Abstract

This study investigates the impact of firm-level investor sentiment derived from Twitter and news media on herding behavior among contributors on Estimize, a leading platform for crowdsourced earnings forecasts. The findings show that sentiment gleaned from tweets and news media content positively influences herding among Estimize contributors. Notably, herding intensifies when Twitter and news sentiment polarities align, while divergent sentiment polarities diminish this herding effect. Additionally, the analysis indicates that firms with investment-grade ratings and those characterized by low valuation uncertainty are particularly prone to sentiment-driven herding. Importantly, positive sentiment is identified as having a more potent influence on herding behavior than negative sentiment. By focusing on Estimize contributors, this study offers insights into how firm-level sentiment cues shape the crowd’s herding behavior, offering new perspectives on how different media sources shape the wisdom of the crowd.

Similar content being viewed by others

1 Introduction

Recent advancements in financial technology have led to the development of platforms that enable the crowdsourcing of earnings estimates. Studies, notably Jame et al. (2016), demonstrate that crowdsourced estimates typically surpass Wall Street analysts’ forecasts in terms of accuracy, exhibiting lower bias and greater timeliness, thereby reflecting market expectations more accurately. This enhanced performance corroborates the law of large numbers, suggesting that group consensus provides a more precise representation of market forecasts than individual predictions.

However, alongside these advantages, the proliferation of crowdsourcing platforms introduces the potential for herding within the crowd’s forecasts. Herding manifests when these estimates become excessively aligned with the prevailing consensus, introducing systemic bias. The growing dependence on social media as a source of financial information can further exacerbate this risk. For example, 71% of Twitter users obtain news through the platform (Shearer & Eva-Matsa 2018), and 63% of investors incorporate social media content into their decision-making processes (Greenwich 2019). This trend is particularly concerning considering retail investors’ vulnerability to emotional biases, as documented by Chou and Wang (2011) and Nofsinger and Sias (1999).

Moreover, it is well documented that increasing market-level sentiment induces a more optimistic outlook among Wall Street analysts, resulting in less accurate forecasts (Walther & Willis 2013). This optimism can also contribute to herding behavior among analysts, as noted in studies by Blasco et al. (2018), Chian and Lin (2019), and Kaplanski and Levy (2017). While the influence of firm-level sentiment on Wall Street analysts’ forecasts has been established (Garica 2021), the effect of firm-level sentiment on crowdsourced forecasting remains largely uncharted. A comprehensive understanding of this influence is critical as it could offer valuable insights into the decision-making processes of a broader range of market participants, extending beyond the confines of Wall Street analysts.

This study addresses this critical gap in the literature by investigating the influence of firm-level investor sentiment derived from Twitter and news media on herding behavior among contributors on Estimize, a prominent platform for crowdsourced earnings forecasts. Prior research has primarily focused on the impact of investor sentiment on various market outcomes such as stock returns (Baker & Wurgler 2006), stock liquidity (Dunham & Garcia 2020), earnings surprises (Chen et al. 2014), and financial distress (Dunham & Garcia 2021). However, the effect of firm-level sentiment on crowdsourced non-professional earnings forecasts has not yet been examined. Building on Garcia’s (2021) work, this study examines the relationship between investor sentiment, gleaned from news and Twitter media content, and herding in crowdsourced earnings forecasts, focusing on Estimize contributors. Considering that crowdsourced estimates have the potential to surpass the accuracy of professional forecasts when independent (Jame et al. 2016), it is imperative to understand the impact of firm-level sentiment on the crowd’s forecast. Their heightened sensitivity to data poses a risk to the reliability of their forecasts, as external sentiment can impair independent judgment and lead to herding, thereby potentially reducing the accuracy of these forecasts.

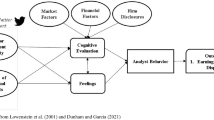

Kahneman (2003) highlights the prevalence of bounded rationality, in which forecasters rely on heuristics and treat sentiment as an important informational cue. This reliance aligns with the ‘affect heuristic’ described by Slovic et al. (2007), where positive sentiment fosters instinctive optimism, impacting judgment and leading to herding behavior, as supported by De Bondt et al. (2008). Further insights from Qin (2015) emphasize how regret influences financial decisions, complemented by Brown et al. (2008), who demonstrate the impact of social interaction on financial choices through regret aversion. These theories suggest that crowdsourced forecasters, comprised primarily of non-professional contributors and susceptible to overconfidence and limited attention spans (Barber & Odean, 2008), may rely on sentiment signals from social media to align with consensus estimates, thereby minimizing regret. The immediacy and unfiltered nature of Twitter content can elicit stronger emotional responses and a confirmation bias toward positive tweets (Nickerson 1998), particularly in complex forecasting tasks where reliance on heuristics and biases is more pronounced (Griffin & Tversky 1992).

Building upon this, confirmation bias, as documented by Nickerson (1998), can lead to a pronounced echo-chamber effect. This effect can be especially pronounced when Twitter and news sentiment polarities align, amplifying existing viewpoints and encouraging herding among Estimize contributors. Rabin and Schrag (1999) suggest this can heighten overconfidence, resulting in a more potent influence. Such an alignment can also trigger an anchoring bias, akin to what Cen et al. (2013) observed in Wall Street analysts’ earnings forecasts. Conversely, when Twitter and news sentiment polarities diverge, cognitive dissonance emerges, disrupting the echo chamber and compelling forecasters to reassess the dominant sentiment. This shift can lessen the inclination toward herding, with the lesser impact of news sentiment under conflicting polarities potentially attributed to Twitter’s greater immediacy and emotional resonance, which exert a more direct influence on forecasters’ decision-making processes.

This study employs Bloomberg’s firm-level investor sentiment indicators and Estimize’s crowdsourced earnings forecasts to examine the relationship between firm-level investor sentiment derived from Twitter and news media content and the herding behavior of crowdsourced forecasters. The study reveals that firm-level sentiment positively relates to Estimize contributors’ herding, with this effect being more pronounced in investment-grade firms and those characterized by low valuation uncertainty. Notably, when Twitter and news sentiment polarities are aligned, the crowd’s herding behavior is amplified, indicative of confirmation bias. This alignment suggests that forecasters are more likely to follow the crowd when sentiment signals from different sources echo each other.

Conversely, when there is a divergence in sentiment polarity between Twitter and news sources, an inverse relationship emerges between the sentiment expressed on Twitter and the tendency for herding among Estimize contributors. Moreover, under these conditions, the influence of news sentiment markedly diminishes, indicating its reduced relevance in driving the herding behavior of Estimize contributors this finding points to cognitive dissonance as a pivotal factor in mitigating the echo chamber effect, thereby encouraging Estimize forecasters to make more independent judgments. Moreover, the analysis reveals that positive sentiment has a more significant impact on promoting herding behavior than negative sentiment, underscoring the asymmetrical influence of sentiment polarity on the crowd’s herding behavior.

These findings underscore the substantial impact of Twitter’s immediate and emotionally charged content on Estimize forecasters’ decisions, often outweighing the influence of traditional news media. This highlights the significant role of behavioral and psychological biases in shaping financial decision-making processes, particularly in the digital age, where information is rapidly disseminated and emotionally resonant. This study contributes to the literature by clarifying how firm-level sentiment influences the crowd’s herding behavior. This aligns with the ‘affect heuristic’ and confirmation bias theories, suggesting that forecasters are more responsive to sentiment that reinforces their existing beliefs. This response is amplified in scenarios where Twitter and news media sentiments align, creating an echo chamber effect that likely intensifies herd behavior and overconfidence. Conversely, when sentiment polarities diverge, they trigger cognitive dissonance, prompting forecasters to reassess dominant sentiments and reduce their herding tendencies. These insights offer valuable contributions to understanding the factors influencing the reliability and processing mechanisms of crowdsourced forecasts.

The remainder of this paper is organized as follows: Sect. 2 discusses the relevant literature and formulates the hypotheses. Section 3 details the methodology and data used to test the hypotheses. Section 4 presents the empirical findings and robustness checks. Finally, Sect. 5 offers concluding remarks.

