient management (Hitt et al. 2009; Bauer and Matzler 2014). A post-merger integration plan should include mechanisms for co-ordination, a plan for training and development, an effective communication strategy amongst M&A transaction teams, and the establishment of mutual trust. The answer is “yes” if the acquirer has a well-defined plan that both parties support. Once more, when a business enters the M&A process without a defined plan to pursue, the probability of competence-based synergy is reduced, and the answer is “No”.

“C” refers to Cultural Fit of Core Competencies. Lastly, the degree to which core competencies align with the culture of the other organization should be evaluated. The response is “Yes” if the organization’s senior management teams and employees of a target and acquirer will embrace and absorb the new cultural contexts (Bijlsma-Frankema 2001; Lodorfos and Boateng 2006; Nguyen and Kleiner 2003). But the response is “No” if there is cultural misfitting or incompatibility. This makes up the sixth component of the M&A process’s potential for synergy.

Rabier (2017) suggests quantifying synergies by mostly using quantitative methods to evaluate synergies in terms of income and expense, therefore, quantifying “value-in-exchange” or an explicit synergy. However, the valuation of competence-based synergies is far more difficult since certain success elements cannot be measured numerically in terms of revenues and costs. The two partners’ mutual trust, interpersonal relationships, methods of communication, clear organizational structures, the absorption capacities (a willingness to learn rather than substitute) of the acquirer and the target, and managerial flexibility are hard to quantify in terms of operating or net profit margins.

The “value-in-development” or tacit competence-based synergies in M&A can be measured as market value added by employing a real options valuation technique. With an application of real options valuation, it becomes easier to assess a tacit synergy in terms of market value added, first. Second, practitioners gain a clearer strategic observation of a tacit synergism valuation of the M&A deal as a result of the application of real options. After developing theoretical reasons, the author has chosen the deviant case study to test the technique of the ARCTIC framework empirically: Amazon.com’s acquisition of One Medical in 2022.

4. Case Study: Amazon.com Acquisition of One Medical, Data Analysis, and Interpretation of Results

This case study examines a phenomenon (the ARCTIC framework and real option valuation application) in the M&A deal: Amazon.com’s acquisition of One Medical in 2022. Research using a single case study has the potential to shed light on hidden factors by investigating the phenomenon’s underlying causes and improving our comprehension of “how” things work (Fiss 2009; Yin 2018).

4.1. Justifications for Amazon.com’s Decision to Purchase One Medical and the Effect of Core Competencies on Collaborative Synergies

On 21 July 2022, Amazon (NASDAQ: AMZN) and One Medical (NASDAQ: ONEM) entered into a definitive merger agreement under which Amazon will acquire One Medical for $ 3.9 bn. Headquartered in San Francisco, CA, USA, 1Life Healthcare, Inc. is the administrative and managerial services company for the affiliated One Medical physician-owned professional corporations that deliver medical services in-office and virtually. 1Life and the One Medical entities do business under the “One Medical” brand. The rationale behind this was to gain access to One Medical’s more than 200 brick-and-mortar medical offices in 26 markets, and roughly 815,000 members (Palmer 2023). Having disclosed its plan to cease the operations of Amazon Care, Amazon has acquired One Medical to deepen its presence in health care, and dramatically improve the experience of obtaining medical care.

4.2. Estimating Prerequisites of Explicit Strategic Synergism in Amazon.com’s Acquisition of One Medical

Amazon has long had ambitions to expand into health care, buying online pharmacy PillPack in 2018 for $750 million, then launching its virtual clinic for chronic conditions and prescription perks for Prime members (Palmer 2023). Previous success in deals of a similar nature, such as Walgreen’s acquisition of VillageMD in 2020 and Cigna’s acquisition of MDLive in 2021, further point to probable success (Lee et al. 2022). The prediction of strategic synergism is given in Table 1.

It is now possible to provide a succinct and accurate summary of the case study data, their interpretations, and the empirical conclusions. The competence-based synergies have six conditions, as determined by the ARCTIC framework. One Medical is a human-centered, tech-driven U.S. primary care organization that makes quality healthcare more accessible, affordable, and pleasurable by combining in-person, online, and virtual care services seamlessly. Amazon is the largest online retailer in the world (Amazon 2022).

As a result, the complementarity (A and R) and compatibility (C and T) of both companies’ fundamental competencies are present. Neil Lindsay, SVP of Amazon Health Services, stated that the two businesses operated in complementary ways (“A” and “R”):

“Together, we believe we can make the health care experience easier, faster, more personal, and more convenient for everyone … We believe we can and will help more people get better care, when and how they need it”.

Concerning the degree to which the core competencies of the two businesses may be absorbed by the other and the amount of time it takes to integrate and utilize them (first “C” and “T”), One Medical CEO Amir Dan Rubin reports the following:

“We look forward to innovating and expanding access to quality healthcare services, together”.

Moreover, Neil Lindsay, senior vice president of Amazon Health, added in November 2023 the following:

“We are bringing One Medical’s exceptional experience to Prime members—it’s health care that makes it dramatically easier to get and stay healthy”.

Regarding the transferability of key competencies regarding integration issues throughout their corporate cultures (the “I” and final “C”), Sanjula Jain, Ph.D., chief research officer and senior vice president of market research company Trilliant Health, stated the following:

“… Amazon’s revised virtual care strategy will likely align with what the data shows: integrating virtual care within an in-person care delivery platform, which is what One Medical offers and one focused more on going directly to a specific segment of consumers.”

