Abstract

This research analyzes the dynamic relationship between green bonds, energy prices, geopolitical risk, and CO2 emissions. In doing so, the study examines the global scale at disaggregated (i.e., sectoral) level, applies a novel time and frequency-based approach (i.e., wavelet local multiple correlation-WLMC), and uses high-frequency daily data between 1st January 2020 and 28th April 2023. In doing so, the study considers the potential differences among sectors. So, aggregated and disaggregated level CO2 emissions on sectoral bases are investigated. Hence, the study comprehensively uncovers the effect of the aforementioned indicators on global CO2 emissions. The results reveal that on CO2 emissions (i) the most influential factor is the geopolitical risk (2020/1–2021/5), green bonds (2021/5–2021/7), energy prices (2021/7–2023/1), and green bonds (2023/1–2023/4); (ii) the effects of the influential factors are much weaker (stronger) at lower (higher) frequencies; (iii) the effect of the influential factors change based on times and frequencies; (iv) however, the effects of the influential factors on CO2 emissions do not differ at aggregated or disaggregated levels. Overall, the results present novel insights for time and frequency-varying effects as well as both aggregated and disaggregated level analyses of global CO2 emissions.

Highlights

-

The study examines global CO2 emissions at aggregated and disaggregated levels.

-

The study applies a novel WLMC approach between 1/1/2020 and 28/04/2023.

-

The most effective variable changes according to various periods.

-

The effects of the variables change based on time and frequency.

-

The effects do not differ at both aggregated and disaggregated levels.

Similar content being viewed by others

Introduction

Rapid economic growth of countries has necessitated the usage of energy, which is an imperative production factor that affects the welfare of nations (Kartal 2022; Adedoyin et al. 2023; Bekun 2024). Despite its significance as a production factor, energy has detrimental effects on environmental sustainability by reducing air quality. Climate change is a global environmental threat that is mainly caused by CO2 emissions (Kartal 2023; Raihan 2023; Erdogan et al. 2024a; Khan et al. 2024; Li et al. 2024; Tedeschi et al. 2024). The emissions create various problems, such as environmental disasters, and weather extremes causing floods, droughts, and hurricanes (Ayhan et al. 2023; Erdogan et al. 2024b). So, many countries and supranational authorities have decided to take action to mitigate the negative effects of current climate conditions (Dogan et al. 2022; Anser et al. 2023; Kirikkaleli 2023). COP26 Climate Conference has noted the necessity of securing global net zero CO2 emissions and keeping the global warming level at 1.5 degrees, thus ensuring the mitigation of CO2 emissions has become a top precedence for countries (Yuan et al. 2022; Kartal et al. 2023a; Ramzan et al. 2024). One challenge related to CO2 emissions is that despite the motivations of the countries to reach a net carbon zero, CO2 emissions have reached the highest level as of 2021 (IEA 2022a). Considering these developments, the level of CO2 emissions and the means to cut down these emissions have been lying at the heart of various studies.

GBs are one of the means to mitigate CO2 emissions through allocating funds to eco-friendly (e.g., green technology) projects (Sharif et al. 2024). GBs stand as one of the financing tools that promote the firms or projects that serve energy efficiency improvements or improvements related to pollution mitigation or environmental sustainability (Dogan et al. 2022). The main hurdle to net zero is the lack of finance for renewable energy investments. The core of the discussions in COP26 is the need for financing that will create the environment for adjusting to a zero-carbon emitting phase. Most of the participants of COP26 have declared their desire to cut down on CO2 emissions, yet they have highlighted financial insufficiency to switch to renewable energy, which is hindered even more as a result of shifting funds to health expenditures due to the global health crisis called the pandemic. Thus, the downside risks of the pandemic on allocating funds to the gigantic need for renewable energy investments call for a significant increase in GBs that are at the core of financing sources for green technologies.

GBs facilitate green technology investments and other means of eco-friendly innovations, which will ensure the meeting of net-zero emission targets consented to under the accord (Wang et al. 2023). GBs represent a critical mechanism for mobilizing the necessary capital to transition to a climate-resilient and low-carbon economy. Moreover, given the energy security issues that the world has been witnessing due to the Russian-Ukraine war, energy prices have been displaying high volatility that also triggers the necessity of the countries to shift to renewable sources to handle any unexpected energy shocks (Kartal et al. 2023b). The success and performance of GBs are shaped by the broader economic and political context. Contractionary economic policies or economic uncertainties affect investments in GBs. Moreover, investments in GBs depend on energy prices from traditional sources. In other words, lower fossil fuel prices will discourage green energy investments and reduce investment in GBs (Glomsrød and Wei 2018; Lee et al. 2021; Sartzetakis 2020). However, higher fossil fuel energy prices will escalate the viability of green investments, which will increase the demand for GBs.

Energy, which is the most significant production factor, has become even more critical following the tightening of the energy markets and the creation of a global energy crisis due to the pandemic and the Russian-Ukraine conflict (IEA 2022b; Kılıç Depren et al. 2022). Most countries have witnessed a rapid economic recovery in the post-pandemic period and the decline in green investments during the pandemic has not met the energy needs of the world, which has triggered the high reliance on fossil fuels, creating a huge discrepancy between energy demand and supply (IEA 2022c). Russia, being a major global energy exporter (23.6% of the natural gas supply and 12.3% of oil supply) (British Petroleum 2023), deliberately cut down on exports of natural gas and oil to developed countries, which remain opponents in this conflict, has upsurged the prices of energy. These developments alongside the detrimental effects of the pandemic on the transition to green energy (Żuk and Żuk 2022) have magnified the severity of the energy crisis and energy prices (Guan et al. 2023). It should be noted that recent higher prices of non-renewable energy have triggered a boost in adopting renewable energy (Cao et al. 2020; Atems et al. 2023; Sarker et al. 2023). Energy prices have a restricting position in managing the energy services within a country and consequently affect the environmental quality (Fatima et al. 2021). All in all, oil price stands as a sign of changes in environmental effects and the effect of oil on the environment varies (Baloch et al. 2020).

