Abstract

The study aims to identify the determinants of digital financial inclusion (DFI) and its role in micro enterprises’ ease of doing business. The study is based on the World Bank’s Enterprises Survey of Micro Firms (ESM) 2022 data of 998 micro-enterprises. The variables that measure access and use of digital finance are extracted from the data. Two sets of independent variables, namely digital resource capability and firms and owners’ characteristics, are taken as explanatory variables of digital financial inclusion. Analysis of variance (ANOVA) has been applied to analyze the difference in perceived business obstacles across the micro-enterprises with and without access and use of digital finance. Further, a logistic regression model is developed to analyze the determinants of DFI. The findings of the study reveal that digital financial inclusion helps to face obstacles in business regulation and handle market externalities. Further, estimates of both the logistic regression model and marginal effects suggest that access to the internet, education, and owner experience are instrumental in digital financial inclusion among micro-enterprises. This study may be helpful for various stakeholders, such as the government, promoters of entrepreneurship, banks, and international organizations working in digital financial inclusion. The originality of the study lies in exploring the determinants of DFI among micro-enterprises, which are still unexplored in the case of India using extensive and specific micro enterprise’s data collected by the World Bank.

Similar content being viewed by others

Introduction

Presently, digital financial inclusion (DFI) is recognized as one of the most important areas of development and has gained global recognition among policymakers and corporations (Duvendack and Mader, 2020; Lai et al. 2020; Gabor and Brooks, 2017; Peric, 2015). The concept of digital financial inclusion refers to the provision of low-cost digital access to financial services, with a particular emphasis on economically underserved demographics (Svotwa et al. 2023; Zhang et al. 2020; Naumenkova et al. 2019). The most important thing about digital finance that it uses the Internet platform, which has low marginal costs, to spread inclusive finance efficiently and effectively (Sharma et al. 2023a; Chen and Zhang, 2021). DFI is a result of the advancement of inclusive finance facilitated by the utilization of the internet, big data, and other related technologies (Zhou et al. 2023; Chen et al. 2022a). The well-known ‘trickle-down effect’ provides evidence that enhancing financial inclusion can contribute to the development of a robust financial system with comprehensive institutions, thereby mitigating regional financial supply and demand imbalances, alleviating poverty, and reducing income inequality (Ji et al. 2021). Digital finance has become a key tool for reducing social inequality and promoting economic growth (Liu et al. 2022; Ozturk and Ullah, 2022). DFI has emerged as a significant catalyst for promoting both an inclusive society as well as inclusive economic system, especially in less developed countries (Aziz and Naima, 2021; Ozili, 2020; Lenka and Barik, 2018). The advent of the internet has compelled the banking sector to reevaluate its information technology strategies, leading to an increased challenge in leveraging the internet as a medium for advertising and endorsing its offerings (Nițescu, 2015; Malik, 2014; Ozawa et al. 2001). Digital financial services improves convenience, affordability, and accessibility to financial services, particularly for low-income individuals and small and micro enterprises.

The significant role of small and medium enterprises in facilitating job creation and advancing economic growth has been widely recognized and extensively discussed in the scholarly literature (Anthanasius Fomum and Opperman, 2023; Shofawati, 2019). According to a report by the International Monetary Fund (IMF) in 2017, the integration of small and medium-sized enterprises (SMEs) into financial systems has a beneficial effect on economic growth, employment generation, the effectiveness of macroeconomic policy, and macro-financial stability. 21 percent of MSMEs in developing economies are completely and partially constrained by access to capital (IFC, 2017). Moreover, micro-enterprises often struggle to secure credit from traditional financial institutions. Digital lending platforms, powered by alternative data sources and algorithms, can assess creditworthiness and provide micro-loans to these businesses, helping them invest in growth opportunities. Digital financial inclusion is a powerful tool for supporting the growth and stability of micro-enterprises. Governments, financial institutions, and technology providers can help these small businesses thrive in the digital economy by providing access to a range of financial services and promoting financial literacy,. Financial inclusion enables investment opportunities regardless of an individual’s parental wealth (Abor et al. 2018; Patwardhan, 2018). The main factor that contribute to failure of small and medium-sized enterprises globally is inadequate financial resources throughout the operation of the business (Hall, 1992). The primary barriers to the growth of SMEs include inadequate access to credit, limited market connections, inadequate training, deficient human resources development programs, reliance on government support and a passive mind set, fluctuations in government policies, price fluctuations, weak connections, and inadequate market and product development strategies (Sharma et al. 2023b; Singh et al. 2023a; Faal, 2020; Irjayanti and Azis, 2012; Tahi Hamonangan Tambunan, 2011; and Olawale and Garwe, 2010). Digital financial inclusion plays a crucial role in empowering micro-enterprises, which are small businesses with limited resources and often operate in underserved or remote areas. By providing these businesses with access to digital financial services and tools, they can overcome various barriers and improve their financial stability and growth prospects. Digital platforms can provide micro-enterprises with access to insurance products that protect against unexpected events such as natural disasters, theft, or illness. This helps safeguard their livelihoods. As microenterprises adopt digital financial services, it’s important to ensure the security and privacy of their financial data. Implementing robust cybersecurity measures and data protection regulations is essential.

Researchers and policymakers continue to stress the necessity of guaranteeing financial inclusion for small and medium-sized firms (SMEs). Technological restrictions, inadequate infrastructure, and corruption are only a few of the external and internal factors that slow down the progress of inclusion in developing countries. Many micro-enterprises lack access to traditional banking services due to their small-scale and remote locations. Digital financial inclusion ensures that they can open bank accounts, receive payments, and access basic financial services through mobile banking apps or agents. The impact of digital financial inclusion on economic growth can be observed through two significant pathways, namely, the facilitation of small and medium-sized enterprise entrepreneurship and the stimulation of household consumption (Liu et al. 2021). This suggests that the primary beneficiaries of digital financial inclusion are individuals and micro-enterprises. The 2030 Agenda for Sustainable Development, as proposed by the United Nations, endeavors to foster economic growth that is both inclusive and sustainable. This is to be achieved by facilitating the formalization and expansion of micro, small, and medium enterprises through the provision of financial services.