Moreover, Amir Dan Rubin, CEO of One Medical, argued the following:

“The opportunity to transform health care and improve outcomes by combining One Medical’s human-centered and technology-powered model and exceptional team with Amazon’s customer obsession, history of invention, and willingness to invest in the long-term is so exciting”

“We join Amazon with its long-term orientation, history of invention, and passion for reimagining a better future… Together, we believe we can make the health care experience easier, faster, more personal, and more convenient for everyone”

Amazon CEO Andy Jassy has added the following:

“Health care will be a major growth area for Amazon, even as the company has reined in spending”.

The ARCTIC analysis has helped to answer the first research question: How does one analyze the prerequisites of explicit competence-based synergism in M&A deals employing the ARCTIC framework? The ARCTIC framework has justified that Amazon.com’s acquisition of One Medical was a highly synergetic deal. Competence-based synergies can also be realized quickly between the care delivery side and pharmacy side with Amazon’s significant assets of technology, consumer platform, and delivery network. The acquisition can foster synergies, helping the success of Amazon’s medical business. (Lee et al. 2022)

Moreover, One Medical was convinced of the following:

“Amazon and One Medical have extensive experience protecting data of all kinds appropriately across a variety of businesses and nothing about this acquisition changes Amazon or One Medical’s commitment to privacy or the strong protections we have for Protected Health Information”

4.3. Valuation of Strategic Synergism by Using Binominal Option Pricing Model (BOPM): Amazon.com’s Acquisition of One Medical

To address “a valuation” in the subsequent part of the research question, the real options parameters have been computed following the recommendations of Dunis and Klein (2005). Furthermore, the real options parameters and data are given in detail in Table 2 and Table 3.

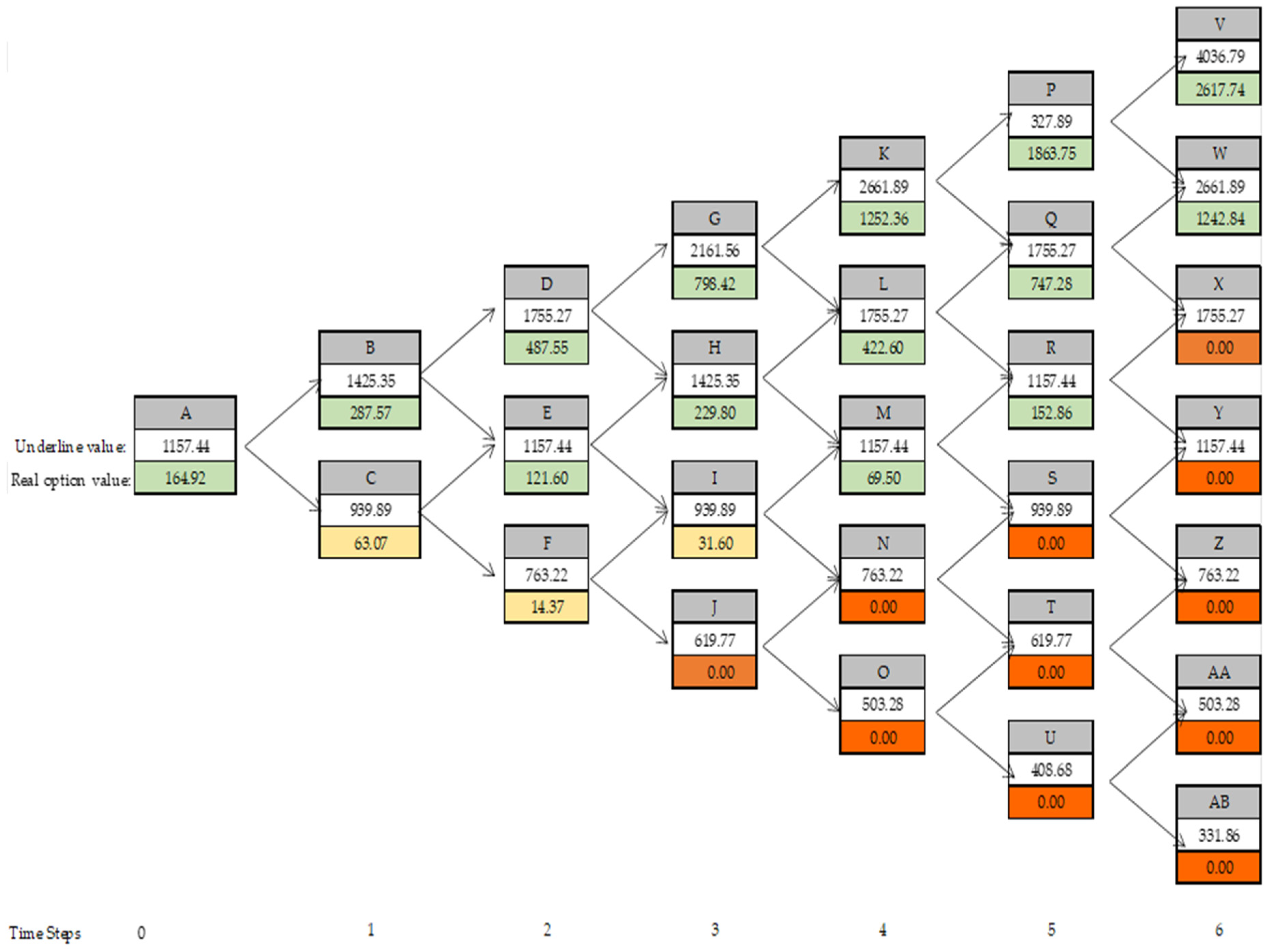

Using Excel spreadsheets, the value of the competence-based synergies of One Medical’s acquisition by Amazon.com in 2022 has been determined by employing BOPM, as seen in Figure 1.

As demonstrated in Figure 1, the binomial option pricing model (BOPM) offers a clear explanation and illustrates how M&A uncertainty, which is represented by implied volatility, affects option value over time. The acquisition of One Medical by Amazon.com has resulted in competence-based synergies valued at USD 164.92 billion.