2 Related literature and hypothesis development

The emergence of platforms, such as Estimize, has marked a significant evolution in financial forecasting. Estimize, facilitating contributions from professionals and non-professionals, is notable for providing forecasts free from typical Wall Street biases. Its over 100,000 contributors have been shown to produce more accurate, timely, and less biased estimates than traditional Wall Street analysts (Jame et al. 2016, 2017). Markets have even shown a more positive reaction to Estimize’s earnings surprises than Wall Street’s (Adebambo & Bliss 2015), highlighting the platform’s impact on financial markets.

The accuracy of crowdsourced forecasting stems from its diverse, independent contributors; however, this accuracy is threatened by herding behavior. Herding, a convergence of forecasts toward a consensus view, can lead to increased bias and reduced forecast accuracy (Olsen 1996; Prechter 2001; Jagadeesh & Kim, 2010). This is especially relevant in light of the finding that retail investors, who form a significant portion of crowdsourced forecasters, are more influenced by behavioral biases and public information than their professional counterparts (Chou & Wang 2011; Li et al. 2017; Nofsinger & Sias 1999).

Earnings estimate dispersion, a measure of forecasting disagreement, provides insights into forecaster herding. The factors influencing dispersion include firm risk, market uncertainty, and variance in analysts’ interpretations (Barron & Stuerke 1998; Diether et al. 2002; Liu & Natarajan 2012). This earnings estimate dispersion, influenced by common and idiosyncratic uncertainty, is subject to analysts’ subjective interpretation of information and sentiment (Barron et al. 1998; Ramnath et al. 2008). Decreased dispersion signals a rise in herding behavior. Dispersion hinges on (1) the firm’s intrinsic risk and overall market uncertainty, (2) uncertainty in the analysts’ information environment, and (3) variance in analysts’ interpretations (Barron et al. 1998; Liu & Natarajan 2012).

Analysts favor simple heuristic models over complex valuation methods (Bradshaw 2004). Their reliance on data decreases with rising complexity (Plumlee 2003), suggesting forces like sentiment can sway analysts (De Long et al. 1990; Kaplanski & Levy 2017). Analysts prioritize colleagues’ opinions over their own (Welch 2000), and research shows that market sentiment drives herding (Blasco et al. 2018; Chiang & Lin 2019; Kaplanski & Levy 2017). Firm-level news and tweet sentiment also increase herding behavior (Garcia 2021). Furthermore, mood correlates with optimism (Hribar & McInnis 2012; Qian 2009) and the ability to convert estimates into recommendations (Ke & Yu 2020). Furthermore, according to Walther and Willis (2013), when the overall sentiment in the market is positive, Wall Street analysts tend to have a more optimistic view, which leads to less accurate predictions. In summary, bounded rationality and social forces such as sentiment can shape analysts’ judgments.

Information from other market participants is a vital data source (Hong et al. 2004). Analysts focus on private data but often underestimate the significance of public information (Chen & Jiang 2006). Investors also make suboptimal decisions because of overconfidence in their accuracy and ability to evaluate data (Barber & Odean 1999). Moreover, investors have limited attention (Chiu et al. 2021), with greater constraints for retail and inexperienced investors (Bartov et al. 2000). Consequently, overconfidence and inattention disproportionately impact less sophisticated investors’ decisions. In summary, behavioral biases such as overconfidence and limited attention more profoundly affect unsophisticated investors.

Research documents a positive relationship between Twitter sentiment and returns, analyst revisions (Gu & Kurov 2020), and analyst ratings (Garcia 2022). Thus, social media offers valuable insights for analysts. However, tweets are unfiltered and more emotionally charged than news articles. This unchecked content can shape investors’ choices. Despite its potential benefits, social media warrants caution owing to misinformation risks.

Forecasters’ emotions should not influence their’ earnings per share (EPS) forecasts. However, sentiment in media content can influence emotions and decisions, especially amid ambiguity (Lowenstein et al. 2001). Lowenstein et al. show that individuals generate cognitive decisions and react emotionally to decision-making, and these two processes are interconnected. Henry (2008) supports the notion that communication tone and sentiment valence are related to investor decision-making. Similarly, Baker and Wurgler (2006, 2007) describe the influence of market mood on stock returns. They find that when the mood is favorable, investors respond more favorably to the news, and this relationship is amplified for firms that are more difficult to value. Further research supports this conclusion (e.g., Antweiler & Frank 2004; Chen et al. 2014; Garcia 2013).

Market sentiment can affect market participants decisions (Bollen et al. 2011; Tetlock 2007). This suggests that Twitter and news media sentiment can shape analysts’ cash flow projections, which may be anchored to a sentiment-influenced target. Kaplanski and Levy (2017) reveal a positive link between market sentiment indices and Wall Street analyst forecasts. Chiang and Lin (2019) and Blasco et al. (2018) also find that analyst herding behavior aligns with market sentiment. Market mood not only impacts analyst projections but also directly influences firm performance, affecting aspects such as future asset returns (Davis & Tama-Sweet 2012), stock returns, earnings surprises (Chen et al. 2014), share price volatility (Bollen et al. 2011), share liquidity (Dunham & Garcia 2020), financial distress (Dunham & Garcia 2021), and the probability of delisting (Gandhi et al. 2019; Mayew et al. 2015).

This study indicates that sentiment markedly influences financial markets. As Nofsinger (2005) noted, individuals often conflate their emotional state with economic or market prospects. Consequently, financial forecasters’ decisions do not always rest on objective data but rather reflect emotional biases potentially shaped by prevailing investor sentiment. This highlights the need to interpret the crowd’s forecasts cautiously, as they may exhibit sentiment-driven emotional biases rather than pure factual analysis.

2.1 Hypotheses

The first hypothesis postulates a positive relationship between firm-level investor sentiment and herding among Estimize contributors. This aligns with research linking sentiment to market participants’ decisions and market outcomes.

Prior research shows that investor sentiment, shaped by emotional biases, significantly impacts judgment and choice (Baker & Wurgler 2006; De Long et al. 1990). Empirically, sentiment links to key market outcomes such as stock returns, trading volumes, and earnings surprises (Antweiler & Frank 2004; Chen et al. 2014), underscoring its pervasive financial market impact.

Further, substantial evidence suggests that market and investor sentiment directly influences financial analysts, particularly regarding herding and forecast revisions (Blasco et al. 2018; Brown & Cliff 2004; Chiang & Lin 2019). Individually, sentiment affects heuristic thinking, confidence, and susceptibility to social cues. Notably, these impacts are more pronounced among amateur than professional forecasters (Barber & Odean 1999; De Bondt et al. 2008; Nofsinger 2005).

Given this empirical and theoretical foundation, the first hypothesis (H1) posits a positive relationship between firm-level investor sentiment and herding among Estimize forecasters.

H1

Investor sentiment from Twitter and news media positively relates to crowdsourced forecaster herding.

There is a debate over whether news or tweets influence forecaster behavior more strongly. On one hand, news offers more credibility than tweets (Schmierbach & Oeldorf-Hirsch 2012). On the other hand, tweets reach audiences faster without undergoing the same fact-checking. Additionally, only 41% believed that news reporting was accurate and fair (Brenan 2019), indicating that while news may be more reliable, tweets’ immediacy and reach could also wield their influence.

Individuals also value early information, even if it is unreliable (Tversky & Kahneman 1974). This tendency suggests that Twitter’s rapid updates may sway forecasters more than slower deliberate news. Supporting this idea, Baird (2020) demonstrated that Wall Street analysts tend to interpret new information with excessive optimism. Additionally, research by Vosoughi et al. (2018) reveals that false tweets capture more attention and disseminate more rapidly than truthful ones, potentially magnifying Twitter’s anchoring effect. This phenomenon underscores the influential role of social media in shaping perceptions and decisions in the financial markets.