The financial services sector in India has undergone significant changes throughout its history. The Government of India (GoI) has undertaken various technology-driven initiatives with the objective of transforming India into a digitally empowered nation. The Unified Payments Interface (UPI), launched by the National Payments Council of India (NPCI) in April 2016, has been a major factor in the rapid growth of digital payments in India since 2014. The ramifications of demonetization have led to the rapid adoption of digital payment methods, including banking cards, mobile wallets, mobile banking, internet banking, and other forms of digital payment. Financial institutions have implemented a range of novel products and services that can be accessed by customers through advanced technological channels (Zhou et al. 2023; Erumban and Das, 2016). A noteworthy advancement that has taken place in the financial services sector of India pertains to the provision of adaptable payment methods and convenient accessibility to digital platforms’ services, including mobile banking, mobile wallets, internet banking, and bank cards, among others (Singh et al. 2023a; Shankar and Rishi, 2020; Priya et al. 2018). Public and private sector innovation has boosted digital financial inclusion in India. The Indian government now provides social welfare scheme benefits digitally via direct benefit transfer into the beneficiary’s bank account. The Indian government has taken various initiatives for digital financial inclusion to leapfrog traditional financial access paradigms. Bank accounts are linked to biometric identification (Aadhaar) and cellphone numbers. The government has licensed new tiers of financial institutions to create a differentiated banking model in which Mobile Network Operators (MNOs) and fintech can provide banking services under a Payment Bank license, and microfinance institutions (MFIs) are encouraged to use technology to align with the market and grow into Small Finance Banks. State-owned enterprises like the State Bank of India, which opened a third of PMJDY accounts, continue to provide direct banking services across India, but the past four years have seen a shift in the government’s role in financial inclusion. In a technology-led model, the government has prioritized the creation of enabling infrastructure, such as digital identification and payment technology.

Mobile money services and digital wallets enable micro-enterprises to send and receive payments, pay bills, and conduct transactions without the need for physical cash. This reduces the risks associated with cash handling and offers convenience. The utilization of mobile payment applications that are supported by smartphones has facilitated the emergence of mobile financial services (Laukkanen, 2016). The provision of mobile-based financial services has enabled customers to engage in convenient financial transactions, such as money transfers between two parties, bill payments for online shopping, and other related services, at any time (Shaikh et al. 2023; Chawla and Joshi, 2019). Digital financial tools also enable micro-enterprises to maintain better records of their financial transactions. This can help them track expenses, revenues, and profits more accurately, making it easier to make informed decisions. As a component of the digital India campaign, the Indian government has instituted a digital payment infrastructure to facilitate the shift from a conventional cash-driven economy to a cashless one. The aforementioned action is aimed at fostering the use of digital payment methods (Sobti, 2019). Various stakeholders, such as organizations working for human development, the banking industry, and developing countries, need to find ways to get more people to use digital financial services (Ozturk and Ullah, 2022). Hence, the expansion of electronic payment modalities can be expedited through efficacious initiatives aimed at advancing digital financial inclusivity. The employment of digital technology in the pursuit of financial inclusion has the potential to yield valuable insights into the operations of small and medium-sized enterprises (SMEs). This, in turn, can incentivize financial institutions to design financial products and services that cater to the specific requirements of SMEs, thereby mitigating their financing impediments and fostering their innovative capabilities (Buchak et al. 2018). MSMEs are the driving force behind the creation of jobs and family wealth in the economy. Despite the fact that ICT, financial inclusion, the informal sector, and poverty reduction have gained prominence on the global policy agenda for development, the academic discourse on digital financial inclusion is still in its nascent stage. A number of studies have explored the determinants of financial inclusion, while very few studies are concerned with the determinants of digital financial inclusion among micro-enterprises. From a policy point of view, it is important to understand the determinants of digital financial inclusion among MSMEs, especially in developing economies where MSMEs make up a large portion of the businesses. Regardless of massive growth in account opening, there is evidence that India’s digital finance push is having a limited impact due to account dormancy and low levels of usage. 48 percent of people with an account at a financial institution made no deposits or withdrawals from that account over the past year. The study aims to analyze the determinants of digital financial inclusion among micro-enterprises and its impact on the ease of doing business using a comprehensive World Bank’s Enterprises Survey of Micro Firms. The specific objective of this paper is to analyze the relationship between firms with access to digital finance and perceived business obstacles to understand the ease of doing business. Furthermore, the study has identified a set of resource capability, firm, and owner characteristics affecting digital financial inclusion among micro-enterprises in India.

This study offers several contributions to the literature on digital financial inclusion among micro-enterprises. Firstly, the present study examines the perceived business obstacles across micro-enterprises with and without access to and use of the digital financial system, which provides an in-depth understanding of the association between digital financial inclusion and ease of doing business. This study complements and supplements the existing studies of determinants of digital financial inclusion among micro firms, which is crucial for an emerging economy like India to penetrate the digital finance among these enterprises because India has 633.9 lakh MSMEs and among them, 630.5 lakh enterprises are micro in nature.

There are five sections in this paper. Section 1 presented the introduction to the study, followed by a review of the literature and research hypotheses in Section 2. The research methodology, which includes the data source and survey instrument, description of variables, and analytical approach applied in this paper, is depicted in Section 3. Section 4 deals with the results and discussion on the determinants of digital financial inclusion in micro-enterprises. The last section highlights the conclusion and implications of the study. At the end of this section, the limitations of the study are presented.

Review of literature and research hypothesis

Digital financial inclusion and perceived business obstacles

Various previous studies found that business performance depends on access to finance (Rokhim et al. 2021; Osano and Languitone, 2016). According to Anthanasius Fomum and Opperman (2023), financial inclusion increases the possibility of microenterprises being classified as emerging and developed enterprises. Yang and Zhang (2020) point out that promoting digital financial inclusion and restructuring the financial industry can boost small and micro companies and the macro economy. Yang and Zhang (2020) demonstrate that promoting digital financial inclusion and restructuring the financial industry can boost small and micro companies and the macro economy. Digital financial inclusion is seen as a feasible solution for addressing the constraints faced by the poor in accessing financial services (Singh et al. 2014). They express that digital financial inclusion increased the flow of money, promoted entrepreneurship, and addressed obstacles faced in businesses. The primary factor contributing to the dearth of productive opportunities is insufficient financial accessibility, which refers to the limited ability to promptly secure funds. The majority of prior research has focused on examining the influence of DFI on the level of income inequality (Neaime and Gaysset, 2018; Zhang et al. 2020). Yang et al. (2022) point out that digital financial inclusion empowers women through increasing entrepreneurship among disadvantaged women, particularly among who are less education or financial autonomy. Chen et al. (2022b) found that digital financial inclusion does not improve the total factor productivity (TFP) of listed companies. However, in large cities with concentrated financial resources, digital financial inclusion can considerably boost listed company productivity. SMEs perceive access to finance as the most significant obstacle that hinders their growth (Wang, 2016). Digital finance has grown swiftly in China, encouraging inclusive finance but also presenting default, fraud, policy, and operational problems (Song and Dong, 2020). Digital finance reduces financing limitations and increases SME innovation, with varying incentives for firms with different property rights and geographies (Yao and Yang, 2022). Financial deepening reduces SMEs’ funding obstacles, promotes company entry into the market and entrepreneurship, and improves resource allocation (Beck, 2013). DFI has increased financial inclusion, enhancing equity and efficiency, which benefits society as well as economy and brings positive externalities. It makes financial services more accessible and efficient. Digital finance institutions can use huge amounts of e-commerce data to reduce financial transaction costs and improve financial inclusion (Frost et al. 2019), and boosts entrepreneurship and economic growth (Xie et al. 2018). Oz-Yalaman (2019) concluded that financial inclusion and business regulation increase tax collections. Bai et al. (2021) express that MSEs now use digital finance in their business dealings, such as bill and tax payments and purchasing. However, the impact of digital financial inclusion on the ease of doing business is not explored exclusively. Based on the above literature, the following research hypotheses have been formulated:

H1: There is no difference in perceived business obstacles by the micro firms with and without access to digital finance.

H2: There is no difference in perceived business obstacles by the micro firms with and without uses of digital finance.

Digital resource capability and digital financial inclusion

The impact of ICT has been a subject of scholarly discourse (Aziz and Naima, 2021; Karakara and Osabuohien, 2020; Niebel, 2018; Hong, 2017), and the literature suggests that information and communication technologies (ICT), specifically mobile phones and the internet, have emerged as significant innovations in the financial sector (Suryono et al. 2020; Pradhan et al. 2017). According to Diniz et al. (2012), the utilization of ICT has facilitated the widespread dissemination of banking services and the operational proximity of banks. The advent of information technology in the banking industry has brought about a significant transformation in the way financial services are delivered to customers worldwide (Chavan, 2013). Gupta and Arya (2019) and Sarkar (2016) expressed that the banking sector has been revolutionized by technological advancements such as automated teller machines (ATMs), internet banking, mobile banking, digital banking kiosks, and the Unified Payments Interface (UPI). These innovations have introduced novel mechanisms that can significantly enhance the capabilities of banks to serve their customers in a more effective and efficient manner. According to Liu et al. (2020), the ongoing third technological revolution based on the internet is significantly affecting efficiency and fairness in banking. The internet revolution has notably provided China with benefits, as it has facilitated the development of the digital economy and digital finance in the country. Due to the adoption of cutting-edge technologies like big data and cloud computing over the past ten years, China’s digital economy, particularly in the area of digital finance, has experienced significant growth (Yin et al. 2019; Gabor and Brooks, 2017). The World Bank says that mobile phones can be used to access digital banking services in more than 80 countries (The World Bank, 2020; Chu, 2018). Mobile phones and other digital tools, like AI, are used by a lot of people, which leads to more people getting access to banking services (Salampasis and Mention, 2018). With digital financial inclusion, people can get financial services at a price they can afford and in a way that is good for them (Gomber et al. 2017). The adoption of digital technologies in financial transactions has had a positive effect on the standard of living of Indian citizens (Malladi et al. 2021). Based on the above literature on digital resources and financial inclusion, the research hypothesis is as follows:

H3: Digital resource capability does not significantly affect the digital financial inclusion among micro firms.

Firms’ and owner’s characteristics and digital financial inclusion

Firm characteristics are likely to influence the firm’s response to financial challenges (Tuffour et al. 2022; Wakaisuka-Isingoma et al. 2016; and Yildirim et al. 2013). Nguli and Odunga (2019) empirically found that financial inclusion is positively and negatively affected by firm size and firm age, respectively. Numerous studies have concluded that an individual’s socioeconomic status is one of the most important factors in determining their access to financial services (Barcellos and Zamarro, 2021; Kulkarni and Ghosh, 2021; Nandru et al. 2015; Izquierdo and Tuesta, 2015). In the studies conducted by Izquierdo and Tuesta (2015) and Frempong (2009), education stands out as an important driver for financial inclusion in enterprises. Education motivates entrepreneurs and improves exploration, communication, and foresight (Smallbone and Wyer, 2000). Miao et al. (2017) contend that experienced entrepreneurs use their expertise and abilities to assist in achieving difficult tasks. Dittmar and Duchin (2016) noted that experienced managers effectively utilize resources such as finances. The CEO’s experience has a substantial impact on the firm’s financial matters (Matemilola et al. 2018). Business experience improves resource acquisition and increases intellectual capital-resource acquisition links. Individual characteristics (manager age, education, and experience) can also impact the effectiveness of financial literacy (Barcellos and Zamarro, 2021; Garg and Singh, 2018), which has significant implications for financial inclusion (Goyal and Kumar, 2021; Schuetz and Venkatesh, 2020). Lack of access to money and information networks is a big reason why women don’t start businesses or make them official (Xheneti et al. 2019). Some studies found that women face trouble getting loans from outside sources (Brixiová and Kangoye, 2016; Demirgüç-Kunt et al. 2013; and Brush and Cooper, 2012). Based on the above literature, the following research hypothesis has been formulated:

H4: Firms’ and owner’s characteristics does not significantly affect the digital financial inclusion among micro firms.

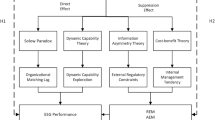

To analyse the determinants of digital financial inclusion and ease of doing business across the micro firm with and without access to and use of digital finance, a conceptual research framework has been developed (Fig. 1). Literature advocates that digital financial inclusion is determined by digital resource capability, firms, and owner characteristics. Therefore, these factors have been considered in the conceptual research framework and identified from the data of the World Bank’s Enterprises Survey of Micro Firms (ESM).

Conceptual research framework of determinants of digital financial inclusion.

Research methodology

Data source and survey Instrument

The study is based on the Enterprises Survey of Micro Firms (ESM) 2022 from the World Bank. Data collection took place between December 2021 and March 2022. Nielsen (India) Pvt. Ltd. surveyed on behalf of the World Bank to analyze the business environment and demographics of micro-enterprises. Data was collected from the enterprises, who have less than five employees registered with a government agency as per the Factory Act and the Shop and Establishment Act. The sixth economic census of India served as the source for the universe table of micro-enterprises. Manufacturing, construction, retail and wholesale trade, transportation and storage, accommodation, and food services are the major sectors covered in the Enterprises Survey of Micro Firms (ESM) 2022. Stratified random sampling was used to collect the survey data, and 998 micro-enterprises were surveyed. Data collection involved a two-stage approach. First, phone calls were made to the micro-enterprises to confirm eligibility and schedule interviews. After that, a face-to-face interview was conducted with the businesses’ owners, managers, and directors. For further information, refer to the Enterprise Survey, Micro, India 2022 implementation report (ESM, 2022). Data collection has been done using a structured questionnaire. A wide range of variables relevant to the firm’s demographic profile, business activities, and perceived business obstacles are included in the questionnaire.