As the next real option by following the methodological triangulation, the author employed the Black–Scholes option pricing model (BSOPM) as shown in Table 2. Parameters of BSOPM variables to value tacit competence-based synergies of Amazon and One Medical are given in Table 4.

Based on the BSOPM valuation results, Amazon.com would add market value through the acquisition of One Medical of around US$ 155.84 billion, as shown in Table 4.

Finally, the tacit synergetic result was generated by using a Monte Carlo simulation, where Excel forecasted the call option value for Amazon’s acquisition of the One Medical case based on the real option parameters discussed above. The option life of one year was divided into six steps for binominal lattices, and the number of simulations was 100,000 times. The simulation results from a custom-made spreadsheet showed an average real option value of US$ 157.23 billion, which is quite close to the BSOPM result as given in Table 5.

Now, the result of the Monte Carlo pricing of the European call option can be collated with the results from a Black–Scholes option pricing model and binomial option pricing model. The call option is in the money if the market value of the merged entity exceeds the expected future market value of the two separate companies (Dunis and Klein 2005, p. 6). According to the BS-OPM, BOPM, and Monte Carlo results, Amazon.com would have added an increased market value of about $155.84–164.92 billion.

Therefore, the expected market value of merging Amazon.com and One Medical was calculated as their market capitalizations after the announcement of the acquisition (So) of $1157.44 bn plus a tacit competence-based synergy of around $162.38 bn, equaling the theoretical market value of $1319.82 bn. As of 26 July 2023, Amazon’s market capitalization was 1322.0 billion (YChart 2022), which was approximately equal to the market value added predicted using a mean of the three real option values.

Thereby, the author has provided the answer to the second research question of how to measure a tacit competence-based synergism of M&A deal with the application of real options. Real options are incorporated into the synergy value to account for management flexibility resulting from mergers and acquisitions. In this vein, real options applications employing BSOPM, BOPM, and MCS methods can be used to quantify dynamically the tacit competence-based synergies in M&A deals.

While the binomial lattices approach is the most convenient, flexible, and intuitive in valuing real options, the BS-OPM and MCS approaches provide highly accurate and quick real options valuation results. Several scholars’ studies have demonstrated that both the Monte Carlo simulation and the binomial models converge to the Black–Scholes option pricing value (Hon 2013). In this vein, the paper contributes to this conversation by justifying Hon’s (2013) arguments with fresh empirical results.

Research does, however, also highlight the limitations of using real options to gauge the collaborative synergy of acquisitions of businesses. When multiple acquisitions occur in anticipation of the time of generating synergies of one concrete deal, whereas Amazon did effectively accomplish several deals in the same 2022 year, such as the acquisitions of iRobot in the UK, Cloostermans in Belgium, and Spirit.ai in the UK, it becomes challenging to justify the synergistic effect of a single isolated purchase agreement using real market capitalization. Yet, despite this limitation, the theoretical contribution and managerial implication of the paper are discussed in the next section.

5. Discussion and Contributions

Corporate foresight is a methodical and well-defined approach to a company’s future (Fergnani 2022, p. 825). It guarantees chances to restructure an acquirer firm’s core competencies by integrating the unique resources and dynamic capabilities of a target company (Čirjevskis 2023a), resulting in the creation of added value for the market. However, it can be highly challenging to put collaborative strategies’ value-creating potential into practice (Bower 2001; King et al. 2004; Schweizer et al. 2022). In the most significant domains for future research on corporate foresight, Fergnani suggests the following path of mediation: corporate foresight > resource-based modifications > new business potential > performance (Fergnani 2022, p. 836).

This research offers a fresh theoretical and empirical contribution to the foresight of an explicit competence-based synergy in international collaborative ventures from the resource-based view and assesses a tacit competence-based synergy by using real options valuation. This is the paper’s primary theoretical contribution. Additionally, the study adds several theoretical and managerial contributions to the fields of financial management and strategic management as follows:

5.1. The Theoretical Contribution

First, this paper contributed to the scientific recommendation of Fergnani (2022, p. 836) by operationalizing the following discourse on mediation paths of foresight: corporate foresight (collaborative strategies) → new business opportunities (employing VRIO analysis to explore VRIN resources and capabilities of collaborative business partners) → resource-based changes (exploring an explicit collaborative synergy with the ARCTIC framework) → performance (valuing a tacit collaborative synergy with real options). This mediation path can be useful in future quantitative research.

Second, by offering the ARCTIC framework as an expansion of the VRIO model (Barney and Hesterly 2015, this paper contributes to the field of corporate foresight research by enabling the prediction of an explicit competence-based synergy in collaborative ventures and the valuation of a tacit collaborative synergy using real options theory.

Third, by connecting financial management research on value-adding praxis with real options application and strategic management research on collaborative synergism with the ARCTIC framework application, the paper thereby contributes to multidisciplinary research. Furthermore, by examining the case study of the One Medical acquisition by Amazon.com, this paper contributes to real options theory by examining whether the target’s core competencies may impact an acquirer’s core competencies in a synergistic way and by providing an example of the tacit strategic synergism measurement process with real options.

Fourth, the application of the ARCTIC framework to the deviant case study justifies that the framework fulfills its purpose and contributes to the pre-acquisition and post-acquisition examination of competence-based explicit synergies in M&A transactions, and this is the main theoretical and managerial contribution to the challenges of global M&A deals.