Beyond speed and anchoring, studies show that social media leads the information dissemination process, with news providing little new data (Nikkinen & Peltomaki 2019). People focus more on salience than accuracy (Subrahmanyam & Sorescu 2006), making Twitter’s straightforward content more impactful. Research also suggests a greater appeal for easily processed information (Song & Schwarz 2008). In addition, the simplicity of tweets outweighs that of complex news. With investors increasingly turning to social media, often disregarding source credibility (Kaduous et al. 2017), variable accuracy and potential misinformation have become concerns. Consequently, overreliance on Twitter versus traditional news could mislead forecasters.

Considering Twitter’s rapid dissemination compared to news and its potent, unfiltered nature, tweet sentiment may have a greater influence than news. Therefore, the second hypothesis (H2) is as follows:

H2

The influence of firm-level investor sentiment from tweets on crowdsourced forecaster herding exceeds that of news sentiment.

Extensive research highlights the asymmetrical impact of negative sentiment on investor behavior and market outcomes compared with positive sentiment (Agrawal et al. 2018; Engle & Ng 1993). Negative emotions and perceptions exert a greater influence on risk assessments, trading, and volatility, underscoring heightened sensitivity to adverse cues (Loughran & McDonald 2011; Ozik & Sadka 2012). Neuroscience corroborates this, demonstrating greater brain activity in response to negative news and events, reflecting deeper cognitive and emotional processing (Tetlock 2011).

This suggests that market participants are more attuned to and impacted by negative sentiment, potentially eliciting more pronounced forecasting reactions. Drawing on these insights, the third hypothesis (H3) posits that negative investor sentiment more strongly influences Estimize forecaster herding than positive sentiment.

H3

Negative firm-level investor sentiment from Twitter and news more strongly relates with crowdsourced forecaster herding than positive sentiment.

In summary, the literature underscores the complex interaction between investor sentiment and earnings forecasts, particularly on crowdsourced platforms. It sets the context for investigating the influence of firm-level investor sentiment on herding behavior among Estimize forecasters.

3 Methods

Multiple ordinary least squares (OLS) regression models were employed to analyze the impact of firm-level investor sentiment, derived from tweets and news media content, on crowdsourced forecaster herding. The primary specification is as follows:

where Herdingi,t is a measure of the Estimize forecasters herding for firm i on day t; InvSENTi,t-k, the variables of interest, are measures of investor sentiment relating to firm i on day t − 1 through t–k; Xi,t–1 is a vector of firm-specific control variables for firm i on day t–1; MktSENT indicates market-level sentiment measures at quarter t–1. The regressions also control for the firm’s industry. Furthermore, to control for the well-documented ‘day-of-the-week’ effect (Rystron & Benson 1989), which influences stock returns, volatility, analysts’ information environments, and investor attention (DellaVigna & Pollet 2009), the day of the week is included as a control variable.

Following prior research on the impact of market sentiment on analyst herding (Brown & Cliff 2004; Chiang & Lin 2019; Garcia 2021; Kaplanski & Levy 2017), lagged sentiment measures were used. The optimal number of daily sentiment lags was determined experimentally by incrementally adding lags to the control model until the model fit ceased to improve per the Akaike Information Criterion (AIC). One lag was optimal for both Twitter and news sentiment.

3.1 Data and sample

This study utilized earnings estimates from all Estimize forecasters, including professionals and non-professionals. This inclusive approach aligns with Hong et al. (2000), who underscore the importance of diverse perspectives in thoroughly understanding market behavior. This approach stands in contrast to Garcia’s (2021) research, which limited its focus to forecasts made by professional analysts only. Including non-professionals offers more nuanced insights into how investor sentiment shapes crowdsourced earnings predictions. Comprehensively capturing diverse market perceptions is crucial for a detailed and representative understanding of the factors influencing the crowds’ forecast.

Moreover, analyzing data from professionals and non-professionals provides a holistic view of the crowd. As Barber and Odean (2008) note, this complete view is vital for understanding investor behavior comprehensively. Additionally, since Estimize categorizes contributors based on self-reported data, interpreting these data carefully is prudent given the validation challenges (Dechow et al. 2010). Hence, segregating the sample based on potentially unreliable self-reported status could compromise the reliability of the analysis. The inclusive approach employed in this study mitigated this concern.

Daily firm-level EPS forecasts were acquired 15 days before each firm’s quarterly earnings announcement.Footnote 1 Market data were sourced from Bloomberg. The herding of crowdsourced forecasters is measured using the commonly employed EPS forecast dispersion metric (Barron & Stuerke 1998; Diether et al. 2002; Ramnath et al. 2008). Specifically, the crowdsourced forecaster herding metric is determined by dividing the standard deviation of the Estimize forecasters’ daily mean EPS by the absolute value of the crowdsourced average daily mean EPS estimateFootnote 2 for firm i on day t.

Following recent research, this study utilized Bloomberg’s sophisticated, firm-specific daily investor sentiment measures derived from tweets and news as a sentiment proxy (Behrendt & Schmidt 2018; Dunham & Garcia 2020, 2021; Garcia 2021, 2022; Gu & Kurov 2020). Bloomberg employs advanced algorithms that mimic human experts in processing text to assign tweets and news about each firm’s daily sentiment scores from -1 (highly negative) to + 1 (highly positive). Individual scores were aggregated into overall daily company-level sentiment ratings and positive, negative, and neutral volumes (Cui et al. 2016).

3.2 Factors affecting forecaster herding

As controls, this study includes firm-level variables assessing a firm’s intrinsic risk, uncertainty, and differences in opinion (Liu & Natarajan 2012), representing the variance in analysts’ EPS prediction dispersion. A company’s market value is intrinsic risk control (Bhushan 1989; Diether et al. 2002). The company’s beta (Diether et al. 2002; Liu & Natarajan 2012) and Bloomberg’s one-year default probabilityFootnote 3 serve as controls for the inherent risk. Conrad et al. (2006) report that analysts react to big price shocks; hence, I include the absolute value of the previous five-day returnsFootnote 4 and a dummy variable indicating whether the five-day return is negative. Avramo et al. (2009) showed a link between analysts’ prediction dispersion and financial hardship, documenting that credit risk information captures information about a company’s uncertain future profitability. As a result, the one-year Bloomberg default probability is included as a control.

The count of Estimize forecasters and daily share trading volumeFootnote 5 were used to measure the analysts’ information environment. Chae (2005) documents that trading volume can be a useful proxy for information asymmetry, whereby it is negatively related to information asymmetry. Hirsleifer et al. (2009) argue that trading volume can be a proxy for investor attention; thus, it is included as a control. Diether et al. (2002) showed that dispersion is positively related to earnings variability, share prices, standard deviations, and beta. The following measures capture uncertainty in the analysts’ information environment: the change in the quarterly EPS from the previous year, an indicator variable for firms reporting a quarterly loss, an indicator variable for firms that invest in R&D, and the standard deviation of the share price (Liu & Natarajan 2012).

A firm’s financial leverage is also a determinant of uncertainty in analysts’ information environment (Liu & Natarajan 2012); consequently, the firm’s Bloomberg one-year default probability is included as a proxy for financial leverage. Consistent with Liu and Natarajan, the natural log of the absolute mean of Estimize forecasters’ EPS forecast is included to control for firms with high earnings forecasts that may have higher levels of EPS forecast dispersion.

It is important to acknowledge that valuation methodologies differ by industry (Barker 1999; Demirakos et al. 2004). Consequently, the study used a company’s industry’s Global Industry Categorization Standard (GICS) classification as a control. In addition, the study used a dummy variable to identify companies with high price-to-earnings (PE) ratios relative to the firm’s relevant stock index.Footnote 6 Owing to the difficulties in valuing companies that disclose losses (Demirakos et al. 2004), companies with no or negative earnings over the last 12 months are classified as high PE firms. Consistent with Liu and Natarajan (2012), the regressions include the natural log of the stock price as a control for any other related omitted EPS dispersion determinants.