Description of variables

The main objective of the study is to identify the determinants of digital financial inclusion among micro-enterprises. Two dimensions have been taken to measure digital financial inclusion: access and usage. The data on related variables is extracted from the surveyed data of micro-enterprises. Digital financial inclusion is measured through two variables: (1) It uses digital payments, and (2) It uses digital payments to pay utility bills. They are taken as dependent variables. These variables are measured on a binary scale, where if firms use digital payments or use digital payments to pay utility bills, it is labeled as 1, and if not, 0 is entered in the data. There are two sets of explanatory variables in the regression model, namely digital resource capability and firms and owners’ characteristics. Firms and owners’ characteristics have been taken in terms of firm age, education level, household size, gender of owner, and manager experience. The availability of the internet and computers or tablets is taken as a digital resource capability. A detailed description of variables, measurement scales, and descriptive statistics is given in Table 1.

Analytical approach

The ESM 2022 data has been digitized with the help of SPSS 22. Simple statistical tools such as descriptive statistics, the chi-square test, and logistic regression have been used to analyze the data. Descriptive statistics are used to understand the nature of the variables extracted for the study. Analysis of Variance (ANOVA) has been used to measure the difference between perceived business obstacles by micro-enterprises with and without access to digital finance and users and non-users of digital finance. Further, a binary logistic regression model has been used to explore the determinants of digital financial inclusion among micro-enterprises. A binary logistic regression model has been used because the dependent variables are measured on a binary scale. This study used two dependent variables: (1) use of digital payment to measure the accessibility of digital finance. (2) uses digital payments to pay utility bills because of the perceived usefulness of digital finance. Where 1 represents digital financial inclusion, and 0 depicts the absence of digital financial inclusion. The regression model is as follows;

The logit model is based on the cumulative logistics probability function and is specified as follows:

Where Z determines a set of explanatory variables X; F(Z) is the cumulative logistic function; \({P}_{i}=1\) if micro enterprises access and uses digital financial services \({P}_{i}=0\) if micro enterprises do not uses the digital financial services. α is the intercept, and \({\beta }_{i}\) is the vector of regression coefficients. \({X}_{i}\) is the vector of independent variables in terms of digital resources capabilities, age of the firms, gender of owner, education level of owner, household size of owners, and managers experience.

Results and discussion

Profile of sample micro enterprises

Out of the total micro-enterprises, 66 percent have reported access to digital financial systems; among 998 enterprises, only 614 have reported on the usage of digital financial systems, and 85 percent of micro-enterprises use the digital platform for payments. 43 percent of micro firms have computers or tablet and 75 percent micro enterprises have access to internet. The average age of firms are 14.11 years. The majority of the firms are headed by males. 14 percent and 34 percent of the owners have an education level of Bachelor or above and a Diploma, respectively. In micro-enterprises, the average experience of managers is 12.34 percent.

Digital financial inclusion and perceived business obstacles

Various factors such as access to resources, market externalities, and business regulation collectively reflect the business environment in any economy (Singh et al. 2023b; Khan et al. 2023; Boateng and Poku, 2019; Njiraini et al. 2018; and Ali, 2016). In the present study, perceived business obstacles in terms of access to resources (access to land, access to electricity to operations of this establishment), market externalities (practices of competitors in the informal sector, corruption, crime, theft, and disorder), and business regulation (tax rates, tax administrations, business licensing and permits, and labor regulations) have been taken to measure the ease of doing business by micro-enterprises. Perceived business obstacles have been analyzed for micro-enterprises with and without access to and usage of digital finance. Analysis of variance has been used to measure the difference in perceived business obstacles with and without access to and usage of digital finance. The results are presented in Table 2. Analysis of variance reflects a significant difference in tax administration as an obstacle across micro-enterprises with and without access to digital finance (F = 4.349, P = 0.037). Means values show that tax administration is a relatively more significant obstacle for firms that do not have access to digital finance. Similarly, F-statistics reveals a difference for micro-enterprises with and without access to digital finance in the case of business licensing and permits as an obstacle (F = 13.153, P = 0.000). Micro enterprises accessing digital finance perceived fewer obstacle in getting business licensing and permits. It implies that digital financial inclusion assists in getting business licensing and permits. It may be due to the fact that it is now easier to pay fess online compared to other methods. ANOVA shows that enterprises with access to digital finance perceive significantly fewer obstacle in labor regulation (F = 10.303, P = 0.001). For the practice of competitors as an obstacle, the analysis of variance shows a very interesting outcome: micro-enterprises with access to digital finance perceived it as a significantly greater obstacle (F = 4.393, P = 0.036) as compared to firms with no access to digital finance. As far as crime, theft, and disorder are concerned, the F-test shows the significant difference between firms with and without access to digital finance (F = 16.368, P = 0.000), which implies that micro-enterprises having access to digital finance perceive crime, theft, and disorder significantly fewer obstacle compared to firms with no access to digital finance. Digital finance minimizes the risk of carrying cash, reducing the chance of crime for money. A noticeable finding has been recorded for access to land as an obstacle across the accessibility status of digital finance. Micro enterprises have access to digital finance perceive significantly more obstacles in accessing the land (F = 3.056, P = 0.081). Hence, hypothesis H1 is partially rejected. Micro enterprises having access to digital finance perceived less business obstacles as compared to the micro enterprises which do not have access to digital finance. Similarly, ease of doing business has been explored across the users or non-users of digital finance. Under the business regulations, analysis of variance shows that tax rate (F = 3.091, P = 0.079), tax administration (F = 4.902, P = 0.027), business licensing and permits (F = 11.573, P = 0.001) are significantly less obstacles for the micro use digital finance and do not face any issues in tax administration. The whole tax administration has become online, so the micro-enterprises using digital finance Under the market externalities category, ANOVA does not reflect statistically significant differences across users and non-users of digital finance. For access to resource groups, digital finance users significantly perceived more obstacles to accessing the land for business purposes. The above finding shows that hypothesis H2 is partially rejected.