5.2. The Managerial Implication

The adoption of formal real option valuation models by practitioners appears to be lagging, even though the academic literature on real options has grown enormously over the past three decades (Lambrecht 2017, p. 166). The problem with most strategic decisions is that they are frequently made only based on qualitative information and strong intuition (Kyläheiko et al. 2002). At least in high-tech-based M&A transactions, it becomes possible to obtain more transparency into strategic decisions and make the results of competence-based synergies measurable with the use of pertinent quantitative information about merging companies and real options variables.

As such, this study contributes to both real options theory and the development of the ARCTIC framework by bridging them onto a new theoretical level and by providing a practical managerial example to support the theoretical proposition. The author used the real option application BSPOM, BOPM, and MCS methods as methodological triangulation, which can be easily understood by managers. While the binomial lattices approach is the most convenient, flexible, and intuitive in valuing real options, the BSOPM and Monto Carlo simulation (MCS) provide highly accurate and quick ROV results. However, BSOPM is impossible and MCS is quite hard to apply to American options (Čirjevskis 2021d).

Furthermore, the BOPM model serves as a “road map” and a tool for valuation. Thus, a clearer strategic observation of the reciprocal synergism of an M&A deal can be made by practitioners when valuing managerial tacit synergies employing real options in M&A deals and applying three real options methods. This is the current paper’s main managerial implication.

When it comes to limitations, Lambrecht argues that real options valuation due to its complexity is not a particularly flexible valuation framework as managers cannot in advance identify the firm’s real options but have to discover and exercise them as uncertainty unfolds (Lambrecht 2017, p. 168). In addition, Liu and Ronn argued that when the number of simulation paths is small and when the number of exercise opportunities is large, the Monte Carlo simulation will have poor performance (Liu and Ronn 2020, p. 3). The BOPM model provides a more favorable condition to be applied in strategic collaborative projects where the execution time could be at any time (Guo and Zhang 2020).

6. Conclusions

The application of the ARCTIC framework contributes to a resource-based view on strategy (Barney and Hesterly 2015) in the domestic and global contexts of collaborative ventures. This goes beyond the application of VRIO resources to the operations of an individual corporation in individual foreign countries (Kogut 1991; Ghemawat 2007). The six ARCTIC framework success factors—which allow one to anticipate explicit competence-based synergies of combined ventures—have been validated by several case studies research.

Furthermore, the ARCTIC framework assisted in anticipating the prerequisites needed for the Amazon and One Medical merger’s explicit synergies, demonstrating how the collaborative partners could reciprocally forge an explicit competence-based synergy as a result of the complementarity (A, R), compatibilities (first C), and transferability (T, I, and second C) of their core competencies. Hence, the ARCTIC framework’s six success aspects facilitate an initial prediction of explicit competence-based synergies in co-operative arrangements, alliances, mergers, and acquisitions.

Moreover, the tacit competence-based synergy of this collaborative exchange was assessed through the application of different real options. Although scholarly literature on real options has expanded significantly over the past three decades, the adoption of formal real options valuation models by practitioners seems to be behind (Lambrecht 2017, p. 166). Regarding managerial contribution, practitioners can use the real options valuations to measure tacit competence-based synergies, and the first is lattices of BOPM that were presented in research as “a road map” to quantify merging firms’ values and competence-based synergies in M&A transactions.

The problem with most strategic decisions is that they are frequently made only based on qualitative information and strong intuition (Kyläheiko et al. 2002). According to Kyläheiko et al. (2002), the real options method can result in a twofold improvement in strategic managerial practice: it foresees the corporate future and provides a quantified appraisal of strategic management decisions. Even though the literature on financial management has long included the “real option” viewpoint, Lambrecht (2017) argues that research on real options has only looked at a small number of strategic praxes. Lambrecht put forth the notion that perhaps more diverse industries and investment opportunities will be the focus of future real options research (Lambrecht 2017, p. 170). By offering a novel perspective on the state-of-the-art managerial practice of M&As that deals with the use of real options valuation, the author contributes to this scientific request in the current paper.

This paper also presents an avenue for future research to explore the role of dynamic capacities (Teece et al. 1997) in the strategic synergism generation in M&A deals in greater detail. Specifically, the dynamic capabilities (DC) view needs to be examined concerning the deployment of real options theory, making DC more measurable. Ultimately, real option valuation is both an art and a science since it blends business strategy and corporate finance (Lambrecht 2017).

More cross-disciplinary research on strategic foresight is needed, that can thus address and contribute to the influencing mechanisms of the synergistic impacts of M&A deals in detail and advance real options valuation perspectives to broader business and scholar societies. Several hypotheses might be developed from the provided proposition and proposed extended mediation paths (Fergnani 2022) for the novel empirical testing of an explicit and tacit collaborative synergies phenomenon with a larger sample size and quantitative research techniques.

Further research may explore and make contributions to associated issues about the prerequisites and governing mechanisms of the implicit synergistic impacts and real options application perspectives in this regard. Additionally, the paper offers a platform for future research that can further the empirical study of the tacit synergism of strategic collaboration with more complex real options applications techniques (e.g., sequential compound, with changing volatilities, and rainbow with multiple uncertainties) and deepen the scientific discussion on the issues raised.

Funding

This research received no external funding.

Data Availability Statement

Publicly available datasets were analyzed in this study. These data can be found in the reference list.

Conflicts of Interest

The author declares no conflict of interest.

References

- Aitken, Roger. 2017. IBM & Walmart Launching Blockchain Food Safety Alliance in China with Fortune 500’s JD.com. Forbes. Available online: https://www.forbes.com/sites/rogeraitken/2017/12/14/ibm-walmart-launching-blockchain-food-safety-alliance-inchina-with-fortune-500s-jd-com/?sh=2c6ba6fd7d9c (accessed on 24 June 2022).