It is noteworthy to highlight that geopolitical risks are still shaping energy markets and energy security while supply issues remain a setback for many economies. Geopolitical risks, wars, invasions, conflicts with energy-supplying nations, and various trade bans have been still affecting global energy markets and energy commodities (Pata et al. 2023a, b, c; Sarker et al. 2023; Zhang et al. 2023). Geopolitical risk has an important effect on crude oil prices as well as renewable energy investments and environmental pollution. Also, the relationship of geopolitical risk with crude oil prices displays very high volatility during political tension times. Geopolitical risks are also reflected in the green energy stocks (Sweidan 2021), which suggests the effects on traditional and renewable energy prices. Boubaker et al. (2022) stress the substantial effects of the developments on energy markets in Ukraine. Geopolitical risks affect the energy markets through three channels. First, geopolitical risks stimulate energy conversion and reduce oil prices, which is propelled by fuel substitution (Rasoulinezhad et al. 2020). Second, conflicts have a negative influence on investor sentiment, which has a further effect on crude oil prices (Ji et al. 2019). Third, conflicts elucidate oil production through disruption of production and demand, which consequently will be reflected in crude oil prices (Noguera-Santaella 2016). Accordingly, these channels affect crude oil prices and shape the supply and demand for fossil fuels, which will affect the tendency to shift the renewable energy eventually leading to different levels of CO2 emissions.

Given the dynamic link between green bonds, energy prices, geopolitical risks, and CO2 emissions, this study aims to probe into this multifaceted relationship to apprehend the complex relationship. CO2 emissions, which are a major contributor to climate change, can be influenced by energy prices and geopolitical risks. Also, the mitigation of CO2 emissions is mostly the primary goal of green projects funded by GBs. In this context, the study handles global CO2 emissions at aggregated and disaggregated levels as the environmental indicators, considers SPGB as the proxy of GBs, COP as the proxy of energy prices, and GPR as the geopolitical risk proxy, applies a novel WLMC approach since it uncovers the dynamic relationship across times and frequencies, and uses high-frequency daily data between 1st January 2020 and 28th April 2023. Thus, this study presents on CO2 emissions that the most influential factor is the geopolitical risk (2020/1–2021/5) followed by green bonds (2021/5–2021/7), energy prices (2021/7–2023/1), and green bonds (2023/1–2023/4); the effects of the variables are weak at lower frequencies, whereas they are strong at higher frequencies; the effects of the influential factors do not differ at sectors; and the effects of the influential factors vary across times and frequencies.

The novelties of this study to the literature are twofold. First, the study considers global CO2 emissions at aggregated and disaggregated levels, which will enable researchers to evaluate whether the effect of each factor varies. Second, the study adopts a novel WLMC method, which facilitates the exploration of the dynamic relationship between the variables by combining wavelet analysis and multiple correlation analysis and stipulates the understanding of the underlying patterns.

The study continues with the following sections: Sect. 2 provides the theory and literature; Sect. 3 introduces the methods; Sect. 4 demonstrates the empirical results; Sect. 5 concludes.

Theoretical background and literature review

In general, GBs provide financing for clean energy projects. Thus, GBs should be associated with decreasing CO2 emissions. In investigating whether GBs have such an effect or not, a variety of studies have focused on country-level or global-level data. Hammoudeh et al. (2020) analyze index-level data to capture the time-varying causal relationship between GBs and other (financial and environmental) variables. The findings note that there is a causality relationship between the allowances of CO2 emissions and GBs. Yet, the counter-argument is not valid that GBs do not have causality to CO2 emissions. Kanamura (2020) questions the greenness of green bonds and The Bloomberg Barclays MSCI and SPGB show positive correlations and rise with WTI and Brent crude oil prices. On the other hand, the Solactive Green Bond Index exhibits negative correlations and declines with COP and Brent crude oil prices.

Meo and Karim (2022) focus on country-level data and consider the effect of GBs on CO2 emissions in the top ten economies with top GB capitalization. The results indicate GBs as the most significant means to reduce emissions yet note that GB market and country-specific market conditions shape the effectiveness of GBs in mitigating CO2 emissions. Marín-Rodríguez et al. (2022) test dynamic co-movements among oil prices, CO2 emissions, and GBs and notice a unidirectional causality from oil price returns to the returns of CO2 futures and a negative dynamic correlation of green bond index on the returns of CO2 futures, with increased correlations during uncertainty periods. In a similar vein, Marín-Rodríguez et al. (2023) study the relationship between oil prices, GBs, and CO2 emissions and point to a strong interdependence between oil prices and returns of CO2 futures at all times and frequencies and similar interlinkage is evident between the green bond index and returns of CO2 futures, while Green Bond Index is the leading one. Moreover, Adebayo and Kartal (2023) delve into the relationship between GBs, oil prices, and the COVID-19 pandemic on industrial CO2 emissions in United States of America and highlight the time and frequency-varying effects of GBs on the emissions.

In the literature, an ample amount of research has investigated the links between crude oil prices and environmental effects. Several studies have noted a direct link between increasing energy prices and emissions. Saboori et al. (2016) focus on Organization of the Petroleum Exporting countries and the results point out that an increase in oil prices enhances environmental conditions. Nwani (2017) investigates Ecuador, which is an oil exporting country, and noted a link between increasing crude oil prices and economic conditions that are associated with higher CO2 emissions. On the other hand, contradictory findings are also evident. Alshehry and Belloumi (2015) consider Saudi Arabia and suggest that increasing prices of oil create increased usage and have detrimental effects on the environment. Same results are determined for Venezuela by noting dynamic linkages between oil prices, economic growth, and CO2 emissions by Agbanike et al. (2019). Ullah et al. (2020) analyze the highest ten carbon emitters and their results display asymmetric findings. Negative shocks diesel prices accompany reductions with CO2 emissions in China and India. Achuo (2022) scrutinizes the crude oil price shocks and environmental quality connection in sub-Saharan African countries and notes a positive long-run relationship between crude oil price and CO2 emissions. A similar increasing effect of crude oil prices on environmental degradation is defined by Ulussever et al. (2023) for Gulf Cooperation Council countries except for Saudi Arabia and Bahrain.

