The Index of the Cycle of Money: The Case of Switzerland

Department of Economics, Economics and Political Sciences, National and Kapodistrian University of Athens (N.K.U.A.), 10559 Athens, Greece

J. Risk Financial Manag. 2024, 17(4), 135; https://doi.org/10.3390/jrfm17040135

Submission received: 12 February 2024

/

Revised: 6 March 2024

/

Accepted: 13 March 2024

/

Published: 22 March 2024

(This article belongs to the Special Issue Emerging Issues in Economics, Finance and Business)

Abstract

:This article focuses on the study of issues related to the functionality and structure of an economy. To achieve this, the theory of the cycle of money is used. The structural features of an economy are reflected in its operational characteristics, and vice versa. The index of the cycle of money indexes how well an economic system can counteract a financial crisis and characterizes how well structured a country’s economy is. Calculations of the index of the cycle of money in Switzerland were compared with the global average index. The results showed that Switzerland is close to the global average; therefore, it has an excellent economy and is equipped to face any economic crisis. The applied methodology abides by theoretical, mathematical, statistical, and econometrical outcomes. This work is significant as it demonstrates the strength of Switzerland’s economy in response to a potential crisis. Prior case studies were reviewed from Latvia, Bulgaria, Serbia, Thailand, Greece, Montenegro, and many other countries. This study postulates that companies with high capital should invest in manufacturing and high technology sectors that should be subject to fewer taxes; this approach facilitates a better distribution of money to the economy by allowing small companies to service the remaining economic activities. The period used for compilations in this study was the global recession of 2007–2017. The reviewed case study results are from a project studying multiple countries, and at present, this article presents the only study about Switzerland’s index of the cycle of money.

1. Introduction

1.1. The Use of Money

The purpose of this article is to utilize the theory of the cycle of money to confirm that Switzerland has an excellent economy. The justification is that Switzerland is one of the few examples of an economic system that perfectly follows the principles of the money cycle, meaning that the country’s financial system adheres to the optimal distribution and reuse of money. This is reflected in the savings that occur in the domestic economy. According to the money cycle, Switzerland’s economic policy is fine because its banking system promotes the economic savings of the country. Enforcement savings are higher than escape savings; these savings contribute to the economy’s robustness through the dispersion and reuse of money, resulting in the successful operation of all economic units and influencing the structure of the economy. This is because a country’s economic structure and functioning are adequate when there is an appropriate distribution and reuse of money, which shows that the structure of the economy is robust, and vice versa. This occurs because, in general, large companies do not substitute the economic functions of small companies that can provide these economic functions. An economic system that achieves high savings relies on economic policy that stands on the low taxation of companies that do not engage in controlled transactions. As a result, neither central bank borrowing nor interventionist policy is required, as these are prevented by the regulatory economic policy provided by the money cycle, which is integrated into the economy’s structure through tax policy.

This study analyzes the theory of the cycle of money in a case study scenario. The research focuses on the index of the cycle of money in the case of Switzerland. As expected, this study confirms that Switzerland can face any financial or economic crisis for a long period without any support. There are many studies and results for other countries, such as Latvia, Costa Rica, Montenegro, Bulgaria, and many others (Challoumis 2021d). The economy of Switzerland has utilized the concept of the cycle of money. According to the theory of the cycle of money, the dynamics of an economy are determined by the frequency with which money is used. An economy should not be considered a closed system but rather a system with fragments, which means that an economy has its limits while also interacting with other economies. This demonstrates that an economy is in a relationship of interaction with other economies, but this relationship has intrinsic characteristics of competitiveness. This means that it is of major importance to determine where savings are made in a financial system: inside or outside of the system. If savings are generated within a country, then the economy does not need the injection of new money, and thus the country does not need to borrow from the banking system, namely the central bank. This description is offered only by the theory of the cycle of money. The use of money determines both the structure and the functioning of an economy, i.e., problems in the functioning of the economy are reflected in its structure, as well as vice versa (Challoumis 2022a, 2023a, 2023e, 2023g, 2024a). Interpreting the aforementioned terms, the presence of fragments of the economic system indicates that an economy interacts with other economies but contemporaneously protects its own money. An amount of money, in many cases, leaves an economy to external banks or other economies. Therefore, the whole concept begins with where the savings take place. Bigger companies and international companies save a large amount of their money in external banks and tax havens. According to this theory, tax authorities should place an additional tax on this kind of company to reduce the losses to the economy. Additionally, small companies and freelancers should be taxed at lower tax rates. Implementing such measures could plausibly increase the dynamics of the economy. Factories, specialized services of large corporations, the healthcare system, and the educational system are special cases in the economy because they improve the quality of the economy and are, therefore, should exempt from taxes. Factories and large specialized companies improve the money cycle because they do not substitute the activities of small- and medium-sized businesses and freelancers (Ainsworth and Shact 2014; Boland 2014; Caldara et al. 2020; Feinschreiber 2004; Gihman and Skorohod 1972; IMF et al. 2017; Kushner 1974; United Nations 2012; Wijnbergen 1987; Wilson 1986). Moreover, educational and healthcare systems improve the quality of the economy and thus boost the economy (Πυλοστόμου 2016). This study seeks to establish how the concept of the cycle of money is applied in the real-world scenario of the economic system of Switzerland and shows that Switzerland is one of the highest-ranked countries based on the index of the cycle of money. The index of the cycle of money indicates how equipped an economic system is to face a monetary crisis and examines how well-structured a country’s economy is (Challoumis 2018b, 2023d, 2023f). To conduct this study, Switzerland’s index of the cycle of money was estimated and compared with the global average. The results show that Switzerland’s index is above the global average and the country could face any financial crisis because it has a well-structured and fully functional economic system.

According to the theory of the cycle of money, taxes are returned to the economy in the form of education and healthcare services (these are exclusions from the mainstream, where taxes support the economy). However, the majority of people believe that tax authorities should keep taxes as low as possible. Moreover, the government should protect small- and medium-sized businesses by levying low taxes while increasing taxes on large businesses. However, some large and international corporations should be taxed at a low rate because they do not compete with small corporations. These types of large corporations include factories and technologically specialized companies. The primary idea is to generate a financial system that optimally supports production

Large companies should not offer products and services that are similar to those of small companies because large companies can invest in economic sectors that small companies cannot support. In this way, an economic system reaches its peak level. Furthermore, the concept of the money cycle demonstrates the importance of the proper allocation of production units and taxes. The principal aim of this study is to assess the index of the cycle of money in Switzerland; moreover, an objective of this study is to answer the question of whether Switzerland is above the worldwide general index rate of the cycle of money according to the simple index or the general index of the cycle of money. Switzerland’s money cycle should be at least similar to or close to the global general index of money cycles to counteract a potential depression. The applied approach is entirely based on mathematical estimates from the relevant theory. The results confirm that Switzerland’s economic system is exceptionally well established, as it does not simply satisfy the general international index rate of the money cycle (0.5), which represents the average global case, but rather has achieved a nearly double rate. The countries near 0.5 and above have an appropriate distribution of money to their financial system. Consequently, Switzerland’s economic system is considered to be perfectly established based on the results of this study. The question regarding the way the index of the cycle of money functions in the case of Switzerland is answered by the structure of its economy and the way in which money is distributed to its economy. Moreover, Switzerland does not require improvements to create a better index cycle of money (OECD, July 2017).

1.2. Companies of Controlled Transactions

There has been a rapid increase in transactions made through offshore companies and these are mainly due to the continuous evolution of world trade and the internationalization of transactions at the global level. At this point, it is apparent that offshore companies are an important part of global business. The significance of offshore opportunities is mainly demonstrated by the option for company owners to establish offshore companies in any tax haven as well as the ability to transfer company headquarters to another offshore area. The term “offshore” or offshore company means an area far from the coast; this concept was created in England, which is a large island. More specifically, by extension, the term means outside the territory and refers to an entity created for a specific purpose that has a short-term duration and is not governed by the accepted principles of conducting business. The advantages that establishing an offshore company can offer, regardless of the tax haven, include the simplicity of the process of setting up an offshore company as well as the short time required to perfect the incorporation.

Indicatively, it has been demonstrated that in most offshore areas the formation and initial operation of an “offshore” company can be carried out within twenty hours by a single shareholder, without prior preparation (e.g., consultations, negotiations, settlement of details, etc.), since all the details can be settled at the time of incorporation. Moreover, the cost of setting up and operating an offshore company is low. For example, an offshore company can be incorporated in the U.S. for only USD 800; furthermore, the founder of the company does not need to hire a lawyer or notary, nor are there any additional charges in the form of bureaucratic costs such as publications, registrations in the relevant chamber, etc. To operate an offshore company in the U.S., USD 500 to USD 700 is required annually depending on the country where the company is based. Notably, the shareholder has the option to remain anonymous. When forming a company, it is perfectly legal for the shareholder or shareholders of the company to keep their name confidential. More specifically, shareholders can in strict confidence opt to not disclose their identity regardless of whether the details of the registered shares are disclosed or the shares are the property of others. In addition, the option of confidentiality provides other notable incentives (Fotis Karadimakis 2019). The shareholder anonymity of offshore operations has been utilized as a tax avoidance strategy. For example, with this advantage, it was possible for shareholders to avoid the tax implications of holding a wealth of assets, both in the acquisition of high-value assets and as a result of proceeds derived from illegal activities. In addition, paying transfer tax, inheritance, or donations made on real estate transfers can be easily avoided if the shareholder of the offshore company acquires the funds automatically. An important consideration is the protection of offshore assets from possible future claims against creditors since it is not possible to ascertain the real shareholder of an offshore company (Johanessen and Zucman 2014).

1.3. Company Characteristics

The feasibility of setting up offshore companies varies in each tax haven and creates various company types and forms such as holding companies. Determining the form of offshore companies is a method of international tax planning designed to finance offshore activities. The functions of a company operating in third countries are concentrated in it, which either has branches operating there or holds shares from international subsidiaries of offshore companies operating in third countries. The advantages that can be gained by someone who establishes a type of an offshore company are the absence of exchange controls and the deferral of tax payment on capital gains, e.g., capital gains from the sale of a subsidiary. Furthermore, another consideration is financial services companies, which are companies providing financial services located in an offshore country that carry out, as their main purpose, the funneling of loans to a foreign subsidiary. Using a financial services company enables effective profits to be shifted from the foreign subsidiary borrower under a jurisdiction with high tax rates to the offshore jurisdiction with low taxation. At this point, it should be mentioned that the disadvantage of this method to the company is that the countries where these companies are based impose a withholding tax on the amount of interest on the loan. In addition, financial services companies gain more value as businesses since they are headquartered in countries that may have high income and dividend tax rates. By repaying interest, not only are the taxable profits of the borrower company reduced, but it also significantly reduces the dividends to be repaid.