- Amazon.com. 2022. Available online: https://press.aboutamazon.com/2022/7/amazon-and-one-medical-sign-an-agreement-for-amazon-to-acquire-one-medical (accessed on 8 January 2024).

- Andrews, Lorraine, Agnes Higgins, Michael Waring Andrews, and Joan G. Lalor. 2012. Classic grounded theory to analyze secondary data: Reality and reflections. The Grounded Theory Review 11: 12–26. [Google Scholar]

- Arias Valencia, María Mercedes. 2022. Principles, Scope, and Limitations of the Methodological Triangulation. Investigación y Educación en Enfermería 40: e03. [Google Scholar] [CrossRef]

- Banerjee, Arindam. 2021. Amazon’s Acquisition of Souq.com: Synergies in the GCC Region. Journal of International Business Education 16: 1–8. [Google Scholar]

- Barney, Jay B., and William S. Hesterly. 2015. Strategic Management and Competitive Advantage: Concepts and Cases, Global ed. Harlow: Pearson Education Limited, Edinburgh Gate Harlow, p. 385. [Google Scholar]

- Bauer, Florian, and Kurt Matzler. 2014. Antecedents on M&A success: The role of strategic complementary, cultural fit, and degree and speed on integration. Strategic Management Journal 35: 269–91. [Google Scholar]

- Baum, Joel, Robin Cowan, and Nicolas Jonard. 2010. Network independent partner selection and the evolution of innovation networks. Management Science 56: 2094–110. [Google Scholar] [CrossRef]

- Bijlsma-Frankema, Katinka. 2001. On managing cultural integration and cultural change processes in mergers and acquisitions. Journal of European Industrial Training 25: 192–207. [Google Scholar] [CrossRef]

- Black, Fischer, and Myron Scholes. 1973. The Pricing of Options and Corporate Liabilities. Journal of Political Economy 81: 637–54. [Google Scholar] [CrossRef]

- Borison, Adam. 2005. Real options analysis: Where are the emperor’s clothes? Journal of Applied Corporate Finance 17: 17–31. [Google Scholar] [CrossRef]

- Bower, Joseph L. 2001. Not all M&As are alike—And that matters. Harvard Business Review 79: 92–101. [Google Scholar] [PubMed]

- Brandão, Luiz E., James S. Dyer, and Warren J. Hahn. 2005. Using Binomial Decision Trees to Solve Real-Option Valuation Problems. Decision Analyses 2: 69–88. [Google Scholar] [CrossRef]

- Brealey, Richard A., and Stewart C. Myers. 2003. Principles of Corporate Finance, 7th ed. New York: McGraw-Hill Companies, Inc., pp. 13–34. [Google Scholar]

- Bruner, Robert F. 2004. Applied Mergers and Acquisitions. New York: John Wiley & Sons. [Google Scholar]

- BSIC. 2017. Bocconi Students’ Investment Club. Amazon of Arabia: Jeff Bezos’ Giant Buys Souq in a Move to Enter the Middle East Market. Available online: https://bsic.it/amazon-arabia-jeff-bezos-giant-buys-souq-move-enter-middle-east-market/ (accessed on 17 December 2022).

- Chirjevskis, Andrejs, and Lev Joffe. 2007. How to Create Competence-based Synergy in M&A. The ICFAI Journal of Mergers & Acquisitions 4: 43–61. [Google Scholar]

- Čirjevskis, Andrejs. 2020. Valuing reciprocal synergies in merger and acquisition deals using the real options analysis. Administrative Sciences 10: 27. [Google Scholar] [CrossRef]

- Čirjevskis, Andrejs. 2021a. Brazilian Natura & Co: Creating cosmetic powerhouse. Empirical evidence of competence-based synergies in M&A processes. Academia Revista Latinoamericana de Administración 34: 18–42. [Google Scholar]

- Čirjevskis, Andrejs. 2021b. Exploring Critical Success Factors of Competence-Based Synergy in Strategic Alliances: The Renault–Nissan–Mitsubishi Strategic Alliance. Journal of Risk and Financial Management 14: 385. [Google Scholar] [CrossRef]

- Čirjevskis, Andrejs. 2021c. Exploring the Link of Real Options Theory with Dynamic Capabilities Framework in Open Innovation-Type Merger and Acquisition Deals. Journal of Risk and Financial Management 14: 168. [Google Scholar] [CrossRef]

- Čirjevskis, Andrejs. 2021d. Value Maximizing Decisions in the Real Estate Market: Real Options Valuation Approach. Journal of Risk and Financial Management 14: 278. [Google Scholar] [CrossRef]

- Čirjevskis, Andrejs. 2022. A Discourse on Foresight and the Valuation of Explicit and Tacit Synergies in Strategic Collaborations. Journal of Risk and Financial Management 15: 305. [Google Scholar] [CrossRef]

- Čirjevskis, Andrejs. 2023a. Managing competence-based synergy in acquisition processes: Empirical evidence from the ICT and global cosmetic industries. Knowledge Management Research & Practice 21: 41–50. [Google Scholar]

- Čirjevskis, Andrejs. 2023b. Measuring dynamic capabilities-based synergies using real options in M&A deals. International Journal of Applied Management Sciences 15: 73–85. [Google Scholar]

- CompaniesMarketcap.com. 2024. Available online: https://companiesmarketcap.com/one-medical/marketcap/ (accessed on 8 January 2024).