Determinants of digital financial inclusion among micro enterprises in India

Determinants of digital financial inclusion in terms of access and usage have been calculated using a logistic regression model and the marginal effect which was calculated using Stata software. Estimates in terms of the regression coefficient, significant level, marginal effect, pseudo-R square, and level of log-likelihood are given in Table 3. Two dimensions of digital financial inclusion, namely access to digital finance and usage of digital finance, have been taken as dependent variables. Therefore, two regression models have been developed to identify the determinants of digital financial inclusion among micro-enterprises. Various studies have explored digital financial inclusion under different scenarios (Lu et al. 2022; Tay et al. 2022, and Yang and Zhang, 2020). Estimates of logistic regression show that out of a total of seven explanatory variables, six variables, namely computers or tablets, the internet, firm’s age, gender of owner, education level of owner, and household size, significantly affect the access to digital finance. The regression coefficient of computers or tablets is negative and significant (β = −0.404, P = 0.029), indicating an unexpected finding that access to computers is less likely to affect access to digital finance. This may be due to the fact that digital banking is generally accessed through smartphones. The estimated regression coefficient of accessibility of the internet has a positive and significant effect on access to digital finance (β = −1.539, P = 0.000); it may be due to the fact that digital resource capability is needed to reach the interface of digital finance. Without the internet it is not possible to use and perform the digital payment. Hence the hypothesis H3 is partially rejected. The results show a positive regression coefficient and marginal effects of a firm’s age on access to digital finance (β = 0.032, P = 0.004), which exhibits that older firms are more likely to adopt digital financial inclusion. It may be due to the fact that older firms have better resource capabilities and infrastructure to handle the digital platform. The estimated regression coefficient for gender reveals that it has significant implications for access to digital finance (β = −0.756, P = 0.066); the value of marginal effects suggests that females are 14.8 percent more likely to access digital finance as compared to male-headed micro-enterprises. About the education categories, logistic regression analysis for secondary education (β = −0.551, P = 0.026) level and bachelor or above (β = −0.916, P = 0.005) depicted a positive and significant implication on digital financial inclusion; it clearly reflects that education is a significant driver of digital financial inclusion among micro-entrepreneur. It may be because education empowers and makes the individual aware of the latest advancements. Therefore, educated micro-entrepreneurs reveal more access to digital finance. Though the process of digital payment or usage has become too simple but still less educated people do not have trust on digital transection. The household size of the micro-entrepreneur significantly and inversely affected the access to digital finance by micro-entrepreneurs (β = −0.129, P = 0.008). The model summary suggests that the regression model reasonably fits the data. The value of chi-square (93.540) reveals that all the explanatory variables in the regression model significantly explain the determinants of digital financial inclusion jointly. The log-likelihood value is high (−473.306), and the negative value indicates a good fit for a regression model.

The determinants of the usage of digital finance have been further explored. Logistics regression analysis reveals that usage of the internet, one category of education, and manager experience significantly affect the usage of digital finance among micro-enterprises. The estimated coefficient of regression for the internet is positive and significant (β = 0.904, P = 0.003), implying that micro-enterprises with internet facilities significantly use digital finance as compared to enterprises that do not have internet facilities. The marginal effect shows that micro-enterprises with the internet are 10.1 percent more likely to use digital financial inclusion. Regarding education, the logistic regression result reflects that the owner of micro-enterprises who has completed the diploma are significantly more likely to use digital finance (β = 0.978, P = 0.022). The parameter estimates for manager experience exhibit that experienced managers are more likely to use digital finance (β = 0.064, P = 0.003). It implies that the usage of digital finance increases with the experience of managers. The model summary suggests that the developed logistic regression model is significant, which implies that all the explanatory variables jointly explain the variation in dependent variable usage of digital finance. Further, the Log-likelihood value is high (−204.032), and the negative sign indicates that the regression model is robust and adequate.

Conclusion, implications and limitations

The financial services sector in India has undergone significant changes. The Government of India (GoI) has undertaken various technology-driven initiatives to transform India into a digitally empowered economy. The Unified Payments Interface (UPI), launched by the National Payments Council of India (NPCI), has been a major factor in the rapid growth of digital payments in India. The study analyzes the determinants of digital financial inclusion among micro-enterprises and its impact on ease of doing business using the comprehensive World Bank’s Enterprises Survey of Micro-Firms. Analysis of variance reveals that micro-enterprises with access to digital finance perceived fewer business obstacles than micro-enterprises without access to digital finance. The findings of the logistic regression analysis revealed that the internet, firm’s age, gender and education level of owner, and household size have positive and significant effects on digital financial inclusion, implying that older firms with access to the internet, owned by educated females from small household are more likely to access digital financial inclusion. The findings of business obstacles across the usage of digital finance reveal that firms that use digital finance perceive fewer business obstacles in terms of tax rates, tax administrations, and business licensing and permits. The regression analysis estimates indicate that usage of digital finance is determined by access to the internet, education, and the manager’s experience. This indicated that micro-enterprises with access to the internet, educated owners, and experienced managers use the digital financial channel in the firm’s business operations. From both models, it is evident that access to the internet, education, and owner experience are instrumental in digital financial inclusion among micro enterprises.

The study has several theoretical and managerial implications for various stakeholders, such as promoters of micro-entrepreneurship, the banking industry, industrial economists, and the government, for promoting the agenda of digitalization at the grass-roots level. Firstly, the current study indicates that businesses implementing digital financial inclusion perceive fewer barriers to conducting business. It is very clear that microenterprises must be encouraged to adopt digital financial inclusion. Distract industrial centers should promote the benefits of digital finance in terms of ease of doing business among micro-enterprises. A live demonstration to micro-entrepreneurs should be given on how to use the digital platform to apply for various licenses and permits, administer taxes, and get information on other business regulations and schemes. The difference in perceived business obstacles between micro-enterprises with and without access to digital finance suggests that micro-enterprises require access to digital finance for better handling of their businesses. Policymakers should adopt a comprehensive policy for digital financial inclusion in order to help micro-enterprises develop. The regression analysis shows that digital resource capability determines digital financial inclusion. Micro enterprises should provide digital resources at a subsidized rate so that they can avail it. Further, older firms owned by educated owners and experienced managers are adopting digital financial inclusion. To fully benefit from digital financial services, micro-enterprises need education and training on how to use these tools effectively. Financial literacy programmes can teach them about budgeting, savings, and responsible borrowing. Digital financial services should be designed to be affordable and accessible to micro-enterprises. Regulatory measures can help prevent predatory practices and ensure that fees and charges are transparent. Integrating digital financial services with supply chains can improve efficiency and transparency for micro-enterprises. Governments can play a crucial role in promoting digital financial inclusion by implementing policies and infrastructure that support these efforts. This might include building a robust digital payments ecosystem or incentivizing financial institutions to serve micro-enterprises. The study gives valuable information for creating a conducive financial services system and gives directions in achieving the goal of digital financial inclusion among micro-enterprises in the country.