Administrative services companies offer administrative and management services to offshore companies. For example, some offshore activities include not only foreign subsidiaries but groups consisting of parent companies and their subsidiaries, each having different activities. The group may be managed and controlled through an offshore administrative and management company. This scheme has the potential to offer commercial advantages by concentrating all administrative–managerial functions in one body. The establishment of a central administration office in an offshore area is a method of profit transfer where the administrative–management activities of a group of companies are covered by the offshore administrative services company where the company’s remuneration is the percentage of the group’s profits. For these incomes, the company is not taxed or is taxed at very low rates. A licensing company is a company that, using an offshore licensing company, may act as a licensee to a foreign subsidiary. Periodic payments for intellectual and industrial property rights such as patents, copyrights, trademarks, images, audio media, scientific information, and others are used by many jurisdictions as rent, i.e., expenses that reduce the taxable matter of businesses. Finally, trading companies are companies that have the import and export of trade as their main activity.

The use of offshore companies effectively helps to shift profits from a high-tax country to a low-tax country. The trade configuration that can be created in these cases is called a triangular trade. The commercial company that carries out import–export establishes an offshore company that acts as an intermediary between the seller and the buyer. In cases in which the founder company carries out imports, the supplier sends the goods directly to the founding company, and the invoice is issued in the name of the offshore company, which in turn invoices the founder company at an increased price. Similarly, if the parent company can export goods, that commodity is sent to the buyer, and the parent company in turn prices the offshore goods at a lower price. In most offshore jurisdictions where high import duties are imposed, an important position would be for the offshore trading firm not to receive the goods, but to instead resell them to a foreign subsidiary of the firm without clearing the goods from the offshore company’s headquarters. Shipping companies in many offshore areas have introduced favorable regulations for companies whose main business is shipping, which includes chartering ships and renting boats. More specifically, these countries have created favorable tax provisions for shipping companies while giving them the country’s flags, which allows these companies to operate temporarily in the offshore areas of these countries. Moreover, profits from these companies are subject to a low-tax system. Investment companies are allowed to invest the aforementioned funds in countries with high tax rates provided that they have concluded tax treaties with an offshore center. Trusts are based on the idea of property protection. The parties to a trust are the settlor, who transfers the assets to a trust; the trustees; the custodian; and the beneficiary (Hampton 2016). It has recently been discovered that offshore trusts are being used to conceal the identity of testators to avoid money laundering provisions and increased taxation. Moreover, in the last decade, a number of banking companies have been operating as banking institutions used as tax havens.

2. Literature Review

2.1. After World War I

Efforts to eliminate the problems of double taxation led many European countries to sign bilateral agreements that were in force from 1843 to 1913. However, the deals were left at an early stage due to the limited direct payment of taxes before World War I, and most tax revenue came from invoices cut by businesses. Bilateral agreements on double taxation and tax evasion and the benefits they offered remained limited and were not implemented by either country or investors. After a peace break in World War I, its aftermath became the most important topic of discussion for many decades at the center of the diplomatic arena. Then, repairing the damage left behind by the war cost the countries involved dearly. The case of arbitrating inflation and taxation to gradually reduce public debt had significantly different effects on the Western powers, but the tax burden at that time increased sharply in all countries. In a decade, this index has roughly doubled in Britain and increased by about 70% in Germany and 40% in France. Subsequently, state governments took measures to tax those with large incomes as well as large real estate. The governments, having as their main concern the participation of all social strata in the efforts they made for monetary and fiscal stabilization, increased progressive taxes significantly in the following years. Subsequently, at the end of World War II, the phenomenon of tax evasion gained great political interest internationally from various political groups.

Given the sharp increase in the tax burden on bank and capital account holders, their resistance was great against the governments of their countries and they were forced to transfer their funds from the so-called great powers of the time to countries that had the same economic and political problems but were neutral with Europe. Countries that were neutral regarding other European countries during World War II included Switzerland and the Netherlands, and thus assets and funds were transferred to banks in these countries and then reinvested in foreign markets. As far as property taxation was concerned, the migration of wealth to these tax havens guaranteed its holders almost tax exemption. The combination of exchange rate controls by European countries and the general lack of cooperation internationally between the relevant tax administrations of the countries did not help much with the efforts made to identify assets transferred from the investor’s country of residence. Apart from tax and monetary factors, non-double taxation, both for the place of residence and at the source of the revenue, was an important incentive for the recovery of capital mainly in the 1920s and 1930s.

In parallel with the rise of capital over these decades, somehow a setback in the evolution of practices for implementing the tax system occurred; the opportunities that arose for tax circumvention through the export of capital constituted a chronic constant obstacle to the permanent consolidation of tax administrations in Western Europe. Since there was not enough data recorded at that time, it is difficult to estimate the magnitude of the first explosion of tax evasion and the emergence of tax havens internationally. However, there is a very significant sample of the amount of foreign assets that began to be transferred to Switzerland at that time. The then Swiss Minister for Finance Mousy estimated that, at that time, foreign assets amounted to USD 2 billion, or, respectively, as he said, this was the amount of long-term investments of the British in Europe. In the five years from 1925 to 1930, deposits by foreign holders in Swiss banks almost tripled from the original USD 2 billion. This amount was equivalent to all external German debts on the eve of the 1931 crisis and constituted three times the Swiss GDP. At the same time, tax evasion incentives in European offshore financial centers were developed to a greater extent, enabling giant companies to create and develop affordable tax residences close to their territories where they could subject repatriated capital to a low tax rate charge.

Initially, these measures began to be applied in small Swiss states, where tax benefits granted to holding companies were assimilated to current Swiss legislation in the 1920s but were also applied to Liechtenstein and Luxembourg in the 1930s. Offshore companies registered in Switzerland went from 158 to 2000 companies between 1920 and 1940 and from 360 to 1110 in the Grand Duchy between 1933 and 1939. The French and Belgian governments made efforts to prevent the transfer of German funds to neutral countries, which by creating currency devaluation, was the best excuse for the Reich to demonstrate the administration’s inability to restructure the war. The Franco-Belgian camp had decided to gradually withdraw the campaign against international tax evasion committed by its inhabitants. Based on the Genoa conference, the debate on tax evasion was directly linked to the issue of double taxation, stipulating that banking secrecy would be safeguarded. In Geneva, a group of experts, including experts familiar with the big issue of tax evasion that was discussed, had come from the major economic powers of Lon, later the United Nations (Fotis Karadimakis 2019). At that time, the alliance between the government and entrepreneurs became closer when, in December 1922, the Swiss Socialist Party tried to implement a capital levy, which was subsequently seriously opposed. At the end of the referendum on the implementation of this levy, 85% rejected this proposal and the Swiss conservative elite thus adopted an aggressive line in defense of its tax haven. The Lon committee drafted against double taxation and tax evasion and aligned itself with the interests of tax havens along the way. Exchanges of information between Member States to combat tax evasion were to some extent limited to information based on the current tax practices of tax administrations and would have been mandatory for the Member States of the Agency to incorporate. In other words, banking secrecy became legal, and the possibility of an information sharing agreement was temporarily suspended.

In any case, Switzerland has demonstrated that it emphasizes booster savings and reduces foregone savings, thereby strengthening the money cycle. Thus, the money cycle is strengthened through the extraordinary distribution and reuse of money. This approach is discussed in further detail in this study.

2.2. After World War II

Direct tax systems increased the tax base significantly after World War II and during the interwar period, allowing for the implementation of improved control and perception techniques. Furthermore, following the end of the war and during a fifteen-year crisis, the free movement of capital increased dramatically. For example, Woods’ Article 6 of the IMF agreement allowed countries to restrict the flow of capital. Due to the disappearance of pre-war wealth, offshore financing declined sharply, even in Switzerland. Switzerland, regardless of its non-participation in the war, has since been a fortress of economic liberalism in the heart of Europe where transnational wealth management declined in the postwar period. Swiss banks saw a 20% decrease in securities deposits, with the volume accounting for 40% of the maximum amount reached before the financial crisis of 1931. Between 1938 and 1953, Swiss companies, including holding companies, fell by 25%, in addition to Swiss deposits. Offshore business declined in the postwar period, which concerned some supporters of tax cooperation. At the end of the war, European money was transferred to America, where it quickly became the prestige of American banks. Although conflicts over tax evasion ceased to be the focus of international organizations, the United Nations Taxation Commission, which conducted activities beginning in 1947, became a battleground between the northern powers and the emerging postcolonial South. In 1954, the International Criminal Court decided to promote a resolution in the interest of developing intra-European trade and investment, namely the signing of a multilateral agreement between EEC countries to reduce double taxation.

The International Criminal Court’s initiative helped to establish a commission in Switzerland comprising Ministry of Finance representatives; the task of this committee was to draft agreements dealing with double taxation and to bring these standards together in a model treaty. Thus, despite minor disagreements among the great powers (Italy, Germany, and France), this committee was able to reach a consensus, prompting even Switzerland’s representative to applaud the outcome. The Roosevelt administration in 1950 used the OECD Commission against tax havens, resulting in a liberalization of capital flows from the emergence of the Eurodollar market, thus increasing offshore activity. During this period, tax havens spread to former English and Dutch colonies. The spread of tax havens proved detrimental to the US economy due to their increased presence in many markets and, as a result, many companies moved to Western Europe to take advantage of the tax credits offered by these countries. Later, the Kennedy administration began discussions in the OECD on tax evasion in tax havens such as Switzerland. The opposition demonstrated by the political system pressure from the OECD and the increase in offshore activities in Switzerland prompted neighboring countries to create a unilateral alliance and establish a European Commission to tackle tax havens. Despite the pressure Switzerland was under from neighboring countries, this pressure did not affect it as it did not sign an agreement on administrative assistance against tax evasion itself (Fotis Karadimakis 2019).