Furthermore, two indicators of market sentiment were included. First, I utilized Baker et al.’s (2016) Economic Policy Uncertainty Index to quantify economic policy uncertainty. The daily index values measure policy-related economic uncertainty and thus capture changes in the information environment tied to policy shifts (Nagar et al. 2019).Footnote 7 Second, the Chicago Board Options Exchange Market Volatility Index (VIX)—often regarded as an “investor fear gauge” reflecting financial market uncertainty (Whaley 2000; Mele et al. 2015)—was also included as a control variable.

3.3 Descriptive statistics

The sample comprises 791 publicly traded U.S. firms, covering 42,323 daily observations.Footnote 8 The sample period ranges from January 14, 2015, to April 29, 2021, determined by the availability of Bloomberg news and Twitter sentiment data. Furthermore, only daily observations with at least two estimated EPS forecasts were retained in the sample.Footnote 9

Panel A of Table 1 presents summary statistics for the variables, while Panel B summarizes Twitter and news sentiment data. The median sample firm had a market capitalization of $36.46 billion, 23 Estimize forecasters, a beta of 1.12, a five-day return of 0.10%, a 10-day share price volatility of 1.70%, a one-year probability of default of 0.00%, and a VIX of 16.57. Panel B summarizes the sentiment measures, with mean (median) Twitter and news sentiment values of 0.023 (0.008) and 0.1125 (0.063), respectively, indicating that investor sentiment scores derived from news articles are more favorable than those derived from Twitter sentiment. The bottom panel of Panel B shows that the average firm generated 290 tweets and 45 news articles daily, with substantial variability among firms.

Panel B also indicates that the sentiment polarity for Twitter and news is positively biased, with the percentages of the total observations with positive sentiment polarity for Twitter and news being 60.8 and 62.0%, respectively. Panel C presents the summary statistics by the firm’s credit quality. Bondioli et al. (2021) define investment-grade firms as those with a one-year default probability of less than 0.52%. The summary statistics indicate that below-investment-grade firms generally have fewer forecasters, lower mean earnings forecasts, market capitalizations, share prices, higher betas, five-day returns, and 10-day share price volatility than investment-grade firms. Lastly, Panel C also indicates that, on average, firms below investment grade had lower Twitter and news sentiment measures.

Table 2 presents the correlations. As predicted, Twitter and news sentiment negatively correlate with EPS dispersion (rs = − 0.03 and − 0.07). Sentiment measures (Columns 1 and 5) show low correlations with the controls. Twitter sentiment is negatively (positively) correlated with volatility and volume (5-day returns). News sentiment correlates negatively (positively) with the VIX (5-day returns). Furthermore, the Twitter and news volume variables have low correlations with dispersion (rs = − 0.08 to − 0.01). Finally, a 0.28 Twitter/news sentiment polarity correlation indicates a significant misalignment in sentiment polarity.

4 Empirical results

4.1 Primary results

Table 3 presents the pooled regression results linking the Estimize forecasters’ EPS dispersion to sentiment derived from tweets and news articles. The dependent variable is the log of EPS dispersion (plus a small constant) observed on day t for firm i. A larger EPS dispersion indicates lower herding among crowdsourced forecasters, whereas a smaller dispersion suggests higher herding. The independent variables of interest—investor sentiment derived from news articles and tweet content—and the control variablesFootnote 10 were measured on day t–1. Each regression model accounts for day- and industry-fixed effects to control for day-of-the-week and industry variations. The variance inflation factors (VIFs) were consistently below five across all models, indicating that multicollinearity is not a concern in the analysis.

Column 1 of Table 3 presents the coefficient estimates from regressing the Estimize forecasters’ EPS dispersion on the control variables. The signs of the control variables are consistent with those previously reported in the literature. Column 2 adds the lagged Twitter sentiment measure, which is negatively associated with the Estimize forecasters’ EPS dispersion (positively related to herding) and is statistically significant at the 0.01 level. Furthermore, the control variables maintain a consistent influence, significance levels, and directional signs, as in column 1.

Consistent with H2, improvements (deteriorations) in tweet sentiment are positively (negatively) related to Estimize forecasters’ herding. Moreover, the adjusted R2 improved, and the AIC decreased by including the lagged Twitter sentiment variable (column 2), indicating a better-fitting model than the control model (column 1). An F-testFootnote 11 comparing the model inclusive of the lagged tweet sentiment measures (column 2) to the control model (column 1) indicated that the model inclusive of Twitter sentiment was a statistically better-fitting model (F = 198.22, p < 0.01).

In column 3 of Table 3, the regression includes the news sentiment measure, which shows a significant positive relationship with herding (p < 0.01). Compared to the control model in column 1, the model in column 3 demonstrates an enhanced fit: the adjusted R2 is higher, and the AIC is lower. An F-test further confirms the superior fit of this model over the control model, with a statistically significant result (F = 382.54, p < 0.01).

The results in columns 2 and 3 of Table 3 demonstrate that tweet and news sentiment positively relate to crowdsourced forecaster herding. Specifically, column 4 provides a detailed analysis of the synergistic impact of Twitter and news sentiment on Estimize forecasters’ EPS dispersion. The findings reveal that news and Twitter sentiment continue to exhibit a negative relationship with crowdsourced forecaster EPS dispersion, which translates to a positive relationship with herding. This suggests that sentiment increases (or decreases) are associated with greater (or lesser) herding among Estimize forecasters. These results support H1, indicating a positive link between firm-level investor sentiment and crowdsourced forecaster herding.

Next, this study investigates the potential amplification of firm-level sentiment’s influence on crowdsourced forecasting herding when news and Twitter sentiment polarities align. If the polarities of the sentiment signals produced from tweets and news articles are consistent, they may reinforce each other and increase the total intensity of the sentiment signals. Consequently, I posit that consistent sentiment polarities amplify the impact of sentiment dynamics on the herding behavior of crowdsourced forecasters. To test this conjecture, in column 5, I calculate the regression estimates with the control variables, lagged Twitter, news sentiment measures, and a dummy variable indicating when the lagged Twitter and news sentiment measures have the same sentiment polarity (set to 1 if they have the same polarity and 0 otherwise), and the interaction between the sentiment measures and the same polarity dummy variable.

The analysis presented in column 5 provides compelling evidence that herding behavior among Estimize forecasters is markedly intensified when Twitter and news sentiment polarities are aligned, with statistical significance at the 0.01 level. This alignment fosters an ‘echo chamber effect,’ where congruent sentiment polarities between these sources reinforce existing viewpoints, thus amplifying herding behavior. This phenomenon is in sync with Rabin and Schrag’s (1999) insights regarding the amplification of overconfidence and mirrors the anchoring bias observed in Wall Street analysts’ earnings forecasts by Cen et al. (2013).

In contrast, when sentiment polarities between Twitter and news sources diverge, the resulting cognitive dissonance disrupts the echo-chamber effect. This divergence challenges forecasters to reassess the prevailing sentiment, reducing their tendency to engage in herding behavior. This shift toward a more critical evaluation of information, prompted by the divergence in sentiment polarities, could lead to more balanced and less biased decision-making among forecasters.

These findings underscore the significant influence of sentiment polarity alignment on forecaster behavior in the context of crowdsourced earnings forecasts. The echo chamber effect, amplified by aligned sentiments from different media sources, plays a pivotal role in shaping herding behavior. Conversely, the cognitive dissonance arising from divergent sentiment polarities mitigates this effect, encouraging a more analytical and unbiased approach to forecasting. This nuanced understanding of the interplay between media sentiment and forecaster behavior adds depth to the existing literature on behavioral finance by highlighting the critical role of psychological biases in financial decision-making processes.

The study’s analysis on the marginal impacts reveals that the alignment of Twitter and news sentiment polarities is a critical determinant in shaping forecaster herding behavior. Specifically, when these polarities align, news sentiment positively correlates with increased forecaster herding. This correlation is statistically significant at the 0.01 level, underscoring the robustness of the findings. In contrast, when sentiment polarities diverge, the influence of news sentiment on herding is not statistically significant, indicating that the positive impact of news sentiment is conditional on its alignment with Twitter sentiment.