- Copeland, Thomas E., and Philip T. Keenan. 1998a. How much is Flexibility Worth? The McKinsey Quarterly 2: 38–49. [Google Scholar]

- Copeland, Thomas E., and Philip T. Keenan. 1998b. Making real options real. The McKinsey Quarterly 3: 128–41. [Google Scholar]

- Copeland, Thomas E., Tim Koller, and Jack Murrin. 2000. Valuation: Measuring and Managing the Value of Companies, 3rd ed. Hoboken: John Wiley & Sons, pp. 339–410. [Google Scholar]

- Cox, John C., Stephen A. Ross, and Mark Rubinstein. 1979. Option Pricing: A simplified approach. Journal of Financial Economics 7: 229–63. [Google Scholar] [CrossRef]

- Damodaran, Aswath. 2005. The Promise and Peril of Real Options. Available online: https://archive.nyu.edu/bitstream/2451/26802/2/S-DRP-05-02.pdf (accessed on 17 February 2024).

- Dunis, Christian L., and Til Klein. 2005. Analyzing mergers and acquisitions in European financial services: An application of real options. European Journal of Finance 11: 339–55. [Google Scholar] [CrossRef]

- Eisenhardt, Kathleen M., and Melissa E. Graebner. 2007. Theory building from cases: Opportunities and challenges. Academy of Management Journal 50: 25–32. [Google Scholar] [CrossRef]

- Fergnani, Alessandro. 2022. Corporate foresight: A new frontier for strategy and management. Academy of Management Perspectives 36: 820–44. [Google Scholar] [CrossRef]

- Finbox.com. 2024. Available online: https://finbox.com/NASDAQGS:AMZN/explorer/ev_to_ebitda_ltm/ (accessed on 8 January 2024).

- Fiss, Peer C. 2009. Case studies and the configurational analysis of organizational phenomena. In The SAGE Handbook of Case-Based Methods. Edited by David Byrne and Charles C. Ragin. London and Thousand Oaks: Sage, pp. 424–40. [Google Scholar]

- Fowler, Geoffrey A. 2022. Amazon just bought my doctor’s office. That makes me very nervous. The Washington Post. Available online: https://www.washingtonpost.com/technology/2022/07/22/amazon-one-medical-privacy/ (accessed on 8 January 2024).

- Ghemawat, Pankaj. 2007. Managing differences: The central challenge of global strategy. Harvard Business Review 85: 58–68. [Google Scholar]

- Gilbert, Evan. 2005. Investment basics XLIX. An introduction to real options. Investment Analysis Journal 60: 49–52. [Google Scholar] [CrossRef]

- Guo, Kai, and Limao Zhang. 2020. Guarantee optimization in energy performance contracting with real options analysis. Journal of Cleaner Production 258: 120908. [Google Scholar] [CrossRef]

- Haleblian, Jerayr, Ji-Yub Kim, and Nandini Rajagopalan. 2006. The influence of acquisition experience and performance on acquisition behavior: Evidence from the U.S. The commercial banking industry. Academy of Management Journal 49: 357–70. [Google Scholar] [CrossRef]

- Hao, Bin, Jiangfeng Ye, Yanan Feng, and Ziming Cai. 2020. Explicit and tacit synergies between alliance firms and radical innovation: The moderating roles of interfirm technological diversity and environmental technological dynamism. R&D Management 50: 432–46. [Google Scholar]

- Helfat, Constance E., and Jeffrey A. Martin. 2014. Dynamic Managerial Capabilities: Review and Assessment of Managerial Impact on Strategic Change. Journal of Management 41: 1281–312. [Google Scholar] [CrossRef]

- Hitt, Michael A., David King, Hema Krishnan, Marianna Makri, Mario Schijven, Katsuhiko Shimizu, and Hong Zhu. 2009. Merger and acquisition: Overcoming pitfalls, building synergy, and creating value. Business Horizon 52: 523–29. [Google Scholar] [CrossRef]

- Hon, Robert. 2013. Monte Carlo and Binomial Simulations for European Option Pricing Computer Science with Mathematics. Available online: https://downloads.dxfeed.com/specifications/dxLibOptions/Hon.pdf (accessed on 12 February 2024).

- Hull, John. C. 2005. Fundamentals of Futures and Options Markets, 5th ed. Upper Saddle River: Pearson Education, pp. 349–55. [Google Scholar]

- Johnston, Melissa P. 2014. Secondary data analysis: A method of which the time has come. Qualitative and Quantitative Methods in Libraries 3: 619–26. [Google Scholar]

- King, Major David R., Dan R. Dalton, Catherine M. Daily, and Jeffrey G. Covin. 2004. Meta-analyses of post-acquisition performance: Indications of unidentified moderators. Strategic Management Journal 25: 187–200. [Google Scholar] [CrossRef]

- Kodukula, Prasad, and Chandra Papudesu. 2006. Project Valuation Using Real Options: A Practitioner’s Guide. Fort Lauderdale: Ross Publishing, pp. 72–96. [Google Scholar]

- Kogut, Bruce. 1991. Joint ventures and the option to expand and acquire. Management Science 37: 19–33. [Google Scholar] [CrossRef]

- Kyläheiko, Kalevi, Jaana Sandström, and Virpi Virkkunen. 2002. Dynamic capability view in terms of real options. International Journal of Production Economics 80: 65–83. [Google Scholar] [CrossRef]

- Lambrecht, Bart M. 2017. Real Option in Finance. Journal of Banking and Finance 81: 166–71. [Google Scholar] [CrossRef]

- Larsson, Rikard, and Sydney Finkelstein. 1999. Integrating strategic, organizational, and human resource perspectives on mergers and acquisitions: A case survey of synergy realization. Organization Science 10: 1–26. [Google Scholar] [CrossRef]

- Lasker, Roz D., Elisa S. Weiss, and Rebecca Miller. 2001. Partnership synergy: A practical framework for studying and strengthening the collaborative advantage. The Milbank Quarterly 79: 179–205. [Google Scholar] [CrossRef]

- Lawrence, Cate. 2018. Will Walmart’s Bet on IBM Blockchain Pay Off? Available online: https://dzone.com/articles/will-walmartsbet-on-ibmblockchain-pay-off (accessed on 29 April 2019).