2.3. Switzerland’s Banking System

The name of the so-called Basel Committee on Banking Supervision is derived from the Swiss city of the same name, where the Bank for International Settlements is located. The Basel Committee on Banking Supervision was founded in 1974 to develop supervisory standards and guidelines for the operation of the banking system. In 1988, the Committee implemented a capital measurement system. The Basel I framework for supervising the international banking system was designed to reduce credit risk by establishing minimum capital requirements. A few years later, in the early 2000s, Basel II replaced Basel I to better reflect credit institutions’ risks and link capital requirements to those risks. The current financial crisis has quickly resulted in the Basel III framework, which establishes regulatory standards for banks’ capital adequacy and liquidity. In recent years, there has been much discussion about international recognition of the content of banks’ capital adequacy rules. The first steps were taken in 1988 when the monetary and supervisory authorities of the banks of the twelve most developed countries—members of the Basel Committee on Banking Supervision—adopted the Basel Capital Accord—Basel I, which stated that the capital of international banks had fallen to low levels due to intense competition and market internationalization. The Basel I Pact identifies banks’ own-fund items and their quality classifications and divides them into main categories, their on- and off-balance-sheet items, depending on the credit risk they contain. Thus, a minimum uniform capital ratio has been proposed, where own funds must be greater than or equal to 8% of the bank’s assets.

There was an initial attempt to harmonize the international supervisory system. It should be noted at this point that the pact was a huge success, becoming the global standard for banking supervision in over a hundred countries in the 1990s. Aside from the positive impact of the pact on the international banking sector, it was also heavily criticized by regulators and banks themselves. Some of the weaknesses of the Basel I Pact are the absence of capital requirements for risks other than credit and market risk, the ability to avoid capital requirements through the development of specific strategies (regulatory capital arbitrage), incentives for reckless risk-taking, and divergence of regulatory capital from economic capital, in particular, the limited sensitivity of credit risk weights for the risk undertaken. In the years that followed, Basel I was amended several times, incorporating more and more provisions for the better functioning of the credit system, until it was replaced by Basel II in June 1999. Taking into account the main weaknesses of Basel I, the Committee adopted in June 1999 a proposal for a new capital adequacy framework to replace the 1988 Pact. Thus, in June 2004, the revised supervisory framework for capital adequacy, also known as Basel II, was issued. The revised framework broadly extends the objective of capital supervision and is based on three pillars or pillars relating to minimum capital requirements, supervisory review, and market discipline. In particular, in June 1999, the Committee adopted a proposal for a new main adequacy framework to replace the 1988 Agreement. This led to the release of the revised framework in June 2004, more commonly known as Basel II. This revised framework included three pillars.

The first pillar concerns the minimum basic requirements, which develop and extend the standard rules laid down in the 1988 agreement. The supervisory review of a banking institution’s capital adequacy and internal assessment process constitutes the second pillar. Procedures are in place for supervisors to review banks’ capital adequacy on an ongoing basis. The establishment of internal control mechanisms to monitor and assess the bank’s capital adequacy and the validity of calculation methods was a necessity. The third pillar concerns the effective use of reporting results through publication rules for more detailed financial data and rules. These relate to corporate governance and management control structures as leverage to strengthen market discipline and encourage sound banking practices. The new framework is designed to improve the way regulatory capital requirements reflect risks and to better address the banking innovation that has emerged in recent years. These three pillars are mutually reinforcing. In more detail, the effectiveness of the rules of the first pillar depends on the ability of supervisors to monitor their correct application through the powers of the second pillar. The disclosure obligations of pillar three also create the right incentives to improve banks’ risk management processes. However, the 2007–2009 financial crisis (the period of 2008 to 2009 was the worst recession in the U.S. since the Great Depression), a period in which the banking sector entered with insufficient liquidity buffers, combined with poor governance in risk management, necessitated the improvement of Basel II through a new pact. Two important issues emerged from the recent financial crisis: one of excessive leverage and the other of illiquidity. Thus, in 2010, the Basel Committee issued two reports that constitute the international regulatory framework known as Basel III, which aims to address these two weaknesses of the system, which were particularly highlighted during the crisis. This new international regulatory framework for banks was developed to revise and strengthen the three pillars of Basel II (Συριόπουλος and Παπαδάμου 2014). The main objectives of this new pact can be summarized in the following two points: first, strengthening of micro-prudential regulatory intervention in the operation of banks and, second, countering the systemic risk that may manifest itself in the financial system through macro-prudential policies.

2.4. Switzerland’s Economy

The EU is a major player in global trade, ranking as the world’s second-largest exporter and importer of goods, behind only China and the United States. Furthermore, the European Union leads the world in service trade. In 2017, the EU’s main partners in the total trade of goods and services were the United States (20% of all extra-EU trade), China (12%), and Switzerland (8%). Between 2008 and 2017, China’s weight increased from 9% to 12%, while the United States’ weight increased from 18% to 20%. On the other hand, Russia’s share of EU trade in goods and services has nearly halved, from 8% to 5%. In 2017, trade in goods made up 70% of total EU trade in goods and services. Looking at goods and services separately, we see similar trends, with prices more than doubling between 2000 and 2017. Both sectors experienced a decline in 2009 due to the financial crisis (CYSTAT 2018). The balance between government and private individuals is very different in Switzerland than in most countries considered developed. Swiss industry has been expansionist and imperialist while the government tends to operate only internally. As a country, it offers more advantages to companies than its neighbors and competitors, the Netherlands. Of course, Switzerland has not taken part in a war and has also never pursued a colonial policy towards less-developed countries as its neighbors did. At this point it is important to mention that the style of each Swiss government has always been comparatively minimalist, reflecting in this way the traditional “social” contract agreement by which the government covers citizens by offering security and justice in exchange for citizens’ loyalty. According to Krayer, former president of the Swiss Private Bankers Association, the Swiss do not like to be governed. In particular, he characterizes the Swiss from their prehistory as farmers who went to the market to buy the cheapest cabbage. By this expression, this means that each party was offered the least freedom to influence the government. Another important element for the Swiss government, according to Krayer, is the federal structure of the state. Each Swiss canton has its autonomy, much more so than the American regions or Canadian provinces, and even more, the municipalities within the cantons also have considerable autonomy where decision-making takes place at the lowest level.

However, important decisions for the smooth functioning of the cantons, such as public expenditure, are largely decided at community and state levels, and decisions on the level of taxes are set at the local level. This results in the creation of a decentralized administration in terms of government and taxation. In applying the structure of this policy, the Swiss believe that self-discipline is imposed at every level of government. Another element of any government that characterizes Switzerland is the sovereignty of the individual. This can be expressed most clearly in the regular holding of referenda, i.e., the implementation of democracy. The striking thing about referendums is that the aim is not to produce extreme results but rather to establish the power of a moderate majority. For example, referendums on shorter working hours, lowering the retirement age, and lowering taxes were rejected by a large majority. Sometimes a change could be approved, but the change would only receive support at the third or fourth opportunity. This process counters extreme policies, thus providing legitimacy to the challenge as well as the emergence of a real prospect of gradual reform. On the contrary, this approach slows down government processes; however, this would not be bad for businesses that want stability and predictability in their environment. The net result of these characteristics is a society designed to rise from the lower floors upwards. Although less important by today’s standards than it was 100 years ago, Switzerland’s neutrality has contributed significantly to the country’s development. With Europe facing serious armed conflicts for many centuries, many opportunities have been created for Switzerland, specifically for traders and manufacturers, thus bringing a large wave of talented and persecuted immigrants to the country. However, Switzerland’s greatest benefit from the neutral stance it demonstrated during the wars is its survival, while the countries involved in war, which are also its neighbors, were hit hard. In addition, given that one consequence of World War II was high inflation, Switzerland acted as a bank for wealthy residents of many countries who tried to preserve the value of their capital. In 1894, an Italian lira was worth as much as a Swiss franc, while in 2002, following Switzerland’s growth trajectory, about 1000 Italian lira was required that year to obtain one Swiss franc, shortly before the lira was replaced by the euro.

Switzerland is a country with minimal foreign debt, high productivity, a GDP per capita among the highest in the world (exceeding that of the richest countries in the European Union), low unemployment rates, and low inflation. Moreover, it boasts one of the highest living standards in Europe and a highly skilled workforce. According to Credit Suisse, the Swiss economy was forecast to grow by 1.2% in 2016. A real economic recession is considered unlikely, despite the strong Swiss franc. The current forecasts are positive according to the bank’s economists, due to the continued strong domestic economy. Moreover, Credit Suisse forecasted the 2016 unemployment rate to be 3.7% and the economy’s export performance to increase by 2% (after a decline of 0.5% in 2015). Currently, the economic environment is expected to improve, particularly in the euro area, and driven by continued growth in the United States, whose demand for Swiss goods was also forecasted to be strong in 2016. In addition, the exchange rate for the export industry, among other things, owing to the maintenance of negative interest rates by the Swiss National Bank, and sporadic foreign purchases will assist in increasing exports. The demographic problem with the gradual aging of the population and the consequent reduction in the supply of labor is a cause for concern for the bank’s economists. With labor productivity stable at the levels it has reached in recent years, it is necessary to admit 40,000 to 50,000 immigrants annually and to support their participation in domestic labor in order to maintain increasing trends. Finally, according to Credit Suisse’s forecasts, the supply of labor in the—very important and fully internationalized—health sector will be the sector with consistently high demand for health services in the coming years, even requiring an increase in labor productivity, which is something that can be achieved mainly owing to information technologies (e.g., e-health) (Ministry of Foreign Affairs 2024).