This interdependence may be attributed to the inherent characteristics of Twitter as a communication medium. Its immediacy and ability to evoke strong emotional responses likely exert a more direct and potent effect on forecasters’ decision-making processes. Consequently, the initial information, often sourced from Twitter, tends to act as an anchoring point, reducing the relative impact of subsequent news sentiment. Therefore, the alignment of sentiment with Twitter is crucial to the influence of news sentiment on herding behavior among forecasters.

Regarding Twitter sentiment, the analysis uncovered diverse patterns contingent on its alignment with news sentiment. When sentiments are aligned, Twitter sentiment negatively relates to Estimize forecasters’ EPS dispersion, suggesting a positive relationship with herding. This finding is statistically significant at the 0.01 level and is marked by a substantial 68.2% increase in the magnitude of impact. In contrast, when sentiments are misaligned, there is a positive relationship between Twitter sentiment and EPS dispersion, implying a reduction in herding behavior. By demonstrating the conditional nature of news sentiment’s influence and the distinct patterns of Twitter sentiment’s impact, this study makes a significant contribution, particularly to understanding how sentiment from media content influences Estimize forecasters’ herding behavior.

Moreover, incorporating a polarity alignment dummy variable and interaction terms in column 5 enhances the model’s fit compared with the reduced model in column 4. This improvement is evidenced by an increased adjusted R2 and decreased AIC in column 5. An F-test confirms this model’s superiority (F = 67.15, p < 0.01), reinforcing the hypothesis that investor sentiment from news articles is positively related to earnings forecast herding. Nonetheless, the influence of Twitter sentiment on herding varies based on its alignment with news sentiment polarity.

What factors may contribute to the contrasting influences of tweet sentiment on crowdsourced forecaster herding? The differing impacts of tweet sentiment on crowdsourced forecaster herding can be attributed to the alignment, or lack thereof, with news sentiment. When tweet and news sentiment do not align, this discrepancy may cast doubt on the reliability of Twitter content. Such misalignment could suggest that Twitter content is either fake or biased, especially if traditional news media does not support it. This creates a more noisy informational environment and increases the cognitive load on forecasters, potentially leading to a greater dispersion in EPS estimates and, hence, a decrease in herding.

Conversely, when Twitter and news sentiments are aligned, it is likely to enhance the perceived trustworthiness and relevance of information on Twitter. Forecasters may find this information easier to process, which is consistent with Fiske and Taylor’s (2013) suggestion. This clearer and more coherent information environment can also amplify confirmation bias, leading to less variance in EPS estimates and increased herding. The reliance on congruence with traditional news as a proxy for Twitter information accuracy underscores the importance of source alignment in influencing the perceived credibility of online content.

Previous research indicates that news contributes to asymmetrical influences on stock market volatility, with negative news frequently having a more pronounced impact than positive news (Engle & Ng 1993). Column 6 explores the influences of negative and positive sentiments on crowdsourced forecaster herding, incorporating the daily counts of both negative and positive news articles and tweets. The findings here align with those in column 5. Controlling for these additional variables, the influence of Twitter and news sentiment on crowdsourced forecaster ratings remains consistent, retaining the same direction and significance as previously observed.

Notably, negative and positive tweets positively relate to the EPS estimate dispersion, although these relationships are not statistically significant. In contrast, the counts of negative and positive news articles exhibit a negative relation with EPS dispersion (indicating a positive relation to herding), with only the positive news article counts reaching statistical significance. Moreover, including daily counts of negative and positive tweets and news articles enhances the model’s fit, as evidenced by an improved adjusted R2 and reduced AIC compared to the model in column 5. An F-test further confirms the superior fit of the comprehensive model in column 6 over the reduced model (F = 84.75, p < 0.01),Footnote 12 providing additional statistical validation for these findings.

This study establishes a pivotal connection between sentiment derived from news and Twitter media and herding behaviors observed in crowdsourced earnings forecasts. This relationship is illuminated when interpreted through the lens of psychological and behavioral theories that influence decision-making. Kahneman’s 2003 research, highlighting bounded rationality, suggests that forecasters often rely on heuristics, treating sentiment as a critical informational cue. This reliance is exemplified by the ‘affect heuristic,’ as identified by Slovic et al. (2007), wherein positive sentiment promotes instinctual optimism, thereby influencing judgment. These predispositions lead to herding behavior, characterized by forecasters aligning with consensus estimates swayed by dominant sentiment, in line with De Bondt et al.’s 2008 insights.

This study’s findings also resonate with the principles of regret theory, as articulated by Loomes and Sugden (1982). This theory posits that individuals’ choices are often influenced by potential outcomes and the anticipated regret associated with these decisions. In scenarios fraught with uncertainty, the potential regret of foregoing a superior alternative choice significantly affects current decision-making. This concept is echoed in Qin’s 2015 research, which underscores the substantial influence of regret on financial decisions. Complementing this, Brown et al. (2008) shed light on the role of social interactions in financial decisions, primarily through the lens of regret aversion. It appears that crowdsourced forecasters strategically utilize sentiment signals from media content to align with consensus estimates, thereby attempting to mitigate the discomfort associated with regret from incorrect predictions. Hence, the tendency for herding among forecasters can be partly attributed to the psychological influence of sentiment disseminated through various media platforms, highlighting the role of regret aversion in their decision-making process.

Twitter content’s immediacy and unfiltered nature markedly enhance emotional reactions, resulting in a more pronounced impact on Estimize contributor herding behaviors than traditional news outlets. Leveraging insights from Kahneman’s (2003) groundbreaking work on cognitive biases and decision-making, it becomes evident that Twitter’s structure is inherently suited to magnifying user emotional engagement. Kahneman’s delineation of System 1 and System 2 thinking processes—where System 1 operates on a fast, instinctual, and emotional level in contrast to the slower, more analytical, and logical System 2—illuminates the mechanisms through which Twitter’s brief and immediate messaging format can amplify emotional responses. This platform design predominantly triggers quick and impulsive reactions characteristic of System 1 processing, thereby intensifying the likelihood and depth of emotional engagement. Specifically, the tendency of positive tweets to trigger confirmation bias, as discussed by Nickerson (1998), profoundly influences user sentiment more than traditional news sources do. This effect is particularly accentuated among crowdsourced forecasters, who, as Barber and Odean (2008) detailed, often exhibit overconfidence and suffer from limited attention spans, making them more susceptible to such biases.

Building on Baird’s (2020) insights into the optimistic bias of Wall Street analysts toward information processing, this study unveils a significant finding: Twitter sentiment exerts a stronger influence on herding behavior among crowdsourced forecasters than news sentiment. This impact is further amplified in complex forecasting scenarios, where forecasters’ reliance on heuristic shortcuts and their vulnerability to confirmation bias, echoing the seminal observations made by Griffin and Tversky (1992), are markedly heightened. Consequently, the herding behavior observed among non-professional forecasters can be attributed to a confluence of factors: bounded rationality, emotional reactions, and a predilection for confirmation bias. These factors manifest in an exaggerated response to new information on Twitter and a preference for social cues over rigorous analytical evaluations.

Interestingly, the analysis reveals a nuanced dynamic: investor sentiment extracted from Twitter media content exerts a more significant impact on herding among Estimize contributors than news sentiment’s influence on Wall Street analysts, as Garcia (2021) documented. This divergence suggests that Wall Street analysts, who gravitate toward more credible information sources, predominantly use analytical and logical System 2 thinking when generating their forecasts. In contrast, Estimize contributors, mainly non-professionals, tend toward more instinctual and impulsive System 1 thinking in their approach to earnings forecasts.

The analysis in column 6 of Table 3 supports the hypothesis that sentiment from Twitter and news media plays a significant role in influencing the herding behavior of Estimize forecasters. However, these results do not present strong empirical evidence to validate hypothesis 2. Furthermore, the findings thus far do not align with hypothesis 3, which posits that negative investor sentiment exerts a more substantial impact on forecaster herding than positive sentiment.

