Abstract

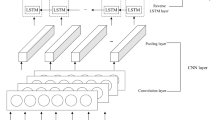

Applying deep learning, especially time series neural networks, to predict stock price, has become one of the important applications in quantitative finance. Recently, some GAN-based stock prediction models are proposed, where LSTM or GRU is used as the generator. However, these generators lack the function of feature extraction, and the prediction accuracies are slightly low. Meanwhile, these models choose some simple volume-price factors (such as OCHLV and OCHLVC) as inputs, without considering the impact of other factors on stock prices. In order to solve these problems, a stock prediction method based on multiple factors and GAN-TrellisNet is proposed. Instead of “OCHLV” or ”OCHLVC,” a multi-factor strategy with ”alpha158+OCHLVC” is introduced to enrich the stock data of inputs. The proposed generative adversarial network (GAN) is a combination of two neural networks which are TrellisNet as generative model and convolutional neural network (CNN) as discriminative model for adversarial training to forecast the stock market. TrellisNet, which integrates the feature extraction capabilities of CNN and the temporal processing capabilities of recurrent neural network (RNN), will generate new predicted results based on historical data, and then CNN will distinguish between predicted results and real stock prices. In order to demonstrate the performance of our method, we selected the decade data of different stocks from four markets (A-shares, U.S. stocks, U.K. stocks and Hong Kong stocks) as dataset and conducted two groups of comparative experiments. Compared with the state-of-the-art methods based on GAN, our method has better performance in terms of MSE, MAE, RMSE and MAPE. In addition, the multi-factor strategy with “alpha158+OCHLVC” is more effective than the original strategy with OCHLVC factors.

Similar content being viewed by others

References

Binkowski MDP, Marti G (2018) Autoregressive convolutional neural networks for asynchronous time series. Paper presented at the 35th International Conference on Machine Learning (ICML), Stockholm, Sweden, 580-589:2018

Mehtab S, DA Sen J (2020) Stock price prediction using machine learning and LSTM-based deep learning models. Paper presented at the Symposium on Machine Learning and Metaheuristics Algorithms, and Applications. Singapore, 88-106:2020

Karasu S, Altan A, Bekiros S, Ahmad W (2020) A new forecasting model with wrapper-based feature selection approach using multi-objective optimization technique for chaotic crude oil time series. Energy 212:118750. https://doi.org/10.1016/j.energy.2020.118750

Karasu S, Altan A (2022) Crude oil time series prediction model based on lstm network with chaotic henry gas solubility optimization. Energy 242:122964. https://doi.org/10.1016/j.energy.2021.122964

Altan A, Karasu S, Bekiros S (2019) Digital currency forecasting with chaotic meta-heuristic bio-inspired signal processing techniques. Chaos, Solitons Fractals 126:325–336. https://doi.org/10.1016/j.chaos.2019.07.011

Abdul-Rahman SMS (2017) Mining textual terms for stock market prediction analysis using financial news. Paper presented at the international conference on soft computing in data science, Singapore, Springer, 293-305 November 2017

Sidra Mehtab JS (2020) Stock price prediction using convolutional neural networks on a multivariate timeseries. Preprint at arXiv: 2001.09769

Sen J MS, Dutta A (2021) Profitability analysis in stock investment using an LSTM-based deep learning model. Paper presented at the 2nd international conference for emerging technology (INCET). Belagavi, 1-9:2021

Roondiwala M, Patel H, Varma S (2017) Predicting stock prices using lstm. Int J Sci Res (IJSR). 6

Jiayu Qiu CZ, Wang B (2020) Forecasting stock prices with long-short term memory neural network based on attention mechanism. PloS one. https://doi.org/10.1371/journal.pone.0227222

Deng S, Zhang N, Zhang W, Chen J, Pan JZ, Chen H (2019) Knowledge-driven stock trend prediction and explanation via temporal convolutional network. Paper presented at the 2019 World Wide Web Conference. San Francisco, 678-685: 2019

Juvenal José Duarte JCCJ, Sahudy Montenegro González (2021) Predicting stock price falls using news data: Evidence from the brazilian market. Comput Econ. 57, 311–340

Yumo Xu SBC (2018) Stock Movement Prediction from Tweets and Historical Prices. Paper presented at the 56th annual meeting of the association for computational linguistics. Melbourne, Australia, 1970-1979 July 2018

Goodfellow IMM, Pouget-Abadie J (2014) Generative adversarial nets. Paper presented at the 27th International conference on neural information processing systems, Cambridge, 2672-2680, 2014

Kong JBJ, Kim J (2020) Hifi-gan: generative adversarial networks for efficient and high fidelity speech synthesis. Adv Neural Inform Process Syst 33:17022–17033

Efros PIJ-YZTZAA (2017) Image-to-image translation with conditional adversarial networks. Paper presented at the IEEE conference on computer vision and pattern recognition. Honolulu, Hawaii, 1125-1134: 2017