- Lee, Jack, Heather Leung, Terry Au-Yeung, Sonia Andrzejuk, Argyro Charizona, and Vlad Marcu. 2022. Amazon’s $3.9bn Acquisition of One Medical. Available online: https://www.mergersight.com/post/amazon-s-3-9bn-acquisition-of-one-medical (accessed on 8 January 2024).

- Li, Yong, Barclay E. James, Ravi Madhavan, and Joseph T. Mahoney. 2007. Real Options: Taking Stock and Looking Ahead. Advances in Strategic Management 24: 33–66. [Google Scholar]

- Lin, Yini, and Lei-Yu Wu. 2014. Exploring the role of dynamic capabilities in firm performance under the resource-based view framework. Journal of Business Research 67: 407–13. [Google Scholar] [CrossRef]

- Liu, Xiaoran, and Ehud I. Ronn. 2020. Using the binomial model for the valuation of real options in computing optimal subsidies for Chinese renewable energy investments. Energy Economics 87: 104692. [Google Scholar] [CrossRef]

- Lodorfos, George, and Agyenim Boateng. 2006. The role of culture in the merger and acquisition process: Evidence from the European chemical industry. Management Decision 44: 1405–21. [Google Scholar] [CrossRef]

- Loukianova, Anna, Egor Nikulin, and Andrey Vedernikov. 2017. Valuing synergies in strategic mergers and acquisitions using the real options approach. Investment Management and Financial Innovations 14: 236–47. [Google Scholar] [CrossRef]

- Macrotrend.com. 2024. Available online: https://www.macrotrends.net/stocks/charts/AMZN/amazon/ebitda (accessed on 8 January 2024).

- MAGNiTT. 2017. A Different Story from the Middle East: Entrepreneurs Building an Arab Tech Economy. Available online: https://magnitt.com/news/different-story-middle-east-entrepreneurs-building-arab-tech-economy-20010 (accessed on 12 January 2023).

- Mun, Johnathan. 2002. Real Options Analysis: Tools and Techniques for Valuing Strategic Investments and Decision. Hoboken: John Wiley & Sons, pp. 144–45, 174, 178–81, 386. [Google Scholar]

- Mun, Johnathan. 2003. Real Options Analysis Course: Business Cases and Software Applications. Hoboken: John Wiley and Sons. [Google Scholar]

- Nembhard, Harriet Black, and Mehmet Aktan. 2009. Real Options in Engineering, Design, Management, and Operations. Boca Raton: CRC Press, pp. 7–32, 158. [Google Scholar]

- Netz, Joakim, Martin Svensson, and Ethel Brundin. 2019. Business disruptions and affective reactions: A strategy-as-practice perspective. Long Range Planning. in press. [Google Scholar] [CrossRef]

- Nguyen, Han, and Brian H. Kleiner. 2003. The effective management of mergers. Leadership and Organization Development Journal 24: 447–54. [Google Scholar] [CrossRef]

- O’Donovan, Caroline. 2023. One Medical CEO departs one year after the Amazon acquisition. The Washington Post. Available online: https://www.washingtonpost.com/technology/2023/08/31/amazon-one-medical-ceo/ (accessed on 8 January 2024).

- One Medical. 2023. Available online: https://www.onemedical.com/mediacenter/one-medical-joins-amazon/ (accessed on 8 January 2024).

- Palmer, Annie. 2023. Amazon closes deal to buy primary care provider One Medical. CNBS. Available online: https://www.cnbc.com/2023/02/22/amazon-closes-deal-to-buy-primary-care-provider-one-medical.html (accessed on 9 January 2024).

- Patton, Michael Quinn. 1999. Enhancing the quality and credibility of qualitative analysis. Health Sciences Research 34: 1189–208. [Google Scholar]

- Penrose, Edith Tilton. 1959. A Theory of the Growth of the Firm. Oxford: Basil Blackwell. [Google Scholar]

- Rabier, Maryjane R. 2017. Acquisition motives and the distribution of acquisition performance. Strategic Management Journal 38: 2666–81. [Google Scholar] [CrossRef]

- Ralph, Nicholas, Melanie Birks, and Ysanne Chapman. 2014. Contextual positioning: Using documents as extant data in grounded theory research. SAGE Open 4: 2158244014552425. [Google Scholar] [CrossRef]

- Rashid, Yasir, Ammar Rashid, Muhammad Akib Warraich, Sana Sameen Sabir, and Ansar Waseem. 2019. Case Study Method: A Step-by-Step Guide for Business Researchers. International Journal of Qualitative Methods 18: 1609406919862424. [Google Scholar] [CrossRef]

- Rugman, Alan M., and Alain Verbeke. 2002. Edith Penrose’s contribution to the resource-based view of strategic management. Strategic Management Journal 23: 769–80. [Google Scholar] [CrossRef]

- Schweizer, Lars, Le Wang, Eva Koscher, and Bjorn Michaelis. 2022. Experiential learning, M&A performance, and post-acquisition integration strategy: A meta-analysis. Long Range Planning 55: 102212. [Google Scholar]

- Seawright, Jason, and John Gerring. 2008. Case-Selection Techniques in Case Study Research: A Menu of Qualitative and Quantitative Options. Political Research Quarterly 61: 294–308. [Google Scholar] [CrossRef]

- Sekaran, Uma, and Roger Bougie. 2018. Research Methods for Business: A Skill-Building Approach. Chichester: Wiley, p. 448. [Google Scholar]

- Siggelkow, Nicolaj. 2007. Persuasion with case studies. Academy of Management Journal 50: 20–24. [Google Scholar] [CrossRef]

- Smith, Emma. 2008. Using Secondary Data in Educational and Social Research. New York: McGraw-Hill Education. [Google Scholar]

- Spanner, Gary E., JoséPablo Nuño, and Charu Chandra. 1993. Time-based strategies—Theory and practice. Long Range Planning 26: 90–101. [Google Scholar] [CrossRef]

- Statista.com. 2024. Available online: https://www.statista.com/statistics/275757/fluctuation-of-three-month-treasury-bill-rate-in-the-united-states/ (accessed on 7 January 2024).