3. Materials and Methods

In this study, the applied methodology was tested multiple times, which was sourced from other articles in different case studies (Challoumis 2021c). For the authorities using the arm’s length principle, it is challenging to obtain data on controlled transactions, as international companies offer similar data to those of uncontrolled transactions, which are concealed to avoid paying taxes. Therefore, governments should apply the fixed-length principle. The fixed-length principle indicates that the companies of controlled transactions manage transactions and avoid tax payments. Then, according to the fixed-length principle, international companies should pay a fixed amount of tax. In this way, the cycle of money is enhanced because large companies do not direct money away from society and the economy and international banks. As a result, the profits of large companies are not invested back into society, and ultimately this contributes to a decrease in consumption (Bourdin and Nadou 2018; Challoumis 2018c, 2019b, 2019c, 2020a, 2021b, 2021d; Driver 2017; Dybowski and Adämmer 2018; Khan and Liu 2019; Marques 2019; Miailhe 2017; Ortun et al. 2017; Shamah-Levy et al. 2019; Taub 2015). Therefore, according to the fixed-length principle, the local companies that save their money in local banks should have lower tax rates.

In conclusion, the fixed-length principle serves the theory of the cycle of money, where small- and medium-sized companies pay lower taxes than large companies; in this way, large companies do not substitute the commercial activities of small- and medium-sized companies (Dybowski and Adämmer 2018; Koethenbuerger 2011; Limberg 2020; Mancuso and Moreira 2013; Ortun et al. 2017; Prestianawati et al. 2020). On the other hand, the arm’s length principle estimates taxes based on methodologies provided by the companies that make international transactions. In this way, the large companies cover the activities of the small companies. Finally, the mainstream approach is that small- and medium-sized companies boost the distribution of money to a country’s economy as typically they do not hold their money outside of the country’s economic system, and instead the money is directed back into the economy. Therefore, money distributed within an economy increases the cycle of money many times. The reason why local money increases the cycle of money is obvious according to Equation (4) of the general index of the cycle of money (Rashid et al. 2020; Siegmeier et al. 2018; Sikka 2018; Tuter 2020; Van de Vijver et al. 2020; Wright et al. 2017).

A prior application of the theory of the cycle of money can be found in the case of Latvia, which has an index in the 0.5 range, indicating that it is a well-structured economy that will not collapse into a severe economic crisis. In the case of Costa Rica, the index of the money cycle is close to 0.5, indicating that the country can face a severe economic crisis, at a slightly lower risk than countries with lower index rates. Countries that exceed the index value of 0.2 can counteract potential crises (Arai et al. 2018; Bartels 2005; Castro and Scartascini 2019; Challoumis 2018c, 2019b, 2019c, 2020a, 2021b, 2021d; Ewert et al. 2021; Holcombe 1998; Kiktenko 2020; Koethenbuerger 2011; Martinez and Rodríguez 2020; Ratten 2019; Ruiz et al. 2017). The methodology used in the current study for Switzerland is presented below, which is consistent with the presented theory. The following mathematical equations help to clarify the calculations for the money cycle:

According to prior studies (Challoumis 2023c), “The is the velocity of financial liquidity, is the velocity of escaped savings and is the cycle of money. The is the index of the cycle of money, is the national income or GDP, and is the bank deposits of the country.” In addition, symbolizes the general index of of the country, is the index of of the country, and is the global index of . The is the condition of the economy (GDP), the a is the cost savings from the economy, and the m is the money that is maintained in the economy. Finally, is the general global index of , and is obtained as a global constant (Amanor-Boadu et al. 2014; Challoumis 2018a, 2019a, 2019d, 2019e; Prestianawati et al. 2020; Saraiva et al. 2020; Zamudio and Cama 2020).

Proof.

Equations (4) and (5) show that an economy close to the value of 0.5 can immediately face an economic crisis. Results close to this value represent an appropriate index of the cycle of money, revealing an adequate economic structure of the society and then the fine distribution of money between the citizens—consumers. Equation (1) is the term for the cycle of money, which is used to define the and of Equation (2). The cycle of money to a quantity value is expressed by GDP, which is an expression of , according to and based on . Then, − , formed on . Thus, S is the savings, I is the investments, and X is the exports. Then, S′ is the savings directed into banks out of the country’s economy, I′ is the investments directed into banks out of the country’s economy, and M is the imports. The cycle of money expresses the GDP as the follows: . According to the theoretical background of this study, for money directed away from economies, the problem of controlled transactions could be addressed, if an organization could identify the money transitions between the economies, by conducting a comparison of the global economies using ΔS, ΔI, and (X-M) (Challoumis 2018b, 2020b, 2021a, 2021e, 2022b, 2022c, 2023b, 2023f, 2024b). Then,

Equation (6) reveals more about the economic policy of the cycle of money, as the difference between the parts of the prior equation defines that the result identifies the liquidity value and where the money is kept. According to the money cycle, all savings and investments are not sufficient. The key point is whether these savings are enforcement or escape savings. Proportionally, the same separation exists for investments as for enforcement and escape investments. Enforcement savings are savings that remain in the local banking system, and escape savings are savings that are directed outside of the local economic system. Enforcement investments are those made by companies that do not substitute the economic functions of small ones. In this way, the whole economic system is active, and simultaneously the large companies invest capital in factories and highly specialized activities. Then, the whole economic system is fully active. Contemporaneously, the structure of the economy is formed and regulated appropriately, as all economic units find their position. On the contrary, escape investments are investments that substitute small companies, direct profits outside of the economy, or money sent for investments outside the economic system. According to enforcement savings and investments, the economy is boosted, as the distribution and reuse of money are increased. Then, the cycle of money has increased, the economic function is at its maximum level, and the structure of the economy has auto-formed. On the other hand, escape savings and investments lead to minimum distribution and reuse of money. The cycle of money eliminates the side effects of interventionism on the public and monetary policy or the autoregulation of the market. Both of these side effects are replaced by an appropriate regulatory tax and public policy according to the money cycle. The regulation policy consisting of higher taxes to companies in order to do not substitute the economic functions of small ones and subsidies for companies that invest capital in factories and highly specialized activities leads to the formation of an adequate money cycle. The application of low taxes boosts the money cycle. The only taxes that return to the economy and support its quality characteristics are those pertaining to the education and healthcare system, as the money cycle suggests. The banking system has a necessary role in the money cycle, as indicated by the economic system in which the money is saved, which is crucial for the distribution and reuse of money. Then, the function of money, via the distribution and the reuse of money, clarifies the structure of the economy through the manner in which all economic units are active. Therefore, according to the theory of the cycle of money, the economic function reflects the structure of the economy and, at the same time, the same function identifies the condition of an economy through its structure.

This study is based on real economic data and their rates per GDP (Al-Ubaydli et al. 2021; Camous and Gimber 2018; Kamradt-Scott and McInnes 2012; Strassheim 2019; Ud Din et al. 2016). The period 2007–2017 was a period of general recession, particularly in Europe, and as a result, multiple countries were scrutinized during this time. The OLS test presents the following general form, according to Equations (1)–(6):

All variables are defined except for c, which is the constant, and the multipliers , , and . □

4. Results

Table 1 shows bank deposit parameters, GDPs, and money cycle indexes. The econometric application of OLS estimations is based on Equation (7). This section demonstrates how Switzerland’s money cycle index is dependent on Swiss bank deposits and Switzerland’s GDP per capita. The global average bank deposits and global GDP per capita were used to compare the Swiss economy and bank deposits. The data are from the World Bank.

Then, for these variables, yearly data from 2007 to 2017 were used (Table 1). Bank deposits according to the definition of the World Bank (The World Bank 2024) are defined as “the total value of demand, time and saving deposits at domestic deposit money banks as a share of GDP. Deposit money banks comprise commercial banks and other financial institutions that accept transferable deposits, such as demand deposits”. The applied equation is:

where constant, Switzerland’s bank deposits, Switzerland’s GDP per capita, global bank deposits, and d_Global index of the cycle of money.

The dependent variable of the OLS test is the index of the money cycle of Switzerland with independent variables presented in Table 2. Therefore, the Durbin–Watson test returns a value of 1.502193, showing that it belongs to the applicable level of 1.5–2.5 values, with p-value = P(F(1, 4) > 0.0896876) = 0.779491. Moreover, according to LM (Lagrange Multiplier), no autocorrelation exists in the model ( no autocorrelation), as p = P(F(1, 4) > 0.0896876) = 0.779491. The test for normality of residuals ( hypothesis: error is normally distributed) is satisfied as p = 0.587518. The p-values of all variables in Table 2 are lower than 0.05; therefore, the results are applicable, as the initial hypothesis ( no relation of variables) has been rejected (Mcleod 2023).

It should be noted that *** represents statistically significant at the 1% level, ** represents statistically significant at the 5% level, and * represents statistically significant at the 10% level (Table 2).

Heteroskedasticity does not exist as, according to White’s test, the p-value should be higher than 0.05, which is then satisfied by p-value = P(Chi-square(9) > 9.438238) = 0.397843 (Table 3). Based on these results and the theoretical concept, the country’s economic structure is clarified, as Switzerland belongs to excellent economies. According to these statistical findings, it is possible to proceed to Switzerland’s money cycle. The VAR (Vector Autoregression) model has the following form:

where is about the vector of endogenous observations, like Switzerland’s index of the cycle of money, Switzerland’s bank deposits, and Switzerland’s GDP per capita. Finally, is about the vector of exogenous observations, like the d_Global index of the cycle of money, and Global bank deposits. contains all deterministic variables, and is a dimensional unobservable zero mean white noise process with a positive definite covariance matrix. Therefore, a more analytic view is obtained by VAR (Vector Autoregression) results (Abdallah et al. 2020).