Zaghdoudi (2017) explores the causality between oil prices, renewable energy consumption, CO2 emissions, and economic growth, and the results propose a negative significant relationship between oil prices, renewable energy, and CO2 emissions. Also, the findings underline a bidirectional relationship between carbon dioxide emissions and oil prices both in the short and long-run. Analysis of China by Zaghdoudi (2018) uncovers the non-linear strong effect of oil prices on CO2 emissions, with supporting evidence both in the short and long-run. Besides, the study unveils that oil price increases escalate CO2 emissions more than their decline. Mahmood et al. (2022) unearth a positive and asymmetrical effect of oil prices on emissions in GCC countries. Similar results are determined by Mohamued et al. (2021) for 26 European countries, 22 oil-producing countries, China, and United States of America with varying evidence for oil-exporting and oil-importing countries. The results suggest that oil price increases in oil-importing (oil-exporting) countries decrease (upsurge) CO2 emissions.

There is little contrasting evidence, which suggests that oil prices have a declining effect on CO2 emissions. Hammoudeh et al. (2014) adopt a quantile framework and observe that an increase in crude oil prices creates a significant decline in carbon prices when the crude oil is at very high quantiles. Wang and Li (2016) explore the 2014 period when crude oil prices declined by nearly half. The analysis reveals that cheaper oil prices create an opportunity to remove fossil fuel subsidies and carbon tax can be introduced during such periods. Okwanya et al. (2023) consider African countries and perceive an asymmetric relationship between oil prices and CO2 emissions, where positive (negative) changes in the oil price cause a reduction (increase) increase in CO2 emissions. The degree of relationship is higher for oil-importing countries.

Moreover, geopolitical risks have long been recognized. Consequently, geopolitical risks act as determinants of huge price hikes and descends that have effects on almost all issues. Despite the significance of the geopolitical risks on the values of green investments and environmental effects, limited studies have focused on this relationship. In the literature, some studies consider similar determinants as a proxy of geopolitical risk (e.g., terrorist activities, political instability) and consider their effects on the environment. Danish et al. (2019) describe the adverse effects of governance indicators, which include political stability and government efficiency, on CO2 emissions in Brazil, Russia, India, and China. Sohag et al. (2019) investigate Türkiye and note that militarization is detrimental to green economic growth. Bildirici and Gokmenoglu (2020) focus on eight countries and find that terrorism is linked to increased CO2 emissions. Also, Bildirici (2020) links terrorist activities with higher CO2 emissions in China, India, Israel, and Türkiye. Wang et al. (2022) investigate the connection between geopolitical risk index and CO2 emissions and it is seen that economic activities are altered through geopolitical risk factors (e.g., trade disputes, military organizations, and energy issues), which in turn affect CO2 emissions. Further, that study highlights that increasing geopolitical risks can lead to higher energy consumption and more military-related activities, potentially hampering research, and development in renewable energy. This limitation in innovation may result in the escalation of CO2 emissions. Tang et al. (2023) investigate the asymmetric effects of various geopolitical risk indicators (e.g., geopolitical acts indices) on crude oil and GB returns. The results show that GB returns are negatively affected by such geopolitical risk indicators in the long-run. Fluctuations in geopolitical risks can also have positive effects by promoting energy independence and encouraging investment in green energy and advanced technology projects (Sweidan 2021). These initiatives can contribute to reducing CO2 emissions.

Although the literature includes various studies, there are some still lack points that no study considers the global case in uncovering the dynamic relationship between GBs, energy prices, GPR, and CO2 emissions at the global level by considering the sectoral differences as well as time and frequency -based varying structure. Accordingly, the study makes a sectoral analysis for the global by applying a novel WLMC approach to close the gap.

Methods

Data

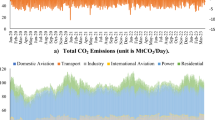

This study investigates the dynamic effects between SPGB, COP, GPR, and CO2 emissions at the global level by making a sector-based analysis. Instead of other environmental indicators that have relatively old and low-frequency data, the present investigation uses CO2 emissions as the environmental indicators to ensure the inclusion of the latest information in line with the studies of Kartal et al. (2022), Adebayo et al. (2023), Hunjra et al. (2023), and Sharif et al. (2023). Also, this study adopts a daily timeframe spanning from 1st January 2020 to 28th April 2023. The selection of this period allows researchers to use up-to-date in the analyses and consideration of recent developments.

Table 1 provides a comprehensive overview of the variables, encompassing their respective symbols, definitions, units of measurement, and sources of data.

Estimation models

To thoroughly uncover the dynamic relationships between the variables, a series of models are constructed. They seek to represent the complex and dynamic relationship between the variables. In light of this objective, a total of four different models are developed, which are presented in Table 2.

These models have been designed to uncover and analyze the complicated connections and dependencies among the variables, shedding light on their mutual effects. By employing these models, a comprehensive and in-depth understanding of the relationships between the variables can be achieved, which provides valuable insights into the underlying mechanisms and dynamics.

Empirical approach

Figure 1 depicts the underlying empirical methodology employed in the analysis. This proposed methodology encompasses six fundamental steps,

Empirical Methodology

The methodology begins with examining the preliminary statistics This analysis serves as a crucial groundwork for gaining a comprehensive understanding of the data and variables under investigation. To achieve this, descriptive statistics are examined. Correlation analysis is also performed, enabling the exploration of relationships and dependencies between the variables. As the methodology progresses, the third step is to test the assumption of stationarity (Dickey and Fuller 1979). Stationarity is crucial, as violating this assumption can lead to biased and unreliable results. In the fourth step, a nonlinearity test is conducted to evaluate the linear relationship between the variables, which helps to determine the appropriateness of linear models in the subsequent analysis (Broock et al. 1996). Finally, cointegration analysis is performed to explore the long-term relationship between variables (Pesaran et al. 2001; Kripfganz and Schneider 2020). In the sixth step, WLMC analysis is carried out to examine the coherence or degree of similarity between the variables at different time scales or frequencies (Polanco- Martínez et al. 2020).

WLMC approach

WLMC analysis is a statistical approach that combines wavelet analysis and multiple correlation analysis to explore the relationships between variables in multivariate data sets. It allows for the investigation of relationships at different times or frequencies by providing a comprehensive understanding of the underlying patterns in the data (Polanco-Martínez et al. 2020).