This study utilizes a comprehensive survey dataset from the World Bank; however, due to its secondary nature, it imposes certain limitations on selecting factors pertaining to the business obstacles faced by micro-enterprises. A future study might be framed within the context of theoretical models, utilizing appropriate indicators and incorporating in-depth interviews to explore the characteristic variables of respondents. In addition, the Enterprises Survey of Micro Firms (ESM) 2022 of the World Bank contains most of the questions on firms and owners’ characteristics. However, behavioral aspects of the owner of micro-enterprises should also be studied as determinant of digital financial inclusion. Future researchers may include the behavioral aspect in their research model in addition to firm and owner profiles in their study.

Data availability

Data has been shared. Data is also available at website of World Bank enterprises Survey, it can be access on https://www.enterprisesurveys.org/en/enterprisesurveys or corresponding author can provide the data on request. Data is available in public domain, it can be access at https://login.enterprisesurveys.org/content/sites/financeandprivatesector/en/library/library-detail.html/content/dam/wbgassetshare/enterprisesurveys/economy/india/IndiaMicro-2022-full-data.dta.

References

Abor JY, Amidu M, Issahaku H (2018) Mobile telephony, financial inclusion and inclusive growth. J Afr Bus 19(3):430–453

Ali J (2016) Performance of small and medium-sized food and agribusiness enterprises: evidence from Indian firms. Int Food Agribus Manag Rev 19(4):53–64

Anthanasius Fomum T, Opperman P (2023) Financial inclusion and performance of MSMEs in Eswatini. Int J Soc Econ 50(11):1551–1567

Aziz A, Naima U (2021) Rethinking digital financial inclusion: Evidence from Bangladesh. Technol Soc 64:101509

Bai C, Quayson M, Sarkis J (2021) COVID-19 pandemic digitization lessons for sustainable development of micro-and small-enterprises. Sustain Prod Consum 27:1989–2001

Barcellos SH, Zamarro G (2021) Unbanked status and use of alternative financial services among minority populations. J Pension- Econ Financ 20(4):468–481

Beck T (2013) Bank financing for SMEs–lessons from the literature. Natl Inst Econ Rev 225:R23–R38

Boateng S, Poku KO (2019) Accessing finance among women-owned small businesses: evidence from lower Manya Krobo municipality, Ghana. J Glob Entrepreneurship Res 9:1–17

Brixiová Z, Kangoye T (2016) Gender and constraints to entrepreneurship in Africa: New evidence from Swaziland. J Bus Venturing Insights 5:1–8

Brush CG, Cooper SY (2012) Female entrepreneurship and economic development: An international perspective. Entrepreneurship Regional Dev 24(1-2):1–6

Buchak G, Matvos G, Piskorski T, Seru A (2018) Fintech, regulatory arbitrage, and the rise of shadow banks. J Financial Econ 130(3):453–483

Chavan J (2013) Internet banking-benefits and challenges in an emerging economy. Int J Res Bus Manag 1(1):19–26

Chawla D, Joshi H (2019) Consumer attitude and intention to adopt mobile wallet in India–An empirical study. Int J Bank Mark 37(7):1590–1618

Chen S, Zhang H (2021) Does digital finance promote manufacturing servitization: Micro evidence from China. Int Rev Econ Financ 76:856–869

Chen S, Liang M, Yang W (2022a) Does Digital Financial Inclusion Reduce China’s Rural Household Vulnerability to Poverty: An Empirical Analysis from the Perspective of Household Entrepreneurship. SAGE Open 12(2):21582440221102423

Chen Y, Yang S, Li Q (2022b) How does the development of digital financial inclusion affect the total factor productivity of listed companies? Evidence from China. Financ Res Lett 47:102956

Chu AB (2018) Mobile technology and financial inclusion. In Handbook of Blockchain, Digital Finance, and Inclusion, Volume 1 (pp. 131-144). Academic Press

Demirgüç-Kunt A, Klapper LF, Singer D (2013) Financial inclusion and legal discrimination against women: evidence from developing countries. World Bank Policy Research Working Paper, (6416)

Diniz E, Birochi R, Pozzebon M (2012) Triggers and barriers to financial inclusion: The use of ICT-based branchless banking in an Amazon county. Electron Commer Res Appl 11(5):484–494

Dittmar A, Duchin R (2016) Looking in the rearview mirror: The effect of managers’ professional experience on corporate financial policy. Rev Financial Stud 29(3):565–602

Duvendack M, Mader P (2020) Impact of Financial Inclusion in Low- and Middle-income Countries: A Systematic Review of Reviews. J Economic Surv 34(3):594–629

Erumban AA, Das DK (2016) Information and communication technology and economic growth in India. Telecommun Policy 40(5):412–431

ESM (2022) Enterprises Survey of Micro Firm, Data can be retrieved from https://www.enterprisesurveys.org/en/enterprisesurveys. Access on March 2023

Faal ML (2020) Understanding binding constraints to small and medium enterprises (SMEs) in the Gambia: A critical review. Asian J Manag 11(2):216–221

Frempong G (2009) Mobile telephone opportunities: the case of micro‐and small enterprises in Ghana. Info 11(2):79–94

Frost J, Gambacorta L, Huang Y, Shin HS, Zbinden P (2019) BigTech and the changing structure of financial intermediation. Econ Polic 1:100–110

Gabor D, Brooks S (2017) The digital revolution in financial inclusion: international development in the fintech era. N. Political Econ 22(4):423–436

Garg N, Singh S (2018) Financial literacy among youth. Int J Soc Econ 45(1):173–186

Gomber P, Koch JA, Siering M (2017) Digital Finance and FinTech: current research and future research directions. J Bus Econ 87:537–580

Goyal K, Kumar S (2021) Financial literacy: A systematic review and bibliometric analysis. Int J Consum Stud 45(1):80–105

Gupta A, Arya PK (2019) Banking Reforms in India with Special Reference to Digital Banking. Asian J Res Bank Financ 9(7):12–27

Hall C (1992) The globalisation of small and medium enterprises: implications for australian business and policy. In Proceedings of the SEAANZ and Institute of Industrial Economics National Small Business Conference, Sydney, Australia (pp. 31-51)

Hong JP (2017) Causal relationship between ICT R&D investment and economic growth in Korea. Technol Forecast Soc Change 116:70–75