- Teece, David J., Gary Pisano, and Amy Shuen. 1997. Dynamic capabilities and strategic management. Strategic Management Journal 18: 509–33. [Google Scholar] [CrossRef]

- Triantis, Alexander J., and Adam Borison. 2001. Real Options: State of the Practice. Journal of Applied Corporate Finance 14: 8–23. [Google Scholar] [CrossRef]

- Vaidya, Anuja. 2023. Amazon Offers One Medical Services as Prime Membership Benefit. mHealth Intelligence. Available online: https://mhealthintelligence.com/news/amazon-offers-one-medical-services-as-prime-membership-benefit (accessed on 8 January 2024).

- V-Lab. 2024. Amazon.com Inc. GARCH Volatility Analysis. Available online: https://vlab.stern.nyu.edu/volatility/VOL.AMZN%3AUS-R.GARCH (accessed on 7 January 2024).

- YChart. 2022. Amazon.com Inc. (AMZN). Available online: https://ycharts.com/companies/AMZN/market_cap (accessed on 7 December 2023).

- Yeo, Khim T., and Fasheng Qiu. 2003. The value of management flexibility—A real options approach to investment evaluation. International Journal of Project Management 21: 243–50. [Google Scholar] [CrossRef]

- Yin, Robert K. 1984. Case Study Research: Design and Methods. Newbury Park: Sage. [Google Scholar]

- Yin, Robert K. 2009. Case Study Research: Design and Methods, 4th ed. Applied Social Research Series; Thousand Oaks: Sage Publications, vol. 5. [Google Scholar]

- Yin, Robert K. 2018. Case Study Research: Design and Methods, 4th ed. Newbury Park: Sage. [Google Scholar]

- Zaheer, Akbar, Xavier Castañer, and David Souder. 2013. Synergy sources, target autonomy, and integration in acquisitions. Journal of Management 39: 604–32. [Google Scholar] [CrossRef]

Figure 1.

BOPM: underlining lattice: the value forecast of Amazon after the acquisition of One Medical (upper digits); and real options lattice: the value of Amazon strategic synergism (real options) of the acquisition of One Medical (lower digits) (in USD billion). Source: developed by the author.

Figure 1.

BOPM: underlining lattice: the value forecast of Amazon after the acquisition of One Medical (upper digits); and real options lattice: the value of Amazon strategic synergism (real options) of the acquisition of One Medical (lower digits) (in USD billion). Source: developed by the author.

{kind=link}

Table 1.

The ARCTIC framework. Exploring complementarity, compatibility, and transferability of core competencies: Amazon.com’s acquisition of One Medical.

Table 1.

The ARCTIC framework. Exploring complementarity, compatibility, and transferability of core competencies: Amazon.com’s acquisition of One Medical.

| The Core Competencies of One Medical and Amazon.com | (A?) | (R?) | (C?) | (T?) | (I?) | (C?) |

|---|---|---|---|---|---|---|

| One Medical serves over 815,000 members through more than 200 physical medical offices spread throughout 26 geographical locations. (Palmer 2023, p. 1) | Yes | Yes | Yes | Yes | Yes | Yes |

| In an increasing number of locations, One Medical offers pediatric, mental health, chronic care management, and preventive and regular health visits (One Medical 2023, p. 1). | Yes | Yes | Yes | Yes | Yes | Yes |

| The seamless in-office and round-the-clock virtual care services, on-site laboratories, and programs offered by One Medical for common illnesses, mental health troubles, chronic care management, and preventative care (One Medical 2023, p. 1) | Yes | Yes | Yes | Yes | Yes | Yes |

| Amazon’s huge customer base and its big data strategy: 44% of Americans are members of Amazon Prime (Lee et al. 2022) | Yes | Yes | Yes | Yes | Yes | Yes |

| Amazon.com innovates in all its businesses, from the production of electronic devices to drone delivery systems (BSIC 2017). | Yes | Yes | Yes | Yes | Yes | Yes |

| As a major player in the technology industry, Amazon has gained vast expertise in automation and artificial intelligence (AI) (Lee et al. 2022) | Yes | Yes | Yes | Yes | Yes | Yes |

Source: developed by the author.

Table 2.

The parameters of real options and data in detail: Amazon.com’s acquisition of One Medical.

Table 2.

The parameters of real options and data in detail: Amazon.com’s acquisition of One Medical.

| Parameters of Financial Options | The Parameters of Real Options and Data |

|---|---|

| Stock price (So) | The cumulated market values of Amazon and One Medical as separated entities (four-week average) before the announcement of the acquisition were as follows: Amazon’s market capitalization on 21 June 2022 was USD 1.106 T, and on 19 July 2022 was 1.204T; thus, the average market value of Amazon was USD 1.155T One Medical market capitalization on 18 June 2022 was USD 1.54 bn, and on 23 July 2022 was 3.33 bn; thus, the average market value of One Medical was USD 2.44 bn (CompaniesMarketcap.com 2024). Therefore, the cumulated market values of Amazon and One Medical as separated entities (four-week average) before the announcement of the acquisition was USD 1155 bn plus USD 2.44 bn, equaling 1157.44 bn |