The WLMC analysis begins by applying the wavelet transform to decompose the signals into different frequency bands or scales. The wavelet transform provides a time–frequency representation of the data, revealing the frequency components present in the signals. By decomposing the data, the WLMC analysis can capture both local and global features of the relationships between variables. The results of the WLMC analysis can be visualized to aid in interpretation and understanding. Heatmaps or other visual representations can be used to display the correlation coefficients obtained from the analysis, allowing researchers to identify patterns and trends across different frequencies or scales (Fernández-Macho 2018).

In the WLMC graphs, the first observation corresponds to January 1, 2020. As the data collection progresses, subsequent observations are recorded at regular intervals, such as the 200th observation on October 6, 2020, the 400th observation on July 13, 2021, the 600th observation on April 19, 2022, and the 800th observation on January 24, 2023. The last observation is dated April 28, 2023.

The frequency intervals and their associated frequency terms play a crucial role in the analysis of WLMC figures. These terms reflect the different temporal scales or frequencies at which relationships between variables are explored. The frequency interval of 2–8 represents the short-term scale. It captures relatively rapid fluctuations and transient patterns in the data. Moving to the interval of 8–32, it enters the medium-term scale. The interval of 32–64 corresponds to the long-term scale. Lastly, the frequency term "very long-term" is attributed to the interval of 64–128. Variables analyzed within this range exhibit the most extended timescales in the dataset.

Results

Preliminary analysis

Descriptive statistics

The summary statistics offer an overview of the variables included. The statistics are given in Table 3, which provides key information regarding variables.

Among all variables, SPGB has the highest mean value followed by GPR, CO2, COP, INDUSTRY, POWER, and TRANSPORT, in order. Also, GPR has the highest variations followed by COP, SPGB, CO2, POWER, INDUSTRY, and TRANSPORT, respectively. Moreover, based on the Jarque–Bera statistics, it can be stated that all variables, except for CO2 and COP, have a normal distribution.

Correlation matrix

The correlation matrix is presented in Table 4.

According to Table 4, there are mainly positive correlations between the aggregated and disaggregated level CO2 emissions and the selected variables except for some cases. Specifically, there are negative correlations between CO2 and SPGB; INDUSTRY & SPGB; TRANSPORT & SPGB. So, the correlation results show the changing correlation between the variables.

Stationarity test

The third step of the methodological process entails conducting a stationarity test for each variable. The ADF test is employed to assess the stationarity characteristics of the variables. The results of the ADF test, which serve as indicators of stationarity, are presented in Table 5. This table provides valuable insights into the stationarity properties of the variables, enabling a thorough examination of their time series behavior.

The ADF test results provide insights into the stationarity properties of the variables. The ADF p-values for each variable indicate the presence of unit roots. Based on the ADF test, all variables exhibit statistically significant p-values at the I(1) level. This indicates that the null hypothesis of a unit root (non-stationarity) is rejected in favor of the alternative hypothesis of stationarity for all variables. Furthermore, the decision column indicates that all variables are classified as I(1), indicating that they are integrated into order 1.

Nonlinearity test

The BDS test is employed to examine the nonlinearity of a time series. It evaluates whether the observed series follows a linear pattern or exhibits non-linear behavior. The test compares the autocorrelation structure of the observed series with that of a randomly shuffled version of the series. The results are reported in Table 6.

The BDS test results indicate that all variables exhibit statistically significant p-values across different dimensions. This suggests strong evidence of nonlinearity in the series for all variables. Based on these results, the decision column indicates that all variables are classified as non-linear. This implies that the observed series for each variable does not follow a linear pattern and exhibits non-linear characteristics. Therefore, non-linear modeling techniques should be applied as a more suitable approach for analyzing and interpreting the data.

Cointegration test

Table 7 presents the results of the PSS and KS bounds test for the models constructed. The table provides the test statistics (K) and critical values at different significance levels (10%, 5%, and 1%) as well as the corresponding p-values. The p-values indicate the significance of the test results. A smaller p-value suggests stronger evidence against the null hypothesis of no bounds.

The findings indicate that all models mainly exceed the corresponding critical values, leading to the rejection of the null hypothesis of no bounds.

WLMC results

In the context of the WLMC analysis, the examination of the multiple correlation structure between variables entails the testing of four different models. Model 1 aims to elucidate the relationship between the dependent variable (TRANSPORT) and the explanatory variables (SPGB, COP, and GPR). Likewise, Models 2, 3, and 4 look into the relationships between the dependent variables (INDUSTRY, POWER, and CO2), respectively, and the aforementioned set of explanatory variables (i.e., SPGB, COP, and GPR). The results are presented in Fig. 2.

WLMC Results for Models

It can be inferred that the correlations observed between the variables demonstrate statistical significance across all models, mostly within the long-term to very long-term periods. A more detailed analysis reveals that in Model 1, the correlation between variables remains consistently significant at a high level throughout all periods. However, it is noteworthy that the strength of the correlation diminishes from the very long-term to the short-term across all observed periods. Specifically, there is not a statistically significant correlation before October 6, 2020 in the short-term as well as during the period spanning from July 13, 2021, to April 19, 2022. These findings show the temporal dynamics of the correlations between variables within Model 1, highlighting the robustness of the correlations in the long-term, their gradual decrease towards the short-term, and the occurrences, where the statistical significance of the correlations is temporarily diminished.

Consistent with the findings observed in Model 1, the analysis conducted in Model 2 indicates a gradual decline of correlations from the very long-term to the short-term. However, an intriguing disparity emerges in the middle-term, where the correlations exhibit a moderate level of strength, rather than being weak as observed in Model 1. This moderate correlation is evident across almost all periods within the middle-term. Furthermore, it is noteworthy that the correlation coefficients in Model 2 demonstrate a relatively high level of association before October 6, 2020, and after April 19, 2022. This implies that the variables examined in Model 2 exhibit a robust and statistically significant relationship during these specific periods. However, it is important to emphasize that the middle-term is characterized by correlations of moderate strength, which distinguishes it from the weakening trend seen in the short-term.