The p-values clarified that all are greater than 0.05, implying that the residuals are white noise and, therefore, the model is valid. The results of impulse responses are as follows (from Table 4):

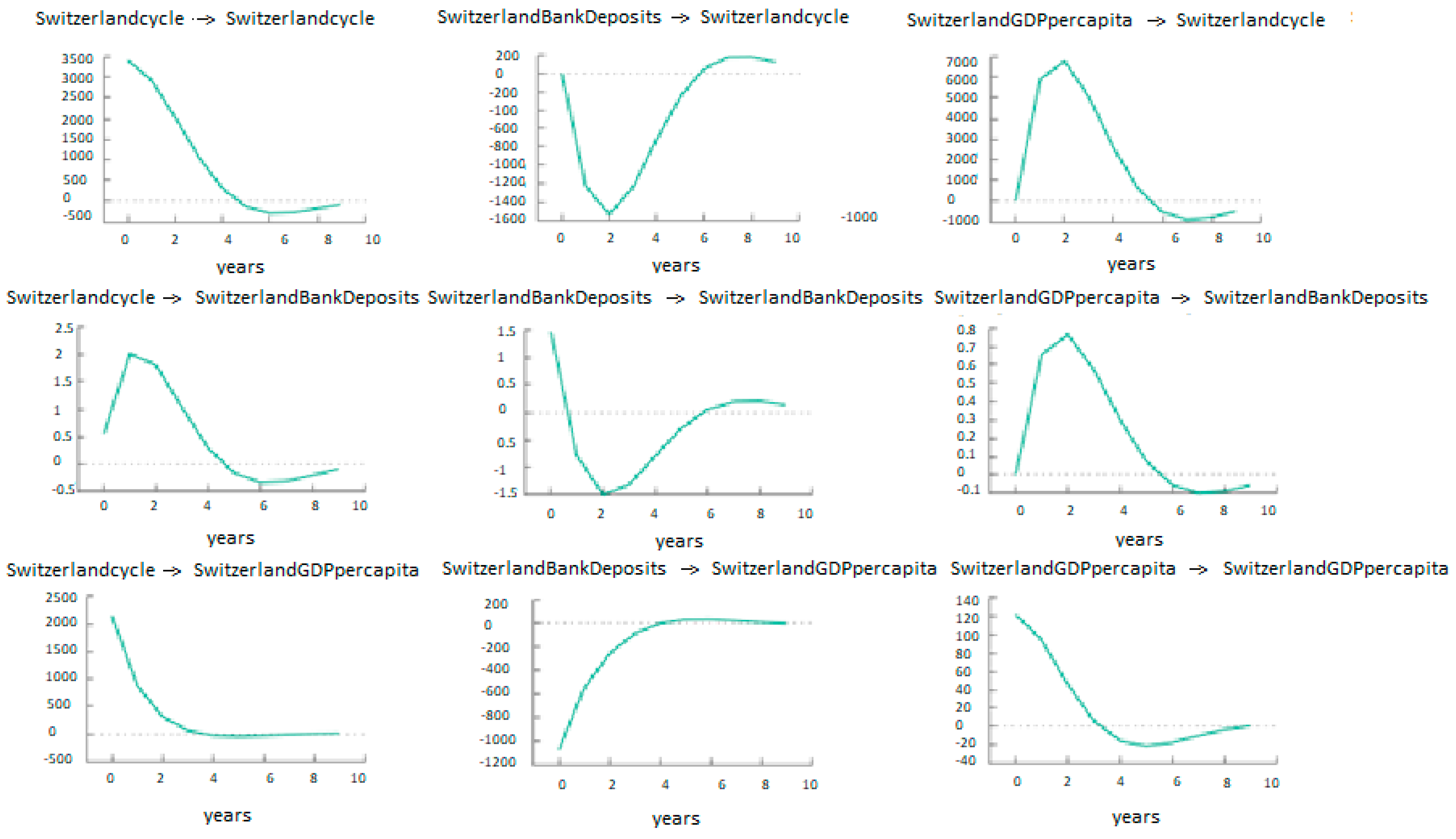

Figure 1 presents impulse responses, where impulse-responses functions (on the graph are Switzerlandcycle, SwitderlandBankDeposits, and SwitzerlandGDPpercapita) describe the evolution of variables of interest along a specified time horizon after shocks in a given moment. According to Equations (3)–(5), the indexes of Switzerland’s money cycle were obtained.

The indexes reveal Switzerland’s distribution of money and the quality of its economic structure (see Table 5).

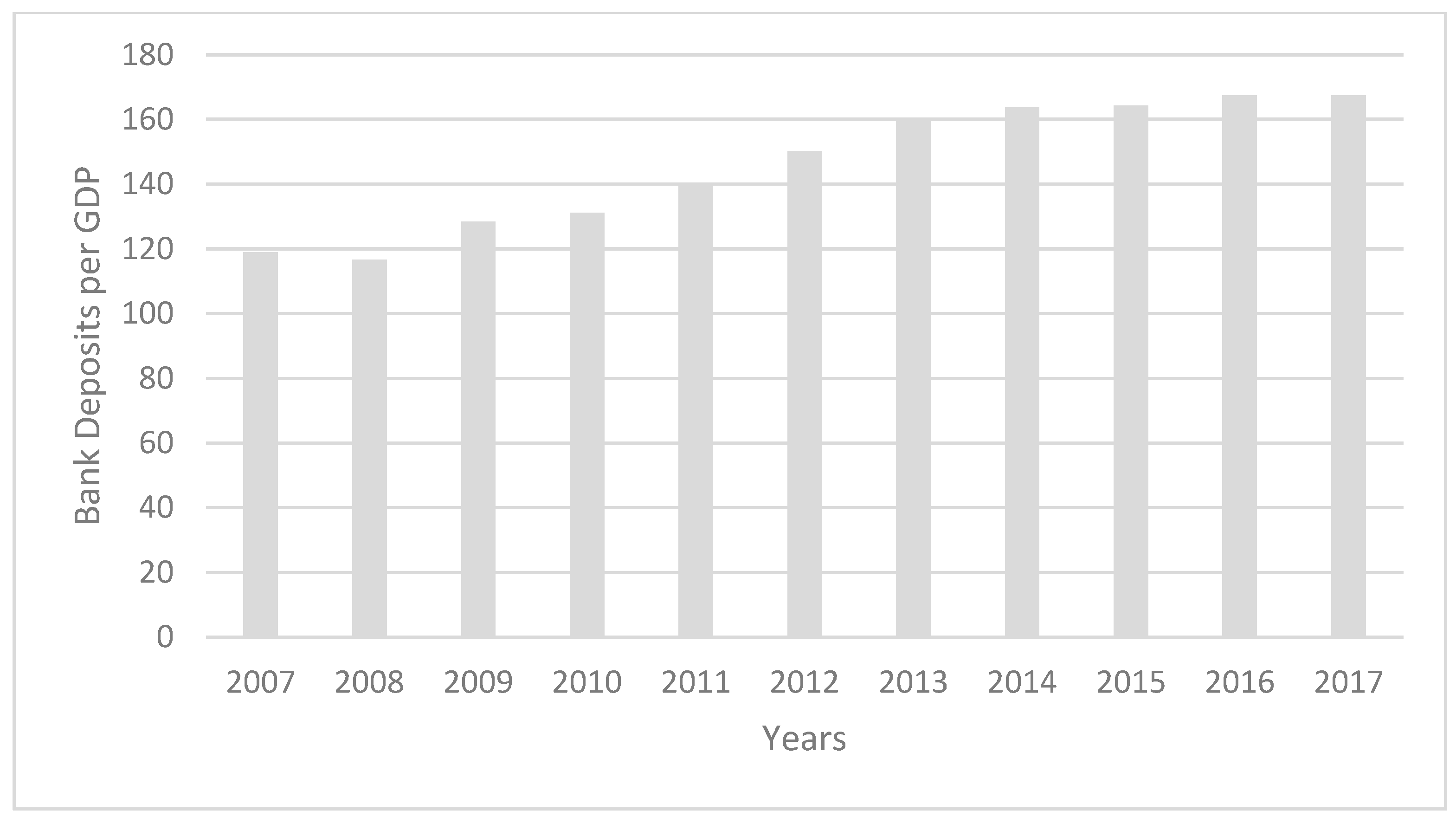

Switzerland’s bank deposits (from Table 1):

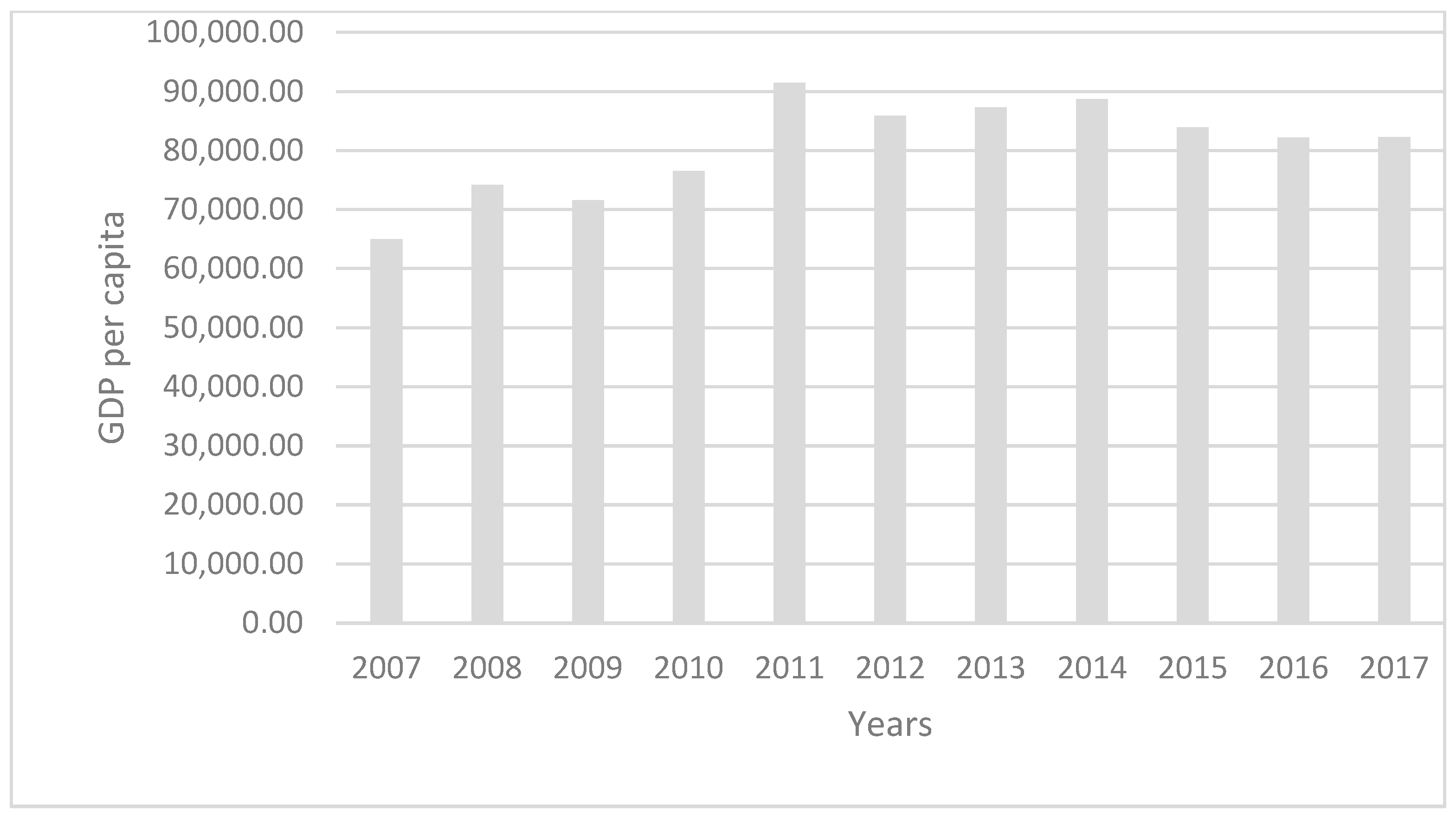

Switzerland’s GDP per capita (from Table 1):