4.2 Influence of sentiment polarity on crowdsourced forecaster herding

Thus far, the findings establish a link between investor sentiment gleaned from news articles and tweets and crowdsourced forecasters’ herding. Table 4 provides a detailed analysis of the marginal impact of negative and positive sentiment, gleaned from tweets and news articles, on Estimize forecaster herding. Column 1 presents the absolute values of news and Twitter sentiment, using a negative sentiment indicator for both Twitter and news (set to 1 for negative sentiment and 0 otherwise) and the interaction between this negative sentiment dummy and the absolute sentiment values. These regression results were then used to calculate the marginal impact of negative and positive sentiments derived from news and Twitter media content.

Column 1 of Table 4 reveals that positive and negative sentiments are positively related to Estimize forecasters’ herding. Notably, the impact of negative sentiment derived from news articles was not statistically significant. Furthermore, the analysis indicated that the marginal influence of positive sentiment on forecasters’ EPS dispersion for news and Twitter content is more potent than that of negative sentiment. This finding was substantiated by a t-test (p < 0.01). These findings indicate that while positive and negative Twitter sentiments positively influence crowdsourced forecaster herding, only positive sentiment from news articles shows a similar positive relation. The results further highlight that positive sentiment has a significantly more potent impact than negative sentiment, suggesting that positive sentiment predominantly drives the herding in Estimize contributor herding.

The findings of this study can be understood through the lens of optimism bias, which impacts the generation of earnings estimates. McNichols and O’Brien (1997) highlighted that individuals tasked with providing earnings estimates typically hold optimistic views of the firms they analyze. This optimism leads to a bias in which individuals are inclined to perceive information more positively. Given that Estimize contributors select the firms they forecast, it is reasonable to infer that a similar optimism bias influences their judgments. This bias likely serves as a cognitive anchor, directing their interpretation and integration of new information to be consistent with their preexisting optimistic views.

Further research demonstrates that Wall Street analysts frequently overreact to positive news and underreact to negative news, a pattern indicative of analyst optimism bias (Ramnath et al. 2008). Aligning with this tendency, this study’s findings suggest that positive sentiment exerts a more potent impact on the herding behavior of crowdsourced forecasters than negative sentiment. This phenomenon underscores the broader trend of financial forecaster behavior in markets, where positive news tends to be weighted more heavily in forecasting and decision-making processes.

This study supports the previously documented finding that Wall Street analysts often exhibit overconfidence in their private information (Friesen & Weller 2006) and frequently prioritize it over publicly available data. This tendency is mirrored in the study’s findings, where Twitter content, akin to private information due to its dissemination through social networks, has a significantly more potent impact on the herding behavior of Estimize contributors than traditional news sources. Thus, the influence of Twitter sentiment on the herding tendencies of Estimize contributors is markedly more potent than that of news sentiment.

In summary, the results presented in column 1 confirm a positive association between positive sentiment and herding behavior among crowdsourced forecasters. Contrary to hypothesis 3, which anticipated that negative sentiment would have a more pronounced impact on herding, the findings point to a more significant impact of positive sentiment.

Building on the premise that firm-specific factors influence market behavior, this study explores the impact of external determinants—namely, a firm’s credit quality—on the dynamics of sentiment-driven herding among crowdsourced forecasters. Credit quality emerges as a pivotal metric of a firm’s inherent risk and uncertainty, significantly shaping the way sentiment influences the collective behavior of Estimize forecasters. Firms with lower credit quality, marked by higher default risks, are often associated with heightened volatility, pronounced information asymmetry, and a wider dispersion in analyst forecasts, as documented by Avramov et al. (2009). This notion is further supported by Hribar and McInnis (2012), who observed that investor sentiment considerably affects the accuracy of analysts’ earnings forecasts, particularly in firms that are harder to value.

The higher risk profile associated with firms of lower credit quality may exacerbate the influence of sentiment on the propensity for herding among crowdsourced forecasters. The prevailing uncertainty within these firms poses significant challenges for forecasters in discerning essential information, potentially nudging them toward a heightened reliance on sentiment cues when revising their earnings projections. Consequently, the analysis, detailed in columns 2–3 of Table 4, investigates the relationship between sentiment and herding among investment grade and below investment grade firms, positing that a firm’s credit quality impacts the sentiment to Estimize contributor herding relationship. This exploration acknowledges the varying risk profiles, transparency concerns, and the dispersion in analysts’ forecasts, aiming to illuminate whether and how the interplay between sentiment and Estimize forecaster herding behaviors diverges across firms with differing credit qualities.

Table 4, columns 2 and 3, offers an analysis of the impact of news and Twitter sentiment on the EPS dispersion among Estimize forecasters, segmented based on the credit quality of the firms. Column 2 presents the marginal impact of sentiment on investment-grade firms, while column 3 examines its effect on below-investment-grade firms.

In the context of investment-grade firms (column 2), both positive and negative sentiment from Twitter and positive news sentiment are positively related to Estimize forecaster herding. Notably, negative news sentiment does not demonstrate a significant influence. A critical observation from these findings is that Twitter sentiment has a more pronounced impact on forecaster herding than news sentiment does, a statistically significant result. This finding supports research conducted by Nikkinen and Peltomaki (2019), which suggests that social media often leads the dissemination of information, outpacing traditional news sources that may provide limited new insights or circulate outdated information. The findings underscore the nuanced role of sentiment derived from different media sources in influencing Estimize contributors’ behavior, particularly in relation to the credit quality of firms.

Table 1, Panel C, delineates the summary statistics for below-investment-grade firms, as examined in column 3. These firms are generally smaller and more likely to be in a loss position, with higher betas and return volatility indicative of increased valuation uncertainty. The analysis in column 3 reveals that positive sentiment from both Twitter and news media content is positively associated with Estimize forecaster herding behavior in these firms. Conversely, negative sentiment, whether originating from Twitter or news media, does not show a significant impact. This phenomenon may be attributed to the elevated valuation uncertainty in these firms, leading forecasters to potentially overlook negative sentiment, perhaps due to factors such as overconfidence or limited attention span. As a result, positive sentiment appears to engender inherent optimism among forecasters, prompting them to align with consensus views and contributing to an echo chamber effect.

To summarize, the analyses presented in columns 2 and 3 of Table 4 consistently indicate a positive relationship between positive sentiment and herding behavior among Estimize contributors. This pattern is evident across firms with varying credit qualities. Notably, positive sentiment consistently emerges as a more influential factor than negative sentiment, challenging hypothesis 3 that negative sentiment has a greater impact on herding behavior. These findings provide critical insights into the dynamics of sentiment influence in Estimize contributor forecasts, particularly highlighting the predominant role of positive sentiment in shaping herding behavior among crowdsourced forecasters.

The results in Table 4, columns 2–3, indicate that the relationship between firm-level sentiment and Estimize contributor herding may be contingent on the degree of uncertainty around a firm’s valuation. Specifically, firms with low valuation uncertainty exhibit a stronger association between sentiment and herding behavior relative to those with higher uncertainty. Building on this basis, this study further investigates differences in the sentiment-herding relationship across firms, specifically comparing firms with high versus low valuation uncertainty. To examine differences across high and low valuation uncertainty firms, I utilize the high relative ratio indicator variable, previously introduced, as a proxy for valuation uncertainty, with a higher ratio indicating greater uncertainty. This ratio reflects the potential overvaluation of a firm’s shares or investor expectations of high future earnings growth. As Fama & French (1992) discussed, these growth anticipations introduce uncertainty into the valuation process, which could impact the precision of earnings forecasts. Consistent with this, Baker and Wurgler (2007) argued that high-growth or pre-profit firms are more susceptible to swings in sentiment, leading to greater volatility and systematic biases in their valuations over time. The underlying premise is that higher uncertainty in current valuations reflects a lack of credible information to gauge future profit potential accurately. This absence of concrete signals leaves more room for sentiment and biases to influence forecasters’ financial estimates.