In both Models 3 and 4, the findings align with those observed in Models 1 and 2, revealing a significant and robust correlation between variables in the long and very long-term, except for the period between July 13, 2021, and August 19, 2021. This signifies a sustained and meaningful relationship between the variables over extended periods, with statistical significance maintained in most instances. Within the medium-term analysis, the correlation between variables remains relatively high during two specific periods: before October 6, 2020, and after April 19, 2022. This indicates the presence of notable associations during these time intervals. However, correlations between variables are generally weak or insignificant in the short-term. This implies a diminished strength of the relationship in the shorter timeframes under examination.

The WLMC heat map analysis reveals valuable insights into the dynamic relationship between the variables across different temporal scales. In the long and very long-term, before July 13, 2021, the GPR variable emerges as the most influential factor affecting CO2 levels. This signifies that GPR plays a prominent role in driving CO2 dynamics during this timeframe. However, there is a notable shift in the most influential factor after July 13, 2021. In the very long-term, the SPGB variable becomes the primary influencer of CO2 dynamics, indicating its heightened significance in shaping CO2 patterns during this period. Conversely, in the smooth term (shorter timeframes), COP takes precedence as the most influential factor, suggesting its dominant role in driving CO2 fluctuations from July 13, 2021, onwards. Furthermore, in the middle-term, it is observed that different factors exert influence on CO2 dynamics depending on specific time ranges. Before October 6, 2020, SPGB is identified as an important factor affecting CO2, highlighting its significance in shaping CO2 patterns during this timeframe. After August 19, 2022, the COP variable assumes a prominent role, indicating its increased influence on CO2 dynamics in the middle-term.

Furthermore, the heat map analysis does not differentiate the CO2 emissions based on sectors. Instead, it provides a comprehensive perspective of the factors affecting CO2 levels across the examined temporal scales without sector-specific differentiation.

Conclusion, policy options, and future research

Conclusion

Degradation in environmental quality has become a sensitive issue for all countries as well as the world. Accordingly, efforts to slow down the negative effects have been increasing. On one hand, countries and international institutions have been putting forth various initiatives and scholars have been searching for the possible causes and potential solutions to this adverse situation on the other hand. While a variety of well-known factors have been considered in the literature, recent knowledge has focused on new factors, such as GBs, energy prices, and GPR. That is why these new factors have been affecting the environmental quality from various perspectives under the current energy crisis and geopolitically risky environment. Also, some countries have a leading role in combating environmental problems, whereas others have a follower role.

Accordingly, this study presents insights about the global case rather than focusing on only one or some countries because “the world is our home”. Hence, the study uncovers dynamic effects between green bonds, energy prices, geopolitical risk, and CO2 emissions by using high-frequency daily data between 1st January 2020 and 28th April 2023 and applying a novel WLMC approach.

It can be summarized that the most influential factor on CO2 emissions is geopolitical risk (2020/1–2021/5) followed by green bonds (2021/5–2021/7), energy prices (2021/7–2023/1), and green bonds (2023/1–2023/4). Also, the effects are weak at lower frequencies, whereas they are strong at higher frequencies. Besides, the effects of the influential factors do not differ according to either aggregated level or disaggregated sectors. Moreover, the effect of the influential factors on CO2 emissions change based on times and frequencies.

The findings of this study are mainly in the same direction as the results of the literature, for instance, Hammoudeh et al. (2020) and Adebayo and Kartal (2023) for GBs; Achuo (2022) and Mahmood et al. (2022) for crude oil price; and Ulussever et al. (2023) for GPR. In addition to presenting consistent results with the current literature, this study further provides new time and frequency-based insights about the dynamic effects between green bonds, energy prices, geopolitical risk, and CO2 emissions by benefitting from the novel WLMC approach.

Policy options

Constructed on the novel WLMC results, various policy alternatives can be argued for the globe. The dynamic relationship between the variables change based on times and frequencies. Also, the effects of green bonds, energy prices, and geopolitical risk on CO2 emissions are stronger at higher frequencies, whereas they are weak at lower frequencies. Hence, global policymakers should care about this fact and adjust their approaches accordingly against various environmental problems. That is why such a time and frequency-based changing effect requires more frequent adjustments in policy framework to obtain a certain success in combating environmental problems.

Besides, the most influential factor change according to periods. Specifically, geopolitical risk is the leading factor for the period between 2020/1 and 2021/5 followed by green bonds (2021/5–2021/7), energy prices (2021/7–2023/1), and green bonds (2023/1–2023/4). Based on this determination, policymakers should think about the most effective factor on environmental quality at the global scale and deal with the most influential factor first, and then go on dealing with other factors as well.

Moreover, the effects of the influential factors on CO2 emissions do not differ according to either aggregated level or disaggregated sectors. In other words, under the different empirical models used, the results are the same, which are aggregated level or disaggregated level effects are similar. For this reason, global policy options can be applied to sub-sectors (transport, industry, and power) as well.

Furthermore, it is critical to understand that green bonds, energy prices, and geopolitical risk do not have a curbing on global CO2 emissions. Although such factors may have a curbing effect in some countries and regions, unfortunately, they are not effective in declining global CO2 emissions. So, global policymakers should focus much more on these factors to turn them into a curbing effect while dealing with other continuous agendas, such as green transition, renewable and nuclear energy stimulates, limiting coal usage (Zeng et al. 2023; Alam et al. 2024).

Future research

The global case in CO2 emissions is examined in this study by some recently critical variables (e.g., GBs, energy prices, and GPR) as the explanatory variables for the period between 1st January 2020 and 28th April 2023 by applying a novel WLMC approach. Based on this reality, new studies can consider analyzing by including the global case and leading CO2-emitting countries at the same time. Also, similar to the approach of this study, new studies can use both aggregated and disaggregated level data simultaneously for further investigation.

Also, because the study uses CO2 emissions as proxy for the environment, new studies can prefer to work with other environmental indicators. Hence other perspectives on environmental quality can be searched in new studies.

Finally, due to the fact that the novel WLMC approach is used in the study, new research can consider applying other recent econometric approaches (e.g., quantile-based as well as wavelet-based other approaches) for further empirical analysis.

Data availability

Data will be made available on request.