IFC (2017) “MSME finance gap: assessment of the shortfalls and opportunities in financing micro, small and medium enterprises in emerging markets”, available at: https://www.smefinanceforum.org/sites/default/files/Data%20Sites%20downloads/MSME%20Report.pdf

IMF (2017) Article IV Consultation–Press Release (No. 17/386). and Staff Report. IMF Country Report. Available online: imf.org/en/ Countries/ETH (accessed on 24 May, 2023)

Irjayanti M, Azis AM (2012) Barrier factors and potential solutions for Indonesian SMEs. Procedia Econ Financ 4:3–12

Izquierdo NC, Tuesta D (2015) Factors that matter for financial inclusion: Evidence from Peru. Aestimatio: IEB Int J Financ 10:10–31

Ji X, Wang K, Xu H, Li M (2021) Has digital financial inclusion narrowed the urban-rural income gap: The role of entrepreneurship in China. Sustainability 13(15):8292

Karakara AAW, Osabuohien E (2020) ICT adoption, competition and innovation of informal firms in West Africa: a comparative study of Ghana and Nigeria. J Enterprising Communities: People Places Glob Econ 14(3):397–414

Khan W, Singh TP, Jamshed M (2023) Understanding the ease of doing agribusiness in emerging Asian economies: evidence from world enterprises survey. J Enterprising Communities: People Places Glob Econ 17(2):419–432

Kulkarni L, Ghosh A (2021) Gender disparity in the digitalization of financial services: challenges and promises for women’s financial inclusion in India. Gend, Technol Dev 25(2):233–250

Lai JT, Yan IK, Yi X, Zhang H (2020) Digital financial inclusion and consumption smoothing in China. China &. World Econ 28(1):64–93

Laukkanen T (2016) Consumer adoption versus rejection decisions in seemingly similar service innovations: The case of the Internet and mobile banking. J Bus Res 69(7):2432–2439

Lenka SK, Barik R (2018) Has expansion of mobile phone and internet use spurred financial inclusion in the SAARC countries? Financial Innov 4(1):1–19

Liu D, Zhang Y, Hafeez M, Ullah S (2022) Financial inclusion and its influence on economic-environmental performance: demand and supply perspectives. Environ Sci Pollut Res 29(38):58212–58221

Liu X, Yang F, Wu J (2020) DEA considering technological heterogeneity and intermediate output target setting: the performance analysis of Chinese commercial banks. Ann Oper Res 291:605–626

Liu Y, Luan L, Wu W, Zhang Z, Hsu Y (2021) Can digital financial inclusion promote China’s economic growth? Int Rev Financial Anal 78:101889

Lu Z, Wu J, Li H, Nguyen DK (2022) Local bank, digital financial inclusion and SME financing constraints: Empirical evidence from China. Emerg Mark Financ Trade 58(6):1712–1725

Malik S (2014) Technological innovations in Indian banking sector: changed face of banking. Int J 2(6):45

Malladi CM, Soni RK, Srinivasan S (2021) Digital financial inclusion: next frontiers—challenges and opportunities. CSI Trans ICT 9(2):127–134

Matemilola BT, Bany-Ariffin AN, Azman-Saini WNW, Nassir AM (2018) Does top managers’ experience affect firms’ capital structure? Res Int Bus Financ 45:488–498

Miao C, Qian S, Ma D (2017) The relationship between entrepreneurial self‐efficacy and firm performance: a meta‐analysis of main and moderator effects. J Small Bus Manag 55(1):87–107

Nandru, P, Anand, B, & Rentala, S (2015). Factors influencing financial inclusion through banking services. J Contemp Res Manag 10(4)

Naumenkova S, Mishchenko S, Dorofeiev D (2019) Digital financial inclusion: Evidence from Ukraine. Invest Manag Financial Innov 16(3):194

Neaime S, Gaysset I (2018) Financial inclusion and stability in MENA: Evidence from poverty and inequality. Financ Res Lett 24:230–237

Nguli JN, Odunga R (2019) Effect of firm characteristics on financial inclusions; evidence from women owned enterprises in Kenya. J Emerg Trends Econ Manag Sci 10(2):53–60

Niebel T (2018) ICT and economic growth–Comparing developing, emerging and developed countries. World Dev 104:197–211

Nițescu DC (2015) Banking Business and Social Media-A Strategic Partnership. Theor Appl Econ 22(4)

Njiraini P, Gachanja P, Omolo J (2018) Factors influencing micro and small enterprise’s decision to innovate in Kenya. J Glob Entrepreneurship Res 8:1–9

Olawale F, Garwe D (2010) Obstacles to the growth of new SMEs in South Africa: A principal component analysis approach. Afr J Bus Manag 4(5):729

Osano H. M, Languitone H (2016) Factors influencing access to finance by SMEs in Mozambique: case of SMEs in Maputo central business district. J Innov Entrep 5:1–16

Ozawa T, Castello S, Phillips RJ (2001) The internet revolution, the “McLuhan” stage of catch-up, and institutional reforms in Asia. J Economic Issues 35(2):289–298

Ozili PK (2020) Contesting digital finance for the poor. Digital Policy, Regul Gov 22(2):135–151

Ozturk I, Ullah S (2022) Does digital financial inclusion matter for economic growth and environmental sustainability in OBRI economies? An empirical analysis. Resour, Conserv Recycling 185:106489

Oz-Yalaman G (2019) Financial inclusion and tax revenue. Cent Bank Rev 19(3):107–113

Patwardhan A (2018) Financial inclusion in the digital age. In Handbook of Blockchain, Digital Finance, and Inclusion, Volume 1 (pp. 57-89). Academic Press

Peric K (2015) Digital financial inclusion. J Paym Strategy Syst 9(3):212–214

Pradhan RP, Arvin M, Nair M, Bennett S, Bahmani S (2017) ICT-finance-growth nexus: Empirical evidence from the Next-11 countries. Cuad de Econía 40(113):115–134

Priya R, Gandhi AV, Shaikh A (2018) Mobile banking adoption in an emerging economy: An empirical analysis of young Indian consumers. Benchmarking: Int J 25(2):743–762

Rokhim R, Mayasari I, Wulandari P (2021) The factors that influence small and medium enterprises’ intention to adopt the government credit program. J Res Market Entrep 23(1):175–194

Salampasis D, Mention AL (2018) FinTech: Harnessing innovation for financial inclusion. In Handbook of Blockchain, Digital Finance, and Inclusion, Volume 2 (pp. 451-461). Academic Press

Sarkar SS (2016) Technological innovations in Indian banking sector-a trend analysis. J Commer Manag Thought 7(1):171–185

