Journal of Marketing Analytics Pub Date : 2023-11-01 , DOI: 10.1057/s41270-023-00263-1 Olivier Mesly , Hareesh Mavoori

|

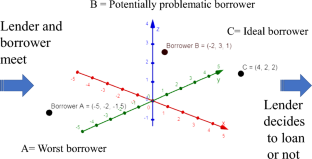

In this interdisciplinary, conceptual article with implications in marketing financial products and services, we study real estate and capital markets characterized by a predatory paradigm and economic agents’ dark financial profiles (DFPs). These are estimated by three orthogonal components—disconnection, irrationality, and deceit. We identify the best interactional patterns of borrower-lender profiles, ones that expectedly minimize the risk of default. We resort to discretized, predator–prey Lotka–Volterra equations where lenders act as predators and borrowers as prey, incorporating market trends and learning effects. To mathematically operationalize our framework, we use combinatorics with high, medium, and low levels of the three components of DFPs. We find 27 salient lender-borrower interactional scenarios and observe three different patterns: explosive, conducive, and implosive. Our theoretical findings indicate that equal (ir)rationality (in financial terms) between lenders and borrowers is a necessary but insufficient condition to maintain harmonious, long-term relationships. We use eutectic theory to map the agents’ profiles by introducing another variable: Expected return [E(Rp)] versus risk [σ], using the Capital Asset Pricing Model (CAPM) as a base. We find six market segments: the inactive predators and prey, the loose, the greedy, the vulnerable, and the stable. We identify the optimal combination of borrowers–lenders interaction under risk, given market trends and learning effects. We propose a path for future research that would see the application of analytical tools such as factor analysis, k-means clustering algorithm, χ2 and non-parametric Kruskal–Wallis and Dunn’s multiple comparison tests to verify differences among the hypothesized segments.

中文翻译:

根据借款人和贷款人的黑暗财务状况绘制他们的互动图

在这篇对金融产品和服务营销具有影响的跨学科、概念性文章中,我们研究了以掠夺性范式和经济主体的黑暗金融概况 (DFP) 为特征的房地产和资本市场。这些是通过三个正交分量来估计的——脱节、非理性和欺骗。我们确定了借款人与贷款人资料的最佳互动模式,这些模式有望最大限度地降低违约风险。我们采用离散的掠夺者-猎物 Lotka-Volterra 方程,其中贷款人充当掠夺者,借款人充当猎物,结合市场趋势和学习效果。为了在数学上操作我们的框架,我们使用 DFP 三个组成部分的高、中、低水平的组合。我们发现了 27 种显着的贷方与借款人互动场景,并观察到三种不同的模式:爆炸性、有利性和内爆性。我们的理论研究结果表明,贷款人和借款人之间的平等(非)理性(在财务方面)是维持和谐、长期关系的必要但不充分的条件。我们以资本资产定价模型 (CAPM) 作为基础,通过引入另一个变量:预期收益 [ E ( R p )]与风险 [ σ ],使用共晶理论来绘制代理人的概况。我们发现了六个细分市场:不活跃的捕食者和猎物、松散的、贪婪的、脆弱的和稳定的。考虑到市场趋势和学习效果,我们确定了风险下借款人与贷款人互动的最佳组合。我们提出了未来研究的路径,即应用因子分析、k均值聚类算法、χ 2和非参数 Kruskal–Wallis 和 Dunn 的多重比较测试等分析工具来验证假设细分之间的差异。

京公网安备 11010802027423号

京公网安备 11010802027423号