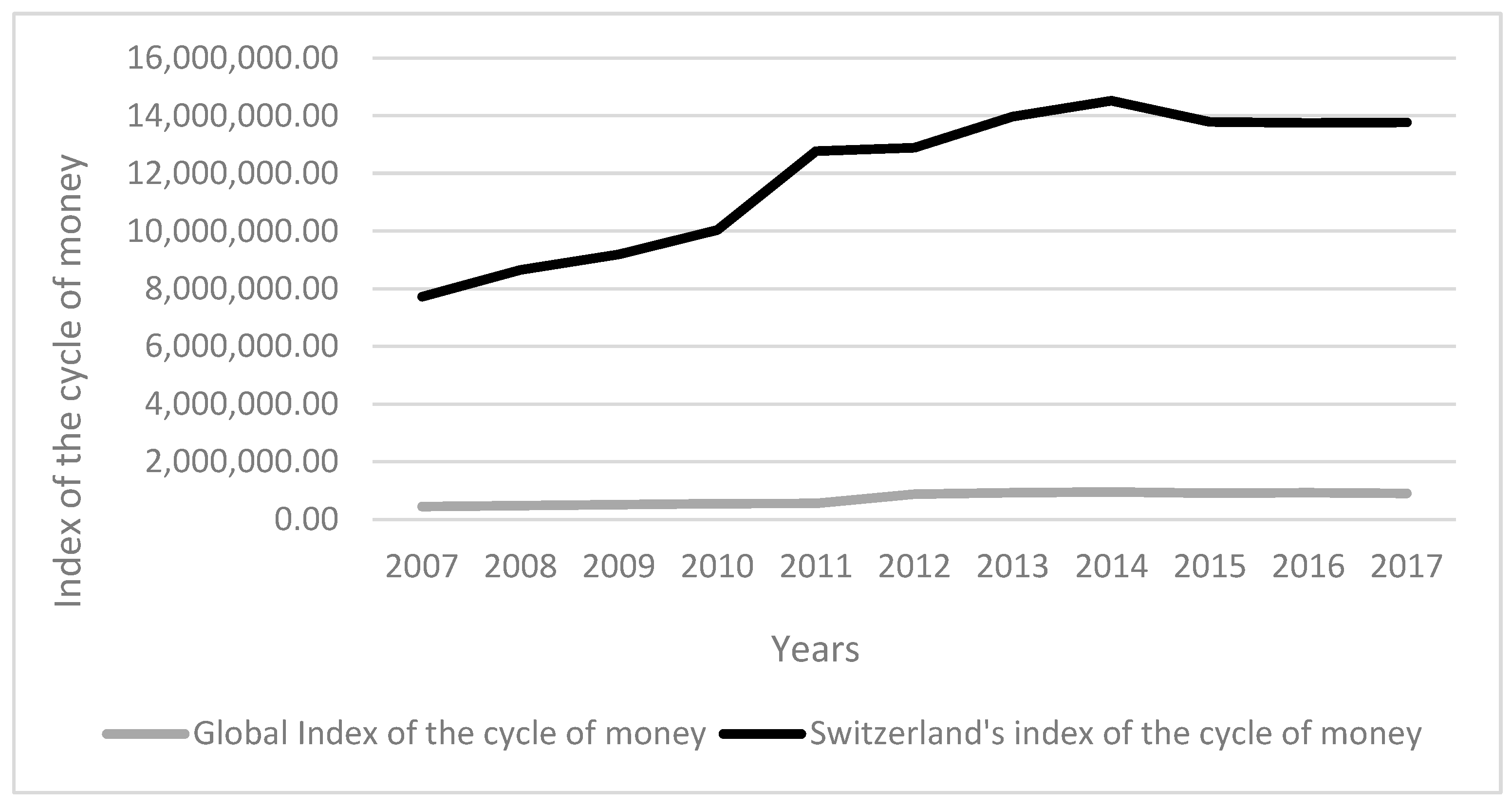

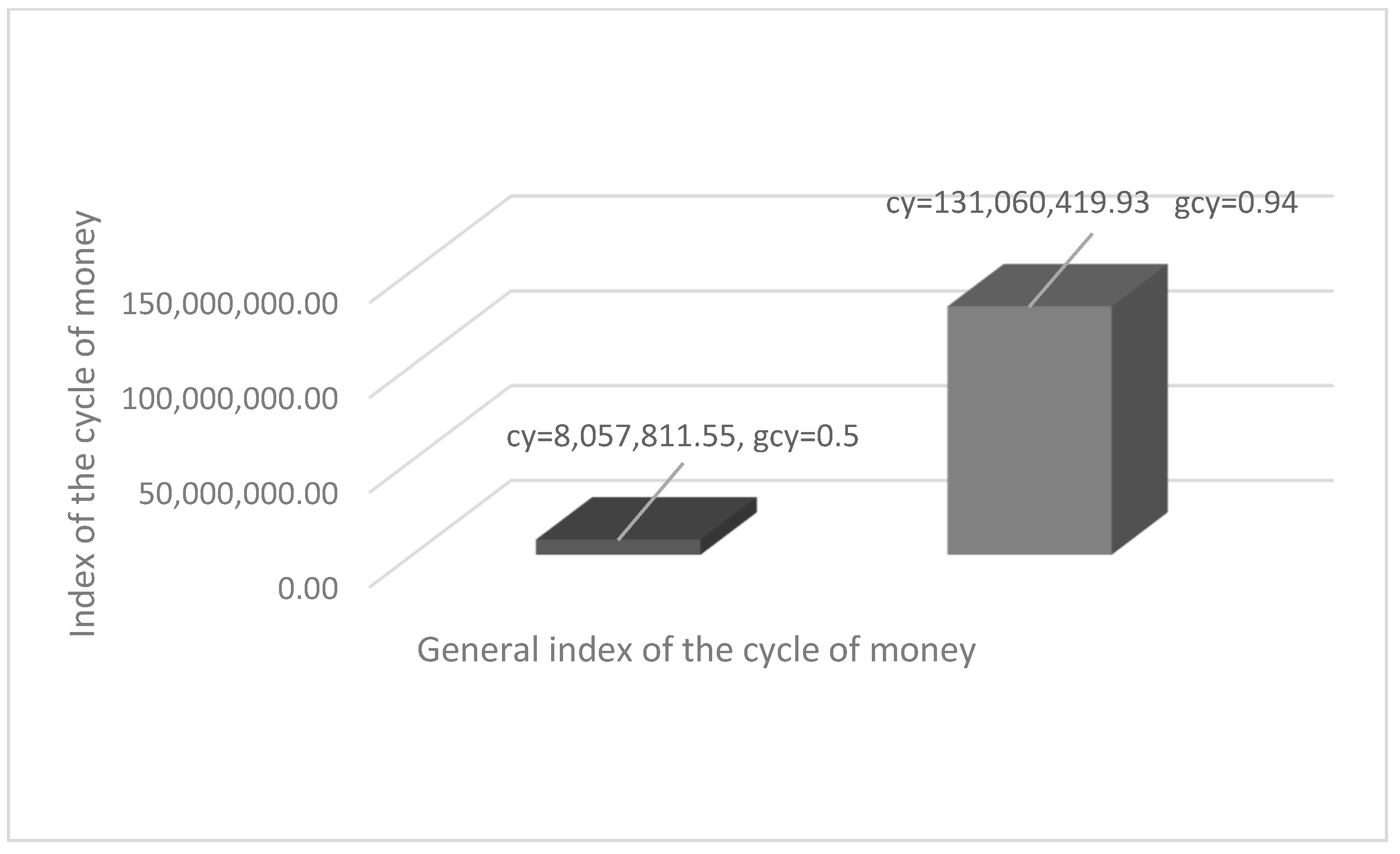

Figure 2 presents the condition of bank deposits per capita of Switzerland’s economy for the period from 2007 to 2017. Moreover, the next scheme (Figure 3) presents the GDPs of Switzerland, for the same period. According to prior results, the index of Switzerland’s is USD 131,060,419.93. The index of the global average is USD 8,057,811.55. The general index for Switzerland is is 0.942079399. The general index of the global view is 0.5. Therefore, it is clarified that Switzerland’s index cycle of money is close to the global average cycle of money. Therefore, the dynamics of Switzerland’s economy comply with the global average. Then, the results of the next scheme (from Table 5).

The index of the cycle of money of Switzerland’s economy is above average and excellent considering the global average of the index of the cycle of money, which is 0.5. The countries that are close to 0.5 have well-structured economies—based on Equation (5) and according to the theoretical concept of the cycle of money. This conclusion means that the economic structure of Switzerland has a perfect distribution of money to its economy. The results are shown in the index of the money cycle of Figure 4, based on Equation (3); the general index of the money cycle of Figure 5, based on Table 5; and Equations (4) and (5).

The prior scheme presents the combination of the index of the cycle of money with the case of the general index of the cycle of money. The affiliation between the global average indexes and Switzerland’s index indicates that Switzerland is in the category of excellent countries according to the global average index of the cycle of money, both for the simple index and general index. The explanation for this result is that this financial system belongs to an absolute level of the cycle of money, meaning that Switzerland has achieved a perfect economic dynamic because the structure of the economy is improving.