Building on the previous analysis, Table 4, columns 4 and 5, delineates the cross-sectional results, partitioning firms into low and high relative PE ratio categories. Specifically, column 4 presents the impact of sentiment on firms with low relative PE ratios, whereas column 5 delineates its implications for firms with high relative PE ratios. This segmented analysis provides a detailed examination of how valuation uncertainty, proxied by the high relative PE ratio indicator variable, influences the association between sentiment and Estimize contributor herding across firms with differing degrees of valuation uncertainty.

Aligning with the earlier findings in Table 4, columns 2 and 3, the results in columns 4 and 5 demonstrate a persistently positive association between positive firm-level sentiment and Estimize contributor herding behavior, whether firms have low or high relative PE ratios. However, a notable distinction emerges with the finding that positive news sentiment does not exert a statistically significant impact on herding for firms with a high relative PE ratio. This outcome aligns with the preliminary insights, which established the more potent influence of positive sentiment over negative sentiment in driving Estimize forecaster herding. Notably, the analysis reveals that negative Twitter sentiment distinctly affects herding behavior exclusively in firms with low relative PE ratios without extending this significance to firms with high relative PE ratios. Furthermore, negative news sentiment does not significantly impact both firm categories. The findings highlight that positive sentiment exerts a more potent influence than negative sentiment in driving herding behavior among Estimize contributors.

This study explores the nuanced impact of Twitter and news sentiment on the herding behavior of Estimize forecasters across diverse risk environments, as presented in Table 4, columns 2–5. The analysis identifies a clear positive relationship between herding behavior and positive and negative Twitter sentiment, as well as positive news sentiment, for firms categorized as investment-grade or those with low relative PE ratios. This pattern emphasizes the substantial impact of firm-specific sentiment, derived from news and Twitter media content, on the Estimize forecaster herding behavior for lower-risk and uncertainty companies, characterized by high credit quality and low valuation uncertainty.

Conversely, the findings diverge in environments marked by higher risk and uncertainty—specifically among firms that are below investment grade and have a high relative PE ratio. In this scenario, only positive sentiments significantly sway Estimize forecasters’ herding behavior, with a notable emphasis on positive Twitter sentiment’s unique role in influencing herding among high relative PE ratio firms. This distinction suggests a pronounced tendency among Estimize contributors to gravitate toward optimistic projections, effectively discounting negative sentiments in the face of uncertainty.

This study corroborates the optimism bias in earnings forecasting, illustrating how the impact of sentiment varies based on a firm’s credit quality and valuation uncertainty. This reveals the critical role of social media sentiment, particularly from Twitter, in influencing herding behavior, overshadowing the influence of traditional news sources. The study highlights that in environments with elevated uncertainty, positive sentiment becomes a more dominant force in shaping the herding behavior of Estimize contributors.

4.3 Robustness checks

Three robustness tests were conducted to validate the main findings linking firm-level sentiment from Twitter and news media content to crowdsourced forecaster herding. The first test probed the potentially destabilizing impact of President Trump’s tweets on financial markets, a factor that could significantly influence the observed results. Research by Gjerstad et al. (2021) indicates that President Trump’s tweets are associated with increased market uncertainty, higher trading volumes, and a downturn in the U.S. stock market. In light of this, the first robustness check integrated the daily frequency of President Trump’s tweetsFootnote 13 into the main regression analysis outlined in Table 3, column 6. The findings in Table 5, column 1, remain consistent with earlier results. They revealed that when Twitter and news sentiment align, they positively influence crowdsourced forecaster herding. Conversely, when these sentiments are misaligned, Twitter sentiment inversely affects forecaster herding, whereas news sentiment continues to demonstrate a positive correlation. Notably, consistent with the notion that President Trump’s tweets contribute to market uncertainty, the daily count of Trump’s tweets shows a positive association with the dispersion in the crowd’s earnings, indicating a reduction in herding behavior, likely attributable to increased market uncertainty.

The second robustness check considers the potential impact of firm size. Even after factoring in market capitalization, as demonstrated in Table 5, column 2, the principal regression was re-run with scaled sentiment and control measures. These results align with the primary findings, confirming that Twitter and news sentiment positively influence crowdsourced forecaster herding when sentiment polarities from news and tweets are consistent. In cases of inconsistency between news and Twitter sentiment, Twitter sentiment shows an inverse relationship with forecaster herding, whereas news sentiment maintains a positive correlation.

For the third robustness check, I address the potential impact of the time window before the earnings report on the results. As shown in Table 5, column 3, I re-run the main regression using a narrower time window, focusing on observations within five days of the earnings report instead of the original 15-day period. The findings from this revised analysis are consistent with the main results, once again indicating a positive relationship between Twitter and news sentiment and crowdsourced forecaster herding.

In summary, these robustness checks lend further credibility to the study’s primary findings, demonstrating that the observed relationships between firm-level investor sentiment and forecaster herding are not driven by President Trump’s tweets, company size, or the time window chosen for analysis. Consequently, these results provide substantial empirical support for the hypothesis that investor sentiment positively influences crowdsourced forecaster herding.

4.4 Limitations and future research

While providing valuable insights into the impact of firm-level sentiment on the herding behavior of crowdsourced earnings forecasters, this study is not without its limitations. One notable constraint is the approach of aggregating forecasts from all contributors on the Estimize platform without differentiating between professional and non-professional forecasters. This aggregation method may obscure the unique forecasting behaviors and biases specific to each group. Consequently, such an approach could influence the interpretations made regarding market sentiment and investor behavior, as the distinct nuances between professional and amateur forecasters’ sentiments are not analyzed separately.

Another limitation of this study lies in its sample selection process, which was restricted to Russell 3000 firms with complete data availability. This criterion may have led to an underrepresentation of smaller, less-covered companies. Consequently, this sampling approach might limit the generalizability of the findings to the broader market, particularly where smaller firms are concerned. Additionally, the study’s reliance on Twitter and traditional news media as the primary sources for sentiment analysis may not encompass the entire spectrum of investor sentiment. Future research could expand this scope by incorporating a variety of other social media platforms, such as LinkedIn, Reddit, or specialized financial forums. This approach is likely to provide a more holistic view of the diverse sentiments prevalent among investors.

Future research should delve deeper into the intricate influence of sentiment on financial markets. A key area of focus could be the impact of extreme sentiment levels on behavioral biases, market efficiency, and asset valuation. Investigating how firm-level sentiment contributes to either exacerbating or rectifying market mispricing is particularly valuable. Additionally, examining the role of investor sentiment in shaping decision-making processes and influencing pricing models would provide further insight. Another crucial aspect to explore is the impact of misinformation or ‘fake news’ on investor sentiment, especially its implications for market forecasts and investor behaviors. Integrating these empirical studies with behavioral finance theories and market microstructure concepts could offer a more comprehensive understanding of the complex relationship between investor sentiment and market dynamics.

As noted in this study, the inability to differentiate between professional and non-professional forecasters in crowdsourced data presents a compelling avenue for future research. Future studies should address this limitation to distinctly analyze these two groups of forecasters. By doing so, researchers can gain more detailed insights into the unique behaviors and contributions of professional versus non-professional participants in crowdsourced forecasting. Additionally, integrating the findings of such analyses with behavioral finance theories and market microstructure concepts will deepen our understanding of how investor sentiment and market behavior interact. This line of research is particularly important for comprehending the influence of digital information on financial markets in today’s increasingly digitalized world.

5 Conclusion

This study establishes a relationship between the herding behavior among crowdsourced forecasters on the Estimize platform and investor sentiment derived from tweets and news articles. A key finding is that the impact of Twitter sentiment on crowdsourced forecaster herding depends on whether it aligns with news sentiment. When sentiment from Twitter and news media content align, a positive impact on herding is observed. Conversely, divergent sentiment polarities lead to an inverse effect of Twitter sentiment on herding while diminishing the influence of news sentiment. Additionally, the analysis reveals that positive sentiment from Twitter and news media content exerts a more potent influence on herding than negative sentiment.