Schuetz S, Venkatesh V (2020) Blockchain, adoption, and financial inclusion in India: Research opportunities. Int J Inf Manag 52:101936

Shaikh AA, Alamoudi H, Alharthi M, Glavee-Geo R (2023) Advances in mobile financial services: a review of the literature and future research directions. Int J Bank Mark 41(1):1–33

Shankar A, Rishi B (2020) Convenience matter in mobile banking adoption intention?. Australas Mark J 28(4):273–285

Sharma HP, Jain M, Anuforo PU (2023b) Adoption of Blockchain as a Solution Strategy for Financial Inclusion: Evidence From Rural India. In The Impact of AI Innovation on Financial Sectors in the Era of Industry 5.0 (pp. 151–170). IGI Global

Sharma HP, Krishna SH, Tiwari M, Tiwari T, Kumar MN (2023a) Analysis of Cyber Security Threats in Payment Gateway Technology. In 2023 3rd International Conference on Advance Computing and Innovative Technologies in Engineering (ICACITE) (pp. 793–799). IEEE

Shofawati A (2019) The role of digital finance to strengthen financial inclusion and the growth of SME in Indonesia. KnE Social Sciences, 389-407

Singh K, Goundar S, Chandran P, Agrawal AK, Singh N, Kolar P (2023a) Digital Banking through the Uncertain COVID Period: A Panel Data Study. J Risk Financial Manag 16(5):260

Singh C, Mittal A, Goenka A, Goud C RP, Karthik R, Rathi VS, Ravi C, Garg R, Kumar U (2014) Financial Inclusion in India: Select Issues, IIMB-WP, No. 474

Singh S, Amini M, Jamshed M, Sharma HP, Khan W (2023b) Understanding the perceived business obstacles and determinants of credit adoption by textile firms: Evidences from World Bank’s enterprises survey. Research Journal of Textile and Apparel. ahead-of-print

Smallbone D, Wyer P (2000) Growth and development in the small firm. Enterp Small Bus 25:100–126

Sobti N (2019) Impact of demonetization on diffusion of mobile payment service in India: Antecedents of behavioral intention and adoption using extended UTAUT model. J Adv Manag Res 16(4):472–497

Song RM, Dong, L (2020) Review of the Development of Digital Inclusive Finance in China [J]. 2020 International Conference on Education, Culture, Economic Management and Information Service (ECEMIS 2020). 399–411

Suryono RR, Budi I, Purwandari B (2020) Challenges and trends of financial technology (Fintech): a systematic literature review. Information 11(12):590

Svotwa TD, Makanyeza C, Wealth E (2023) Exploring Digital Financial Inclusion Strategies for Urban and Rural Communities in Botswana, Namibia, South Africa and Zimbabwe. In Financial Inclusion and Digital Transformation Regulatory Practices in Selected SADC Countries: South Africa, Namibia, Botswana and Zimbabwe (pp. 161-179). Cham: Springer International Publishing

Tahi Hamonangan Tambunan T (2011) Development of small and medium enterprises in a developing country: The Indonesian case. J Enterprising Communities: People Places Glob Econ 5(1):68–82

Tay LY, Tai HT, Tan GS (2022) Digital financial inclusion: A gateway to sustainable development. Heliyon, e09766

The World Bank. 2020. Digital Financial Inclusion. Available online: https://www.worldbank.org/en/topic/financialinclusion/publication/digital-financial-inclusion (accessed on 13 April 2023)

Tuffour JK, Amoako AA, Amartey EO (2022) Assessing the effect of financial literacy among managers on the performance of small-scale enterprises. Glob Bus Rev 23(5):1200–1217

Wakaisuka-Isingoma J, Aduda J, Wainaina G, Mwangi CI (2016) Corporate governance, firm characteristics, external environment and performance of financial institutions in Uganda: A review of literature. Cogent Bus Manag 3(1):1261526

Wang Y (2016) What are the biggest obstacles to growth of SMEs in developing countries?–An empirical evidence from an enterprise survey. Borsa Istanb Rev 16(3):167–176

Xheneti M, Madden A, Thapa Karki S (2019) Value of formalization for women entrepreneurs in developing contexts: A review and research agenda. Int J Manag Rev 21(1):3–23

Xie X, Shen Y, Zhang H, Guo F (2018) Can digital finance promote entrepreneurship? Evidence from China. China Econ Quart 17(4):1557–1580

Yang L, Zhang Y (2020) Digital financial inclusion and sustainable growth of small and micro enterprises—evidence based on China’s new third board market listed companies. Sustainability 12(9):3733

Yang X, Huang Y, Gao M (2022) Can digital financial inclusion promote female entrepreneurship? Evidence and mechanisms. North Am J Econ Financ 63:101800

Yao L, Yang X (2022) Can digital finance boost SME innovation by easing financing constraints? Evidence from Chinese GEM-listed companies. PLoS One 17(3):e0264647

Yildirim HS, Akci Y, Eksi IH (2013) The effect of firm characteristics in accessing credit for SMEs. J Financial Serv Mark 18:40–52

Yin Z, Gong X, Guo P (2019) The impact of mobile payment on entrepreneurship—Micro evidence from China household finance survey. China Ind Econ 3:119–137

Zhang X, Zhang J, Wan G, Luo Z (2020) Fintech, growth and inequality: evidence from China’s household survey data. Singap Economic Rev 65:75–93

Zhou M, Zhang H, Zhang Z, Sun H (2023) Digital financial inclusion, cultivated land transfer and cultivated land green utilization efficiency: an empirical study from China. Sustainability 15(2):1569

Author information

Authors and Affiliations

Contributions

All authors contributed to the study conception and design. In particular, the specific contributions made by each author is illustrated as following. AJ, Conceptualization, Writing and validation, Supervision MA: Writing original draft, visualization and supervision. PT: Literature, Discussion and validation. WK: Data acquisition and preparation for analysis, Formal analysis. RA: Methodology, Investigation, Resources. MW: Writing, revision, Review, Editing and Validation.

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Ethical approval

Ethical approval was not required as the study did not involve human participants.

Informed consent

Informed consent was not required because the study did not involve human participants.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary information

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Johri, A., Asif, M., Tarkar, P. et al. Digital financial inclusion in micro enterprises: understanding the determinants and impact on ease of doing business from World Bank survey. Humanit Soc Sci Commun 11, 361 (2024). https://doi.org/10.1057/s41599-024-02856-2

Received:

Accepted:

Published:

DOI: https://doi.org/10.1057/s41599-024-02856-2