5. Discussion

5.1. Switzerland’s Economic Environment

Initially, Switzerland’s small size forced businesses based and operating in the country to internationalize. From 1920 onwards, 80% of their production was exported abroad by companies. In addition, Swiss companies managed to significantly increase their foreign direct investment at the end of the 19th century. In 1914, 29 out of 57 companies managed to export most of their production to major markets such as Asia and the U.S. The intensity of world trade measured as exports and imports of 46 goods and services, divided by GDP, shows that Switzerland ranks third internationally in income exchange, which includes income payments and receipts concerning internationally traded factors of production. In addition, in 2005, the population of Switzerland, according to data, was occupied by foreign residents, thus placing Switzerland in the first place of countries whose population is largely made up of foreigners. Indeed, even in the Swiss business world, the most successful entrepreneurs were foreigners. In other words, a part of the success of the country is also occupied by immigrants who later became involved in the business field. For example, well-known foreign businessmen in Switzerland were Henri Nestlé who was a German political refugee, and Charles Eugene Lancelot Brown who was from the United Kingdom. In addition, another example is Zino Davidoff, who was a Russian Jewish immigrant.

The success of immigrants in Switzerland seems to be a result of the Swiss environment offered by the country and the immigrant mentality. A small and different country by nature, the people of Switzerland were forced to develop an understanding of the benefits of immigration by opening up to people with different cultures and civilizations. As in other countries, in Switzerland, immigrants are initially viewed with suspicion until they demonstrate reciprocity by contributing positively to their new home (Fotis Karadimakis 2019). In their homeland, immigrants are more likely to have the comfort of being part of a community, while in a new country, they would have to first establish a new existence, and from the results of their achievements, they could gain respect from the local inhabitants. In addition to commercial success and potential wealth creation (Johanessen and Zucman 2014), migrants have the opportunity to advance up the social ladder and build a better life, thus fulfilling the basic reason for their migration. However, this does not mean that Switzerland was the first choice for permanent immigration. Powerful thinkers such as Einstein, Erasmus, Lenin, Rousseau, Bakunin, and Trotsky lived in Switzerland, but their work was not much appreciated. Many entrepreneurs innovated and exported their innovations abroad. For example, César Ritz exported Swiss ingenuity into hotel management, thus developing a luxury standard that transcended his life and is synonymous with his name. Therefore, this bilateral flow of intellectual and business energy of the highest quality has played and continues to play an important role in Switzerland’s highly sophisticated industry, which never ceases to evolve and harmonize.

5.2. Switzerland’s Economic Results

Large companies should provide economic activities that small businesses cannot support; moreover, authorities should impose low taxes on specialized companies and factories. Furthermore, large companies should no longer replace small businesses’ activities. The investments of a country are ameliorated by increasing the distribution of money. In general, a country with a well-formed economic system is a country with a good cycle of money and, therefore, is equipped to face an economic crisis. Therefore, companies with high capital should invest in the manufacturing and high technology sectors that should be subject to fewer taxes; this approach facilitates better distribution of money to the economy and small companies, which supports other economic sectors. The same time, smaller companies should have the most lower taxes. The bigger companies that substitute their activities should be taxed higher, until these bigger companies become factories or high technological units. Furthermore, the question that arises is whether authorities can successfully implement more structural changes to their economies in order to achieve even better economic results, following the theory of the cycle of money. However, Switzerland is a different case in that its economic system receives more than it distributes. This means that the banking system works adequately in that savings are oriented to the local banking system. In addition, Switzerland simultaneously receives savings from foreign economic systems, thus increasing its cycle of money. In this way, the distribution and the reuse of money are ideal, contemporaneously affecting both the functionality and the structure of the economic system. Therefore, Switzerland’s economic system is superior and above the index of common GDP per capita, in general, but especially from 2007 to 2017 using the index of average GDP per capita.

5.3. Switzerland’s Money Cycle Contribution

The contribution of this article is important as it confirms previous studies; however, in the case of Switzerland, which has an excellent economy, there are few examples verifying both the theoretical model and the equations quoted. The case of Switzerland is one of the few examples of economic systems that perfectly satisfy the principles of the money cycle, i.e., the financial system of Switzerland serves the optimal distribution and reuse of money. This is also reflected in the savings that take place in the local economy. Essentially, this study presents the implementation of the money cycle of an economy that satisfies these principles. In other words, Switzerland’s economic policy is appropriate because the banking system serves the economic savings of that economy well. Because enforcement savings are extremely large compared with escape savings where no money leaves the economy, serving its robustness through the dispersion and reuse of money results in the operation of all economic units, which ultimately affects the structure of the economy. This is because its structure and functioning are correct, in line with their interrelation, since an appropriate reuse of money means that the structure of this economy is correct, and vice versa. This presupposes an economic policy based on low taxation of companies that do not engage in controlled transactions, companies that do not substitute economic functions of small companies that can provide these economic functions, or on an economic system that achieves high savings in the economic system, according to Equation (6). The money cycle is the evolution of GDP and reflects both the proper structure and the functioning of the economy. Therefore, neither borrowing from the central bank nor interventionist policy is required, as these activities are prevented by the regulatory economic policy provided by the money cycle, with the structure of the economy determined through tax policy.

6. Conclusions

6.1. Switzerland’s General Economic Conclusions

Direct democracy is an important part of Switzerland’s political system. Any citizens’ group with the ability to organize and directly collect 50,000 signatures can hold a referendum on any law passed by parliament. If there is a referendum on a law, then it will be put to a popular vote, which can prove to be costly, time-consuming, and present uncertainty regarding the outcome. Political parties, for their part, are attempting to anticipate the concerns of interest groups and reach an agreement with them on the existence of a suitable solution. The referendum tool provides a better understanding of why the Swiss format has evolved into a mechanism capable of finding compromises and taking into account potential veto concerns. The result of this model is stability in a political system such as Switzerland, which limits abuse of power and ensures a high level of stability and predictability of property rights and contracts. Switzerland’s banking institutions are exceptionally stable when compared with other rich countries. Of course, Switzerland received this designation because the yields on Swiss franc assets, particularly bonds and money market assets, were consistently lower than the gains of other currencies. Investors have demonstrated a willingness to forego a return or pay a higher price to keep their assets in Swiss francs. This investor behavior occurs because the banking system has a primary role in the money cycle and the historical facts demonstrate that this activity is economically beneficial in the case of Switzerland.

6.2. Switzerland’s Money Cycle

Whether these savings are enforcement or escape savings is the crucial distinction. There is a proportionately equal division between enforcement and escape investments of the investments. The savings that remain in the local banking system are known as enforcement savings, and the savings that are diverted away from the local economy are known as escape savings. The investments in enforcement are made by businesses that do not assume the financial roles of small ones. In this way, large corporations invest capital in manufacturing and highly specialized activities while the entire economic system is active. As a result, the entire economy operates at maximum capacity. This happens in the case of Switzerland, as the enforcement savings are much higher than the escape savings, according to Switzerland’s bank deposits per GDP in Table 1. As each economic unit finds its place, the economy’s structure is developed and suitably governed simultaneously. Alternatively, escape investments are those that take the place of small businesses, lead profits outside the economy, or divert funds for investments outside the framework of the economy. Enforcement savings and investments indicate that as money is distributed and reused more, the economy is strengthened. At that point, the money cycle has accelerated, the economy is operating at full capacity, and the economy’s structure has self-organized. Conversely, escape savings and investments result in the least amount of money being distributed and used again. According to the results of Table 5 and Figure 5, the enforcement savings and investments in the case of Switzerland are in line with the results of the high index money cycle and the general index money cycle of approximately 0.94 (with the theoretical ideal value to be 1). As a result, Switzerland has a high distribution and reuse of money, leading to an appropriate structure of the economy. The consequences of interventionism on monetary and public policy, as well as free market autoregulation, are eliminated by the money cycle.

The money cycle replaces both of the above policies with suitable regulatory public and tax policy via an appropriate banking system, which works as a receiver (more enforcement than escape savings) not as a giver (more escape than enforcement savings). An appropriate money cycle is formed by the regulatory policy that imposes higher taxes on businesses that replace the economic tasks of small ones and provides subsidies for them to invest their capital in factories and highly specialized activities. The money cycle is strengthened by the imposition of low taxes. According to the money cycle, the only taxes that have an impact on the economy, and particularly its qualitative attributes, are those related to the healthcare and education systems. As demonstrated by the economic system in which the money is saved, Switzerland’s banking system plays a critical part in the money cycle, which is essential for the distribution and reuse of money. The theory of the cycle of money holds that the economic function both reflects and identifies the state of the economy at the same time. Therefore, because all economic units are operational, the role of money—namely, its distribution and reuse—makes the structure of the economy more apparent.

6.3. Switzerland’s Specific Economic Conclusions

The cycle of money in Switzerland facilitates an excellent distribution of money. The losses of the local banks are to a low degree because an amount of money is excluded from the local financial system by worldwide transactions. The model tested in this article complies with the initial assumption of this study, demonstrating the dynamic distribution of money to Switzerland’s economy. For comparison, Switzerland’s economic system tended in recent decades to have better reuse of money within the financial system, comparing 2007–2014 and 2015–2017. The objective of this study was to define Switzerland’s general index of the cycle of money. According to the adjusted methodology, which uses mathematical and econometrical estimations, Switzerland’s economy has a perfect value above 0.5. This means that the country has a best-structured economy and appropriate distribution of money, making it equipped to face any possible economic crisis. Finally, based on the data presented in Figure 4 and Figure 5, the index of the cycle of money in Switzerland is above the worldwide average of the index, demonstrating that Switzerland’s distribution of money is at its maximum rate.

Funding

This research received no external funding.

Data Availability Statement

The data are sourced from the World Bank: https://databank.worldbank.org/source/global-financial-development/Series/GFDD.OI.02, https://data.worldbank.org/indicator/NY.GDP.PCAP.CD?locations=CH. The data are analyzed and compiled by the author.

Acknowledgments

The author wishes to thank the publishing journal, the main editor and the manuscript editors.

Conflicts of Interest

The author declares no conflicts of interest.

