Review of Derivatives Research ( IF 0.786 ) Pub Date : 2022-10-17 , DOI: 10.1007/s11147-022-09192-0 Ziming Dong , Dan Tang , Xingchun Wang

|

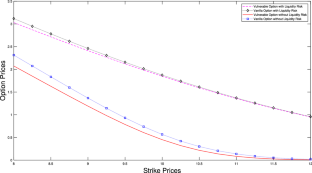

In this paper, we investigate the pricing of vulnerable basket options and basket spread options with stochastic liquidity risk. A liquidity-adjusted pricing model is used to incorporate liquidity risk in the market, and the default risk of option issuers is considered as well. An approximation method is applied to derive the closed-form approximated prices, and numerical experiments show that our approximated prices are quite accurate spanning different underlying asset numbers and alternative strike prices. Finally, we illustrate the effects of default risk and liquidity risk on the prices of basket and basket spread options numerically.

中文翻译:

为具有流动性风险的脆弱篮子价差期权定价

在本文中,我们研究了具有随机流动性风险的脆弱篮子期权和篮子价差期权的定价。流动性调整定价模型用于纳入市场流动性风险,并考虑期权发行人的违约风险。应用近似方法来推导封闭形式的近似价格,数值实验表明,我们的近似价格在不同的标的资产数量和替代执行价格上是相当准确的。最后,我们用数字说明了违约风险和流动性风险对一揽子期权和一揽子价差期权价格的影响。

京公网安备 11010802027423号

京公网安备 11010802027423号