Using Bloomberg’s firm-level Twitter and news sentiment measures, this study provides strong empirical evidence that investor sentiment from these media sources significantly impacts crowdsourced forecaster herding. However, this relationship is nuanced and varies based on the media source and sentiment alignment. Moreover, the study evaluates how these effects differ among firms with varying levels of credit quality and valuation uncertainty. It demonstrates that investment-grade firms and those with lower valuation uncertainty exhibit a heightened sensitivity to both positive and negative sentiments expressed on Twitter and positive sentiments from news media content. This suggests a broader range of sentiment receptivity among firms perceived as more stable or less risky.

Conversely, firms rated below investment grade or those with high valuation uncertainty are found to be primarily influenced by positive sentiments. This highlights an optimism bias in environments characterized by greater volatility and uncertainty, suggesting that in contexts where information is less certain, positive news has a disproportionate impact on investor behavior and forecasting herding.

The integration of psychological and behavioral theories into this study offers deeper insights. The concept of bounded rationality, as proposed by Kahneman (2003), and the affect heuristic identified by Slovic et al. (2007) resonate with the observed herding phenomenon. These theories underpin the psychological impact of the sentiment conveyed through social media. With its immediate and unfiltered content, Twitter evokes strong emotional responses, often leading to confirmation bias, especially among non-professional forecasters. This propensity is amplified in complex forecasting scenarios, where reliance on heuristics and susceptibility to confirmation bias are more pronounced.

This study makes a substantial contribution by establishing a relationship between firm-level sentiment, gleaned from Twitter and news media content, and crowdsourced forecaster herding. The findings provide a deeper understanding of the key drivers of crowdsourced herding and illuminate the varying impacts of sentiment from different media sources. These insights are critically important in an era in which financial markets increasingly rely on crowdsourced information.

This study’s implications are especially relevant considering the growing dependence of markets on crowdsourced estimates and the potential of earnings forecasters’ herding behavior to destabilize stock prices, as Xu et al. (2017) noted. Understanding these dynamics is essential for market participants, who must navigate the complexities of crowdsourced forecasting. The potential for forecaster herding to precipitate market crashes underscores the importance of this research in providing a comprehensive view of market behavior in the digital age.

By integrating psychological and behavioral theories, this study opens avenues for further exploration of the complex interactions between investor sentiment and market behavior. This study marks a significant step toward unraveling the intricacies of modern financial markets in the digital era. This paves the way for future research to build on these findings and further explore the nuanced relationships between digital sentiment, crowdsourced forecasting, and market dynamics.

Notes

Estimize forecasters have short earnings forecast horizons (Jame et al. 2016). Fifteen days is selected as the cutoff period as using the 12/31/20 reporting period, the fraction of total Estimize forecasts in the quarter reaches over 50% by 15 days prior to 12/31/20. A five-day cutoff was also used as a robustness test, leading to 62% of the cumulative total Estimize estimates being contributed by then.

The daily EPS dispersion metric was log-transformed to normalize the data. Before calculating the logarithm, I added a small constant (0.00125) to all the dispersion values because some observations had a zero standard deviation. In accordance with Liu and Nararajan (2012) and Berry (1987), I have included a constant that minimizes the sum of the absolute values of skewness and excess kurtosis. The distribution of log(DISP + constant) was relatively normal, with a total of 1.13 for the absolute values of skewness and excess kurtosis.

The Bloomberg one-year default probability was transformed by taking the square root to normalize the data. The Bloomberg one-year ahead expected default probability, a percentage between zero and one, is Bloomberg’s independent judgment of a firm’s financial health at a given time. It is a forward-looking indicator of credit risk, computed using a firm’s fundamental financial and market data. A key advantage of this measure is that it is available daily, which enables the examination of high-frequency interactions with sentiment that lower-frequency measures such as Altman’s Z-score cannot. Additionally, it incorporates timely market data, which prior research finds leads to more effective credit risk models (Hillegeist et al. 2004). Bloomberg’s default likelihood model is based on Merton’s distance-to-default measure (Merton, 1974) and other economic and statistically significant factors (Bondioli et al. 2021), and has been previously established as a valid credit risk measure (e.g., Manser 2023; Johnson et al. 2018).

The absolute value of the five-day return was log-transformed to make the data approximately normal. Since some observations had a zero return, I added a small constant (0.029) to all the values before taking the natural logarithm. I added a constant that minimized the sum of the absolute values of skewness and excess kurtosis. The resulting distribution was approximately normal, with the sum of the absolute values of skewness and excess kurtosis being 0.76.

The daily trading volume was log-transformed to make the data approximately normal.

Using the PE ratio relative to the PE ratio of the firm's relevant Bloomberg benchmark index (e.g., Standard & Poor's 500, Russell 1000, etc.), companies over the third quartile (1.575) were coded as 1. Companies with zero or negative earnings were likewise assigned the value 1. The remaining observations were coded with a zero.

The daily index values were retrieved from http://www.policyuncertainty.com/.

This study focuses on firms in the Russell 3000 Index that have complete data availability for key variables from Bloomberg and Estimize from January 2015 to April 2021 sample period. Requiring complete data improves integrity but results in excluding companies with missing observations, notably smaller and less covered firms. Although necessary for the analysis, this selection criterion creates a potential sample bias that may limit the generalizability of the findings. This limitation should be considered when interpreting the results, as the sample overweighs larger, more liquid stocks than the Russell 3000 universe.

To mitigate the effect of extreme outliers, the five-day return (before taking the absolute value), book-to-market ratio, and 10-day share price volatility measures were winsorized at the 1st and 99th percentiles, and the EPS dispersion measure was winsorized at the 99th percentile.

The controls consist of the log of the mean crowd’s forecasters’ EPS; log of total crowed forecasters covering the firm; natural log of share price; log of market capitalization; the absolute value of the five-day return; log of the daily trading volume; the beta; log of the 10-day share price volatility; square-root of the one-year Bloomberg default probability; log of the daily economic policy uncertainty measure; log of the daily VIX; and dummy variables for whether the firm reported a loss, experienced a negative five-day return, incurred R&D expense, and has a high relative PE ratio.

The covariance matrix of the regression coefficients was corrected for heteroskedasticity. All subsequent F-tests were also corrected for heteroskedasticity.

Although not reported for brevity, I also performed regressions identical to those in Table 3, column 5, but using the total counts of firm-level tweets and news articles as supplemental controls (negative, neutral, and positive counts together). These findings were comparable to those in Table 3, column 6, but the AIC was greater, suggesting that this model does not fit the data better than one that includes the negative and positive counts independently.

I express sincere appreciation to the anonymous reviewer for their valuable recommendation to incorporate an analysis of Donald Trump’s tweets as a robustness check. Data for these tweets were obtained from the Trump Twitter Archive (https://www.thetrumparchive.com/faq), covering the period from January 2015 to December 2020. The analysis is confined to days on which Donald Trump posted at least one tweet. The daily tweet volume varied considerably, ranging from a minimum of one to a maximum of 153 tweets, with a median of 14 tweets per day.

References

Adebambo, B. N., & Bliss, B. A. (2015). The Value of Crowdsourcing: Evidence from Earnings Forecasts. Working Paper, (July), 1–53.

Agrawal, S., Azar, P.D., Lo, A.W., Singh, T.: Social media: Evidence from StockTwits and Twitter. J. Portfolio Manag. 44(7), 85–95 (2018)

Antweiler, W., Frank, M.Z.: Is all that talk just noise ? The information content of Internet stock message boards. J. Financ.financ. 59(3), 1259–1294 (2004). https://doi.org/10.1111/j.1540-6261.2004.00662.x

Avramov, D., Chordia, T., Jostova, G., Philipov, A.: Dispersion in analysts’ earnings forecasts and credit rating. J. Financ. Econ.financ. Econ. 91(1), 83–101 (2009). https://doi.org/10.1016/j.jfineco.2008.02.005

Baird, P.L.: Do investors recognize biases in securities analysts’ forecasts? Rev. Financial Eco. 38(4), 623–634 (2020)