Abbreviations

- ADF:

-

Augmented Dickey-Fuller

- BPS:

-

Basis Points

- CO2 :

-

Carbon Dioxide

- GBs:

-

Green Bonds

- IEA:

-

International Energy Agency

- KS:

-

Kripfganz & Schneider

- MtCO2 :

-

Metric Tons of CO2 Equivalent

- PSS:

-

Pesaran, Shin, & Smith

- WLMC:

-

Wavelet Local Multiple Correlation

- WTI:

-

West Texas Intermediate

- TRANSPORT:

-

CO2 Emissions in Transport Sector

- INDUSTRY:

-

CO2 Emissions in Industry Sector

- POWER:

-

CO2 Emissions in Power Sector

- CO2 :

-

Global CO2 Emissions in Total

- SPGB:

-

S&P Green Bond Index

- COP:

-

WTI Crude Oil Price

- GPR:

-

Global Geopolitical Risk Index

References

Achuo ED (2022) The nexus between crude oil price shocks and environmental quality: empirical evidence from sub-Saharan Africa. SN Bus Econ 2(7):79

Adebayo TS, Ağa M, Kartal MT (2023) Analyzing the co-movement between CO2 emissions and disaggregated nonrenewable and renewable energy consumption in BRICS: evidence through the lens of wavelet coherence. Environ Sci Pollut Res 30:38921–38938

Adebayo TS, Kartal MT (2023) Effect of green bonds, oil prices, and COVID-19 on industrial CO2 emissions in the USA: evidence from novel wavelet local multiple correlation approach. Energy Environ. https://doi.org/10.1177/0958305X231167

Adedoyin FF, Erum N, Taşkın D, Chebab D (2023) Energy policy simulation in times of crisis: revisiting the impact of renewable and non-renewable energy production on environmental quality in Germany. Energy Rep 9:4749–4762

Agbanike TF, Nwani C, Uwazie UI, Anochiwa LI, Onoja TGC, Ogbonnaya IO (2019) Oil price, energy consumption and carbon dioxide (CO2) emissions: insight into sustainability challenges in Venezuela. Latin Am Econ Rev 28(1):1–26

Alam MM, Destek MA, Haque A, Kirikkaleli D, Pinzón S, Khudoykulov K (2024) Can undergoing renewable energy transition assist the BRICS countries in achieving environmental sustainability? Environ Sci Pollut Res. https://doi.org/10.1007/s11356-023-31738-4

Alshehry AS, Belloumi M (2015) Energy consumption, carbon dioxide emissions and economic growth: the case of Saudi Arabia. Renew Sustain Energy Rev 41:237–247

Anser MK, Khan KA, Umar M, Awosusi AA, Shamansurova Z (2023) Formulating sustainable development policy for a developed nation: exploring the role of renewable energy, natural gas efficiency and oil efficiency towards decarbonization. Int J Sust Dev World. https://doi.org/10.1080/13504509.2023.2268586

Atems B, Mette J, Lin G, Madraki G (2023) Estimating and forecasting the impact of nonrenewable energy prices on US renewable energy consumption. Energy Policy 173:113374

Ayhan F, Kartal MT, KılıçDepren S, Depren Ö (2023) Asymmetric effect of economic policy uncertainty, political stability, energy consumption, and economic growth on CO2 emissions: evidence from G-7 countries. Environ Sci Pollut Res 30(16):47422–47437

Baloch ZA, Tan Q, Iqbal N, Mohsin M, Abbas Q, Iqbal W, Chaudhry IS (2020) Trilemma assessment of energy intensity, efficiency, and environmental index: evidence from BRICS countries. Environ Sci Pollut Res 27(27):34337–34347

Bekun FV (2024) Race to carbon neutrality in South Africa: What role does environmental technological innovation play? Appl Energy 354:122212

Bildirici ME (2020) Terrorism, environmental pollution, foreign direct investment (FDI), energy consumption, and economic growth: Evidences from China, India, Israel, and Turkey. Energy Environ 32(1):75–95

Bildirici M, Gokmenoglu SM (2020) The impact of terrorism and FDI on environmental pollution: evidence from Afghanistan, Iraq, Nigeria, Pakistan, Philippines, Syria, Somalia, Thailand and Yemen. Environ Impact Assess Rev 81:106340

Bloomberg (2023) Bloomberg Terminal. Accessed 10 Aug 2023

Boubaker S, Goodell JW, Pandey DK, Kumari V (2022) Heterogeneous impacts of wars on global equity markets: evidence from the invasion of Ukraine. Financ Res Lett 48:102934

British Petroleum. (2023). Statistical Review of World Energy 2022 , https://www.bp.com/content/dam/bp/business-sites/en/global/corporate/pdfs/energy-economics/statistical-review/bp-stats-review-2022-full-report.pdf, Accessed on 15 August 2023

Broock WA, Scheinkman JA, Dechert WD, LeBaron B (1996) A test for independence based on the correlation dimension. Economet Rev 15(3):197–235

Cao H, Guo L, Zhang L (2020) Does oil price uncertainty affect renewable energy firms’ investment? Evidence from listed firms in China. Financ Res Lett 33:101205

Carbonmonitor. (2023). Data of CO2 Emissions and Electricity Generation. https://carbonmonitor.org, Accessed on 15 August 2023

Danish K, Baloch MA, Wang B (2019) Analyzing the role of governance in CO2 emissions mitigation: the BRICS experience. Struct Chang Econ Dyn 51:119–125

Dickey DA, Fuller WA (1979) Distribution of the estimators for autoregressive time series with a unit root. J Am Stat Assoc 74:427–431

Dogan E, Madaleno M, Taskin D, Tzeremes P (2022) Investigating the spillovers and connectedness between Green Finance and renewable energy sources. Renew Energy 197:709–722

Erdogan S, Pata UK, Kartal MT (2024a) Assessing decarbonization: a comparison of the green sacrifice ratio for China and India. Int J Sust Dev World. https://doi.org/10.1080/13504509.2023.2294461

Erdogan S, Kartal MT, Pata UK (2024b) Does climate change cause an upsurge in food prices? Foods 13(1):154

Fatima N, Li Y, Ahmad M, Jabeen G, Li X (2021) Factors influencing renewable energy generation development: a way to environmental sustainability. Environ Sci Pollut Res 28(37):51714–51732

