Applied Mathematics and Optimization ( IF 1.8 ) Pub Date : 2023-10-17 , DOI: 10.1007/s00245-023-10066-6 Junkee Jeon , Jehan Oh

|

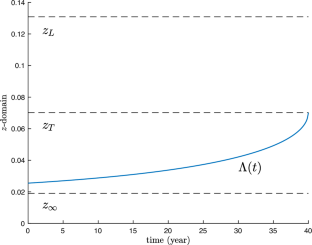

In this paper, we study the optimal consumption, investment, and life insurance problem of an economic agent who can choose a flexible labor supply and has an option to retire early with the existence of a mandatory retirement date. We model the agent’s preference as the Cobb–Douglas utility, which is a function of consumption and leisure, and consider the agent’s unit wage rate as a stochastic process. The optimization problem has a feature of combining both stochastic control and optimal stopping. To attack this problem, we adopt a dual-martingale approach and derive a dual problem, which is a finite-horizon optimal stopping problem choosing the early retirement date. Based on the partial differential equation techniques, we fully analyze the variational inequality arising from the dual problem. We show that the optimal early retirement time is characterized as the free boundary of the agent’s wealth-to-wage ratio. Finally, we establish a duality theorem and obtain an integral equation representation of optimal strategies.

中文翻译:

劳动力供应灵活性和投资组合选择以及提前退休选项

在本文中,我们研究了经济主体的最优消费、投资和人寿保险问题,该经济主体可以选择灵活的劳动力供给,并且可以选择在存在强制退休日期的情况下提前退休。我们将代理人的偏好建模为柯布-道格拉斯效用,它是消费和休闲的函数,并将代理人的单位工资率视为随机过程。优化问题具有随机控制和最优停止相结合的特点。为了解决这个问题,我们采用双鞅方法并导出一个对偶问题,这是一个选择提前退休日期的有限范围最优停止问题。基于偏微分方程技术,我们充分分析了由对偶问题引起的变分不等式。我们表明,最佳提前退休时间的特征是代理人财富与工资比率的自由边界。最后,我们建立对偶定理并获得最优策略的积分方程表示。

京公网安备 11010802027423号

京公网安备 11010802027423号