Xiong W, Luo W, Ma L, Liu W, Luo J (2018) Learning to generate time-lapse videos using multi-stage dynamic generative adversarial networks. Paper presented at the IEEE conference on computer vision and pattern recognition. Salt Lake City, 2364-2373: 2018

Generating videos with scene dynamics (2016) Carl Vondrick, A.T. Hamed Pirsiavash. Adv Neural Inf Process Syst 29:613–621

Zhang K, Zhong G, Dong J, Wang S, Wang Y (2019) Stock market prediction based on generative adversarial network. Procedia Comput Sci 147:400–406. https://doi.org/10.1016/j.procs.2019.01.256

Lin H-Y, Chen C, Huang G, Jafari A (2021) Stock price prediction using generative adversarial networks. J Comput Sci

Sonkiya P, Bajpai V, Bansal A (2021) Stock price prediction using bert and gan. arXiv preprint arXiv:2107.09055

Li Y, Cheng D, Huang X, Li C (2022) Stock price prediction based on generative adversarial network. Paper presented at 2022 International conference on big data, information and computer network (BDICN), Sanya, China, pp. 637-641, https://doi.org/10.1109/BDICN55575.2022.00122.(2022)

Asgarian S, Ghasemi R, Momtazi S (2023) Generative adversarial network for sentiment-based stock prediction. Concur Comput: Pract Exp 35(2):7467. https://doi.org/10.1002/cpe.7467

Santiago Pellegrini AE, Ruiz E (2011) Prediction intervals in conditionally heteroscedastic time series with stochastic components. Int J Forecast 27:308–319. https://doi.org/10.1016/j.ijforecast.2010.05.007

Dadhich M, Pahwa MS, Jain V, Doshi R (2021) Predictive models for stock market index using stochastic time series ARIMA modeling in emerging economy. Paper presented at the Advances in mechanical engineering. Springer, Singapore, 281-290 June 2021

Zhang GP (2003) Time series forecasting using a hybrid arima and neural network model. Neurocomputing 50:159–175. https://doi.org/10.1016/S0925-2312(01)00702-0

Kai Chen FD Yi Zhou (2015) A LSTM-based method for stock returns prediction: a case study of China stock market. Paper presented at the 2015 IEEE international conference on big data (Big Data), Santa Clara, CA, USA, 2823-2824 December 2015

Wang Z, Huang Y, Cai B, Ma R, Wang Z (2021) Stock turnover prediction using search engine data. J Circuits, Syst Comput 30(07):2150122. https://doi.org/10.1142/S021812662150122X

Wang Z, Su Q, Chao G, Cai B, Huang Y, Fu Y (2022) A multi-view time series model for share turnover prediction. Appl Intell. https://doi.org/10.1007/s10489-021-02979-y

Qin Y, Song D, Chen H, Cheng W, Jiang G, Cottrell G (2017) A dual-stage attention-based recurrent neural network for time series prediction. arXiv preprint arXiv:1704.02971

Mehrnaz Faraz HK (2020) Multi-step-ahead stock market prediction based on least squares generative adversarial network. Paper presented at the 28th Iranian conference on electrical engineering (ICEE). Tabriz, Iran. 1-6 November 2020

Zhou X, Pan Z, Hu G, Tang S, Zhao C (2018) Stock market prediction on high-frequency data using generative adversarial nets. Math Problems Eng. https://doi.org/10.1155/2018/4907423

Mohammad Diqi ASN, Hiswati Marselina Endah (2022) Stockgan: robust stock price prediction using gan algorithm. Int J Inform Technol 14:2309–2315. https://doi.org/10.1007/s41870-022-00929-6

Kumar A, Alsadoon A, Prasad PWC, Abdullah S, Rashid TA, Pham DTH, Nguyen TQV (2022) Generative adversarial network (gan) and enhanced root mean square error (ermse): deep learning for stock price movement prediction. Multimedia Tools and Applications volume 81, 3995–4013. https://doi.org/10.1007/s11042-021-11670-w

Yang X, Liu W, Zhou D, Bian J, Liu T-Y (2020) Qlib: An AI-oriented quantitative investment platform. Preprint at arXiv: 2009.11189

Acknowledgements

This work is supported by the National Natural Science Foundation of China (62071240), the Innovation Program for Quantum Science and Technology (2021ZD0302901), the Natural Science Foundation of Jiangsu Province (BK20231142 and BK20220804) and the Priority Academic Program Development of Jiangsu Higher Education Institutions (PAPD).

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors declare that they have no conflict of interest

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Alpha158 factors

Alpha158 factors

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Liu, W., Ge, Y. & Gu, Y. Multi-factor stock price prediction based on GAN-TrellisNet. Knowl Inf Syst (2024). https://doi.org/10.1007/s10115-024-02085-8

Received:

Revised:

Accepted:

Published:

DOI: https://doi.org/10.1007/s10115-024-02085-8