Fernández-Macho J (2018) Time-localized wavelet multiple regression and correlation. Physica A 492:1226–1238

Glomsrød S, Wei T (2018) Business as unusual: the implications of fossil divestment and green bonds for financial flows, economic growth and energy market. Energy Sustain Dev 44:1–10

Guan Y, Yan J, Shan Y, Zhou Y, Hang Y, Li R, ... Hubacek K (2023) Burden of the global energy price crisis on households. Nat Energy 8(3):304–316

Hammoudeh S, Nguyen DK, Sousa RM (2014) Energy prices and CO2 emission allowance prices: a quantile regression approach. Energy Policy 70:201–206

Hammoudeh S, Ajmi AN, Mokni K (2020) Relationship between green bonds and financial and environmental variables: a novel time-varying causality. Energy Econ 92:104941

Hunjra AI, Hassan MK, Zaied YB, Managi S (2023) Nexus between green finance, environmental degradation, and sustainable development: evidence from developing countries. Resour Policy 81:103371

IEA (2022a) Global Energy Crisis. https://www.iea.org/topics/global-energy-crisis. Accessed 15 Aug 2023

IEA (2022b) World Energy Outlook 2022. https://www.iea.org/reports/world-energy-outlook-2022, Accessed on 15 August 2023

IEA (2022c) Global CO2 Emissions rebounded to their highest level in history in 2021-news. https://www.iea.org/news/global-co2-emissions-rebounded-to-their-highest-level-in-history-in-2021. Accessed 15 Aug 2023

Ji Q, Li J, Sun X (2019) Measuring the interdependence between investor sentiment and crude oil returns: new evidence from the CFTC’s disaggregated reports. Financ Res Lett 30:420–425

Kanamura T (2020) Are green bonds environmentally friendly and good performing assets? Energy Econ 88:104767

Kartal MT (2022) The role of consumption of energy, fossil sources, nuclear energy, and renewable energy on environmental degradation in top-five carbon producing countries. Renew Energy 184:871–880

Kartal MT (2023) Production-based disaggregated analysis of energy consumption and CO2 emission nexus: Evidence from the USA by novel dynamic ARDL simulation approach. Environ Sci Pollut Res 30(3):6864–6874

Kartal MT, Ali U, Nurgazina Z (2022) Asymmetric effect of electricity consumption on CO2 emissions in the USA: analysis of end-user electricity consumption by nonlinear quantile approaches. Environ Sci Pollut Res 29(55):83824–83838

Kartal MT, Ertuğrul HM, Taşkın D, Ayhan F (2023a) Asymmetric nexus of coal consumption with environmental quality and economic growth: Evidence from BRICS, E7, and Fragile Five countries by novel quantile approaches. Energy Environ. https://doi.org/10.1177/0958305X231151675

Kartal MT, Pata UK, KılıçDepren S, Depren Ö (2023b) Effects of possible changes in natural gas, nuclear, and coal energy consumption on CO2 emissions: evidence from France under Russia’s gas supply cuts by dynamic ARDL simulations approach. Appl Energy 339:120983

Khan I, Muhammad I, Sharif A, Khan I, Ji X (2024) Unlocking the potential of renewable energy and natural resources for sustainable economic growth and carbon neutrality: a novel panel quantile regression approach. Renew Energy 221:119779

KılıçDepren S, Kartal MT, Ertuğrul HM, Depren Ö (2022) The role of data frequency and method selection in electricity price estimation: comparative evidence from Turkey in pre-pandemic and pandemic periods. Renew Energy 186:217–225

Kirikkaleli D (2023) Environmental taxes and environmental quality in Canada. Environ Sci Pollut Res 30:117862–117870

Kripfganz S, Schneider DC (2020) Response surface regressions for critical value bounds and approximate p-values in equilibrium correction models. Oxford Bull Econ Stat 82(6):1456–1481

Lee CC, Lee CC, Li YY (2021) Oil price shocks, geopolitical risks, and green bond market dynamics. North Am J Econ Finance 55:101309

Li S, Sun H, Sharif A, Bashir M, Bashir MF (2024) Economic complexity, natural resource abundance and education: implications for sustainable development in BRICST economies. Resour Policy 89:104572

Mahmood H, Asadov A, Tanveer M, Furqan M, Yu Z (2022) Impact of oil price, economic growth and urbanization on CO2 emissions in GCC countries: asymmetry analysis. Sustainability 14(8):4562

Marín-Rodríguez NJ, González-Ruiz JD, Botero S (2022) Dynamic relationships among green bonds, CO2 emissions, and oil prices. Front Environ Sci 10:992726

Marín-Rodríguez NJ, González-Ruiz JD, Botero S (2023) A wavelet analysis of the dynamic connectedness among oil prices, green bonds, and CO2 emissions. Risks 11(1):15

Meo MS, Karim MZ (2022) The role of Green Finance in reducing CO2 Emissions: an empirical analysis. Borsa Istanbul Rev 22(1):169–178

Mohamued EA, Ahmed M, Pypłacz P, Liczmańska-Kopcewicz K, Khan MA (2021) Global oil price and innovation for sustainability: the impact of R&D spending, oil price and oil price volatility on GHG emissions. Energies 14(6):1757

Noguera-Santaella J (2016) Geopolitics and the oil price. Econ Model 52:301–309

Nwani C (2017) Causal relationship between crude oil price, energy consumption and carbon dioxide (CO2) emissions in Ecuador. OPEC Energy Review 41(3):201–225

Okwanya I, Abah PO, Amaka E-OG, Öztürk İ, Alhassan A, Bekun FV (2023) Does carbon emission react to oil price shocks? Implications for sustainable growth in Africa. Resour Policy 82:103610

Pata UK, Cevik EI, Destek MA, Dibooglu S, Bugan MF (2023a) The impact of geopolitical risks on clean energy mineral prices: does the Russia-Ukrainian war matter? Int J Green Energy. https://doi.org/10.1080/15435075.2023.2295867

Pata UK, Kartal MT, Zafar MW (2023c) Environmental reverberations of geopolitical risk and economic policy uncertainty resulting from the Russia-Ukraine conflict: a wavelet based approach for sectoral CO2 emissions. Environ Res 231:116034