References

- Abdallah, Wissam, Nassib Abdallah, Marion Jean-Marie, Mohamad Oueidat, and Pierre Chauvet. 2020. A Vector Autoregressive Methodology for Short-Term Weather Forecasting: Tests for Lebanon. SpringerLink 5: 1–9. [Google Scholar] [CrossRef]

- Ainsworth, Richard Thompson, and Andrew Shact. 2014. Transfer Pricing: Un Practical Manual China. SSRN Electronic Journal 15: 1–35. [Google Scholar] [CrossRef]

- Al-Ubaydli, Omar, Min Sok Lee, John A. List, Claire L. Mackevicius, and Dana Suskind. 2021. How Can Experiments Play a Greater Role in Public Policy? Twelve Proposals from an Economic Model of Scaling. Behavioural Public Policy 5: 2–49. [Google Scholar] [CrossRef]

- Amanor-Boadu, Vincent, Peter H. Pfromm, and Richard Nelson. 2014. Economic Feasibility of Algal Biodiesel under Alternative Public Policies. Renewable Energy 67: 136–42. [Google Scholar] [CrossRef]

- Arai, Real, Katsuyuki Naito, and Tetsuo Ono. 2018. Intergenerational Policies, Public Debt, and Economic Growth: A Politico-Economic Analysis. Journal of Public Economics 166: 39–52. [Google Scholar] [CrossRef]

- Bartels, Larry M. 2005. Homer Gets a Tax Cut: Inequality and Public Policy in the American Mind. Perspectives on Politics 3: 15–31. [Google Scholar] [CrossRef]

- Boland, Lawrence A. 2014. The Methodology of Economic Model Building: Methodology after Samuelson. The Methodology of Economic Model Building: Methodology after Samuelson. London: Routledge. [Google Scholar] [CrossRef]

- Bourdin, Sébastien, and Fabien Nadou. 2018. French Tech: A New Form of Territorial Mobilization to Face up to Global Competition? Annales de Geographie 2018: 612–34. [Google Scholar] [CrossRef]

- Caldara, Dario, Matteo Iacoviello, Patrick Molligo, Andrea Prestipino, and Andrea Raffo. 2020. The Economic Effects of Trade Policy Uncertainty. Journal of Monetary Economics 109: 38–59. [Google Scholar] [CrossRef]

- Camous, Antoine, and Andrew R. Gimber. 2018. Public Debt and Fiscal Policy Traps. Journal of Economic Dynamics and Control 93: 239–59. [Google Scholar] [CrossRef]

- Castro, Edgar, and Carlos Scartascini. 2019. Imperfect Attention in Public Policy: A Field Experiment During a Tax Amnesty in Argentina. IDB Discussion Paper. New York and Washington, DC: Inter-American Development Bank. [Google Scholar]

- Challoumis, Constantinos. 2018a. Identification of Significant Economic Risks to the International Controlled Transactions. Economics and Applied Informatics 2018: 149–53. [Google Scholar] [CrossRef]

- Challoumis, Constantinos. 2018b. Methods of Controlled Transactions and the Behavior of Companies According to the Public and Tax Policy. Economics 6: 33–43. [Google Scholar] [CrossRef]

- Challoumis, Constantinos. 2018c. The Role of Risk to the International Controlled Transactions. Economics and Applied Informatics 2018: 57–64. [Google Scholar] [CrossRef]

- Challoumis, Constantinos. 2019a. The Arm’s Length Principle and the Fixed Length Principle Economic Analysis. World Scientific News 115: 207–17. [Google Scholar]

- Challoumis, Constantinos. 2019b. The Impact Factor of Education on the Public Sector and International Controlled Transactions. Complex System Research Centre 2019: 151–60. [Google Scholar]

- Challoumis, Constantinos. 2019c. The Issue of Utility of Cycle of Money. Journal Association SEPIKE 2019: 12–21. [Google Scholar]

- Challoumis, Constantinos. 2019d. The R.B.Q. (Rational, Behavioral and Quantified) Model. Ekonomika 98: 6–18. [Google Scholar] [CrossRef]

- Challoumis, Constantinos. 2019e. Theoretical Analysis of Fuzzy Logic and Q. E. Method in Economics. IKBFU’s Vestnik 2019: 59–68. [Google Scholar]

- Challoumis, Constantinos. 2020a. Impact Factor of Capital to the Economy and Tax System. Complex System Research Centre 2020: 195–200. [Google Scholar]

- Challoumis, Constantinos. 2020b. The Impact Factor of Education on the Public Sector—The Case of the U.S. International Journal of Business and Economic Sciences Applied Research 13: 69–78. [Google Scholar] [CrossRef]

- Challoumis, Constantinos. 2021a. Index of the Cycle of Money—The Case of Greece. IJBESAR International Journal of Business and Economic Sciences Applied Research 14: 58–67. [Google Scholar] [CrossRef]

- Challoumis, Constantinos. 2021b. Index of the Cycle of Money—The Case of Latvia. Economics and Culture 17: 5–12. [Google Scholar] [CrossRef]

- Challoumis, Constantinos. 2021c. Index of the Cycle of Money—The Case of Thailand. Chiang Mai University Journal of Economics 25: 1–14. [Google Scholar]

- Challoumis, Constantinos. 2021d. Index of the Cycle of Money—The Case of Bulgaria. Economic Alternatives 27: 225–34. [Google Scholar]

- Challoumis, Constantinos. 2021e. The Cycle of Money with and without the Enforcement Savings. Belgrade: Paksom Mathematical Institute Sanu. Niš: Complex System Research Centre. [Google Scholar]

- Challoumis, Constantinos. 2022a. Conditions of the CM (Cycle of Money). In Social and Economic Studies within the Framework of Emerging Global Developments. Edited by Muhammed Veysel Kaya. New York: Peter Lang, vol. 1, pp. 13–24. [Google Scholar] [CrossRef]

- Challoumis, Constantinos. 2022b. Impact Factor of the Rest Rewarding Taxes. Belgrade: Paksom Mathematical Institute Sanu. Niš: Complex System Research Centre. [Google Scholar]

- Challoumis, Constantinos. 2022c. Index of the Cycle of Money—the Case of Poland. Research Papers in Economics and Finance 6: 72–86. [Google Scholar] [CrossRef]

- Challoumis, Constantinos. 2023a. A Comparison of the Velocities of Minimum Escaped Savings and Financial Liquidity. In Social and Economic Studies within the Framework of Emerging Global Developments. Edited by Muhammed Veysel Kaya. New York: Peter Lang, vol. 4, pp. 41–56. [Google Scholar] [CrossRef]

- Challoumis, Constantinos. 2023b. Capital and Risk in the Tax System. Niš: Complex System Research Centre, pp. 241–44. [Google Scholar]

- Challoumis, Constantinos. 2023c. Currency Rate of the CM (Cycle of Money). Research Papers in Economics and Finance 7: 48–66. [Google Scholar] [CrossRef]

- Challoumis, Constantinos. 2023d. From savings to escape and enforcement savings. Cogito XV: 206–16. [Google Scholar]

- Challoumis, Constantinos. 2023e. Impact Factor of Liability of Tax System According to the Theory of Cycle of Money. In Social and Economic Studies within the Framework of Emerging Global Developments. Edited by Muhammed Veysel Kaya. New York: Peter Lang, vol. 3, pp. 31–42. [Google Scholar] [CrossRef]

- Challoumis, Constantinos. 2023f. Risk on the Tax System of the E.U. from 2016 to 2022. Economics 11: 55–72. [Google Scholar] [CrossRef]

- Challoumis, Constantinos. 2023g. Utility of Cycle of Money without the Escaping Savings (Protection of the Economy). In Social and Economic Studies within the Framework of Emerging Global Developments. Edited by Muhammed Veysel Kaya. New York: Peter Lang, vol. 2, pp. 53–64. [Google Scholar] [CrossRef]

- Challoumis, Constantinos. 2024a. Rewarding Taxes on the Cycle of Money. In Social and Economic Studies within the Framework of Emerging Global Developments. Berlin: Peter Lang GmbH, vol. 5. [Google Scholar]

- Challoumis, Constantinos. 2024b. The Inflation According to the Cycle of Money (C.M.). In Economic Alternatives. Sofia: University of International and World Economy. [Google Scholar]

- CYSTAT. 2018. H Ευρωπαϊκή Oικονομία Aπό Την Aρχή Της Χιλιετίας—ΕΝA ΣΤAΤΙΣΤΙΚO ΠOΡΤΡΕΤO. Available online: https://library.cystat.gov.cy/Documents/Publication/European_Economy_Digital-2018-EL.pdf (accessed on 9 December 2023). (In Greek)

- Driver, Ciaran. 2017. Advertising’s Elusive Economic Rationale: Public Policy and Taxation. Journal of Economic Surveys 31: 1–16. [Google Scholar] [CrossRef]

- Dybowski, T. Philipp, and Philipp Adämmer. 2018. The Economic Effects of U.S. Presidential Tax Communication: Evidence from a Correlated Topic Model. European Journal of Political Economy 55: 511–25. [Google Scholar] [CrossRef]

- Ewert, Benjamin, Kathrin Loer, and Eva Thomann. 2021. Beyond Nudge: Advancing the State-of-the-Art of Behavioural Public Policy and Administration. Policy and Politics 49: 3–23. [Google Scholar] [CrossRef]

- Feinschreiber, Robert. 2004. Transfer Pricing Methods, An Applications Guide. Hoboken: John Wiley & Sons, Inc. [Google Scholar]

- Fotis Karadimakis. 2019. H Πολιτική Της Υπεράκτιας Χρηματοδότησης Στην Ελβετία. Available online: https://dspace.lib.uom.gr/bitstream/2159/23547/5/KaradimakisPhotisMsc2019.pdf (accessed on 3 December 2023). (In Greek).

- Gihman, I. I., and A. V. Skorohod. 1972. The Solution of Stochastic Differential Equations. In Stochastic Differential Equations. Berlin: Springer. [Google Scholar] [CrossRef]

- Hampton, Mark B. 2016. Where Currents Meet: The Offshore Interface between Corruptions and Offshore Finance Centre and Economic Development. Journal Bulleton 27: 78–87. [Google Scholar] [CrossRef]

- Holcombe, Randall G. 1998. Tax Policy from a Public Choice Perspective. National Tax Journal 51: 359–71. [Google Scholar] [CrossRef]