Pata UK, Alola AA, Erdogan S, Kartal MT (2023b) The influence of income, economic policy uncertainty, geopolitical risk, and urbanization on renewable energy investments in G7 countries. Energy Econ 128:107172. https://doi.org/10.1016/j.eneco.2023.107172

Pesaran MH, Shin Y, Smith RJ (2001) Bounds testing approaches to the analysis of level relationships. J Appl Economet 16(3):289–326

Polanco-Martínez JM, Fernández-Macho J, Medina-Elizalde M (2020) Dynamic wavelet correlation analysis for multivariate climate time series. Sci Rep 10(1):21277

Raihan A (2023) Nexus between greenhouse gas emissions and its determinants: the role of renewable energy and technological innovations towards green development in South Korea. Innov Green Dev 2(3):100066

Ramzan M, Razi U, Kanwal A, Adebayo TS (2024) An analytical link of disaggregated green energy sources in achieving carbon neutrality in China: a policy based novel wavelet local multiple correlation analysis. Prog Nucl Energy 24:104986

Rasoulinezhad E, Taghizadeh-Hesary F, Sung J, Panthamit N (2020) Geopolitical risk and energy transition in Russia: evidence from ARDL bounds testing method. Sustainability 12(7):2689

Saboori B, Al-Mulali U, Bin Baba M, Mohammed AH (2016) Oil-induced environmental Kuznets curve in organization of petroleum exporting countries (OPEC). Int J Green Energy 13(4):408–416

Sarker PK, Bouri E, Marco CKL (2023) Asymmetric effects of climate policy uncertainty, geopolitical risk, and crude oil prices on clean energy prices. Environ Sci Pollut Res 30(6):15797–15807

Sartzetakis ES (2020) Green bonds as an instrument to finance low carbon transition. Econ Chang Restruct 54(3):755–779

Sharif A, Kartal MT, Bekun FV, Pata UK, Foon CL, KılıçDepren S (2023) Role of green technology, environmental taxes, and green energy towards sustainable environment: insights from sovereign Nordic countries by CS-ARDL approach. Gondwana Res 117:194–206

Sharif A, Sofuoglu E, Kocak S, Anwar A (2024) Can green finance and energy provide a Glimmer of hope towards sustainable environment in the midst of chaos? An evidence from Malaysia. Renew Energy 119982

Sohag K, Taşkın FD, Malik MN (2019) Green economic growth, cleaner energy and militarization: evidence from Turkey. Resour Policy 63:101407

Sweidan OD (2021) The geopolitical risk effect on the US renewable energy deployment. J Clean Prod 293:126189

Tang Y, Chen XH, Sarker PK, Baroudi S (2023) Asymmetric effects of geopolitical risks and uncertainties on Green Bond Markets. Technol Forecast Soc Chang 189:122348

Tedeschi M, Foglia M, Bouri E, Dai PF (2024) How does climate policy uncertainty affect financial markets? Evidence from Europe. Econ Lett 234:111443

Ullah S, Chishti MZ, Majeed MT (2020) The asymmetric effects of oil price changes on environmental pollution: evidence from the top ten carbon emitters. Environ Sci Pollut Res 27(23):29623–29635

Ulussever T, Kartal MT, KılıçDepren S (2023) Effect of income, energy consumption, energy prices, political stability, and geopolitical risk on the environment: evidence from GCC countries by novel quantile-based methods. Energy Environ. https://doi.org/10.1177/0958305X231190351

Wang Q, Li R (2016) Impact of cheaper oil on economic system and climate change: a SWOT analysis. Renew Sustain Energy Rev 54:925–931

Wang KH, Kan JM, Jiang CF, Su CW (2022) Is geopolitical risk powerful enough to affect carbon dioxide emissions? Evidence from China. Sustainability 14(13):7867

Wang T, Umar M, Li M, Shan S (2023) Green Finance and clean taxes are the ways to curb carbon emissions: an OECD experience. Energy Econ 124:106842

www.matteoiacoviello.com (2023) Global Geopolitical Risk Index, https://www.matteoiacoviello.com/gpr.htm, Accessed on 15 August 2023

Yuan R, Rodrigues JFD, Wang J, Tukker A, Behrens P (2022) A global overview of developments of urban and rural household GHG footprints from 2005 to 2015. Sci Total Environ 806:150695

Zaghdoudi T (2017) Oil prices, renewable energy, CO2 emissions and economic growth in OECD countries. Econ Bull 37(3):1844–1850

Zaghdoudi T (2018) Asymmetric responses of CO2 emissions to oil price shocks in China: a nonlinear ARDL approach. Econ Bull 38(3):1485–1493

Zeng Q, Destek MA, Khan Z, Badeeb RA, Zhang C (2023) Green innovation, foreign investment and carbon emissions: a roadmap to sustainable development via green energy and energy efficiency for BRICS economies. Int J Sust Dev World. https://doi.org/10.1080/13504509.2023.2268569

Zhang D, Chen XH, Lau CKM, Cai Y (2023) The causal relationship between green finance and geopolitical risk: implications for environmental management. J Environ Manage 327:116949

Żuk P, Żuk P (2022) National energy security or acceleration of transition? Energy policy after the war in Ukraine. Joule 6(4):709–712

Acknowledgements

Not applicable.

Funding

Open access funding provided by the Scientific and Technological Research Council of Türkiye (TÜBİTAK). Open access funding provided by the Scientific and Technological Research Council of Türkiye (TÜBİTAK).

Author information

Authors and Affiliations

Contributions

The authors have contributed equally to this work. All authors read and approved the final manuscript.

Corresponding author

Ethics declarations

Ethics approval and consent to participate

Not applicable.

Consent for publication

The authors are willing to permit the Journal to publish the article.

Competing interests

The authors declare that they have no competing interests.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Kartal, M.T., Taşkın, D. & Kılıç Depren, S. Dynamic relationship between green bonds, energy prices, geopolitical risk, and disaggregated level CO2 emissions: evidence from the globe by novel WLMC approach. Air Qual Atmos Health (2024). https://doi.org/10.1007/s11869-024-01544-z

Received:

Accepted:

Published:

DOI: https://doi.org/10.1007/s11869-024-01544-z